- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Quantum Pharmaceutical Simulation Market Size, Share | CAGR 14.8%

Global Quantum Pharmaceutical Simulation Market Size, Share Analysis By Deployment (Cloud, On-Premises, Hybrid, QCaaS), By Processing (Gate-Based, Annealing, Classical-Hybrid, Superconducting, Trapped Ion, Photonic), By Stage (Target ID, Lead Optimization, Molecular Modeling, Protein Folding, Drug Repurposing), By Therapy (Oncology, Neurology, Cardiovascular, Infectious) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

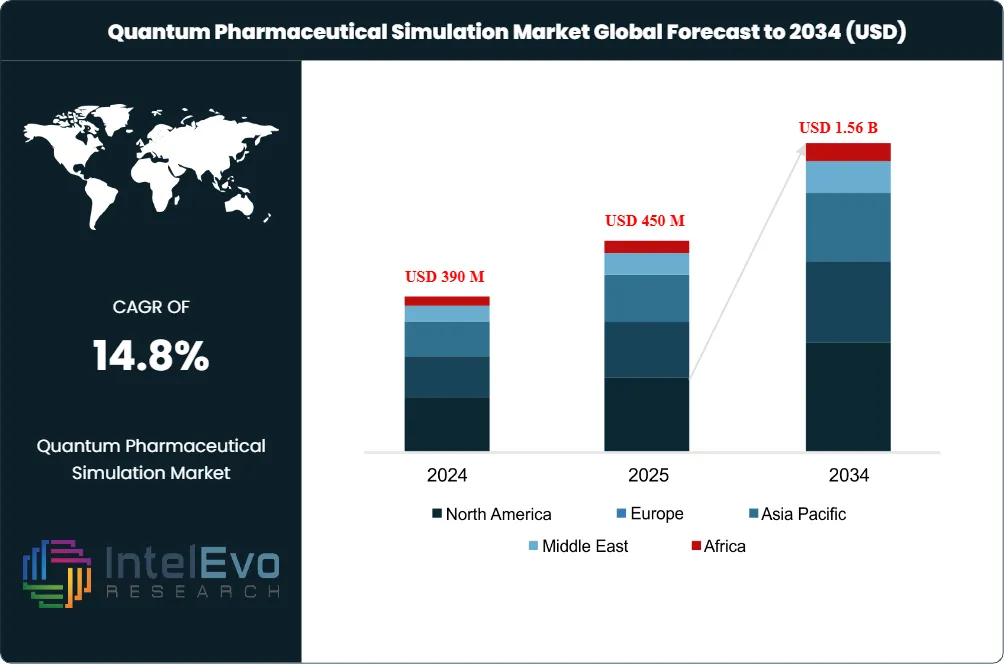

| USD 450 Million | USD 1.56 Billion | 14.8% | North America, 45.0% |

The Quantum Pharmaceutical Simulation Market was valued at USD 390 Million in 2024 and USD 450 Million in 2025. The market is projected to reach USD 1.56 Billion by 2034, expanding at a CAGR of 14.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.11 Billion over the analysis period. Demand is driven by pharmaceutical R&D pressure on shorter discovery timelines, rising hybrid quantum-classical workflow capability, and consolidating cloud access through IBM Quantum Network, Microsoft Azure Quantum Elements, AWS Braket, and Google Cloud Quantum Engine.

Get More Information about this report -

Request Free Sample ReportQuantum pharmaceutical simulation applies variational quantum eigensolvers (VQE), QAOA approximate-quantum algorithms, and quantum-classical hybrid workflows to molecular dynamics, protein-ligand binding, conformational analysis, and reaction-mechanism prediction tasks. Insilico Medicine's KRAS-focused project screened 100 million molecules on a combined classical-quantum workflow during 2025, illustrating scale advantages impossible for either approach alone. June 2025's IonQ partnership with AstraZeneca, Amazon Web Services, and NVIDIA demonstrated a quantum-accelerated computational chemistry workflow achieving more than 20-times speed improvement in molecular simulation, validating hybrid quantum-classical approaches for reaction modeling and drug development.

