- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Quantum Dot Display Market Size, Share & Forecast | CAGR 17.5%

Global Quantum Dot Display Market Size, Share Analysis By Architecture (QLED, QD-OLED, NanoLED, Electroluminescent, LCD, MicroLED), By Material (Cadmium-Based, Cadmium-Free, Indium Phosphide, Graphene, Perovskite), By Application (TVs, Phones, Laptops, Monitors, Gaming, Automotive, AR/VR), By End-User, By Panel Size Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 1.70 Billion | USD 7.20 Billion | 17.5% | Asia Pacific, 40.0% |

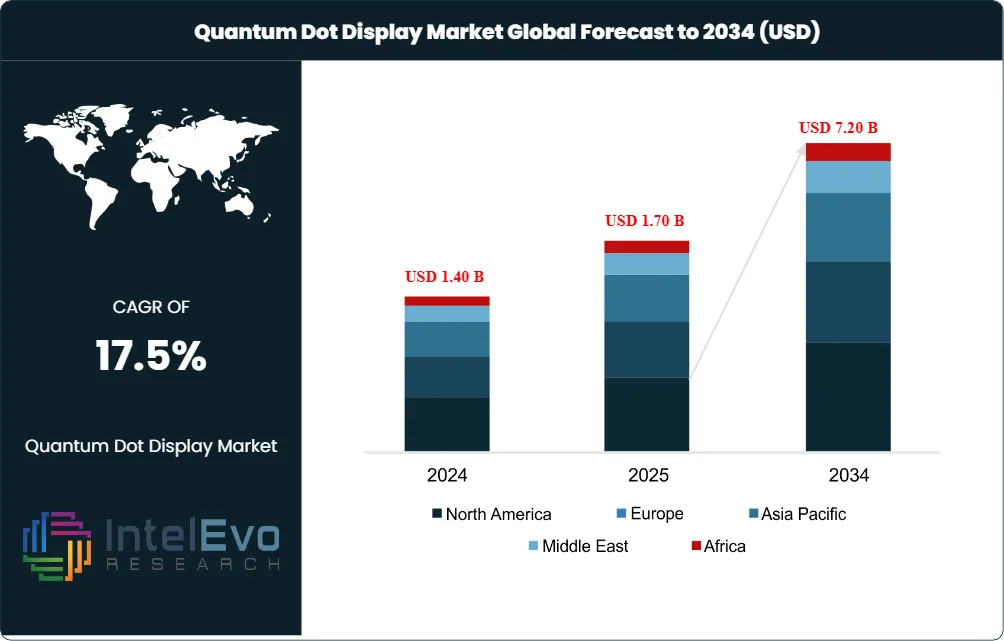

The Quantum Dot Display Market was valued at USD 1.40 Billion in 2024 and USD 1.70 Billion in 2025. The market is projected to reach USD 7.20 Billion by 2034, expanding at a CAGR of 17.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 5.50 Billion over the analysis period. Demand is driven by accelerating QD-OLED monitor shipments at Samsung Display, premium QLED TV adoption at Samsung Electronics and TCL, and direct alignment with EU RoHS cadmium-restriction mandates pushing the cadmium-free quantum dot share toward 75% of the materials market by 2027.

Get More Information about this report -

Request Free Sample ReportQuantum dot displays use semiconductor nanocrystals approximately 1.5 to 5 nanometers in diameter to produce pure monochromatic red, green, and blue light through quantum confinement effects. Samsung Display anchors the QD-OLED segment with 75% market share of OLED monitor panels in 2025 and cumulative QD-OLED monitor panel shipments exceeding 5 million units by March 2026. Samsung shipped 2.5 million QD-OLED monitor panels in 2025 alone. TCL CSOT, BOE Technology, AUO, Innolux, Sony, Sharp, Hisense, and Vizio anchor commercial QD-LCD, QD-Mini LED, and QD-OLED deployments. Cadmium-based quantum dots reached USD 957.8 Million in 2025 segment revenue, while cadmium-free indium phosphide formulations are accelerating regulatory-compliance migration.

