- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Quantum Communication Market Size, Share, Grwoth | CAGR of 35.99%

Global Quantum Communication Market Size, Share, Analysis Report By Product Type(Software, Services, Hardware) Technology Type(Quantum Teleportation, Quantum Key Distribution (QKD)) Security Service(Network Security, Application Security) End-User(Banking & Financial Services, Telecommunications, Government & Defense, Other Applications) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034

Report Overview

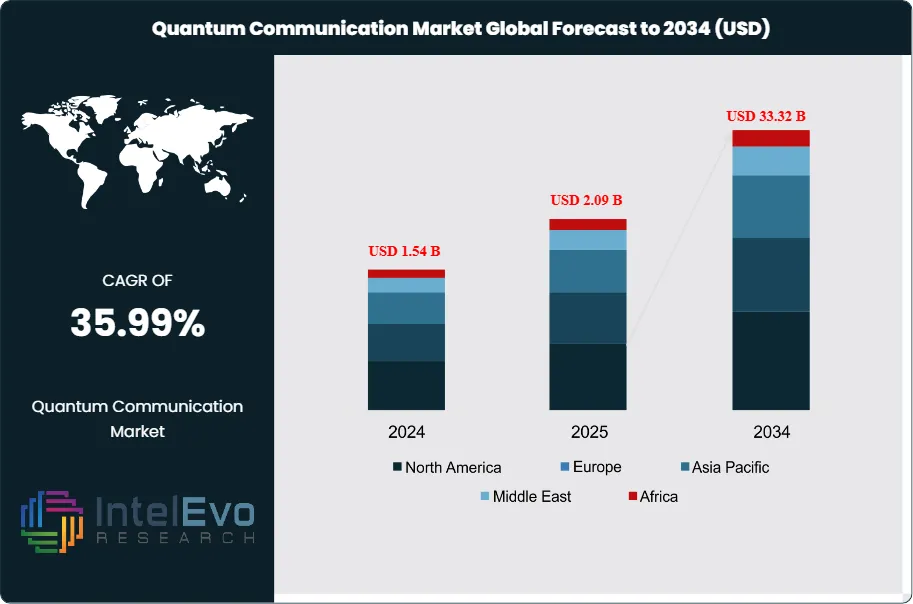

The Quantum Communication Market size is expected to be worth around USD 33.32 Billion by 2034, from USD 1.54 Billion in 2024, growing at a CAGR of 35.99% during the forecast period from 2024 to 2034. The quantum communication market encompasses technologies and solutions that leverage quantum mechanical properties to ensure ultra-secure data transmission and cryptographic key distribution. This includes Quantum Key Distribution (QKD) systems, quantum repeaters, photonic detectors, quantum teleportation infrastructure, and related hardware, software, and services. The market serves critical applications requiring the highest levels of communication security, including government networks, financial institutions, telecommunications infrastructure, and enterprise data protection systems.

Get More Information about this report -

Request Free Sample ReportThe quantum communication sector experiences unprecedented growth driven by escalating cybersecurity threats and the looming quantum computing threat to conventional encryption methods. Organizations across sectors are proactively implementing quantum-safe communication solutions to protect against future quantum attacks. Government initiatives worldwide, including substantial R&D investments and national quantum programs, are accelerating market development. The increasing digitization of critical infrastructure and the growing volume of sensitive data requiring protection are creating sustained demand for quantum communication technologies.

