- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Quantum Dot Material Market Size, Share & Forecast | CAGR 12.8%

Global Quantum Dot Material Market Size, Share, Growth Analysis By Material Type (Cadmium-Based QDs, Indium Phosphide QDs, Perovskite QDs, Carbon/Graphene QDs, Silicon QDs), By Product Form (QD Films, QD Solutions, LED Packages, Color Conversion Layers, Polymer Resins), By Application (Display, Solar Cells, Biomedical Imaging, Sensors), By End-Use Industry & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 6.42 Billion | USD 18.96 Billion | 12.8% | Asia Pacific, 52.4% |

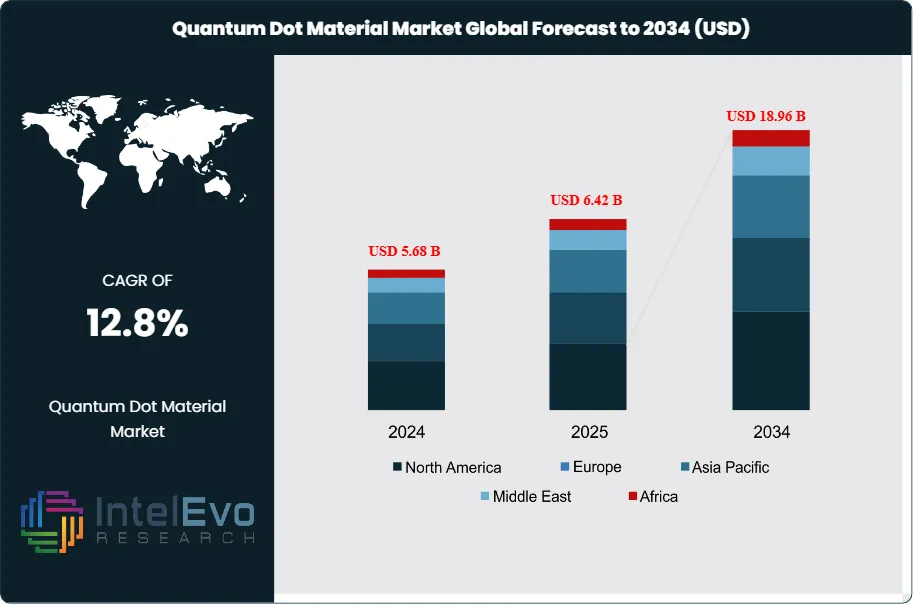

The Quantum Dot Material Market was valued at approximately USD 5.68 Billion in 2024 and reached USD 6.42 Billion in 2025. The market is projected to grow to USD 18.96 Billion by 2034, expanding at a CAGR of 12.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 12.54 Billion over the analysis period, driven by accelerating adoption of quantum dot-enhanced displays across consumer electronics, expanding solid-state lighting applications, emerging photovoltaic energy harvesting programs, and growing biomedical imaging deployment where quantum dots' size-tunable photoluminescence, narrow emission bandwidth, and high quantum yield deliver performance levels unattainable with conventional phosphors and organic fluorophores.

Get More Information about this report -

Request Free Sample ReportQuantum dots are semiconductor nanocrystals with diameters of 2-10 nanometers whose electronic and optical properties are governed by quantum confinement effects. When a quantum dot's physical dimensions approach the exciton Bohr radius of the semiconductor material, bandgap energy becomes size-dependent, enabling precise tuning of emission wavelength by controlling particle diameter during synthesis. A cadmium selenide (CdSe) quantum dot of 2 nm diameter emits blue light at approximately 480 nm; the same material at 6 nm emits red light at approximately 630 nm. This tunability, combined with full-width-at-half-maximum (FWHM) emission linewidths of 20-35 nm (versus 50-100 nm for traditional phosphors), enables quantum dot materials to produce ultra-high color saturation displays exceeding 99% of the DCI-P3 color gamut standard.

The quantum dot material market is dominated by display applications, which account for 72.5% of total revenue in 2025. Samsung Display's QD-OLED panel technology, which combines blue OLED emitters with cadmium-free InP quantum dot color conversion layers, has established the commercial benchmark for premium television, monitor, and laptop displays. Samsung shipped an estimated 3.2 million QD-OLED panels in 2024, consuming approximately 18 tonnes of InP quantum dot material. TCL CSOT and BOE Technology are developing competing QD-enhanced display architectures, with TCL's QD-Mini LED backlight systems capturing 14% of the global premium TV panel market in 2025.

