- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Programmable Money Platform Market Size, Share | CAGR 25.9%

Global Programmable Money Platform Market Size, Share, Analysis By Asset Type (Central Bank Digital Currencies (CBDCs), Stablecoins, Tokenized Bank Deposits, Tokenized Securities, Tokenized Real-World Assets, Digital Fiat Currencies), By Deployment Architecture (Public Blockchain, Private Blockchain, Consortium Blockchain, Hybrid Architecture, Cloud-Based, On-Premise), By Use Case (Cross-Border Payments, Automated Settlement, Treasury Management, Smart Contracts) Industry Trends, Market Dynamics & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 12.45 Billion | USD 98.60 Billion | 25.9% | North America, 44.5% |

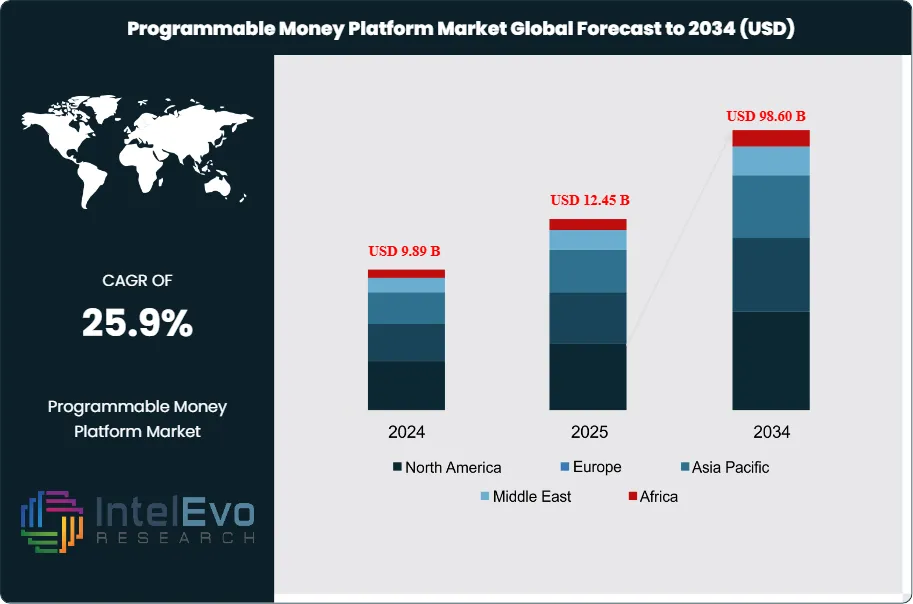

The Programmable Money Platform Market was valued at approximately USD 9.89 Billion in 2024 and reached USD 12.45 Billion in 2025. The market is projected to grow to USD 98.60 Billion by 2034, expanding at a CAGR of 25.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 86.15 Billion over the analysis period. The Programmable Money Platform Market covers enterprise infrastructure for stablecoin issuance, tokenized deposits, central bank digital currency (CBDC) rails, smart-contract-enabled settlement, and programmable payment middleware that embeds conditional logic into digital value transfer.

Get More Information about this report -

Request Free Sample ReportDemand acceleration is driven by three structural shifts. First, stablecoins settled USD 27.6 Trillion in 2024, surpassing Visa and Mastercard combined transaction volume for the first time, with total stablecoin supply crossing USD 310 Billion by mid-December 2025 per DefiLlama data. Second, the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act), signed into law by President Donald J. Trump on 18 July 2025, created the first federal regulatory framework for payment stablecoins in the United States, requiring 100% reserve backing and monthly public disclosures. Third, enterprise treasurers are pursuing programmable settlement to address the USD 4.7 Trillion trapped daily in inefficient payment processes globally.

Institutional adoption accelerated sharply in 2025. Circle Internet Group IPO'd on the New York Stock Exchange on 5 June 2025 at USD 31 per share, closing its first trading day up 168% with an initial market capitalization of USD 6.8 Billion. JPMorgan Chase's Kinexys business rolled out the JPMD USD deposit token on Coinbase's Base Layer-2 in November 2025 following a June 2025 proof-of-concept with B2C2, Coinbase, and Mastercard. Visa continued deploying its Visa Tokenized Asset Platform (VTAP) for bank stablecoin issuance, while Stripe acquired stablecoin infrastructure platform Bridge in late 2024 and launched the Tempo stablecoin-focused chain with Paradigm in 2025.