Cloud-based deployment held the largest 2025 share at approximately 68.3% of revenue because pharmaceutical companies prefer pay-per-use access over multimillion-dollar capital purchases of cryogenically cooled quantum hardware. Lead refinement captured the largest drug-discovery-stage share at 65.5% of 2025 revenue, addressing protein-ligand binding affinity refinement, off-target prediction, and ADMET property modeling. Oncology held 65.5% of therapeutic-area revenue in 2025, anchored by KRAS, EGFR, and tumor-microenvironment quantum simulations. Gate-model architectures led 2024 hardware revenue with 46.7%, reflecting compatibility with VQE central to quantum chemistry, while photonic systems are forecast to grow at 15.7% CAGR through 2030.

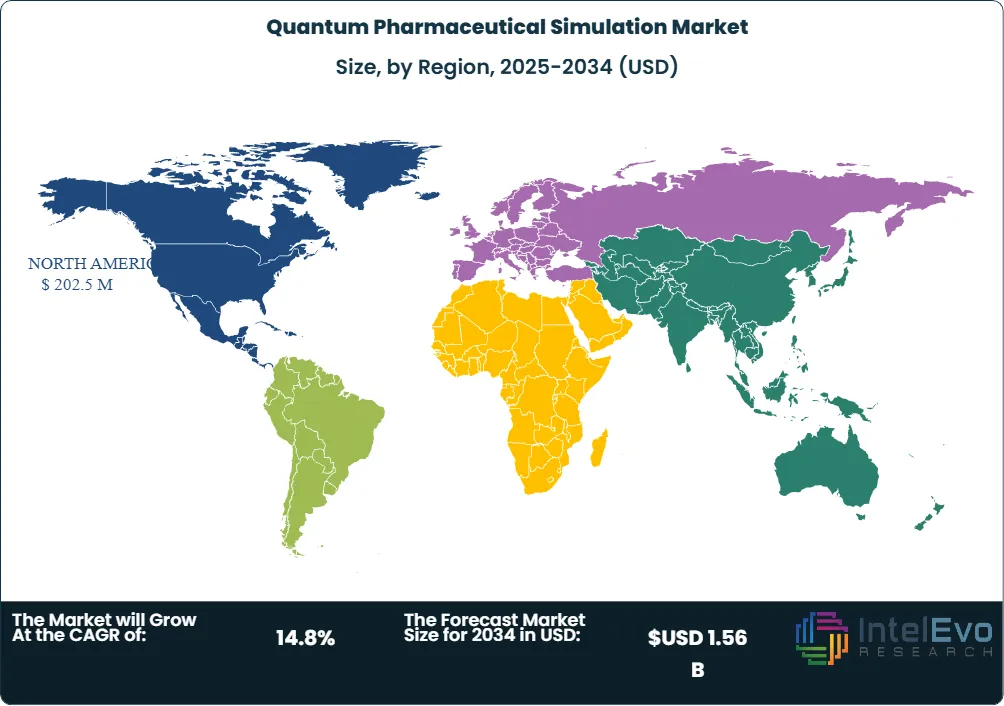

North America led the quantum pharmaceutical simulation market with 45.0% revenue share in 2025, equivalent to approximately USD 202.5 Million in regional revenue, anchored by IBM Yorktown Heights, Microsoft Redmond, IonQ College Park, AWS Center for Quantum Computing at Caltech, and the U.S. National Quantum Initiative. Asia Pacific captured the second-largest share and is forecast as the fastest-growing region at a 17.1% CAGR through 2030, propelled by China's quantum priority funding, Japan's METI Q-LEAP, and India's National Quantum Mission. PsiQuantum's March 2026 partnership with the National Cancer Center Japan, the August 2025 QIDO cloud platform launch by Mitsui & Co. with Quantinuum, and Qubit Pharmaceuticals' 2025 Sorbonne University Quantum AI model collectively redrew the competitive landscape.

Market Definition & Scope

The quantum pharmaceutical simulation market is defined as the global commercial activity covering quantum computing software, hardware access, and managed services applied to pharmaceutical molecular simulation, drug-target interaction prediction, conformational analysis, and quantum chemistry workloads. The market includes IBM Qiskit Chemistry, Microsoft Azure Quantum Elements, IonQ computational chemistry workflows, D-Wave hybrid solvers for molecular conformer clustering, Quantinuum InQuanto, Xanadu PennyLane chemistry modules, and specialized application platforms from Qubit Pharmaceuticals, SandboxAQ, and POLARISqb.

