- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Protein Engineering Platform Market Size, Share | CAGR 15.1%

Global Protein Engineering Platform Market Size, Share & Industry Analysis By Product and Service (Instruments, Reagents and Consumables, Software and Computational Tools), By Technology Approach (Rational Protein Design, Directed Evolution, De Novo Protein Design, AI-Assisted Protein Engineering and High-Throughput Screening), By Protein Type (Monoclonal Antibodies, Enzymes, Therapeutic Proteins and Vaccines), By End-User (Pharmaceutical & Biotechnology Companies, CROs and Academic Institutes) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 3.85 Billion | USD 13.65 Billion | 15.1% | North America, 44.8% |

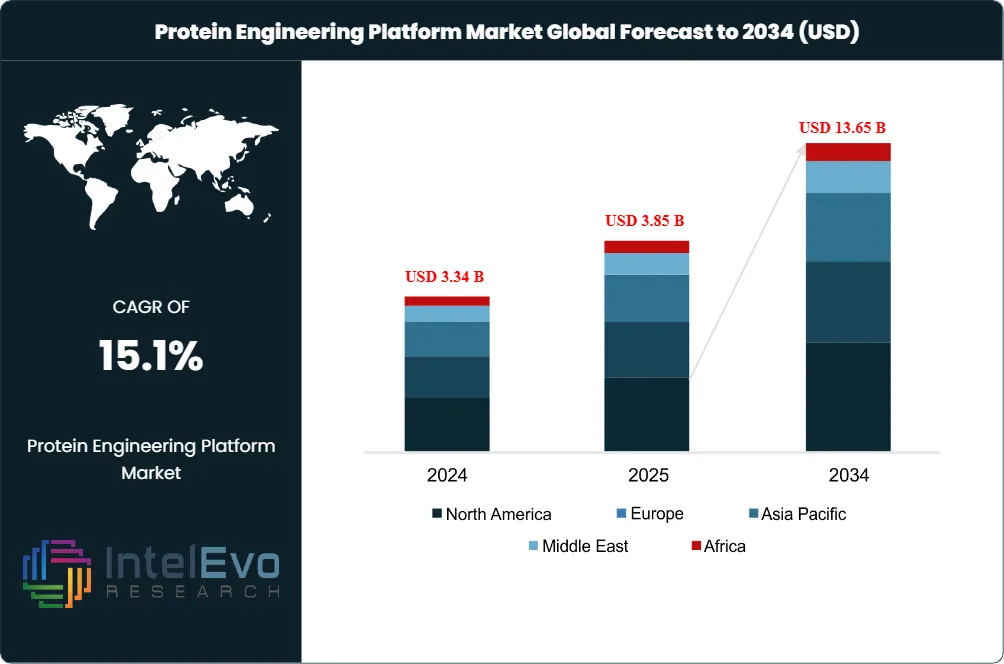

The Protein Engineering Platform Market was valued at USD 3.34 Billion in 2024 and USD 3.85 Billion in 2025. The market is projected to reach USD 13.65 Billion by 2034, expanding at a CAGR of 15.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 9.80 Billion over the analysis window, anchored to the rapid maturation of generative AI protein design, expansion of biologics pipelines, and pharmaceutical industry adoption of computational platforms for therapeutic development.

Get More Information about this report -

Request Free Sample ReportDemand for the protein engineering platform market is driven by the convergence of deep learning and structural biology that enabled Google DeepMind's AlphaFold 3 to predict over 200 million protein structures by 2024, with AlphaProteo achieving binding-affinity success rates up to 700 times higher than legacy methods such as RFdiffusion. Pharmaceutical R&D budgets increasingly fund platform partnerships, as evidenced by the USD 1 Billion Novartis-Generate Biomedicines collaboration signed in September 2024 and the USD 1.9 Billion Amgen-Generate alliance covering five protein therapeutic targets.