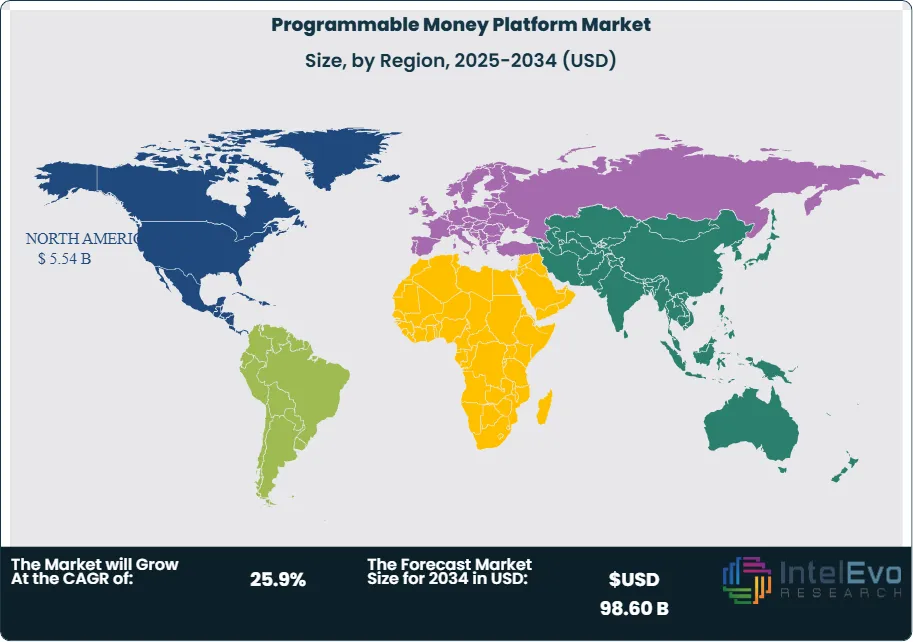

North America held 44.5% of global Programmable Money Platform Market revenue in 2025, equivalent to USD 5.54 Billion, anchored by the GENIUS Act, OCC digital asset trust guidance, and the presence of USDC, JPMD, and PYUSD issuers. The FDIC approved a proposed rulemaking in 2025 to establish GENIUS Act application procedures for insured depository institutions seeking to issue payment stablecoins through subsidiaries. Europe held 23.5% share, reflecting the Markets in Crypto-Assets (MiCA) regulation effective 30 December 2024, which structures e-money tokens (EMT) and asset-referenced tokens (ART) issuance across the 27 EU member states.

Forward visibility through 2034 rests on three catalysts. First, Citigroup's 2025 stablecoin base case projects USD 1.9 Trillion in total stablecoin issuance by 2030, with bull case reaching USD 4.0 Trillion, each scenario supporting platform infrastructure demand. Second, tokenized deposit rails led by Kinexys JPMD and bank-issued deposit tokens on Canton Network provide a regulated alternative to stablecoins under GENIUS Act Section 5 subsidiary provisions. Third, Boston Consulting Group and similar industry analyses project up to USD 10 Trillion of tokenized real-world assets by 2030, each settling on programmable money rails. These forces together underwrite the 25.9% forecast CAGR in the Programmable Money Platform Market through 2034.

Market Definition & Scope

The Programmable Money Platform Market is defined as the commercial space for enterprise infrastructure, APIs, and settlement networks that enable digital value to carry embedded logic and execute automated transactions based on predefined conditions. The market encompasses stablecoin issuance platforms (Circle USDC, Tether USDT, PayPal PYUSD), bank-issued tokenized deposit platforms (JPMorgan JPMD via Kinexys), central bank digital currency rails, smart-contract settlement networks, programmable payment middleware (Quant Flow, Stablecore), and institutional custody infrastructure (Fireblocks, Anchorage Digital, BitGo).