This analysis includes target identification, hit generation, lead refinement, ADMET prediction, biomarker discovery, and reaction-mechanism workloads delivered to pharmaceutical and biotechnology companies. Excluded are general quantum computing services without pharmaceutical-specific application focus, classical computational chemistry packages (Gaussian, Schrodinger, OpenMM) without quantum acceleration modules, post-quantum cryptography software, and pure pharmaceutical AI platforms without quantum computing components. The quantum pharmaceutical simulation market sits within the broader quantum computing parent market and represents the largest commercial application segment within healthcare and life sciences quantum spending.

, By Processing (Gate-Based, Annealing, Classical-Hybrid, Superconducting, Trapped Ion, Photonic), By Stage (Target ID, Lead Optimization, Molecular Modeling, Protein Folding, Drug Repurposing), By Therapy (Oncology, Neurology, Cardiovascular, Infectious) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The quantum pharmaceutical simulation market grew from USD 450 Million in 2025 toward a forecast value of USD 1.56 Billion by 2034 at a 14.8% CAGR.

- Segment Dominance: Cloud-based deployment captured approximately 68.3% revenue share in 2024, anchored by IBM Quantum Network, Microsoft Azure Quantum Elements, and AWS Braket access.

- Segment Dominance: Lead refinement held 65.5% of drug-discovery-stage revenue in 2025, addressing protein-ligand binding affinity, off-target prediction, and ADMET property modeling.

- Driver: Pharmaceutical R&D cost pressure is the primary driver, with industry analysis indicating average drug development costs exceeding USD 2.6 Billion per approved compound.

- Restraint: Hardware decoherence limits quantum circuit depth for complex molecules, restraining near-term whole-protein simulations to hybrid quantum-classical workflows through 2030.

- Opportunity: Hybrid quantum-classical workflows represent the largest forecast-period opportunity, with Insilico Medicine's KRAS project screening 100 million molecules on a combined classical-quantum workflow in 2025.

- Trend: Photonic quantum processors are gaining commercial momentum at a 15.7% forecast CAGR through 2030, supported by Xanadu Borealis and PsiQuantum room-temperature operation advantages.

- Regional: North America led with 45.0% share in 2025 equivalent to roughly USD 202.5 Million, while Asia Pacific is the fastest-growing region at a 17.1% forecast CAGR through 2030.

Key Insights Summary

- IonQ collaborated with AstraZeneca, Amazon Web Services, and NVIDIA in June 2025 to demonstrate a quantum-accelerated computational chemistry workflow achieving more than 20-times speed improvement in molecular simulation.

- PsiQuantum partnered with the National Cancer Center Japan in March 2026 to build fault-tolerant quantum algorithms with clinical applications targeting utility-scale oncology drug discovery.

- Mitsui & Co. Ltd., Quantum Simulation Technologies, and Quantinuum launched the QIDO cloud platform in August 2025 to improve molecular simulation and reaction analysis through quantum-classical hybrid technology.

- Insilico Medicine's KRAS-focused project screened 100 million molecules on a combined classical-quantum workflow during 2025, illustrating scale advantages impossible for either approach alone.

- Qubit Pharmaceuticals announced a Quantum AI model developed with Sorbonne University in 2025 to improve molecular modeling, with the company among the most directly specialized in quantum-physics-based drug design.

- POLARISqb secured DARPA funding in October 2025 to advance quantum computing applications in drug design, focusing on protein-protein interaction targeting.

- Microsoft expanded its 1910 Genetics partnership into a five-year commercial agreement in 2025 aimed at AI-driven pharmaceutical R&D using Azure Quantum Elements infrastructure.

Competitive Landscape Overview

The quantum pharmaceutical simulation market is moderately consolidated, with the top four vendors (IBM Corporation, Microsoft Corporation, IonQ Inc., and Qubit Pharmaceuticals) collectively representing an estimated 50 to 58% of 2025 revenue. IBM holds the leading position through IBM Quantum Network membership covering more than 250 organizations including Pfizer, Roche, Boehringer Ingelheim, and Mitsubishi Chemical. Microsoft Azure Quantum Elements anchors enterprise distribution with built-in chemistry workflow templates. IonQ's June 2025 AstraZeneca-AWS-NVIDIA collaboration demonstrated the most-cited quantum-pharmaceutical performance benchmark to date at more than 20-times classical speedup.