The regulatory environment is a defining force in the quantum dot material market. The European Union's Restriction of Hazardous Substances (RoHS) Directive exemption for cadmium in display quantum dots, limited to 100 ppm cadmium per homogeneous material, has accelerated the industry transition from cadmium-based (CdSe) to cadmium-free indium phosphide (InP) quantum dots. The RoHS exemption for cadmium QDs expired for review in 2024, and industry consensus anticipates full phase-out of cadmium QD exemptions by 2027, effectively mandating InP or alternative cadmium-free quantum dot chemistries for any product sold in EU markets. This regulatory trajectory has redirected over USD 1.2 Billion in cumulative R&D investment toward cadmium-free QD synthesis, shell passivation, and film integration technologies since 2019.

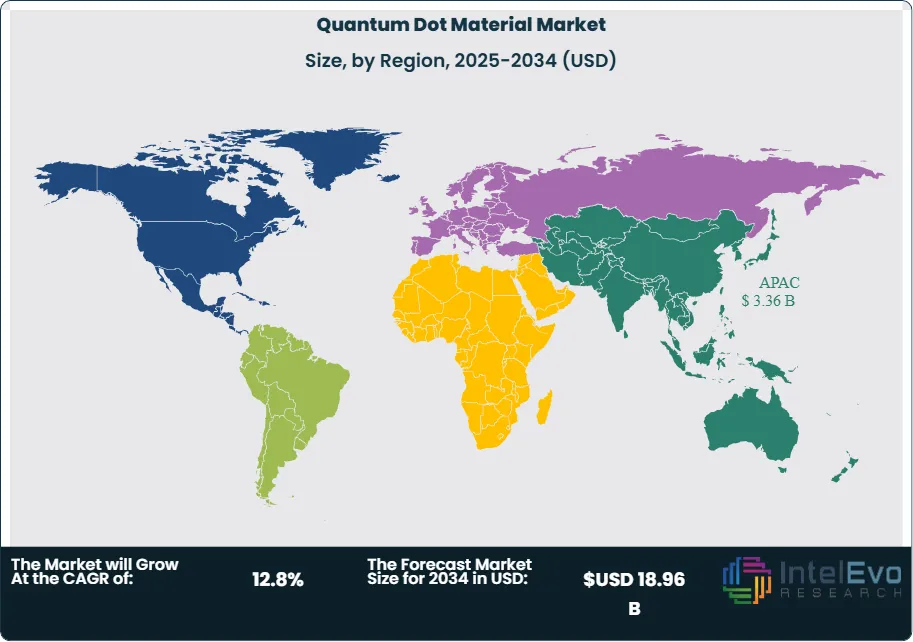

Regional dynamics in the quantum dot material market are heavily concentrated in Asia Pacific, which commands 52.4% of global revenue at USD 3.36 Billion in 2025. South Korea alone accounts for 48% of the Asia Pacific total, driven by Samsung Display and Samsung SDI's QD-OLED manufacturing ecosystem and Hansol Chemical's quantum dot film supply chain. China holds 28% of Asia Pacific share, with TCL CSOT, BOE, and emerging QD material suppliers building domestic supply capacity aligned with the Made in China 2025 advanced display initiative. North America at 24.8% (USD 1.59 Billion) is anchored by Nanosys, UbiQD, and a deep university research ecosystem generating QD material innovations that feed global commercial pipelines.

, By Product Form (QD Films, QD Solutions, LED Packages, Color Conversion Layers, Polymer Resins), By Application (Display, Solar Cells, Biomedical Imaging, Sensors), By End-Use Industry & Forecast 2026-2034")

Key Takeaways

- Market Growth: The quantum dot material market was valued at USD 6.42 Billion in 2025 and is projected to reach USD 18.96 Billion by 2034, expanding at a CAGR of 12.8% across the 2026-2034 forecast period.