This analysis includes platform subscription revenue, transaction fee revenue, reserve income net of partner share, custody fees, and SaaS licenses for bank deployment of programmable money capability. The scope explicitly excludes pure speculative cryptocurrency trading volume, generic retail payment processing without programmable logic, conventional real-time gross settlement (RTGS) systems such as Fedwire or TARGET2 without smart contract capability, and speculative DeFi yield farming protocols without enterprise compliance infrastructure. The parent digital payments market is projected to reach USD 361 Billion by 2030, and the programmable money segment analyzed here represents roughly 3.5% of the parent market in 2025.

, Stablecoins, Tokenized Bank Deposits, Tokenized Securities, Tokenized Real-World Assets, Digital Fiat Currencies), By Deployment Architecture (Public Blockchain, Private Blockchain, Consortium Blockchain, Hybrid Architecture, Cloud-Based, On-Premise), By Use Case (Cross-Border Payments, Automated Settlement, Treasury Management, Smart Contracts) Industry Trends, Market Dynamics & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Programmable Money Platform Market grew from USD 12.45 Billion in 2025 to a projected USD 98.60 Billion in 2034, expanding at a 25.9% CAGR.

- Segment Dominance (By Asset Type): Fiat-backed stablecoins held 82% revenue share in 2025, anchored by Tether USDT at 60% and Circle USDC at 25% of stablecoin market capitalization.

- Segment Dominance (By Use Case): Cross-border payments and B2B settlement accounted for 41% of 2025 revenue, followed by on-chain trading collateral at 28% and institutional treasury at 15%.

- Driver: Enterprise treasury inefficiency costs up to USD 100 Million annually per organization per the 2025 Oxford Economics-FIS study, with 51% of firms citing money movement friction as the primary pain point.

- Restraint: GENIUS Act compliance requires 100% reserves in cash or short-dated U.S. Treasuries, excluding Bitcoin and gold held by Tether and forcing structural rework for non-compliant issuers targeting U.S. access.

- Opportunity: Tokenized real-world assets are projected to reach up to USD 10 Trillion by 2030, with each tokenized bond, real-estate share, or carbon credit requiring programmable settlement infrastructure.

- Trend: Bank-issued deposit tokens are emerging as the regulated alternative to public stablecoins, with JPMorgan JPMD available on Base Layer-2 since November 2025 and Canton Network from January 2026.

- Regional: North America held 44.5% revenue share in 2025 at USD 5.54 Billion, supported by GENIUS Act enactment, Circle NYSE listing, and JPMorgan Kinexys platform expansion.

Key Insights Summary

- Stablecoins settled USD 27.6 Trillion in transaction volume during 2024 per CEX.IO Stablecoin Landscape Report, surpassing the combined Visa and Mastercard transaction volume for the first time.

- Total stablecoin supply reached approximately USD 310 Billion by mid-December 2025 per DefiLlama data, up more than 50% from USD 205 Billion at the start of 2025 while the broader crypto market fell 10%.

- President Donald J. Trump signed the GENIUS Act into law on 18 July 2025, following Senate passage 68-30 on 17 June 2025 and House passage 308-122 on 17 July 2025, establishing the first U.S. federal stablecoin regulatory framework.

- Circle Internet Group IPO'd on NYSE on 5 June 2025 at USD 31 per share, raising USD 1.05 Billion on 34 million shares, with shares closing up 168% on day one and rallying to over 675% above IPO price by 20 June 2025.

- Kinexys by J.P. Morgan rolled out the JPMD USD deposit token on Coinbase Base Layer-2 in November 2025, following a June 2025 proof-of-concept with B2C2, Coinbase, and Mastercard for institutional clients.

- USDC market capitalization reached approximately USD 61 Billion at Q2 2025, capturing 25% of the stablecoin market, with Tether USDT holding 60% at approximately USD 150 Billion.

- Circle reported 2024 revenue of USD 1.68 Billion and net income of USD 156 Million, with distribution fees paid to Coinbase of USD 900 Million in 2024 representing 54% of total revenue.