Regulatory tailwinds are altering the protein engineering platform market. The EU Biotech Act and U.S. AI Action Plan implemented in 2025 mandated enforceable biosecurity screening for DNA synthesis orders, raising compliance bars while legitimizing platform credibility. The FDA's Center for Drug Evaluation and Research approved 73 monoclonal antibody therapeutics by year-end 2025, fueling demand for upstream design and engineering platforms. Cell and gene therapy quality control mandates from FDA CBER and EMA further drive enzyme engineering for AAV manufacturing and biosimilar characterization.

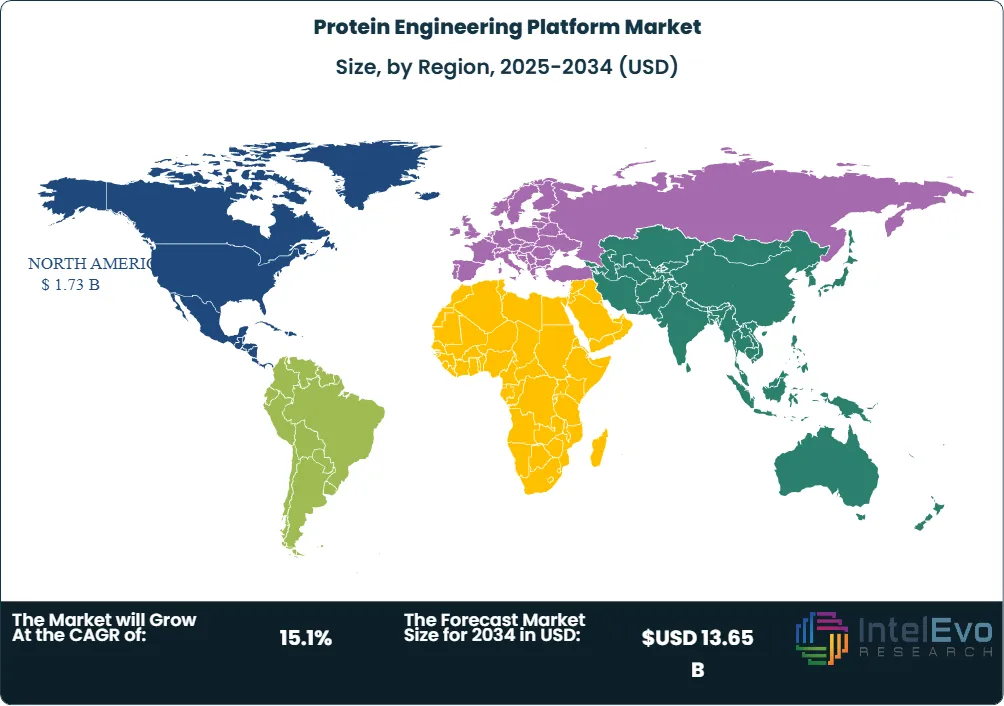

North America held 44.8% of the protein engineering platform market in 2025, supported by NIH RePORTER grants, Boston-Cambridge biotech density, and the Bay Area cluster of AI-native biotechs including Generate Biomedicines, Absci, and Insitro. Asia Pacific is the fastest-growing region, advancing at a CAGR of 19.6% through 2034 because of China's Made in China 2025 biotech reforms, India's Production Linked Incentive (PLI) scheme for biopharmaceuticals, and Japan's regenerative medicine push. Combined, these dynamics anchor protein engineering as a core foundational technology supporting the broader USD 500 Billion bioeconomy projected by 2035.

By 2034, consolidation should reshape the protein engineering platform market further. The top four tools and platform vendors hold approximately 47% of 2025 revenue, with mergers reflecting platform-over-asset strategy. Thermo Fisher Scientific's Q1 2025 Ingenza acquisition for synthetic biology, and Generate Biomedicines' USD 400 Million February 2026 IPO, signal that incumbents and challengers alike pay premium multiples to lock in computational and wet-lab integration.

Market Definition & Scope

The protein engineering platform market is defined as the global commercial activity surrounding integrated systems that design, modify, optimize, and validate proteins for therapeutic, industrial, agricultural, and diagnostic applications. The market encompasses computational design platforms (rational design, directed evolution, semi-rational hybrid, generative AI), wet-lab instrumentation (chromatography, mass spectrometry, expression systems), reagents and consumables, and software-and-services layers used across drug discovery, biosimilar development, and enzyme engineering.