QLED and QD enhancement film (QDEF) architectures captured approximately 35% of quantum dot display market revenue in 2025, anchored by widespread adoption in premium televisions and monitors. QD-OLED captured approximately 28% revenue share, anchored by Samsung Display's Asan campus expansion and February 2026's Penta Tandem branding announcement. QDEL and QD-LED architectures held approximately 12% emerging share, forecast as the fastest-growing segment at 15.7% CAGR through 2030 driven by Nanosys-Samsung commercialization targeting 2029. QD-MicroLED captured remaining emerging share.

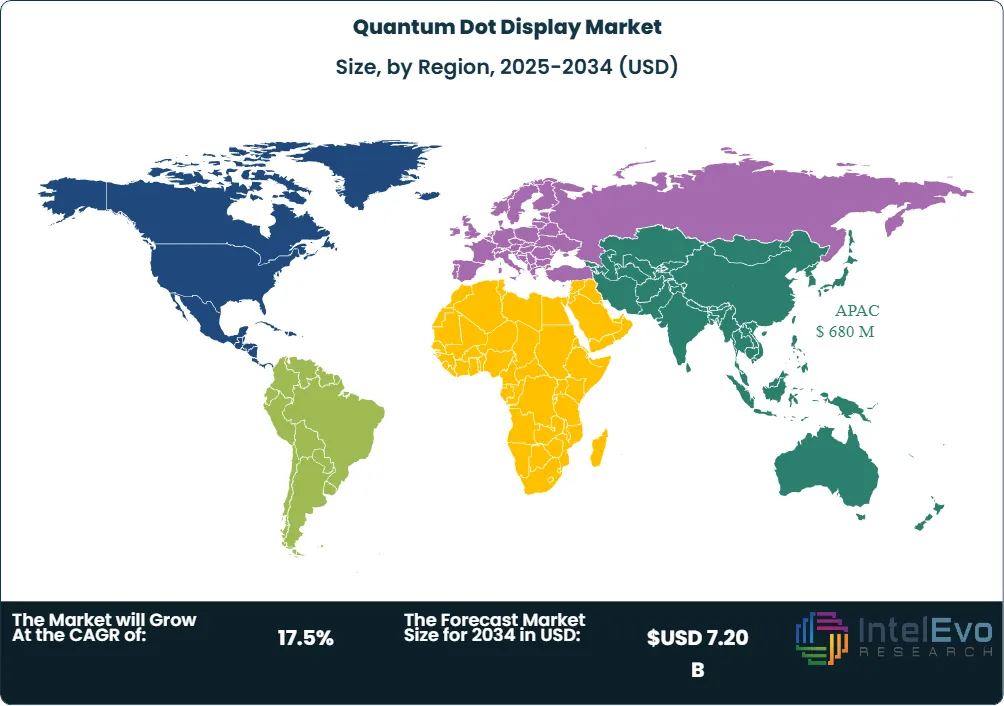

Asia Pacific led the quantum dot display market with approximately 40.0% revenue share in 2025, equivalent to roughly USD 680 Million in regional revenue, anchored by Samsung Display (Asan, South Korea), LG Display (Paju, South Korea), TCL CSOT (Shenzhen), BOE Technology (Beijing), Sony (Tokyo), and Sharp (Osaka) manufacturing concentration. North America captured 28.5% revenue share through Samsung Electronics, Vizio, and Nanosys. Europe captured 18% share through Merck KGaA, Nanoco Group, and German automotive demand. China and South Korea collectively account for approximately 60% of global QD display manufacturing capacity. February 2026's QD-OLED Penta Tandem launch and March 2026's Samsung QuantumBlack film redrew competitive positioning.

Market Definition & Scope

The quantum dot display market is defined as the global commercial activity covering quantum dot enhancement films (QDEF), QLED LCD displays, QD-OLED panels, QDEL/QD-LED self-emissive displays, QD-MicroLED panels, and the underlying quantum dot materials supply chain serving televisions, monitors, smartphones, tablets, automotive displays, commercial signage, and medical displays. The market includes Samsung Display QD-OLED Penta Tandem, LG Display QD-WOLED Tandem, TCL CSOT AMQLED and Super Quantum Dots (SQD), BOE Technology AMQLED, Sony Bravia QD-OLED, Sharp QD Mini-LED, AUO ALCD QD, Innolux QD LCD, Vizio Quantum Pro, and Hisense ULED X platforms.