Competitive Landscape Overview

The Programmable Money Platform Market is highly consolidated at the issuance layer and fragmenting at the infrastructure layer. At the stablecoin issuance layer, Tether Holdings and Circle Internet Group together hold approximately 87% of the stablecoin market, with USDT at 60% and USDC at 25% by Q2 2025. At the tokenized deposit layer, JPMorgan Kinexys leads institutional volume with USD 10 Trillion in daily payments engine throughput now linked to public chains via JPMD. At the infrastructure and middleware layer, Fireblocks, Anchorage Digital, Stablecore, and Quant Network compete for bank integration mandates.

Competitive dynamics shifted sharply in 2025 toward regulatory arbitrage and public-market access. Circle's NYSE IPO opened public-market exposure to stablecoin economics and triggered follow-on interest from Bullish and Gemini. Tether announced development of a new U.S.-based stablecoin USAT to align with GENIUS Act reserve asset restrictions that exclude Bitcoin and gold from its existing USDT reserves. Stripe's acquisition of Bridge stablecoin platform and launch of Tempo chain with Paradigm positioned the payments processor for vertically integrated programmable money. Circle announced the Arc Layer-1 blockchain dedicated to USDC activity, and Tether backed new networks including USDT-powered Stable Chain and omnichain liquidity project USDT0.

Competitive Landscape Matrix

| Company | HQ | Position | Key Platform | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Circle Internet Group, Inc. | New York, NY, USA | Leader | USDC; EURC; USYC; Cross-Chain Transfer Protocol; Arc Layer-1 | Global | NYSE IPO on 5 June 2025 at USD 31/share; unveiled Arc Layer-1 chain for USDC activity in 2025 |

| Tether Holdings Limited | El Salvador | Leader | USDT; planned USAT U.S.-compliant stablecoin | Global ex-US | Announced USAT development for GENIUS Act compliance in 2025 |

| JPMorgan Chase & Co. (Kinexys) | New York, NY, USA | Leader (Institutional) | JPMD deposit token on Base; Kinexys Digital Payments | Global | Rolled out JPMD on Coinbase Base Layer-2 in November 2025; Canton Network availability January 2026 |

| Visa Inc. | Foster City, CA, USA | Leader (Network) | Visa Tokenized Asset Platform (VTAP); USDC settlement | Global | Continued expansion of VTAP stablecoin issuance platform for banks 2025 |

| Stripe, Inc. | Dublin/San Francisco | Challenger | Bridge stablecoin platform; Tempo blockchain (with Paradigm) | Global | Acquired Bridge stablecoin infrastructure; launched Tempo stablecoin-focused chain 2025 |

| Mastercard Incorporated | Purchase, NY, USA | Leader (Network) | Multi-Token Network; USDC card settlement | Global | Partnered with JPMorgan Kinexys on JPMD settlement pilots 2025 |

| Fireblocks Ltd. | New York, NY, USA | Leader (Custody) | Institutional custody and tokenization infrastructure | Global | Continued expansion of enterprise-grade digital asset custody through 2025 |

| Anchorage Digital Bank N.A. | Sioux Falls, SD, USA | Challenger (Custody) | Regulated custody for stablecoins and deposit tokens | United States | First federally chartered digital asset bank; supporting GENIUS Act issuance |

| PayPal Holdings, Inc. | San Jose, CA, USA | Challenger | PayPal USD (PYUSD) stablecoin on Ethereum and Solana | United States | Continued PYUSD integration into consumer and B2B payments 2025 |

| Quant Network Ltd. | London, United Kingdom | Niche (Interoperability) | Quant Flow programmable money middleware | EU, UK | Continued expansion of bank middleware for tokenized deposit settlement 2025 |

Segmentation Analysis

The Programmable Money Platform Market segments across asset type, deployment architecture, use case, and end-user category. Procurement leaders building a programmable money platform procurement checklist should benchmark vendors on regulatory coverage (GENIUS Act compliance, MiCA authorization, Singapore Payment Services Act licensure), reserve transparency, smart-contract composability, and cross-chain interoperability across each segmentation dimension.

By Asset Type

Fiat-backed stablecoins led the Programmable Money Platform Market with 82% revenue share in 2025, equivalent to approximately USD 10.21 Billion. USD-pegged stablecoins represented 97% of stablecoin issuance per IMF data, with euro-denominated stablecoins the remaining minority but growing faster. Circle's EURC captured 47% of the EUR stablecoin market since MiCA took effect, illustrating the regulatory advantage of compliance-first issuance. Tether USDT and Circle USDC collectively hold approximately 87% of stablecoin market capitalization.