Competitive evolution centers on three axes: hybrid quantum-classical workflow integration, pharmaceutical-domain partnership depth, and dataset-and-algorithm proprietary positioning. SandboxAQ continued its Sanofi biomarker discovery partnership through 2025, extending the AQBioSim and AQChem simulation suites into clinical applications. Qubit Pharmaceuticals operates as the most directly specialized player at the application-layer end of the market through quantum-physics-based molecular design. POLARISqb secured DARPA funding in October 2025 for protein-protein interaction targeting. Strategic moves through 2025 included August 2025's IBM-AMD platform collaboration, August 2025's Mitsui-Quantinuum QIDO cloud launch, October 2025's GNQ Insilico-Mindlab Drug Assessment Platform partnership, and continued Rigetti collaborations with Riverlane and Astex Pharmaceuticals.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| IBM Corporation | USA | Leader | IBM Quantum, Heron R2, Qiskit Chemistry | North America, Europe | Aug 2025 collaborated with AMD on quantum platforms |

| Microsoft Corporation | USA | Leader | Azure Quantum Elements, Q# chemistry | North America, Europe | 2025 expanded 1910 Genetics 5-year agreement |

| IonQ Inc. | USA | Leader | Trapped-ion processors, computational chemistry | North America, Europe | Jun 2025 partnered with AstraZeneca, AWS, NVIDIA |

| Qubit Pharmaceuticals | France | Leader | Quantum AI molecular design, Atlas | Europe, North America | 2025 launched Quantum AI model with Sorbonne University |

| D-Wave Quantum Inc. | Canada | Challenger | Advantage2 annealer, hybrid solvers | North America, Europe | FY2025 reported USD 23.9M revenue across applications |

| Rigetti Computing | USA | Challenger | Ankaa-2 84-qubit, Novera 9-qubit, QCS | North America, Europe | Continued Astex Pharmaceuticals partnership through 2025 |

| Quantinuum Ltd. | UK/USA | Challenger | H2 trapped-ion, InQuanto chemistry | North America, Europe | Aug 2025 contributed to QIDO platform with Mitsui |

| SandboxAQ | USA | Niche Player | AQBioSim, AQChem simulation suites | North America, Europe | 2025 extended Sanofi biomarker discovery partnership |

| Xanadu Quantum Tech. | Canada | Niche Player | Photonic quantum, PennyLane chemistry | North America | Continued Menten AI drug discovery collaboration |

| PsiQuantum Corp. | USA | Niche Player | Photonic fault-tolerant quantum systems | North America, Asia Pacific | Mar 2026 partnered with National Cancer Center Japan |

Segmentation Analysis

The quantum pharmaceutical simulation market is segmented by deployment mode, quantum processing type, drug discovery stage, therapeutic area, and end-user, each producing distinct competitive and adoption patterns across the forecast period.

By Deployment Mode

Cloud-based deployment captured approximately 68.3% of quantum pharmaceutical simulation market revenue in 2024 because pharmaceutical and biotechnology customers prefer pay-per-use access over multimillion-dollar capital purchases of cryogenically cooled quantum hardware. IBM Quantum Network, Microsoft Azure Quantum Elements, AWS Braket, Google Cloud Quantum Engine, and IonQ Cloud anchor cloud-access revenue. On-premises deployment retains the remaining 31.7% revenue share, dominated by national-laboratory installations including Forschungszentrum Julich, RIKEN, and the U.K. National Quantum Computing Centre. Cloud is forecast to expand at a 16% CAGR through 2030 versus low-single-digit on-premises growth, driven by lower capital outlays and continuous solver-version updates.

By Quantum Processing Type

Gate-model architectures led the quantum pharmaceutical simulation market with approximately 46.7% revenue share in 2024, reflecting compatibility with variational quantum eigensolvers (VQE) central to quantum chemistry and the unitary coupled cluster (UCC) ansatz family used at IBM Heron R2, Google Willow, IonQ trapped-ion, and AWS Emerald systems. Quantum annealers held 23.1% share, supporting discrete combinatorial workloads such as conformer clustering and protein-folding minimum-energy state search at D-Wave. Simulator-oriented systems captured 18.5% share through Quantinuum InQuanto and IBM Aer for time-evolution studies of mid-size molecules. Photonic systems represent 11.7% revenue share with the highest forecast growth at 15.7% CAGR through 2030, driven by Xanadu Borealis room-temperature operation and PsiQuantum scale plans.