This analysis includes AI-driven generative platforms, automated liquid handling for high-throughput screening, recombinant protein expression systems, mass spectrometry and structural-biology instrumentation, dedicated software for protein modeling, and contract platform services. Excluded are end-stage therapeutic manufacturing equipment, generic proteomics tools without engineering function, raw amino-acid commodity chemistry, and downstream fill-finish operations. Within the broader USD 22 Billion biopharmaceutical R&D tools parent market, protein engineering platforms represent approximately 17.5% of total revenue in 2025.

, By Technology Approach (Rational Protein Design, Directed Evolution, De Novo Protein Design, AI-Assisted Protein Engineering and High-Throughput Screening), By Protein Type (Monoclonal Antibodies, Enzymes, Therapeutic Proteins and Vaccines), By End-User (Pharmaceutical & Biotechnology Companies, CROs and Academic Institutes) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The protein engineering platform market expanded from USD 3.85 Billion in 2025 toward USD 13.65 Billion by 2034 at a 15.1% CAGR, generating USD 9.80 Billion in absolute dollar opportunity.

- Segment Dominance: Instruments commanded 51.8% of revenue in 2025, driven by mass spectrometry, chromatography, and automated liquid handling demand from biopharma R&D centers.

- Segment Dominance: Rational design held 56.6% of technology-approach revenue in 2025, supported by mature workflows in antibody and enzyme development across pharmaceutical and biotechnology pipelines.

- Driver: Generative AI integration is the primary growth catalyst, with AlphaProteo achieving 88% success rates on BHRF1 targets and Generate Biomedicines' platform feeding 17 active programs in oncology, immunology, and infectious disease as of 2025.

- Restraint: Per-target development costs of USD 5 Million to USD 25 Million for full platform licensing, plus specialized AI talent shortages, constrain adoption among small and mid-size biotechs.

- Opportunity: Software and services represents an addressable opportunity exceeding USD 2.7 Billion by 2034, expanding at a 19.85% CAGR as pharma teams license cloud-based modeling and analytics from Cradle Bio, OpenProtein.AI, and Isomorphic Labs.

- Trend: Foundation protein language models including ESM3, OpenProtein.AI's PoET-2, and Chai Discovery's Chai-1 have shifted protein engineering platforms from physics-based simulation toward learned representations trained on the 200-million-structure AlphaFold database.

- Regional: North America led with USD 1.73 Billion in 2025 revenue at 44.8% share, while Asia Pacific posted the fastest regional CAGR of 19.6% through 2034.

Key Insights Summary

- The protein engineering platform market reached over 200 million predicted protein structures in the AlphaFold Database by mid-2024, with the AlphaFold 3 paper accumulating more than 9,000 citations through November 2025.

- Generate Biomedicines completed a USD 400 Million IPO at USD 16 per share in February 2026, valuing the company at approximately USD 2.04 Billion at pricing and dedicating USD 300 Million to Phase 3 GB-0895 severe asthma trials.

- Absci Corporation reported USD 4.5 Million in 2024 revenue with a USD 596.4 Million cash position as of September 30, 2025, sufficient to fund operations into 2029, plus an AMD strategic equity investment of USD 20 Million in January 2025.

- AlphaProteo achieved binding affinities 3 to 300 times stronger than existing protein-design methods across eight high-value targets including the SARS-CoV-2 spike protein and the inflammatory protein IL-17A in DeepMind benchmarks published in 2024.

- Cradle Bio's USD 73 Million Series B brought total funding above USD 100 Million by November 2024, with active partnerships covering Novo Nordisk, Johnson & Johnson, Grifols, and Twist Biosciences for protein optimization across enzymes, vaccines, peptides, and antibodies.

- OpenProtein.AI's PoET-2 protein language model outperformed substantially larger models while using a fraction of the compute and experimental data, with Boehringer Ingelheim embedding the platform into oncology and inflammatory disease engineering programs in 2025.