- Segment Dominance: Indium phosphide (InP) quantum dots lead the By Material Type segment with 48.5% market share in 2025, valued at USD 3.11 Billion, driven by mandatory cadmium-free compliance under EU RoHS and consumer electronics OEM specification convergence on InP chemistry.

- Segment Dominance: Display applications dominate the By Application segment with 72.5% share in 2025, representing USD 4.65 Billion in revenue, anchored by Samsung QD-OLED panel production and TCL QD-Mini LED backlight systems across TV, monitor, and laptop product categories.

- Driver: Global premium display shipments exceeding 45 million QD-enhanced units in 2025, growing at 28% year-on-year, represent the primary demand driver, with each QD-OLED panel consuming 5-7 grams of quantum dot material at current film architectures.

- Restraint: Indium supply concentration, with 58% of global refined indium produced in China, creates raw material dependency risk and price volatility that increased InP quantum dot production costs by 14% between 2023 and 2025, constraining margin expansion for QD material suppliers.

- Opportunity: Quantum dot solar cells represent the largest emerging opportunity, with an estimated addressable market of USD 3.2 Billion by 2034, as perovskite-QD tandem architectures achieve certified power conversion efficiencies exceeding 30%, crossing the commercial viability threshold for utility-scale deployment.

- Trend: Electroluminescent quantum dot (QLED) direct-emission displays, eliminating the need for OLED or LED backlights, are the dominant technology trend, with Samsung, BOE, and TCL targeting commercial production of true-QLED panels by 2027-2028, a transition that would increase QD material consumption per display panel by 8-12x.

- Regional Analysis: Asia Pacific leads all regions with a 52.4% share in 2025, representing USD 3.36 Billion in revenue, driven by South Korea's QD-OLED manufacturing ecosystem, China's emerging QD material production base, and Japan's advanced QD laser and biomedical applications.

Competitive Landscape Overview

The quantum dot material market exhibits moderate concentration in 2025, with the top four participants — Samsung SDI/Display, Nanosys (Shoei Chemical), Hansol Chemical, and Merck KGaA — collectively commanding approximately 56% of global revenue. Competition is technology-driven, centered on quantum yield efficiency (target above 95% for display applications), emission linewidth (FWHM below 30 nm), cadmium-free material purity, and long-term photostability under continuous blue light excitation. The market structure is vertically stratified: Samsung operates as both the dominant QD material consumer and a key display panel producer; Nanosys and Hansol serve as the primary independent QD material suppliers; and Merck KGaA provides specialty QD materials for display and lighting OEMs globally. Patent litigation has been a competitive feature, with Nanoco's USD 150 Million settlement from Samsung in 2024 confirming the strategic value of QD intellectual property portfolios.

Competitive Landscape Matrix

| Company | HQ | Position | Key QD Product / Platform | Geo Strength | Recent Strategic Move (2024-2026) |

| Samsung SDI / Samsung Display | South Korea | Leader | Cadmium-Free QD-OLED Panels | Asia Pacific / Global | Commenced mass production of 3rd-generation QD-OLED panels at Asan facility (Q1 2025), achieving 2,000 nit peak brightness and 99.3% DCI-P3 color gamut coverage. |

| Nanosys (acquired by Shoei Chemical) | USA / Japan | Leader | Hyperion InP Quantum Dots | North America / Asia Pacific | Expanded InP quantum dot production capacity to 40 tonnes/year at Milpitas, CA facility (Mar 2025), supplying Samsung, TCL, and Hisense QD display programs. |

| Hansol Chemical | South Korea | Leader | Cadmium-Free QD Color Converter Films | Asia Pacific | Secured KRW 450B (USD 340M) multi-year supply contract with Samsung Display for QD color conversion films used in QD-OLED panels (Jun 2025). |

| Merck KGaA | Germany | Leader | isiphor Quantum Dot Materials | Europe / Global | Launched isiphor Red and Green InP quantum dot portfolio certified under EU RoHS and REACH for display and solid-state lighting applications (2025). |

| Nanoco Group plc | UK | Challenger | CFQD Cadmium-Free Quantum Dots | Europe / North America | Received USD 150M settlement from Samsung in IP litigation (2024) and reinvested proceeds into scaled CFQD production at Runcorn, UK facility targeting 20 tonnes/year capacity by 2026. |