This analysis includes both display panels and quantum dot material supply across cadmium-based quantum dots (USD 957.8 Million in 2025) and cadmium-free quantum dots. Excluded are non-quantum-dot OLED displays without QD color converters, traditional LCD displays without quantum dot enhancement, MicroLED displays without QD color conversion, and standalone quantum dot research applications outside the display industry. The quantum dot display market sits within the broader display panel parent market valued at approximately USD 165 Billion in 2025.

, By Material (Cadmium-Based, Cadmium-Free, Indium Phosphide, Graphene, Perovskite), By Application (TVs, Phones, Laptops, Monitors, Gaming, Automotive, AR/VR), By End-User, By Panel Size Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The quantum dot display market grew from USD 1.70 Billion in 2025 toward a forecast value of USD 7.20 Billion by 2034 at a 17.5% CAGR.

- Segment Dominance: QLED and QDEF architectures captured approximately 35% revenue share in 2025, anchored by Samsung Electronics, TCL, Hisense, and Vizio premium television deployments.

- Segment Dominance: Television applications held the largest 45.5% application share in 2025, with smartphones forecast as the fastest-growing application at 17.2% CAGR through 2030.

- Driver: Samsung Display reached 75% market share of OLED monitor panels in 2025, with cumulative QD-OLED monitor panel shipments exceeding 5 million units by March 2026.

- Restraint: Cadmium-based quantum dot regulatory restrictions under EU RoHS and accelerating cadmium-free migration constrain near-term cost economics, though cadmium-free will exceed 75% of materials market by 2027.

- Opportunity: QDEL/NanoLED self-emissive quantum dot displays represent the largest forecast-period opportunity, with Nanosys targeting 2029 commercialization at TVs and premium monitors.

- Trend: OLED penetration in the premium monitor segment above USD 500 grew from 14% in 2024 to 23% in 2025 and is forecast to reach 27% in 2026 per industry research.

- Regional: Asia Pacific led with 40.0% share in 2025, while China and South Korea collectively account for approximately 60% of global QD display manufacturing capacity.

Key Insights Summary

- Samsung Display launched QuantumBlack anti-reflective film technology for QD-OLED monitors on March 26, 2026, reducing light reflection by 20% and increasing surface hardness from 2H to 3H, deployed in 2026 ASUS, Gigabyte, and MSI monitors.

- Samsung Display unveiled QD-OLED Penta Tandem branding on February 12, 2026, built on a five-layer organic light-emitting structure delivering up to 1300 nits monitor brightness and 4500 nits TV brightness with doubled lifespan.

- Samsung Display revived QNED (quantum dot nanorod emitting diode) development in late 2025 per ETNews reporting from March 2026, with the QNED team regrouped following a breakthrough in QD nanorod arrangement.

- Samsung Display introduced V-Stripe RGB pixel structure for QD-OLED in January 2026, with the first 34-inch 360Hz panel entering mass production in December 2025 supplied to seven monitor makers including ASUS, MSI, and Gigabyte.

- Samsung Display invested USD 10.8 Billion in October 2019 to convert all 8G factories to QD-OLED production through 2025, anchoring the company's competitive moat in quantum dot display capacity.

- Nanosys announced via Insight Media in January 2026 that 2029 represents a realistic target for QDEL (NanoLED) commercialization, with BT.2020 Super Quantum Dots already deployed in TCL's 2026 X11L flagship TV.

- In March 2026, the Landgericht Munchen I ruled in favor of Samsung Electronics in a misleading-advertising case against TCL Deutschland, barring TCL from continuing to market certain TVs as QLED.

Competitive Landscape Overview

The quantum dot display market is highly consolidated, with the top two vendors (Samsung Display and LG Display) collectively representing an estimated 70% of 2025 revenue per industry analysis. Samsung Display anchors the dominant QD-OLED panel segment with 75% market share of OLED monitor panels in 2025, cumulative QD-OLED monitor panel shipments exceeding 5 million units by March 2026, and Penta Tandem five-layer branding launched February 2026. LG Display anchors the second-largest position through QD-WOLED Tandem panels and Q3 2025's multi-year contract to supply QD panels to Sony for the Bravia TV lineup.