Tokenized bank deposits represented 11% of revenue in 2025 and are projected to grow fastest through 2034 as JPMorgan JPMD scales on Base and Canton Network. Deposit tokens differ from stablecoins in that they represent digital claims on existing bank deposits rather than external reserves, and they can be interest-bearing under GENIUS Act provisions that prohibit stablecoin issuers from directly offering interest. Crypto-backed and algorithmic stablecoins collectively held 5% share, led by MakerDAO's DAI and Ethena's USDe at approximately USD 13 Billion market cap. CBDC platforms captured 2% of revenue in 2025 through procurement contracts, despite broader pilot activity across 80+ central banks including the ECB digital euro preparation phase.

By Deployment Architecture

Public blockchain deployment led at 71% revenue share in 2025. Ethereum holds approximately 70% of stablecoin supply on-chain, with Binance Smart Chain at 14-16% and Tron concentrated in USDT circulation. USDC natively mints on 20 blockchains per Circle disclosure, enabled by Cross-Chain Transfer Protocol (CCTP). Layer-2 networks including Coinbase Base, Arbitrum, Optimism, and zkSync are absorbing incremental transaction volume due to lower fees and faster settlement. Permissioned blockchain deployment captured 22% share, led by JPMorgan Kinexys (previously Onyx) and Canton Network for institutional settlement. Hybrid architectures held 7% share and are declining as public-chain institutional adoption normalizes.

By Use Case

Cross-border payments and B2B settlement held 41% revenue share in 2025, equivalent to approximately USD 5.10 Billion. Stablecoins process USD 20 to 30 Billion in real on-chain payments per day per Visa Onchain Analytics, concentrated in remittances, supplier payments, and cross-border invoice settlement. On-chain trading collateral captured 28% of revenue, reflecting stablecoins' role as the base pair for centralized and decentralized exchange activity. Institutional treasury automation held 15%, driven by real-time liquidity management, programmatic escrow, and FX exposure automation. Remaining share split among consumer payments, merchant acceptance (Shopify, PayPal), and tokenized real-world asset settlement.

By End-User

Financial institutions held 46% revenue share in 2025, anchored by tier-one banks including JPMorgan Chase, Citigroup, Goldman Sachs, HSBC, and Deutsche Bank deploying tokenized deposit and stablecoin-adjacent infrastructure. Fintechs and payment service providers captured 27% share, led by Stripe, PayPal, Block, and Adyen integrating programmable money rails. Cryptocurrency exchanges held 15% share, with Coinbase capturing 22% of USDC supply at USD 12 Billion and Binance holding 51% of global USDC trading volume at weekly USD 24 Billion in May 2025. Corporate treasury and enterprise held 8%, with the remaining 4% split among public sector, central banks, and multilateral institutions. Programmable money ROI calculation models typically show positive ROI within 6 months and full integration within 90 days for standard enterprise deployments.

Regional Analysis

The Programmable Money Platform Market divides across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, with North America leading in 2025 and Asia Pacific growing fastest through 2034.

North America

North America held 44.5% of global Programmable Money Platform Market revenue in 2025, equivalent to USD 5.54 Billion. The United States accounted for approximately 93% of regional revenue. The GENIUS Act, signed on 18 July 2025, restricts payment stablecoin issuance to subsidiaries of insured depository institutions, nonbank institutions supervised by the Office of the Comptroller of the Currency (OCC), or state-chartered entities meeting federal standards. The FDIC approved GENIUS Act application procedures in 2025 for FDIC-supervised state nonmember banks seeking subsidiary issuance. Circle, JPMorgan Kinexys, Paxos, Anchorage Digital (the first federally chartered digital asset bank), and Fireblocks are headquartered in the region.