| UbiQD Inc. | USA | Challenger | UbiGro Quantum Dot Films | North America | Deployed UbiGro luminescent greenhouse films across 2.4 million sq ft of controlled-environment agriculture in North America (2025), growing 82% year-on-year. |

| Quantum Solutions | Saudi Arabia | Niche Player | Perovskite Quantum Dots | Middle East | Commenced pilot production of lead-free perovskite quantum dots at Thuwal, Saudi Arabia facility (Q4 2025) targeting display backlight and solar concentrator applications. |

| OSRAM / ams-OSRAM | Germany / Austria | Challenger | QD-Enhanced Automotive Lighting | Europe / Global | Launched QD-enhanced micro-LED headlamp module achieving 150 lm/W efficacy for BMW iX platform (Jan 2026), the first automotive QD lighting application. |

| Crystalplex Corporation | USA | Niche Player | Core/Shell CdSe & InP QDs | North America | Expanded catalog quantum dot product line to 120 SKUs covering emission wavelengths from 450 nm to 800 nm for life sciences and display R&D applications (2025). |

| QD Laser Inc. | Japan | Niche Player | QD Laser Diodes & Retinal Displays | Asia Pacific | Received PMDA medical device approval for QD-based retinal laser projection eyewear for low-vision patients in Japan (Mar 2025). |

By Material Type:

Indium phosphide (InP) quantum dots command the largest segment share at 48.5% in 2025, valued at USD 3.11 Billion, reflecting the industry's accelerating transition from cadmium-based to cadmium-free quantum dot chemistries driven by EU RoHS compliance and OEM sustainability commitments. InP quantum dots achieve quantum yields of 85-95% with emission linewidths of 35-42 nm FWHM, narrower than organic phosphors but wider than CdSe alternatives, creating an ongoing R&D focus on InP core/shell engineering to close this performance gap. Cadmium-based quantum dots (CdSe, CdS, CdTe) hold 22.0% share at USD 1.41 Billion, maintaining relevance in research, biomedical imaging, and markets outside EU jurisdiction where RoHS restrictions do not apply. CdSe quantum dots deliver the highest performance metrics in the market: quantum yields above 98% and FWHM below 25 nm, but regulatory phase-out timelines are progressively constraining their commercial addressable market. Perovskite quantum dots represent 14.5% at USD 931 Million, the fastest-growing material type at an estimated CAGR of 22.4%, driven by exceptional defect tolerance, tunable bandgaps across the visible spectrum, and low-cost solution-phase synthesis. Carbon and graphene quantum dots account for 9.0% at USD 578 Million, valued for biocompatibility, chemical stability, and potential for heavy-metal-free fluorescence in biomedical and environmental sensing. Silicon quantum dots hold 6.0% at USD 385 Million, pursued for CMOS-compatible integration in photonic and sensing applications.

By Product Form:

QD films and sheets lead at 38.5% share, valued at USD 2.47 Billion in 2025, representing the dominant delivery format for display applications where quantum dot color conversion layers are laminated onto OLED or LED backlight sources. Hansol Chemical and Nanosys supply the majority of QD film volume consumed by Samsung Display and other panel manufacturers. QD solutions and dispersions hold 22.0% at USD 1.41 Billion, serving R&D, biomedical imaging, and coating applications requiring liquid-phase QD integration. QD-enhanced LED packages account for 18.5% at USD 1.19 Billion, used in QD-enhanced backlighting and solid-state lighting where quantum dots are encapsulated on-chip or in remote phosphor configurations. QD color conversion layers, distinct from films in that they are directly printed or deposited on display substrates, represent 14.0% at USD 899 Million, growing as inkjet-printed QD display manufacturing progresses. QD-embedded polymer resins hold 7.0% at USD 449 Million, used in agricultural luminescent films and specialty optical applications.