Competitive Landscape Overview

The protein engineering platform market is moderately fragmented across two competitive layers. Tools and instruments incumbents, namely Thermo Fisher Scientific, Bio-Rad Laboratories, Merck KGaA, and Agilent Technologies, hold approximately 47% of 2025 revenue collectively. AI-native platform challengers including Generate Biomedicines, Absci, Cradle Bio, and Isomorphic Labs add another 18% combined, with the remaining share distributed among service providers, contract research organizations, and academic spinouts.

Competitive evolution is shifting from instrument differentiation toward integrated AI-plus-wet-lab platforms with proprietary data moats. Generate Biomedicines anchors USD 3 Billion of potential platform-licensing value across its Amgen and Novartis collaborations, while Absci's zero-shot generative AI partnerships span AstraZeneca, Almirall, and Merck. Specialty players including Nabla Bio (USD 550 Million in active collaborations) and Syneron Bio (USD 3.4 Billion AstraZeneca peptide deal) demonstrate that platform credibility now translates directly into multi-billion-dollar pharma alliances.

Competitive Landscape Matrix

| Company | HQ | Position | Key Platform/Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Thermo Fisher Scientific Inc. | United States | Leader | Gibco protein expression, Applied Biosystems instruments, ProteinSimple | Global | Q1 2025 acquisition of Ingenza for synthetic biology and enzyme engineering |

| Bio-Rad Laboratories, Inc. | United States | Leader | ChromLab, NGC chromatography, ddPCR validation | Americas, EMEA, APAC | Q2 2025 named new head of protein engineering division to expand biologics franchise |

| Merck KGaA | Germany | Leader | MilliporeSigma protein engineering reagents, BioReliance services | Europe, North America | Q4 2024 strategic protein therapeutic partnership signed with GenScript Biotech |

| Agilent Technologies, Inc. | United States | Leader | AssayMAP Bravo, BioTek instruments, mass spectrometry portfolio | Global | Expanded targeted protein characterization and biologics QC suite through 2025 |

| Generate Biomedicines, Inc. | United States | Challenger | The Generate Platform (generative AI biology) | North America | February 2026 IPO raised USD 400 million to fund Phase 3 GB-0895 asthma trials |

| Absci Corporation | United States | Challenger | Integrated Drug Creation Platform with zero-shot generative AI | North America, Europe | September 2025 collaboration with Oracle Cloud Infrastructure and AMD to scale AI workloads |

| Bruker Corporation | United States | Challenger | timsTOF, NMR, and X-ray protein structural analysis | Global | May 2025 launched timsOmni mass spectrometer for biologics QC and drug discovery |

| GenScript Biotech Corporation | China | Challenger | Custom gene synthesis, antibody engineering services | Asia Pacific, North America | Q4 2024 protein therapeutics co-development partnership signed with Merck KGaA |

| Cradle Bio B.V. | Netherlands | Niche Player | Cradle generative AI protein optimization platform | Europe, North America | Active partnerships with Novo Nordisk, Johnson & Johnson, and Twist Biosciences in 2025 |

| Isomorphic Labs Limited | United Kingdom | Niche Player | AlphaFold 3 and AlphaProteo derivative platforms | Global | January 2026 announced first AI-designed drugs entering human clinical trials |

Segmentation Analysis

The protein engineering platform market segments by product and service, technology approach, protein type, and end-user, with segment economics shaped by recurring instrument utilization, AI software licensing, and biopharma platform-partnership terms.

By Product and Service

Instruments dominated the protein engineering platform market with 51.8% revenue share and approximately USD 1.99 Billion in 2025, ahead of reagents and consumables at 28.4% and software and services at 19.8%. Mass spectrometry instruments including Bruker Corporation's timsTOF and Thermo Fisher Scientific's Orbitrap families enable identification and sequencing of thousands of proteins per run, while automated liquid handlers from Hamilton, Tecan, and Beckman Coulter streamline high-throughput screening. The instrument refresh cycle accelerated through 2025 as biopharma capital expenditure recovered from constrained 2023-2024 funding environments.