Competitive evolution centers on emissive QD architecture maturity (QD-OLED, QDEL, QNED, QD-MicroLED), cadmium-free quantum dot material transition under regulatory pressure, and end-market expansion beyond television into monitors, smartphones, automotive displays, and AR/VR. TCL CSOT and BOE Technology anchor the Chinese AMQLED segment under Made in China 2025 mandates. Sony, Sharp, AUO, and Innolux anchor the broader Asia Pacific competitive set. Hisense and Vizio anchor commercial brand-level deployments. Strategic moves through 2025 included Samsung's Asan QD-OLED expansion, BOE-Nanosys supply agreement, TCL Shenzhen facility opening, and Sharp QD Mini-LED mass production.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Samsung Display | South Korea | Leader | QD-OLED Penta Tandem, V-Stripe RGB panels | Asia Pacific, North America, Europe | Mar 2026 launched QuantumBlack anti-reflective film tech |

| LG Display | South Korea | Leader | QD-WOLED Tandem panels, premium TV displays | Asia Pacific, North America, Europe | Q3 2025 secured Sony Bravia QD panel supply contract |

| TCL CSOT | China | Leader | AMQLED, QD-Mini LED, Super QD (SQD) panels | Asia Pacific, EMEA, North America | Q2 2025 opened new Shenzhen QD display facility |

| BOE Technology Group | China | Leader | AMQLED panels, QD enhancement films | Asia Pacific, EMEA | Q2 2025 multi-year Nanosys QD supply agreement |

| Sony Corporation | Japan | Challenger | Bravia QD-OLED TVs, professional reference monitors | Asia Pacific, North America, Europe | Q3 2025 sourced LG Display QD panels for Bravia |

| AUO Corporation | Taiwan | Challenger | ALCD QD panels, automotive QD displays | Asia Pacific, North America | Continued cadmium-free QD LCD expansion through 2025 |

| Sharp Corporation | Japan | Challenger | Quantum dot Mini-LED TVs, commercial displays | Asia Pacific, North America, Europe | Q3 2025 began QD Mini-LED TV mass production |

| Hisense | China | Challenger | ULED X QD-Mini LED TVs, commercial displays | Asia Pacific, EMEA, North America | Continued ULED X QD line expansion 2025 |

| Innolux Corporation | Taiwan | Niche Player | QD LCD panels, automotive displays | Asia Pacific, North America | Continued QD LCD automotive expansion 2025 |

| Vizio Inc. | USA | Niche Player | Quantum Pro QD-Mini LED TVs | North America | Continued North America QD-Mini LED expansion 2025 |

Segmentation Analysis

The quantum dot display market is segmented by display technology architecture, quantum dot material type, application, end-user industry, and panel size, each producing distinct competitive and adoption patterns across the forecast period.

By Display Technology Architecture

QLED and quantum dot enhancement film (QDEF) architectures captured approximately 35% of quantum dot display market revenue in 2025, anchored by Samsung Electronics QLED TVs, TCL C-series, Hisense ULED X, and Vizio Quantum Pro deployments. QD-OLED captured approximately 28% revenue share through Samsung Display panels supplied to Samsung Electronics, Sony Bravia, ASUS, Dell, Gigabyte, MSI, and Alienware. QDEL and QD-LED self-emissive architectures held approximately 12% emerging share, forecast at 15.7% CAGR through 2030. QD-Mini LED captured 18% share through TCL, Hisense, Sharp, and Vizio premium TV deployments. QD-MicroLED and other emerging architectures represented the remaining 7% share.

By Quantum Dot Material Type

Cadmium-based quantum dots captured approximately 56% of quantum dot display market materials revenue in 2025, equivalent to USD 957.8 Million, anchored by CdSe red and green emitters with established manufacturing maturity. Cadmium-free quantum dots using indium phosphide (InP), indium arsenide (InAs), and emerging perovskite alternatives held approximately 44% revenue share in 2025, with industry forecasts projecting cadmium-free dominance exceeding 75% of materials market by 2027 driven by EU RoHS Directive 2011/65/EU restrictions on cadmium content above 100 ppm. Samsung, TCL, Vizio, Nanoco Group, Merck KGaA, and Shoei Chemical anchor cadmium-free supply.