By Drug Discovery Stage

Lead refinement captured 65.5% of quantum pharmaceutical simulation market revenue in 2025, the largest drug-discovery-stage segment, addressing protein-ligand binding affinity refinement, off-target prediction, ADMET property modeling, and selectivity profiling. The stage commands the highest spending because cost-per-decision is greatest at lead refinement and quantum methods directly target the binding-energy-calculation bottleneck. Hit generation and lead identification held 18% share, anchored by virtual screening of compound libraries against curated protein targets. Target identification and validation captured 11% share, with the remaining 5.5% covering ADMET-only assessments and biomarker discovery. Lead refinement is forecast to retain segment leadership through 2030 because quantum chemistry calculations directly accelerate the binding-affinity scoring functions central to medicinal-chemistry decisions.

By Therapeutic Area

Oncology dominated the quantum pharmaceutical simulation market with approximately 65.5% therapeutic-area revenue share in 2025, anchored by KRAS, EGFR, BRAF, and tumor-microenvironment quantum simulations. The high global cancer burden continues to drive quantum adoption, with Insilico Medicine's KRAS-focused project screening 100 million molecules on a combined classical-quantum workflow during 2025. Central nervous system (CNS) disorders held 11% share through Alzheimer's, Parkinson's, and amyotrophic lateral sclerosis (ALS) target programs. Infectious diseases captured 8% share, with antimicrobial-resistance and antiviral protein-target work intensifying after the COVID-19 pandemic. Cardiovascular, immunological, gastrointestinal, dermatological, endocrine, musculoskeletal, and respiratory disorders together account for the remaining 15.5% therapeutic-area demand.

By End-User

Pharmaceutical companies controlled approximately 58% of quantum pharmaceutical simulation market revenue in 2025, anchored by Pfizer, Roche, Novartis, Boehringer Ingelheim, Merck, AstraZeneca, GSK, Eli Lilly, and Bristol Myers Squibb internal pilots. Biopharmaceutical companies held 19% share at Moderna, Genentech, Regeneron, Gilead Sciences, and Vertex Pharmaceuticals. Contract research organizations (CROs) including Charles River Laboratories, Evotec, and WuXi AppTec captured 12% share through service-delivery models for pharmaceutical clients. Research and academic institutes held 8% share, anchored by Memorial Sloan Kettering, Dana-Farber, the Francis Crick Institute, and RIKEN. Technology vendors and startups (SandboxAQ, Qubit Pharmaceuticals, POLARISqb, Insilico Medicine) held the remaining 3% through internal R&D revenue. Implementation timelines for production quantum pharmaceutical pilots typically run 12 to 24 months.

Regional Analysis

The global quantum pharmaceutical simulation market shows distinct regional revenue and growth profiles across North America, Europe, Asia Pacific, Latin America, and Middle East and Africa, with North American hyperscaler concentration and European academic-pharmaceutical density driving the geographic mix.

North America

North America led the quantum pharmaceutical simulation market with 45.0% share in 2025, equivalent to approximately USD 202.5 Million in regional revenue. The United States anchors regional demand through Pfizer, Merck, Eli Lilly, Bristol Myers Squibb, Moderna, and Regeneron pilot programs, alongside hyperscaler distribution through IBM, Microsoft, AWS, and Google Cloud. The U.S. National Quantum Initiative Act funded more than USD 1.2 Billion through fiscal year 2025, with DARPA selecting Microsoft for utility-scale quantum computer development. October 2025's POLARISqb DARPA award supports quantum drug-design research. Canada anchors regional supply through Xanadu Quantum Technologies (Toronto) and D-Wave Systems (Burnaby), supported by Innovation, Science and Economic Development Canada Quantum Strategy.

Europe

Europe held approximately 26% of quantum pharmaceutical simulation market revenue in 2025, valued near USD 117 Million. Germany leads regional demand through Boehringer Ingelheim, Bayer, and Merck KGaA pilot programs supported by the Munich Quantum Valley initiative. France anchors regional vendor supply through Qubit Pharmaceuticals (Paris), Pasqal (Massy), and the EUR 1.8 Billion Plan Quantique. The United Kingdom contributes through Quantinuum (Cambridge), the National Quantum Computing Centre, GSK pilots, and AstraZeneca quantum partnerships. Switzerland anchors demand through Roche and Novartis. The European Union Quantum Flagship committed EUR 1 Billion over ten years, while the European Medicines Agency framework supports regulatory acceptance of quantum-derived simulation evidence.