Software and services is the fastest-growing protein engineering platform sub-segment at a 19.85% CAGR through 2034, surpassing USD 2.7 Billion by the forecast year. AI-driven modeling platforms from Cradle Bio, OpenProtein.AI, and Isomorphic Labs license cloud access on per-seat or per-program terms, with typical pharmaceutical contracts ranging from USD 500,000 to USD 5 Million annually. Procurement teams comparing platform vendors increasingly weigh model accuracy, training-data provenance, and wet-lab integration depth as primary decision criteria when running ROI calculations on AI protein design platform spend.

By Technology Approach

Rational design held 56.6% of protein engineering platform market revenue in 2025, equivalent to approximately USD 2.18 Billion, anchored by mature antibody engineering and enzyme development workflows. Computational structure-guided redesign using molecular dynamics, homology modeling, and crystal-structure refinement remains the workhorse approach across pharmaceutical and biotechnology R&D centers. Bio-Rad Laboratories, Thermo Fisher Scientific, and Bruker Corporation supply the underlying chromatography, mass spectrometry, and structural-analysis instruments that anchor rational design pipelines.

Hybrid semi-rational approaches will post the fastest 18.5% CAGR through 2034 as protein engineering platform vendors integrate generative AI predictions with directed evolution screening. AlphaFold 3, AlphaProteo, RFdiffusion, ProteinMPNN, ESM3, and Chai-1 reduced backbone-RMSD prediction error to under 2 Angstroms on benchmark targets, compressing design-build-test cycles from months to days. Directed evolution platforms from GenScript Biotech and Twist Biosciences serve the experimental-validation tier, capturing the remaining 24.9% of segment revenue. Buyers comparing protein engineering platform vendors should examine the integration timeline between in-silico design and wet-lab validation.

By Protein Type

Monoclonal antibodies accounted for 40.4% of protein engineering platform market revenue in 2025, equivalent to approximately USD 1.55 Billion, driven by oncology, immunology, and inflammatory-disease pipelines that yielded over USD 315 Billion in annual antibody-therapeutic sales by 2025. Bispecific and antibody-drug conjugate (ADC) formats now constitute a notable share of new FDA filings, with platforms from Generate Biomedicines, Absci, and Nabla Bio specifically optimizing affinity, manufacturability, and immunogenicity. Enzymes and peptides represented 22.6% and 18.4% of revenue respectively, with Syneron Bio's Synova macrocyclic peptide platform exemplifying the design-space expansion enabled by AI.

Vaccines captured 11.8% of protein engineering platform revenue in 2025, supported by mRNA platform success and booster-shot demand across coronavirus, RSV, and flu indications. Other protein modalities including cytokines, fusion proteins, and engineered enzymes for cell and gene therapy held the remaining 6.8%. Cell and gene therapy AAV-vector engineering, where capsid optimization platforms reduce immunogenicity and increase tropism precision, will outpace the broader segment at an estimated 17.4% CAGR through 2034.

By End-User

Pharmaceutical and biotechnology companies represented the largest end-user category at 48.8% of protein engineering platform market revenue in 2025, anchored by in-house drug discovery, biosimilar development, and platform-licensing programs. Contract research organizations followed at 27.3%, with academic and research institutes at 18.4% and forensic and other end-users at 5.5%. The CRO sub-segment will post the fastest 18.6% CAGR through 2034 as small-to-mid-sized biotechs outsource protein engineering to specialized CROs in China and India to compress R&D budgets while accessing AI-platform capability without in-house capital expenditure.

Regional Analysis

The protein engineering platform market exhibits geographic concentration in North America and Europe, with Asia Pacific advancing fastest. Regional shares aggregate to 100% across the five regions surveyed.

North America

North America led the protein engineering platform market with 44.8% share and USD 1.73 Billion in revenue in 2025. The United States dominates regional demand at approximately USD 1.46 Billion, with Canada at USD 0.21 Billion and Mexico at USD 0.06 Billion. Demand drivers include NIH RePORTER grant funding, NIST industrial enzyme standards programs, and biopharma R&D concentration in Boston-Cambridge, Bay Area, and Research Triangle Park. AI-native biotech density anchors the region: Generate Biomedicines (Somerville, MA), Absci Corporation (Vancouver, WA), Insitro (South San Francisco, CA), and OpenProtein.AI (Cambridge, MA) all closed material capital events through 2025-2026, with Generate's February 2026 IPO raising USD 400 Million.