By Application

Television applications captured approximately 45.5% of quantum dot display market revenue in 2025, the largest application segment, anchored by Samsung QLED, Samsung S95H QD-OLED, TCL Q-series and X11L, Hisense ULED X, Sony Bravia 8 II, Sharp QD Mini-LED, and Vizio Quantum Pro deployments. PC monitors and IT computing displays held approximately 22% share, with Samsung Display capturing 75% of OLED monitor panel market in 2025. Smartphones captured approximately 12% share with the segment growing at a 17.2% CAGR through 2030. Automotive displays captured 8% share. Commercial signage held 7% share. Medical and industrial displays represented the remaining 5.5% share.

By End-User Industry

Consumer electronics captured approximately 50.4% of quantum dot display market revenue in 2025, the largest end-user vertical, anchored by Samsung Electronics, LG Electronics, TCL, Hisense, Sony, Sharp, Vizio, OnePlus, and Xiaomi. Consumer electronics manufacturers held a 38.3% share within the broader QLED segment per industry analysis. Healthcare captured the fastest-growing segment at 21.0% CAGR through 2030, anchored by QDI Systems medical imaging applications. Automotive captured 12% share, anchored by ADAS displays, in-cabin infotainment, and AR head-up displays. IT and telecommunications captured 14% share through enterprise-monitor deployments. Industrial applications represented the remaining 8% share.

By Panel Size

Large-format panels above 55 inches captured approximately 48% of quantum dot display market revenue in 2025, the dominant panel-size segment, anchored by Samsung S95H 55-77 inch QD-OLED, LG QD-WOLED, TCL X11L, and Sony Bravia 8 II flagship television deployments. Medium-format panels 27 to 49 inches captured approximately 32% share, anchored by Samsung Display QD-OLED monitor panels (27-inch 4K, 32-inch 4K, 34-inch WQHD, 49-inch ultrawide). Small-format panels under 27 inches held 14% share, anchored by smartphones, tablets, and automotive infotainment displays. Ultra-large above 77 inches captured the remaining 6% share.

Regional Analysis

The global quantum dot display market shows distinct regional revenue and growth profiles across North America, Europe, Asia Pacific, Latin America, and Middle East and Africa, with Asian manufacturing concentration and North American premium-consumer demand driving the geographic mix.

Asia Pacific

Asia Pacific led the quantum dot display market with 40.0% share in 2025, equivalent to approximately USD 680 Million in regional revenue. South Korea anchors regional supply through Samsung Display (Asan), LG Display (Paju), and Samsung Electronics QLED TV manufacturing. China contributes through TCL CSOT (Shenzhen), BOE Technology (Beijing), Hisense (Qingdao), Visionox, and Tianma Microelectronics under the Made in China 2025 strategy. Japan anchors supply through Sony (Tokyo) and Sharp (Osaka). Taiwan supports the global supply chain through AUO (Hsinchu) and Innolux (Miaoli). India contributes through emerging consumer electronics demand. China and South Korea collectively account for approximately 60% of global QD display manufacturing capacity.

North America

North America held approximately 28.5% of quantum dot display market revenue in 2025, equivalent to roughly USD 485 Million, anchored by U.S. premium-consumer demand at Samsung America, LG Electronics USA, Sony, TCL North America, Hisense USA, and Vizio. Vizio (Irvine, California) anchors domestic brand-level supply alongside Nanosys (Milpitas, California) quantum dot material leadership. The U.S. CHIPS and Science Act allocated USD 52 Billion through fiscal year 2027 for domestic semiconductor manufacturing. The U.S. Federal Trade Commission display-marketing-claims oversight following Samsung-TCL litigation patterns affects QLED labeling enforcement. Canada anchors regional demand through retail consumer electronics distribution. Mexico contributes through automotive display Tier-1 manufacturing.