Europe

Europe held 23.5% share in 2025 at approximately USD 2.93 Billion, with Germany, France, the Netherlands, and the United Kingdom leading adoption. The Markets in Crypto-Assets (MiCA) Regulation, effective 30 December 2024, established a unified framework for e-money tokens and asset-referenced tokens across the 27 EU member states. Circle registered as an electronic money institution (EMI) in France in 2024 to issue USDC and EURC under MiCA. The ECB's digital euro preparation phase continues through 2025-2026, with programmable money provisions under active balance design. The UK's Financial Conduct Authority (FCA) continues parallel regulatory development with potential fiat-referenced stablecoin regime consultation through 2025.

Asia Pacific

Asia Pacific captured 18.5% share in 2025 at approximately USD 2.30 Billion and is growing fastest at 28.5% CAGR through 2034. Singapore, Hong Kong, Japan, and Australia are the primary regulatory leaders. Hong Kong's Stablecoin Ordinance, passed in May 2025, requires licensing from the Hong Kong Monetary Authority for all HKD-backed stablecoin issuers. Circle holds a Major Payment Institution license from the Monetary Authority of Singapore under the Payment Services Act framework. Japan's Financial Services Agency maintains its stablecoin licensing regime, and China's NMPA-adjacent digital yuan (e-CNY) continues cross-border pilot expansion through the mBridge project with the Bank for International Settlements.

Latin America

Latin America held 7.5% share in 2025 at approximately USD 934 Million, led by Brazil, Mexico, Argentina, and El Salvador. Tether Holdings Limited relocated its domicile to El Salvador, leveraging the country's Bitcoin legal-tender framework under the Ley Bitcoin of September 2021. Brazil's central bank Drex CBDC project continues pilot expansion through 2025, and Mexico's fintech sector is integrating stablecoin rails for remittance corridors with the United States. The Inter-American Development Bank estimates Latin America is among the fastest-growing stablecoin adoption regions globally, with individual consumer use for savings and hedging supplementing enterprise B2B deployment.

Middle East & Africa

The Middle East & Africa region held 6.0% share in 2025 at approximately USD 747 Million. The United Arab Emirates' CBUAE Payment Token Services Regulation, issued in 2024, provides licensed pathway for dirham-denominated stablecoin issuance. Saudi Arabia continues participation in the mBridge multi-CBDC project. Sub-Saharan African corridors including Nigeria, Kenya, and South Africa demonstrate strong consumer stablecoin adoption for remittances and store-of-value, with local fintechs integrating USDT and USDC on-chain rails. South Africa's SARB CBDC pilot and Ghana's e-Cedi pilot continue through 2025.

Country Analysis

The Programmable Money Platform Market concentrates in four national markets that together contribute more than 60% of 2025 global revenue: the United States, the United Kingdom, Singapore, and Germany.

United States

The United States generated approximately USD 5.15 Billion in Programmable Money Platform Market revenue in 2025 and is projected to grow at a country CAGR of 26.0% through 2034. The GENIUS Act, signed 18 July 2025 as Public Law 119-27, takes effect the earlier of 18 months after enactment or 120 days after final implementing regulations. The OCC, FDIC, and Federal Reserve share supervisory authority for federally qualified payment stablecoin issuers. President Trump signed an Executive Order on digital assets in January 2025 and established a Strategic Bitcoin Reserve and U.S. Digital Asset Stockpile by Executive Order in March 2025. The Anti-CBDC Surveillance State Act (H.R. 1919) passed the House in July 2025, restricting federal issuance of a retail central bank digital currency.

United Kingdom

The United Kingdom contributed approximately USD 685 Million in Programmable Money Platform Market revenue in 2025, growing at a country CAGR of 24.5% through 2034. The Financial Conduct Authority (FCA) published fiat-referenced stablecoin regulatory consultation papers through 2024-2025, building on the Bank of England's Real-Time Gross Settlement (RTGS) renewal program. The UK is a strategic location for Quant Network, ClearBank, and several institutional stablecoin infrastructure providers. HM Treasury maintains the Digital Securities Sandbox for tokenized securities trials. The UK's FSMA 2023 framework provides the statutory foundation for extending regulation to digital assets, with secondary legislation expected through 2026.