Europe

Europe held 25.2% of the protein engineering platform market in 2025, equivalent to USD 0.97 Billion, with Germany, the United Kingdom, and Switzerland constituting the tri-core demand cluster. The EU Biotech Act and updated GMP guidelines tightened compliance requirements but enabled cross-border platform commercialization. Imperial College London opened Imperial Global USA in November 2024 to develop 100 new US-UK partnerships in 2025. Cradle Bio (Netherlands) anchors the European AI-platform layer, while Bruker Corporation (Karlsruhe, Germany) and Merck KGaA (Darmstadt) supply mass spectrometry and reagents respectively. Novo Nordisk's Q1 2025 protein engineering R&D center inauguration in Denmark further deepened regional capacity.

Asia Pacific

Asia Pacific captured 22.5% of protein engineering platform market revenue in 2025 at USD 0.87 Billion, posting the highest regional CAGR at 19.6% through 2034. China's Made in China 2025 reforms, India's Production Linked Incentive (PLI) scheme for biopharmaceuticals, Japan's regenerative medicine policy, and South Korea's K-Bio Vision 2030 drove regional momentum. WuXi AppTec launched AI-assisted protein optimization services in early 2026, and Takeda Pharmaceutical expanded protein engineering R&D across Japan and Southeast Asia in July 2025. GenScript Biotech (China) and Syneron Bio (China-based with international investors) anchor the regional platform layer, with Syneron closing a USD 150 Million Series B in April 2025.

Latin America

Latin America accounted for 4.5% of the protein engineering platform market in 2025 at USD 0.17 Billion, with Brazil and Mexico leading demand. Brazil's Embrapa funded enzyme engineering programs for sugarcane bioethanol and animal-feed applications. Distributor partnerships and bundled instrument-plus-reagent contracts dominate regional sales motions, reflecting price sensitivity in academic and public-sector budgets.

Middle East & Africa

Middle East and Africa held 3.0% of protein engineering platform market revenue in 2025 at USD 0.12 Billion. Saudi Arabia's Vision 2030 healthcare-modernization program and the United Arab Emirates' Mohamed bin Zayed University of Artificial Intelligence (MBZUAI) life-science partnerships anchored Gulf demand. South African academic institutions including the University of Cape Town deployed protein engineering platforms for HIV vaccine and tuberculosis therapeutic research, often funded through Wellcome Trust and Bill and Melinda Gates Foundation grants.

Country Analysis

United States

The United States protein engineering platform market reached USD 1.46 Billion in 2025 and is forecast to grow at a country-specific CAGR of 14.6% through 2034. Demand drivers include NIH grants, NIST industrial biotechnology standards, and biopharma R&D concentration in Boston-Cambridge, Bay Area, and Research Triangle Park. Federal procurement under HHS BARDA contracts funded antibody engineering for pandemic preparedness, while California's CIRM and Texas's CPRIT supported translational protein design. The U.S. AI Action Plan implemented in 2025 mandated SafeProtein-style biosecurity screening for DNA synthesis orders. Generate Biomedicines' February 2026 IPO and Absci Corporation's January 2025 AMD equity investment underscore U.S. capital depth for AI protein engineering.

China

China's protein engineering platform market reached approximately USD 0.347 Billion in 2025 and is projected to expand at a 21.4% country-level CAGR through 2034, the highest among major economies. Demand drivers include the Made in China 2025 biotech reforms, provincial genomics-research grants, and the rise of academic-industrial AI consortia at Tsinghua University, Peking University, and Westlake University. WuXi Biologics, BeiGene, and GenScript Biotech anchor industrial capacity, while Syneron Bio raised USD 150 Million in April 2025 with Decheng Capital, CDH VGC, and the Abu Dhabi Investment Authority. Syneron Bio's USD 3.4 Billion AstraZeneca peptide-platform deal signed in March 2025 demonstrates Chinese platform credibility commanding multi-billion-dollar pharma multiples.