Europe

Europe captured approximately 18% of quantum dot display market revenue in 2025, equivalent to roughly USD 305 Million. Germany anchors regional supply through Merck KGaA (Darmstadt) quantum dot material leadership and consumer demand at BMW, Mercedes-Benz, and Audi automotive display integration. The United Kingdom anchors supply through Nanoco Group plc (Manchester) cadmium-free quantum dot manufacturing. France, Italy, Spain, and the Nordics anchor consumer-electronics retail demand. The European Union RoHS Directive 2011/65/EU restricts cadmium content above 100 ppm, accelerating cadmium-free quantum dot adoption. The March 2026 Landgericht Munchen I ruling barring TCL Deutschland from QLED labeling validated regulatory enforcement of display marketing claims across European markets.

Latin America

Latin America accounted for approximately 8% of quantum dot display market revenue in 2025. Brazil leads regional adoption through Samsung Brazil, LG Brazil, and TCL Brazil consumer-electronics deployments at Magazine Luiza and Casas Bahia retail channels. Mexico contributes through Samsung de Mexico, LG Mexico, and Vizio distribution alongside automotive Tier-1 manufacturing supporting U.S. OEM supply chains. Argentina, Chile, Colombia, and Peru represent emerging demand pockets supported by rising middle-class consumer electronics adoption. Regional growth is constrained by import tariffs and currency volatility. Brazilian Development Bank (BNDES) financing supports gradual capacity additions through 2027.

Middle East & Africa

Middle East and Africa held approximately 5.5% of quantum dot display market revenue in 2025. The United Arab Emirates anchors regional demand through Samsung Gulf, LG Gulf, and TCL Middle East premium consumer-electronics deployments, with TCL launching the C6K QD-Mini LED TV range in the UAE in May 2025. Saudi Arabia anchors demand through Vision 2030 retail expansion. South Africa contributes through Samsung South Africa and LG Africa retail distribution. Israel, Turkey, Egypt, and Nigeria represent emerging demand pockets. Regional growth is supported by Vision 2030 mandates and rising premium-consumer-electronics retail penetration through 2030.

Country Analysis

China

China's quantum dot display market reached approximately USD 320 Million in 2025, with country CAGR tracking near 18% through 2034, the highest among major economies. Domestic supply concentrates at TCL CSOT (Shenzhen), BOE Technology (Beijing), Hisense (Qingdao), Visionox, and Tianma Microelectronics. China manufactured over 50% of global LCDs integrated with QD technology in 2024 per industry analysis. Demand concentrates at Samsung China, LG China, TCL Electronics, Hisense, Skyworth, and Konka premium TV deployments alongside smartphone adoption at Huawei, Xiaomi, OPPO, vivo, and Honor. The 14th Five-Year Plan and the Made in China 2025 strategy committed substantial state capital to display industry self-sufficiency. Q2 2025's TCL Shenzhen QD facility opening anchors continued domestic capacity expansion.

South Korea

South Korea's quantum dot display market reached approximately USD 280 Million in 2025, with country CAGR near 16% through 2034. Samsung Display (Asan campus) anchors global QD-OLED panel supply with 75% market share of OLED monitor panels in 2025, cumulative QD-OLED monitor panel shipments exceeding 5 million units by March 2026, and the USD 10.8 Billion 8G factory conversion investment announced in October 2019. LG Display (Paju) anchors QD-WOLED Tandem supply alongside the Q3 2025 Sony Bravia QD panel contract. Domestic demand concentrates at Samsung Electronics, LG Electronics, and emerging premium consumer brands. The Korean K-Chips Act and the K-Display strategy support display industry capacity expansion.

United States

The United States quantum dot display market reached approximately USD 250 Million in 2025, with country CAGR near 15% through 2034. Demand concentrates at Best Buy, Costco, Amazon, Walmart, and Target retail distribution alongside premium-consumer adoption of Samsung S95H, LG QD-WOLED, Sony Bravia 8 II, TCL X11L, Hisense ULED X, Sharp Aquos, and Vizio Quantum Pro deployments. Domestic supply concentrates at Vizio (Irvine, California), Nanosys (Milpitas, California) quantum dot material leadership, and emerging fabless QD startups. The CHIPS and Science Act allocated USD 52 Billion through fiscal year 2027. The U.S. FTC display-marketing-claims oversight following Samsung-TCL litigation patterns affects QLED labeling enforcement across the U.S. retail channel.