Singapore

Singapore generated approximately USD 435 Million in Programmable Money Platform Market revenue in 2025, with a country CAGR of 30.2% through 2034. The Monetary Authority of Singapore (MAS) operates the most mature licensed stablecoin regime globally, with Circle, Paxos, and StraitsX holding Major Payment Institution licenses. MAS Project Guardian continues institutional tokenization pilots with JPMorgan, DBS Bank, and Marketnode through 2025. Project Orchid explores retail purpose-bound money, a programmable form of Singapore-dollar-denominated digital currency. Singapore's status as Asia Pacific headquarters for multiple global stablecoin issuers reinforces its country CAGR premium.

Germany

Germany accounted for approximately USD 525 Million in Programmable Money Platform Market revenue in 2025, with a country CAGR of 24.8% through 2034. BaFin supervises German-licensed e-money token issuers under MiCA, including domestic stablecoin pilot participants. The Bundesbank's wholesale CBDC trial activities with the ECB and Banque de France continue under the Eurosystem wholesale trial program. Deutsche Bank, Commerzbank, and DZ Bank participate in institutional tokenization initiatives including the Canton Network and Fnality International. German industrial treasury operations at Siemens, SAP, and Mercedes-Benz have deployed early-stage programmable payment pilots for supplier settlement.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Asset Type

- Central Bank Digital Currencies (CBDCs)

- Stablecoins

- Tokenized Bank Deposits

- Tokenized Securities

- Tokenized Real-World Assets (RWAs)

- Digital Fiat Currencies

- Other Digital Assets

By Deployment Architecture

- Public Blockchain-Based Platforms

- Private Blockchain-Based Platforms

- Consortium / Permissioned Blockchain Platforms

- Hybrid Architecture Platforms

- Cloud-Based Platforms

- On-Premise Platforms

By Use Case

- Automated Payments & Settlement

- Cross-Border Payments

- Trade Finance & Supply Chain Finance

- Treasury & Liquidity Management

- Conditional Payments & Escrow Services

- Government Disbursements & Social Benefits

- Machine-to-Machine (M2M) Payments

- Subscription & Recurring Payments

- Digital Asset Management

- Smart Contract-Based Financial Services

By End-User

- Banks & Financial Institutions

- Central Banks & Government Agencies

- FinTech Companies

- Payment Service Providers

- Corporates & Enterprises

- Retail & E-Commerce Companies

- Telecommunications Providers

- Healthcare Organizations

- Manufacturing & Industrial Enterprises

- Others (Energy, Transportation, Logistics, Education)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 12.45 B |

| Forecast Revenue (2034) | USD 98.60 B |

| CAGR (2025-2034) | 25.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Asset Type, (Central Bank Digital Currencies (CBDCs), Stablecoins, Tokenized Bank Deposits, Tokenized Securities, Tokenized Real-World Assets (RWAs), Digital Fiat Currencies, Other Digital Assets), By Deployment Architecture, (Public Blockchain-Based Platforms, Private Blockchain-Based Platforms, Consortium / Permissioned Blockchain Platforms, Hybrid Architecture Platforms, Cloud-Based Platforms, On-Premise Platforms), By Use Case, (Automated Payments & Settlement, Cross-Border Payments, Trade Finance & Supply Chain Finance, Treasury & Liquidity Management, Conditional Payments & Escrow Services, Government Disbursements & Social Benefits, Machine-to-Machine (M2M) Payments, Subscription & Recurring Payments, Digital Asset Management, Smart Contract-Based Financial Services), By End-User, (Banks & Financial Institutions, Central Banks & Government Agencies, FinTech Companies, Payment Service Providers, Corporates & Enterprises, Retail & E-Commerce Companies, Telecommunications Providers, Healthcare Organizations, Manufacturing & Industrial Enterprises, Others (Energy, Transportation, Logistics, Education)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CIRCLE INTERNET GROUP, INC., TETHER HOLDINGS LIMITED, JPMORGAN CHASE & CO., VISA INC., STRIPE, INC., MASTERCARD INCORPORATED, FIREBLOCKS LTD., ANCHORAGE DIGITAL BANK N.A., PAYPAL HOLDINGS, INC., QUANT NETWORK LTD., PAXOS TRUST COMPANY, LLC, COINBASE GLOBAL, INC., BLOCK, INC., BITGO INC., RIPPLE LABS INC., MAKERDAO, ETHENA LABS, BASTION TECHNOLOGIES, INC., STABLECORE INC., DIGITAL ASSET HOLDINGS, LLC, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Stablecoins, Tokenized Bank Deposits, Tokenized Securities, Tokenized Real-World Assets, Digital Fiat Currencies), By Deployment Architecture (Public Blockchain, Private Blockchain, Consortium Blockchain, Hybrid Architecture, Cloud-Based, On-Premise), By Use Case (Cross-Border Payments, Automated Settlement, Treasury Management, Smart Contracts) Industry Trends, Market Dynamics & Forecast 2026-2034")