Asia Pacific

Asia Pacific captured approximately 22% of quantum pharmaceutical simulation market revenue in 2025, valued near USD 99 Million, and is forecast as the fastest-growing region at a 17.1% CAGR through 2030. Japan leads regional supply through Fujitsu-RIKEN's 256-qubit superconducting system and the August 2025 Mitsui-Quantum Simulation Technologies-Quantinuum QIDO cloud platform. PsiQuantum's March 2026 partnership with the National Cancer Center Japan extended regional engagement. China leads regional demand through Origin Quantum, WuXi AppTec, BeiGene, and Hengrui Pharmaceutical pilots. India anchors emerging supply through QpiAI (Bangalore) and the National Quantum Mission INR 6,003 Crore allocation, with Sun Pharmaceutical and Dr. Reddy's Laboratories anchoring domestic demand. South Korea contributes through Samsung Biologics and Celltrion.

Latin America

Latin America accounted for approximately 4% of quantum pharmaceutical simulation market revenue in 2025. Brazil leads regional adoption through EMS Pharmaceutical, Eurofarma, and the Oswaldo Cruz Foundation (Fiocruz) research-stage pilots. Mexico contributes through CINVESTAV academic collaborations with U.S. quantum vendors and Laboratorios PiSA pharmaceutical demand. Argentina, Chile, and Colombia represent emerging demand pockets supported by university research grants and limited commercial pharmaceutical pilots. Regional growth is constrained by limited domestic quantum hardware capacity and Spanish-language quantum chemistry toolchain coverage, although AWS Sao Paulo and Azure Brazil South cloud regions provide remote access for pharmaceutical pilots through 2027.

Middle East & Africa

Middle East and Africa held approximately 3% of quantum pharmaceutical simulation market revenue in 2025. The United Arab Emirates anchors regional demand through the Quantum Research Center at Technology Innovation Institute (Abu Dhabi) and emerging pharmaceutical-research partnerships. Saudi Arabia's KAUST quantum initiative and Vision 2030 healthcare investments drive secondary demand. Israel contributes through Quantum Machines, Classiq Technologies, and Teva Pharmaceutical Industries enterprise pilots. South Africa's national quantum technology initiative supports African demand through Aspen Pharmacare. Regional growth is constrained by limited specialized-talent depth and pharmaceutical-research scale, although Vision 2030 healthcare funding supports capacity additions through 2027.

Country Analysis

United States

The United States quantum pharmaceutical simulation market reached approximately USD 185 Million in 2025, with country CAGR tracking near 15.5% through 2034. Demand concentrates at Pfizer, Merck, Eli Lilly, Bristol Myers Squibb, Moderna, Regeneron, and Vertex Pharmaceuticals R&D pilot programs. Domestic supply concentrates at IBM (Yorktown Heights), Microsoft (Redmond), Google Quantum AI (Santa Barbara), IonQ (College Park), Rigetti (Berkeley), AWS (Pasadena), QuEra (Boston), and SandboxAQ (Palo Alto). The U.S. National Quantum Initiative Act funded more than USD 1.2 Billion through fiscal year 2025, with DARPA October 2025 awards to POLARISqb and continued NIH research grants supporting academic-industry collaboration. June 2025's IonQ-AstraZeneca-AWS-NVIDIA collaboration demonstrated more than 20-times speed improvement in molecular simulation.

Germany

Germany's quantum pharmaceutical simulation market reached approximately USD 35 Million in 2025, with country CAGR near 16% through 2034. Boehringer Ingelheim, Bayer, and Merck KGaA anchor pharmaceutical demand through internal quantum pilots and IBM Quantum Network membership. The Federal Ministry of Education and Research (BMBF) committed EUR 3 Billion through 2026 for quantum technology, with the Munich Quantum Valley initiative anchoring regional infrastructure. The IBM Quantum System Two installation at Forschungszentrum Julich anchors regional cloud access for German pharmaceutical R&D. The European Medicines Agency framework supports regulatory acceptance of quantum-derived simulation evidence. Domestic biotech demand at MorphoSys, BioNTech, and Evotec extends commercial pipeline through 2030.