By Application:

Display applications dominate at 72.5% of the quantum dot material market, valued at USD 4.65 Billion in 2025. Within displays, QD-OLED panels represent the highest-value sub-segment at USD 2.1 Billion, followed by QD-enhanced Mini LED backlights at USD 1.6 Billion and QD-enhanced LCD backlights at USD 950 Million. Solid-state lighting holds 8.5% at USD 546 Million, with QD-enhanced LEDs achieving color rendering indices above 95 and luminous efficacies exceeding 150 lumens per watt for architectural, retail, and automotive lighting. Solar cells and photovoltaics represent 6.0% at USD 385 Million, driven by perovskite-QD tandem cell research achieving certified efficiencies above 30%. Biomedical imaging and diagnostics account for 5.5% at USD 353 Million, with QD fluorescent probes providing 10-100x brighter signals and 10-100x greater photostability versus organic fluorophores in multiplexed immunoassay, flow cytometry, and in vivo imaging. Sensors and photodetectors hold 4.0% at USD 257 Million. Lasers and optical communication represent 2.0% at USD 128 Million. Agriculture applications account for 1.5% at USD 96 Million.

By End-Use Industry:

Consumer electronics commands 68.0% of the quantum dot material market at USD 4.37 Billion in 2025, reflecting display dominance. Healthcare and life sciences hold 6.5% at USD 417 Million. Energy and solar represent 6.5% at USD 417 Million. Automotive accounts for 5.5% at USD 353 Million, with QD materials entering headlamp, instrument cluster, and head-up display applications. Agriculture holds 2.5% at USD 161 Million. Defense and aerospace represent 2.0% at USD 128 Million, consuming QD infrared photodetectors and narrow-band imaging sensors. Telecommunications account for 2.0% at USD 128 Million. Other industries represent 7.0% at USD 449 Million.

By Synthesis Method:

Colloidal hot-injection synthesis dominates at 52.0% of production volume, the gold standard for high-quality CdSe and InP quantum dots with controlled size distribution (polydispersity below 5%) and quantum yields above 90%. Heat-up non-injection methods hold 24.0%, favored for large-scale production due to simplified reactor design and batch scalability to 100+ kilogram runs. Aqueous synthesis represents 12.0%, used primarily for biocompatible quantum dot production for life sciences. Microfluidic synthesis accounts for 8.0%, enabling continuous-flow production with exceptional batch-to-batch reproducibility suited to pharmaceutical and diagnostic applications. Mechanochemical synthesis holds 4.0%, an emerging solvent-free method aligned with green chemistry principles.

Regional Analysis

Asia Pacific

Asia Pacific dominates the global quantum dot material market with a 52.4% share in 2025, valued at USD 3.36 Billion. South Korea is the single largest country market at 48% of regional revenue (USD 1.61 Billion), reflecting Samsung Display's position as the world's sole commercial QD-OLED panel manufacturer, Hansol Chemical's QD film production, and a concentrated supply chain of QD material, chemical precursor, and equipment suppliers clustered around the Chungcheong manufacturing corridor. South Korea's Ministry of Trade, Industry and Energy (MOTIE) designated quantum dot materials a national strategic technology under the K-Semiconductor Strategy, providing KRW 1.2 Trillion in R&D and capex incentives through 2030. China accounts for 28% of Asia Pacific revenue at USD 941 Million, driven by TCL CSOT and BOE Technology's QD-enhanced display panel programs, with BOE commissioning a QD-Mini LED production line in Hefei (2025) and the Chinese Academy of Sciences coordinating a national QD material development program under the 14th Five-Year Plan. Japan holds 16% at USD 538 Million, with QD Laser's medical device applications, Shoei Chemical's acquisition of Nanosys's Japanese operations, and active QD solar cell research at RIKEN and the University of Tokyo. India represents 5% at USD 168 Million, primarily in QD biomedical research and early-stage display component assembly. Asia Pacific is projected to grow at 13.4% CAGR to reach USD 10.28 Billion by 2034.

North America

North America accounts for 24.8% of the quantum dot material market in 2025, valued at USD 1.59 Billion. The United States dominates at 91% of regional revenue (USD 1.45 Billion), anchored by Nanosys (the largest independent QD material supplier globally), UbiQD (agricultural QD applications), Crystalplex (catalog QD products), and a research ecosystem spanning MIT, Los Alamos National Laboratory, and the National Renewable Energy Laboratory (NREL) that produces more QD-related publications and patents than any other country. The US Department of Energy (DOE) allocated USD 180 Million for QD solar cell and solid-state lighting research through the SunShot and SSL programs between 2022 and 2026. Canada holds 7% at USD 111 Million, with QD research programs at the National Research Council and University of Toronto contributing to solar cell and biomedical QD development. The CHIPS and Science Act, while primarily targeting semiconductor fabrication, includes provisions for advanced materials research that indirectly support QD manufacturing technology development. North America is forecast to grow at 12.2% CAGR to reach USD 4.56 Billion by 2034.