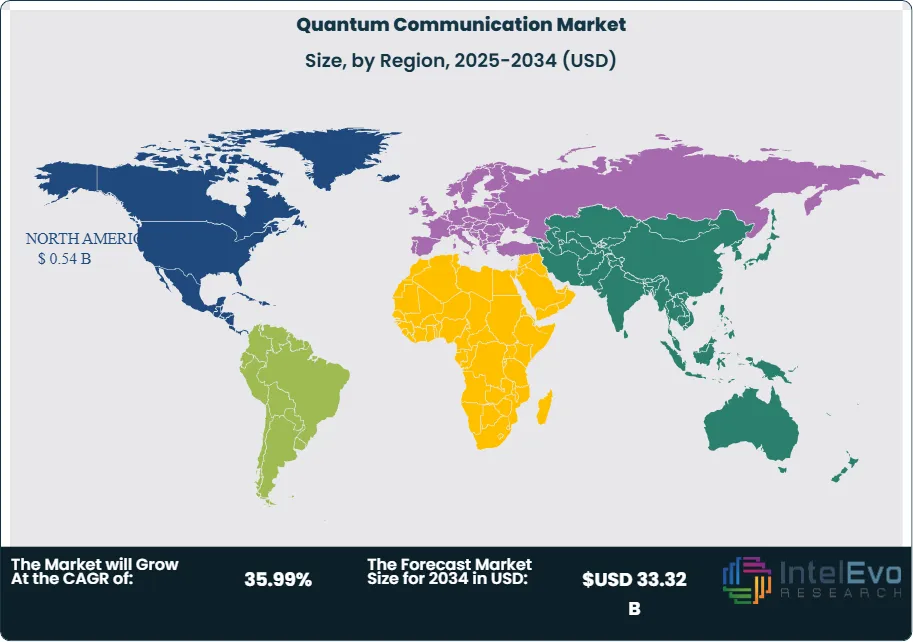

North America currently leads the global quantum communication market, driven by significant government investments, advanced research institutions, and early adopter enterprises in defense and financial sectors. The United States' National Quantum Initiative and substantial defense spending on quantum technologies support market growth. Asia-Pacific, particularly China and Japan, represents the fastest-growing region with massive government investments in quantum infrastructure and commercial deployments. Europe maintains strong market presence through coordinated quantum research programs and regulatory frameworks supporting quantum technology adoption.

The pandemic accelerated quantum communication market growth by highlighting vulnerabilities in digital infrastructure and increasing reliance on secure remote communications. Government agencies and enterprises recognized the critical importance of quantum-safe communication systems as cyber threats intensified during global lockdowns. The shift toward digital-first operations and remote work environments created new security requirements that conventional encryption methods struggled to address adequately, driving interest in quantum communication solutions.

Geopolitical tensions have significantly influenced quantum communication market dynamics, with nations viewing quantum technologies as strategic national assets. Export controls and technology transfer restrictions have shaped international collaboration patterns and market access. The ongoing technology competition between major powers has accelerated domestic quantum research investments and created regional supply chain preferences. These dynamics have both constrained international cooperation and intensified national quantum development programs.

Technology Type(Quantum Teleportation, Quantum Key Distribution (QKD)) Security Service(Network Security, Application Security) End-User(Banking & Financial Services, Telecommunications, Government & Defense, Other Applications) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Key Takeaways

- Market Growth: The Quantum Communication Market is expected to reach USD 33.32 Billion by 2034, fueled by government investments in national quantum programs, increasing digitization of critical infrastructure, and the urgent need to secure sensitive data before quantum computers can break current cryptographic methods.

- Product Type Dominance: Hardware leads the quantum communication market due to fundamental infrastructure requirements and high-value component demand for QKD systems and quantum repeaters.

- Technology Type Dominance: Quantum Key Distribution (QKD) dominates the technology landscape, driven by proven commercial viability and established security protocols.

- Security Service Dominance: Application security leads the market, primarily due to comprehensive data protection scope and direct encryption implementation needs.

- End-User Dominance: Government and defense hold the largest share in the application segment, owing to national security imperatives and substantial R&D investments.

- Drivers: Key drivers accelerating growth include quantum computing threat emergence and cybersecurity imperative escalation, which boost market expansion through proactive security investments and regulatory compliance requirements.

- Restraints: Growth is hindered by high implementation costs and technical complexity barriers, which create challenges such as limited accessibility for smaller organizations and integration difficulties with existing infrastructure.

- Opportunities: The market is poised for expansion due to opportunities like satellite-based quantum networks and quantum internet development, which enable global secure communication infrastructure and next-generation connectivity solutions.

- Trends: Emerging trends including quantum-safe cryptography standardization and commercial quantum network deployment are reshaping the market by establishing technical standards and enabling practical quantum communication applications.

- Regional Leader: North America leads owing to substantial government investments and advanced research ecosystem. Asia-Pacific and Europe show high promise due to coordinated quantum initiatives and infrastructure development programs.

Product Type Analysis:

Hardware dominance in quantum communication reflects the fundamental infrastructure requirements for quantum systems implementation. Quantum Key Distribution systems, quantum repeaters, photonic detectors, and specialized optical components represent the core technological foundation enabling secure quantum communication networks. The segment's leadership stems from the capital-intensive nature of quantum infrastructure deployment and the critical importance of reliable quantum devices in maintaining communication security. Hardware components require sophisticated manufacturing processes, precision engineering, and advanced materials science, creating high barriers to entry and substantial value concentration. The ongoing evolution of quantum technologies drives continuous hardware innovation cycles, sustaining demand for next-generation components and system upgrades across government, enterprise, and telecommunications sectors.

Technology Type Analysis:

Quantum Key Distribution Leads With nearly 35% Market Share In Quantum Communication Market: Quantum Key Distribution has established technological dominance through demonstrated commercial viability and proven security advantages over conventional cryptographic methods. QKD's ability to detect eavesdropping attempts through quantum mechanical principles provides unparalleled communication security, making it the preferred choice for government and high-security applications. The technology benefits from established technical standards, mature implementation protocols, and growing ecosystem of compatible devices and systems. QKD's commercial success has attracted substantial investment and research focus, accelerating technology refinement and cost reduction initiatives. The segment's maturity has enabled practical deployments in metropolitan networks, government facilities, and critical infrastructure, demonstrating real-world feasibility and encouraging broader adoption across security-conscious industries.