Japan

Japan's quantum dot display market reached approximately USD 180 Million in 2025, with country CAGR near 14% through 2034. Sony Corporation (Tokyo) anchors domestic supply through Bravia QD-OLED and professional reference monitor deployments, with the Q3 2025 multi-year LG Display QD panel supply contract anchoring premium TV portfolios. Sharp Corporation (Osaka) anchors domestic supply through QD Mini-LED TV mass production launched in Q3 2025. Domestic demand concentrates at Sony, Sharp, Panasonic, and Toshiba Visual Solutions premium consumer-electronics brands. The METI display industry strategy supports domestic display capacity. Quantum dot material supply chain integration through Shoei Chemical Industry and Mitsubishi Chemical supports domestic vertical capacity.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Display Technology Architecture

- Quantum Dot Light Emitting Diode (QLED) Displays

- Quantum Dot OLED (QD-OLED) Displays

- Quantum Dot NanoLED Displays

- Electroluminescent Quantum Dot (EL-QD) Displays

- Quantum Dot LCD Displays

- Quantum Dot MicroLED Displays

- Hybrid Quantum Dot Display Architectures

- Self-Emissive Quantum Dot Displays

- Others

By Quantum Dot Material Type

- Cadmium-Based Quantum Dots

- Cadmium-Free Quantum Dots

- Indium Phosphide (InP) Quantum Dots

- Graphene Quantum Dots

- Perovskite Quantum Dots

- Silicon Quantum Dots

- Carbon Quantum Dots

- Colloidal Quantum Dots

- Others

By Application

- Televisions

- Smartphones

- Laptops and Notebooks

- Monitors

- Tablets

- Smartwatches and Wearables

- Digital Signage Displays

- Gaming Displays

- Automotive Displays

- Medical Imaging Displays

- Industrial and Commercial Displays

- Augmented Reality (AR) and Virtual Reality (VR) Devices

- Others

By End-User Industry

- Consumer Electronics

- Automotive

- Healthcare

- Media and Entertainment

- Information Technology and Telecommunications

- Retail and Digital Advertising

- Education

- Industrial Manufacturing

- Aerospace and Defense

- Hospitality and Tourism

- Others

By Panel Size

- Below 32 Inches

- 32–50 Inches

- 51–65 Inches

- 66–75 Inches

- 76–85 Inches

- Above 85 Inches

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.70 B |

| Forecast Revenue (2034) | USD 7.20 B |

| CAGR (2025-2034) | 17.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Display Technology Architecture, (Quantum Dot Light Emitting Diode (QLED) Displays, Quantum Dot OLED (QD-OLED) Displays, Quantum Dot NanoLED Displays, Electroluminescent Quantum Dot (EL-QD) Displays, Quantum Dot LCD Displays, Quantum Dot MicroLED Displays, Hybrid Quantum Dot Display Architectures, Self-Emissive Quantum Dot Displays, Others), By Quantum Dot Material Type, (Cadmium-Based Quantum Dots, Cadmium-Free Quantum Dots, Indium Phosphide (InP) Quantum Dots, Graphene Quantum Dots, Perovskite Quantum Dots, Silicon Quantum Dots, Carbon Quantum Dots, Colloidal Quantum Dots, Others), By Application, (Televisions, Smartphones, Laptops and Notebooks, Monitors, Tablets, Smartwatches and Wearables, Digital Signage Displays, Gaming Displays, Automotive Displays, Medical Imaging Displays, Industrial and Commercial Displays, Augmented Reality (AR) and Virtual Reality (VR) Devices, Others), By End-User Industry, (Consumer Electronics, Automotive, Healthcare, Media and Entertainment, Information Technology and Telecommunications, Retail and Digital Advertising, Education, Industrial Manufacturing, Aerospace and Defense, Hospitality and Tourism, Others), By Panel Size, (Below 32 Inches, 32–50 Inches, 51–65 Inches, 66–75 Inches, 76–85 Inches, Above 85 Inches, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SAMSUNG DISPLAY CO., LTD., LG DISPLAY CO., LTD., TCL CHINA STAR OPTOELECTRONICS TECHNOLOGY (TCL CSOT), BOE TECHNOLOGY GROUP CO., LTD., SONY CORPORATION, SHARP CORPORATION, AUO CORPORATION, INNOLUX CORPORATION, TIANMA MICROELECTRONICS, VISIONOX TECHNOLOGY, HISENSE GROUP, VIZIO INC., NANOSYS INC. (SHOEI CHEMICAL), NANOCO GROUP PLC, MERCK KGAA, SHOEI CHEMICAL INDUSTRY CO., LTD., QD VISION (SAMSUNG), QDI SYSTEMS, QUANTUM MATERIALS CORP, AVANTAMA AG, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Material (Cadmium-Based, Cadmium-Free, Indium Phosphide, Graphene, Perovskite), By Application (TVs, Phones, Laptops, Monitors, Gaming, Automotive, AR/VR), By End-User, By Panel Size Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Material (Cadmium-Based, Cadmium-Free, Indium Phosphide, Graphene, Perovskite), By Application (TVs, Phones, Laptops, Monitors, Gaming, Automotive, AR/VR), By End-User, By Panel Size Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Material (Cadmium-Based, Cadmium-Free, Indium Phosphide, Graphene, Perovskite), By Application (TVs, Phones, Laptops, Monitors, Gaming, Automotive, AR/VR), By End-User, By Panel Size Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Quantum Dot Display Market?