Germany

Germany's protein engineering platform market reached approximately USD 0.270 Billion in 2025, expanding at a country-level CAGR of 14.0% through 2034. Strong biopharma R&D in Bavaria and North Rhine-Westphalia, plus academic-medical centers including Charite Berlin and Heidelberg University Hospital, anchor demand. The Federal Ministry of Education and Research (BMBF) funded Industrial Biotechnology and Future Cluster Initiative programs covering enzyme engineering. Merck KGaA's Darmstadt headquarters serves as a strategic hub for the global MilliporeSigma protein-engineering reagent franchise, and Bruker Corporation's Bremen mass-spectrometry operations support biopharma analytical workflows. The May 2025 timsOmni launch from Bruker addressed advanced biologics quality control with sub-ppm mass accuracy.

Japan

Japan's protein engineering platform market stood at approximately USD 0.193 Billion in 2025, expanding at a country-level CAGR of 12.8% through 2034. The Japan Society for the Promotion of Science (JSPS) Grant-in-Aid program and AMED (Japan Agency for Medical Research and Development) funded translational protein engineering. Takeda Pharmaceutical expanded protein engineering R&D across Japan and Southeast Asia in July 2025, targeting therapeutic peptides, vaccines, and biologics. FUJIFILM Holdings, Shimadzu Corporation, and Takara Bio Inc. anchor domestic instrument and reagent supply, while Astellas Pharma and Daiichi Sankyo expanded internal AI-driven design capabilities in 2025.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Product and Service

- Instruments

- Reagents and Consumables

- Software and Computational Tools

- Protein Engineering Services

- Contract Research Services

- Assay and Screening Services

- Protein Expression and Purification Services

- Bioinformatics and Data Analysis Services

- Others

By Technology Approach

- Rational Protein Design

- Directed Evolution

- Semi-Rational Design

- De Novo Protein Design

- Computational Protein Engineering

- Machine Learning and Artificial Intelligence (AI)-Assisted Protein Engineering

- High-Throughput Screening Technologies

- Phage Display Technology

- Yeast Display Technology

- Ribosome Display Technology

- Others

By Protein Type

- Monoclonal Antibodies

- Enzymes

- Therapeutic Proteins

- Vaccines and Vaccine Proteins

- Cytokines and Growth Factors

- Fusion Proteins

- Structural Proteins

- Industrial Proteins

- Biosimilar Proteins

- Others

By End-User

- Pharmaceutical and Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic and Research Institutes