Japan

Japan's quantum pharmaceutical simulation market reached approximately USD 38 Million in 2025, the largest single-country market within Asia Pacific with country CAGR near 16% through 2034. Pharmaceutical demand concentrates at Takeda Pharmaceutical, Astellas, Daiichi Sankyo, Eisai, and Otsuka Pharmaceutical for oncology and CNS programs. August 2025's QIDO cloud platform launch by Mitsui & Co. with Quantum Simulation Technologies and Quantinuum specifically targets molecular simulation and reaction analysis for Japanese pharmaceutical R&D. PsiQuantum's March 2026 partnership with the National Cancer Center Japan validates utility-scale fault-tolerant quantum oncology research. The METI Q-LEAP program and Cabinet Office Moonshot Goal 6 target fault-tolerant quantum computing by 2050.

United Kingdom

The United Kingdom quantum pharmaceutical simulation market reached approximately USD 28 Million in 2025, with country CAGR near 15% through 2034. Pharmaceutical demand concentrates at AstraZeneca, GSK, and emerging biotech companies through partnerships with Quantinuum (Cambridge), Oxford Quantum Circuits, and the National Quantum Computing Centre (NQCC). The National Quantum Strategy committed GBP 2.5 Billion through 2033, anchoring regional infrastructure. AstraZeneca's June 2025 collaboration with IonQ, AWS, and NVIDIA demonstrated quantum-accelerated computational chemistry achieving more than 20-times speed improvement. The Medicines and Healthcare products Regulatory Agency (MHRA) post-Brexit framework supports regulatory acceptance of quantum-simulation evidence in drug submissions.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Deployment Mode

- Cloud-Based Deployment

- On-Premises Deployment

- Hybrid Deployment

- Multi-Cloud Deployment

- Quantum Computing as a Service (QCaaS)

- Others

By Quantum Processing Type

- Gate-Based Quantum Computing

- Quantum Annealing

- Hybrid Quantum-Classical Computing

- Superconducting Quantum Processing

- Trapped Ion Quantum Processing

- Photonic Quantum Computing

- Neutral Atom Quantum Computing

- Topological Quantum Computing

- Others

By Drug Discovery Stage

- Target Identification and Validation

- Hit Identification

- Lead Discovery

- Lead Optimization

- Preclinical Research

- Molecular Modeling and Simulation

- Protein Folding and Structure Prediction

- Drug Repurposing

- Biomarker Discovery

- Clinical Trial Design and Optimization

- Others

By Therapeutic Area

- Oncology

- Neurology

- Cardiovascular Diseases

- Infectious Diseases

- Immunology

- Rare Diseases

- Metabolic Disorders

- Respiratory Diseases

- Genetic and Genomic Disorders

- Autoimmune Diseases

- Central Nervous System (CNS) Disorders

- Others

By End-User

- Pharmaceutical Companies

- Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic and Research Institutions