Europe

Europe represents 16.2% of the quantum dot material market in 2025, valued at USD 1.04 Billion. Germany leads at 32% of regional revenue (USD 333 Million), driven by Merck KGaA's isiphor quantum dot material platform, ams-OSRAM's QD-enhanced lighting products, and Fraunhofer Institute's QD application research programs. The United Kingdom holds 22% at USD 229 Million, anchored by Nanoco Group's CFQD production and a strong university research base at Imperial College London, University of Cambridge, and University of Manchester. France accounts for 15% at USD 156 Million, with CEA-LETI and CNRS advancing QD photodetector and display integration technologies. The Netherlands represents 12% at USD 125 Million, with Philips Lighting (Signify) and TNO conducting QD-enhanced lighting and solar cell research. The EU Horizon Europe program allocated EUR 85 Million to quantum dot research between 2021 and 2025, with a focus on cadmium-free materials aligned with REACH and RoHS regulatory trajectories. Europe is forecast to grow at 11.6% CAGR to reach USD 2.86 Billion by 2034.

Latin America

Latin America holds 3.8% of the quantum dot material market in 2025, valued at USD 244 Million. Brazil represents 52% of regional revenue at USD 127 Million, with QD-enhanced consumer electronics imports and early-stage QD solar cell research at the University of Sao Paulo. Mexico accounts for 30% at USD 73 Million, driven by consumer electronics display assembly and distribution. Chile contributes 10% at USD 24 Million, with copper indium gallium selenide (CIGS) and QD solar research programs supported by CORFO innovation funding. The region is predominantly a QD-enhanced product consumer rather than a QD material producer. Latin America is forecast to grow at 12.0% CAGR to reach USD 678 Million by 2034.

Middle East and Africa

Middle East and Africa accounts for 2.8% of the quantum dot material market in 2025, valued at USD 180 Million. Saudi Arabia leads at 40% of regional revenue (USD 72 Million), driven by Quantum Solutions' perovskite QD production facility at KAUST and Saudi Arabia's Vision 2030 advanced materials investment program. The UAE holds 28% at USD 50 Million, with QD-enhanced consumer electronics demand and IRENA-supported QD solar cell pilot programs. South Africa represents 18% at USD 32 Million. King Abdullah University of Science and Technology (KAUST) has emerged as a globally significant QD research center, producing over 200 peer-reviewed QD publications annually and supporting Quantum Solutions' commercialization of perovskite quantum dots. MEA is forecast to grow at 13.8% CAGR to reach USD 578 Million by 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Material Type

- Cadmium-Based QDs (CdSe, CdS, CdTe)

- Indium Phosphide (InP) QDs

- Perovskite QDs

- Carbon / Graphene QDs

- Silicon QDs

By Product Form

- QD Solutions / Dispersions

- QD Films / Sheets

- QD-Enhanced LED Packages

- QD Color Conversion Layers

- QD-Embedded Polymer Resins

By Application

- Display (TV, Monitor, Laptop, Mobile)

- Solid-State Lighting

- Solar Cells / Photovoltaics

- Biomedical Imaging & Diagnostics

- Sensors & Photodetectors

- Lasers & Optical Communication

- Agriculture (Luminescent Films)

By End-Use Industry

- Consumer Electronics

- Healthcare & Life Sciences

- Energy & Solar

- Automotive

- Agriculture

- Defense & Aerospace

- Telecommunications

By Synthesis Method

- Colloidal Synthesis (Hot Injection)