- Clinical Research Organizations

- Hospitals and Diagnostic Centers

- Food and Beverage Companies

- Agricultural and Veterinary Organizations

- Industrial Biotechnology Companies

- Government and Public Research Agencies

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.85 B |

| Forecast Revenue (2034) | USD 13.65 B |

| CAGR (2025-2034) | 15.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product and Service, (Instruments, Reagents and Consumables, Software and Computational Tools, Protein Engineering Services, Contract Research Services, Assay and Screening Services, Protein Expression and Purification Services, Bioinformatics and Data Analysis Services, Others), By Technology Approach, (Rational Protein Design, Directed Evolution, Semi-Rational Design, De Novo Protein Design, Computational Protein Engineering, Machine Learning and Artificial Intelligence (AI)-Assisted Protein Engineering, High-Throughput Screening Technologies, Phage Display Technology, Yeast Display Technology, Ribosome Display Technology, Others), By Protein Type, (Monoclonal Antibodies, Enzymes, Therapeutic Proteins, Vaccines and Vaccine Proteins, Cytokines and Growth Factors, Fusion Proteins, Structural Proteins, Industrial Proteins, Biosimilar Proteins, Others), By End-User, (Pharmaceutical and Biotechnology Companies, Contract Research Organizations (CROs), Academic and Research Institutes, Clinical Research Organizations, Hospitals and Diagnostic Centers, Food and Beverage Companies, Agricultural and Veterinary Organizations, Industrial Biotechnology Companies, Government and Public Research Agencies, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | THERMO FISHER SCIENTIFIC INC., BIO-RAD LABORATORIES, INC., MERCK KGAA, AGILENT TECHNOLOGIES, INC., GENERATE BIOMEDICINES, INC., ABSCI CORPORATION, BRUKER CORPORATION, GENSCRIPT BIOTECH CORPORATION, CRADLE BIO B.V., ISOMORPHIC LABS LIMITED, WATERS CORPORATION, DANAHER CORPORATION, AMGEN INC., ELI LILLY AND COMPANY, NOVO NORDISK A/S, WUXI APPTEC CO., LTD., TAKARA BIO INC., OPENPROTEIN.AI, NABLA BIO, INC., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology Approach (Rational Protein Design, Directed Evolution, De Novo Protein Design, AI-Assisted Protein Engineering and High-Throughput Screening), By Protein Type (Monoclonal Antibodies, Enzymes, Therapeutic Proteins and Vaccines), By End-User (Pharmaceutical & Biotechnology Companies, CROs and Academic Institutes) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Technology Approach (Rational Protein Design, Directed Evolution, De Novo Protein Design, AI-Assisted Protein Engineering and High-Throughput Screening), By Protein Type (Monoclonal Antibodies, Enzymes, Therapeutic Proteins and Vaccines), By End-User (Pharmaceutical & Biotechnology Companies, CROs and Academic Institutes) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Technology Approach (Rational Protein Design, Directed Evolution, De Novo Protein Design, AI-Assisted Protein Engineering and High-Throughput Screening), By Protein Type (Monoclonal Antibodies, Enzymes, Therapeutic Proteins and Vaccines), By End-User (Pharmaceutical & Biotechnology Companies, CROs and Academic Institutes) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Protein Engineering Platform Market?

The Global Protein Engineering Platform Market was valued at USD 3.34 Billion in 2024 and USD 3.85 Billion in 2025, and is projected to reach USD 13.65 Billion by 2034, growing at a CAGR of 15.1% from 2026 to 2034. Market growth is driven by rising demand for novel biologics, increasing biopharmaceutical R&D investments, and advancements in AI-enabled protein engineering technologies.

Who are the major players in the Protein Engineering Platform Market?

THERMO FISHER SCIENTIFIC INC., BIO-RAD LABORATORIES, INC., MERCK KGAA, AGILENT TECHNOLOGIES, INC., GENERATE BIOMEDICINES, INC., ABSCI CORPORATION, BRUKER CORPORATION, GENSCRIPT BIOTECH CORPORATION, CRADLE BIO B.V., ISOMORPHIC LABS LIMITED, WATERS CORPORATION, DANAHER CORPORATION, AMGEN INC., ELI LILLY AND COMPANY, NOVO NORDISK A/S, WUXI APPTEC CO., LTD., TAKARA BIO INC., OPENPROTEIN.AI, NABLA BIO, INC., OTHERS

Which segments covered the Protein Engineering Platform Market?

By Product and Service, (Instruments, Reagents and Consumables, Software and Computational Tools, Protein Engineering Services, Contract Research Services, Assay and Screening Services, Protein Expression and Purification Services, Bioinformatics and Data Analysis Services, Others), By Technology Approach, (Rational Protein Design, Directed Evolution, Semi-Rational Design, De Novo Protein Design, Computational Protein Engineering, Machine Learning and Artificial Intelligence (AI)-Assisted Protein Engineering, High-Throughput Screening Technologies, Phage Display Technology, Yeast Display Technology, Ribosome Display Technology, Others), By Protein Type, (Monoclonal Antibodies, Enzymes, Therapeutic Proteins, Vaccines and Vaccine Proteins, Cytokines and Growth Factors, Fusion Proteins, Structural Proteins, Industrial Proteins, Biosimilar Proteins, Others), By End-User, (Pharmaceutical and Biotechnology Companies, Contract Research Organizations (CROs), Academic and Research Institutes, Clinical Research Organizations, Hospitals and Diagnostic Centers, Food and Beverage Companies, Agricultural and Veterinary Organizations, Industrial Biotechnology Companies, Government and Public Research Agencies, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Protein Engineering Platform Market

Published Date : 15 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date