, Stablecoins, Tokenized Bank Deposits, Tokenized Securities, Tokenized Real-World Assets, Digital Fiat Currencies), By Deployment Architecture (Public Blockchain, Private Blockchain, Consortium Blockchain, Hybrid Architecture, Cloud-Based, On-Premise), By Use Case (Cross-Border Payments, Automated Settlement, Treasury Management, Smart Contracts) Industry Trends, Market Dynamics & Forecast 2026-2034")

, Stablecoins, Tokenized Bank Deposits, Tokenized Securities, Tokenized Real-World Assets, Digital Fiat Currencies), By Deployment Architecture (Public Blockchain, Private Blockchain, Consortium Blockchain, Hybrid Architecture, Cloud-Based, On-Premise), By Use Case (Cross-Border Payments, Automated Settlement, Treasury Management, Smart Contracts) Industry Trends, Market Dynamics & Forecast 2026-2034")

Frequently Asked Questions

How big is the Programmable Money Platform Market?

The Global Programmable Money Platform Market was valued at USD 9.89 Billion in 2024 and is projected to reach USD 98.60 Billion by 2034, growing at a CAGR of 25.9% from 2026 to 2034. Growth is driven by increasing adoption of CBDCs, stablecoins, tokenized assets, smart contract-based payments, real-time settlement systems, digital banking transformation, cross-border payment innovation, and the rising demand for automated, secure, and programmable financial transactions across global financial ecosystems.

Who are the major players in the Programmable Money Platform Market?

CIRCLE INTERNET GROUP, INC., TETHER HOLDINGS LIMITED, JPMORGAN CHASE & CO., VISA INC., STRIPE, INC., MASTERCARD INCORPORATED, FIREBLOCKS LTD., ANCHORAGE DIGITAL BANK N.A., PAYPAL HOLDINGS, INC., QUANT NETWORK LTD., PAXOS TRUST COMPANY, LLC, COINBASE GLOBAL, INC., BLOCK, INC., BITGO INC., RIPPLE LABS INC., MAKERDAO, ETHENA LABS, BASTION TECHNOLOGIES, INC., STABLECORE INC., DIGITAL ASSET HOLDINGS, LLC, Others

Which segments covered the Programmable Money Platform Market?

By Asset Type, (Central Bank Digital Currencies (CBDCs), Stablecoins, Tokenized Bank Deposits, Tokenized Securities, Tokenized Real-World Assets (RWAs), Digital Fiat Currencies, Other Digital Assets), By Deployment Architecture, (Public Blockchain-Based Platforms, Private Blockchain-Based Platforms, Consortium / Permissioned Blockchain Platforms, Hybrid Architecture Platforms, Cloud-Based Platforms, On-Premise Platforms), By Use Case, (Automated Payments & Settlement, Cross-Border Payments, Trade Finance & Supply Chain Finance, Treasury & Liquidity Management, Conditional Payments & Escrow Services, Government Disbursements & Social Benefits, Machine-to-Machine (M2M) Payments, Subscription & Recurring Payments, Digital Asset Management, Smart Contract-Based Financial Services), By End-User, (Banks & Financial Institutions, Central Banks & Government Agencies, FinTech Companies, Payment Service Providers, Corporates & Enterprises, Retail & E-Commerce Companies, Telecommunications Providers, Healthcare Organizations, Manufacturing & Industrial Enterprises, Others (Energy, Transportation, Logistics, Education))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Programmable Money Platform Market

Published Date : 08 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date