- Heat-Up / Non-Injection Method

- Aqueous Synthesis

- Microfluidic Synthesis

- Mechanochemical Synthesis

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.42 B |

| Forecast Revenue (2034) | USD 18.96 B |

| CAGR (2025-2034) | 12.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material Type, (Cadmium-Based QDs (CdSe, CdS, CdTe), Indium Phosphide (InP) QDs, Perovskite QDs, Carbon / Graphene QDs, Silicon QDs), By Product Form, (QD Solutions / Dispersions, QD Films / Sheets, QD-Enhanced LED Packages, QD Color Conversion Layers, QD-Embedded Polymer Resins), By Application, (Display (TV, Monitor, Laptop, Mobile), Solid-State Lighting, Solar Cells / Photovoltaics, Biomedical Imaging & Diagnostics, Sensors & Photodetectors, Lasers & Optical Communication, Agriculture (Luminescent Films)), By End-Use Industry, (Consumer Electronics, Healthcare & Life Sciences, Energy & Solar, Automotive, Agriculture, Defense & Aerospace, Telecommunications), By Synthesis Method, (Colloidal Synthesis (Hot Injection), Heat-Up / Non-Injection Method, Aqueous Synthesis, Microfluidic Synthesis, Mechanochemical Synthesis) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SAMSUNG SDI / SAMSUNG DISPLAY, MERCK KGAA, QUANTUM SOLUTIONS, QD LASER INC., AVANTAMA AG, NANOSYS (SHOEI CHEMICAL), NANOCO GROUP PLC, OSRAM / AMS-OSRAM, TCL CSOT, QUANTUM MATERIALS CORP., HANSOL CHEMICAL, UBIQD INC., CRYSTALPLEX CORPORATION, BOE TECHNOLOGY, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Product Form (QD Films, QD Solutions, LED Packages, Color Conversion Layers, Polymer Resins), By Application (Display, Solar Cells, Biomedical Imaging, Sensors), By End-Use Industry & Forecast 2026-2034")

, By Product Form (QD Films, QD Solutions, LED Packages, Color Conversion Layers, Polymer Resins), By Application (Display, Solar Cells, Biomedical Imaging, Sensors), By End-Use Industry & Forecast 2026-2034")

, By Product Form (QD Films, QD Solutions, LED Packages, Color Conversion Layers, Polymer Resins), By Application (Display, Solar Cells, Biomedical Imaging, Sensors), By End-Use Industry & Forecast 2026-2034")

Frequently Asked Questions

How big is the Quantum Dot Material Market?

The Global Quantum Dot Material Market was valued at USD 5.68 Billion in 2024 and is projected to reach USD 18.96 Billion by 2034, growing at a CAGR of 12.8% from 2026 to 2034, driven by increasing demand for advanced display technologies, rising adoption in photovoltaics and healthcare imaging, rapid advancements in nanotechnology, and expanding applications across consumer electronics, semiconductors, energy, and biomedical sectors.

Who are the major players in the Quantum Dot Material Market?

SAMSUNG SDI / SAMSUNG DISPLAY, MERCK KGAA, QUANTUM SOLUTIONS, QD LASER INC., AVANTAMA AG, NANOSYS (SHOEI CHEMICAL), NANOCO GROUP PLC, OSRAM / AMS-OSRAM, TCL CSOT, QUANTUM MATERIALS CORP., HANSOL CHEMICAL, UBIQD INC., CRYSTALPLEX CORPORATION, BOE TECHNOLOGY, OTHERS

Which segments covered the Quantum Dot Material Market?

By Material Type, (Cadmium-Based QDs (CdSe, CdS, CdTe), Indium Phosphide (InP) QDs, Perovskite QDs, Carbon / Graphene QDs, Silicon QDs), By Product Form, (QD Solutions / Dispersions, QD Films / Sheets, QD-Enhanced LED Packages, QD Color Conversion Layers, QD-Embedded Polymer Resins), By Application, (Display (TV, Monitor, Laptop, Mobile), Solid-State Lighting, Solar Cells / Photovoltaics, Biomedical Imaging & Diagnostics, Sensors & Photodetectors, Lasers & Optical Communication, Agriculture (Luminescent Films)), By End-Use Industry, (Consumer Electronics, Healthcare & Life Sciences, Energy & Solar, Automotive, Agriculture, Defense & Aerospace, Telecommunications), By Synthesis Method, (Colloidal Synthesis (Hot Injection), Heat-Up / Non-Injection Method, Aqueous Synthesis, Microfluidic Synthesis, Mechanochemical Synthesis)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date