- Government Research Organizations

- Healthcare and Life Sciences Organizations

- Quantum Computing Service Providers

- Drug Discovery Startups

- Clinical Research Organizations

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 450 M |

| Forecast Revenue (2034) | USD 1.56 B |

| CAGR (2025-2034) | 14.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment Mode, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment, Multi-Cloud Deployment, Quantum Computing as a Service (QCaaS), Others), By Quantum Processing Type, (Gate-Based Quantum Computing, Quantum Annealing, Hybrid Quantum-Classical Computing, Superconducting Quantum Processing, Trapped Ion Quantum Processing, Photonic Quantum Computing, Neutral Atom Quantum Computing, Topological Quantum Computing, Others), By Drug Discovery Stage, (Target Identification and Validation, Hit Identification, Lead Discovery, Lead Optimization, Preclinical Research, Molecular Modeling and Simulation, Protein Folding and Structure Prediction, Drug Repurposing, Biomarker Discovery, Clinical Trial Design and Optimization, Others), By Therapeutic Area, (Oncology, Neurology, Cardiovascular Diseases, Infectious Diseases, Immunology, Rare Diseases, Metabolic Disorders, Respiratory Diseases, Genetic and Genomic Disorders, Autoimmune Diseases, Central Nervous System (CNS) Disorders, Others), By End-User, (Pharmaceutical Companies, Biotechnology Companies, Contract Research Organizations (CROs), Academic and Research Institutions, Government Research Organizations, Healthcare and Life Sciences Organizations, Quantum Computing Service Providers, Drug Discovery Startups, Clinical Research Organizations, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | IBM CORPORATION, MICROSOFT CORPORATION, IONQ INC., QUBIT PHARMACEUTICALS, GOOGLE LLC (ALPHABET INC.), AMAZON WEB SERVICES INC., D-WAVE QUANTUM INC., RIGETTI COMPUTING INC., QUANTINUUM LTD., SANDBOXAQ, XANADU QUANTUM TECHNOLOGIES, PSIQUANTUM CORP., QUERA COMPUTING INC., POLARISQB INC., INSILICO MEDICINE, ZAPATA COMPUTING INC., 1QBIT INFORMATION TECHNOLOGIES, FUJITSU LIMITED, QUANTUM BRILLIANCE PTY LTD, MENTEN AI INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Processing (Gate-Based, Annealing, Classical-Hybrid, Superconducting, Trapped Ion, Photonic), By Stage (Target ID, Lead Optimization, Molecular Modeling, Protein Folding, Drug Repurposing), By Therapy (Oncology, Neurology, Cardiovascular, Infectious) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Processing (Gate-Based, Annealing, Classical-Hybrid, Superconducting, Trapped Ion, Photonic), By Stage (Target ID, Lead Optimization, Molecular Modeling, Protein Folding, Drug Repurposing), By Therapy (Oncology, Neurology, Cardiovascular, Infectious) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Processing (Gate-Based, Annealing, Classical-Hybrid, Superconducting, Trapped Ion, Photonic), By Stage (Target ID, Lead Optimization, Molecular Modeling, Protein Folding, Drug Repurposing), By Therapy (Oncology, Neurology, Cardiovascular, Infectious) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Quantum Pharmaceutical Simulation Market?

The Global Quantum Pharmaceutical Simulation Market was valued at USD 390 Million in 2024 and USD 450 Million in 2025, and is projected to reach USD 1.56 Billion by 2034, growing at a CAGR of 14.8% from 2026 to 2034. Market growth is driven by increasing adoption of quantum computing for drug discovery, molecular simulation, and pharmaceutical research.

Who are the major players in the Quantum Pharmaceutical Simulation Market?

IBM CORPORATION, MICROSOFT CORPORATION, IONQ INC., QUBIT PHARMACEUTICALS, GOOGLE LLC (ALPHABET INC.), AMAZON WEB SERVICES INC., D-WAVE QUANTUM INC., RIGETTI COMPUTING INC., QUANTINUUM LTD., SANDBOXAQ, XANADU QUANTUM TECHNOLOGIES, PSIQUANTUM CORP., QUERA COMPUTING INC., POLARISQB INC., INSILICO MEDICINE, ZAPATA COMPUTING INC., 1QBIT INFORMATION TECHNOLOGIES, FUJITSU LIMITED, QUANTUM BRILLIANCE PTY LTD, MENTEN AI INC., Others

Which segments covered the Quantum Pharmaceutical Simulation Market?

By Deployment Mode, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment, Multi-Cloud Deployment, Quantum Computing as a Service (QCaaS), Others), By Quantum Processing Type, (Gate-Based Quantum Computing, Quantum Annealing, Hybrid Quantum-Classical Computing, Superconducting Quantum Processing, Trapped Ion Quantum Processing, Photonic Quantum Computing, Neutral Atom Quantum Computing, Topological Quantum Computing, Others), By Drug Discovery Stage, (Target Identification and Validation, Hit Identification, Lead Discovery, Lead Optimization, Preclinical Research, Molecular Modeling and Simulation, Protein Folding and Structure Prediction, Drug Repurposing, Biomarker Discovery, Clinical Trial Design and Optimization, Others), By Therapeutic Area, (Oncology, Neurology, Cardiovascular Diseases, Infectious Diseases, Immunology, Rare Diseases, Metabolic Disorders, Respiratory Diseases, Genetic and Genomic Disorders, Autoimmune Diseases, Central Nervous System (CNS) Disorders, Others), By End-User, (Pharmaceutical Companies, Biotechnology Companies, Contract Research Organizations (CROs), Academic and Research Institutions, Government Research Organizations, Healthcare and Life Sciences Organizations, Quantum Computing Service Providers, Drug Discovery Startups, Clinical Research Organizations, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Quantum Pharmaceutical Simulation Market

Published Date : 18 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date