Security Service Analysis:

Application security dominates the quantum communication security landscape through comprehensive data protection capabilities and direct encryption implementation at the software and system level. This segment addresses the fundamental security requirements of organizations seeking to protect sensitive data, intellectual property, and communications from current and future threats. Application security solutions provide end-to-end protection mechanisms that integrate with existing enterprise systems while offering quantum-safe cryptographic capabilities. The segment's growth reflects the increasing recognition that data security must be embedded throughout the application layer rather than relying solely on network-level protection. As organizations prepare for the quantum computing era, application security becomes critical for ensuring long-term data protection and regulatory compliance across diverse industry sectors and use cases.

End-User Analysis:

Government and defense applications lead quantum communication adoption due to national security imperatives and the critical importance of protecting classified information from sophisticated threats. Defense agencies require communication systems capable of withstanding advanced persistent threats and potential quantum computer attacks on conventional encryption methods. The segment benefits from substantial government R&D budgets, long-term procurement commitments, and strategic technology development programs supporting quantum communication infrastructure. Military applications demand the highest levels of communication security, making quantum technologies essential for future defense capabilities. Additionally, government agencies serve as early adopters and technology validators, helping establish technical standards and implementation best practices that facilitate broader market development and commercial adoption.

Regional Analysis:

North America Leads With over 35% Market Share In Quantum Communication Market: North America maintains its leadership position in the quantum communication market through substantial government investments, world-class research institutions, and early enterprise adoption across defense and financial sectors. The United States National Quantum Initiative has allocated billions of dollars for quantum research and development, while defense agencies actively deploy quantum communication systems for classified networks. The region benefits from a mature technology ecosystem, including leading universities, national laboratories, and quantum technology companies driving innovation and commercialization. Asia-Pacific emerges as the fastest-growing region, led by China's massive quantum infrastructure investments and Japan's technological excellence in quantum devices. China has deployed the world's longest quantum communication networks and continues expanding quantum satellite capabilities, while South Korea and Singapore are implementing national quantum programs. Europe maintains significant market presence through coordinated research initiatives like the European Quantum Technologies Flagship and strong industrial partnerships between technology companies and research institutions. The region emphasizes quantum-safe cryptography standards and regulatory frameworks supporting quantum technology adoption across member nations, creating favorable conditions for market growth and international collaboration in quantum communication development.

Get More Information about this report -

Request Free Sample ReportMarket Key Segment

Product Type:

- Software

- Services

- Hardware

Technology Type:

- Quantum Teleportation

- Quantum Key Distribution (QKD)

Security Service:

- Network Security

- Application Security

End-User:

- Banking & Financial Services

- Telecommunications

- Government & Defense

- Other Applications

Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.09 B |

| Forecast Revenue (2034) | USD 33.32 B |

| CAGR (2025-2034) | 35.99% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Product Type(Software, Services, Hardware) Technology Type(Quantum Teleportation, Quantum Key Distribution (QKD)) Security Service(Network Security, Application Security) End-User(Banking & Financial Services, Telecommunications, Government & Defense, Other Applications) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Toshiba Corporation, ID Quantique, Thales Group, QuantumCTek Co. Ltd, Arqit Quantum Inc., ColdQuanta Inc., Excelitas Technologies, USTC, Atos, SK Telecom |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Technology Type(Quantum Teleportation, Quantum Key Distribution (QKD)) Security Service(Network Security, Application Security) End-User(Banking & Financial Services, Telecommunications, Government & Defense, Other Applications) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Technology Type(Quantum Teleportation, Quantum Key Distribution (QKD)) Security Service(Network Security, Application Security) End-User(Banking & Financial Services, Telecommunications, Government & Defense, Other Applications) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Technology Type(Quantum Teleportation, Quantum Key Distribution (QKD)) Security Service(Network Security, Application Security) End-User(Banking & Financial Services, Telecommunications, Government & Defense, Other Applications) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Frequently Asked Questions

How big is the Quantum Communication Market?

Quantum Communication Market is set for explosive growth, projected to hit $33.32B by 2034 with a staggering 35.99% CAGR. Discover the trends driving this future of secure communication.

Who are the major players in the Quantum Communication Market?

Toshiba Corporation, ID Quantique, Thales Group, QuantumCTek Co. Ltd, Arqit Quantum Inc., ColdQuanta Inc., Excelitas Technologies, USTC, Atos, SK Telecom

Which segments covered the Quantum Communication Market?

Product Type(Software, Services, Hardware) Technology Type(Quantum Teleportation, Quantum Key Distribution (QKD)) Security Service(Network Security, Application Security) End-User(Banking & Financial Services, Telecommunications, Government & Defense, Other Applications)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Quantum Communication Market

Published Date : 12 Aug 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date