The Global Quantum Dot Display Market was valued at USD 1.40 Billion in 2024 and USD 1.70 Billion in 2025, and is projected to reach USD 7.20 Billion by 2034, growing at a CAGR of 17.5% from 2026 to 2034. Market growth is driven by QLED displays, QD-OLED technology, consumer electronics demand, and advanced display innovations.

Who are the major players in the Quantum Dot Display Market?

SAMSUNG DISPLAY CO., LTD., LG DISPLAY CO., LTD., TCL CHINA STAR OPTOELECTRONICS TECHNOLOGY (TCL CSOT), BOE TECHNOLOGY GROUP CO., LTD., SONY CORPORATION, SHARP CORPORATION, AUO CORPORATION, INNOLUX CORPORATION, TIANMA MICROELECTRONICS, VISIONOX TECHNOLOGY, HISENSE GROUP, VIZIO INC., NANOSYS INC. (SHOEI CHEMICAL), NANOCO GROUP PLC, MERCK KGAA, SHOEI CHEMICAL INDUSTRY CO., LTD., QD VISION (SAMSUNG), QDI SYSTEMS, QUANTUM MATERIALS CORP, AVANTAMA AG, Others

Which segments covered the Quantum Dot Display Market?

By Display Technology Architecture, (Quantum Dot Light Emitting Diode (QLED) Displays, Quantum Dot OLED (QD-OLED) Displays, Quantum Dot NanoLED Displays, Electroluminescent Quantum Dot (EL-QD) Displays, Quantum Dot LCD Displays, Quantum Dot MicroLED Displays, Hybrid Quantum Dot Display Architectures, Self-Emissive Quantum Dot Displays, Others), By Quantum Dot Material Type, (Cadmium-Based Quantum Dots, Cadmium-Free Quantum Dots, Indium Phosphide (InP) Quantum Dots, Graphene Quantum Dots, Perovskite Quantum Dots, Silicon Quantum Dots, Carbon Quantum Dots, Colloidal Quantum Dots, Others), By Application, (Televisions, Smartphones, Laptops and Notebooks, Monitors, Tablets, Smartwatches and Wearables, Digital Signage Displays, Gaming Displays, Automotive Displays, Medical Imaging Displays, Industrial and Commercial Displays, Augmented Reality (AR) and Virtual Reality (VR) Devices, Others), By End-User Industry, (Consumer Electronics, Automotive, Healthcare, Media and Entertainment, Information Technology and Telecommunications, Retail and Digital Advertising, Education, Industrial Manufacturing, Aerospace and Defense, Hospitality and Tourism, Others), By Panel Size, (Below 32 Inches, 32–50 Inches, 51–65 Inches, 66–75 Inches, 76–85 Inches, Above 85 Inches, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date