- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Quantum Radar Market Size, Share & Forecast 2034 | CAGR 8.5%

Global Quantum Radar Market Size, Share Analysis By Type (Entanglement-Based, Illumination, Photon Detection, Superconducting, Hybrid, Microwave), By Application (Military Surveillance, Missile Tracking, Stealth Detection, Border Security, Maritime, Air Traffic, Space Situational Awareness), By End-User (Defense, Government, Aerospace, Research, Space Agencies), By Platform (Ground, Airborne, Naval, Space) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

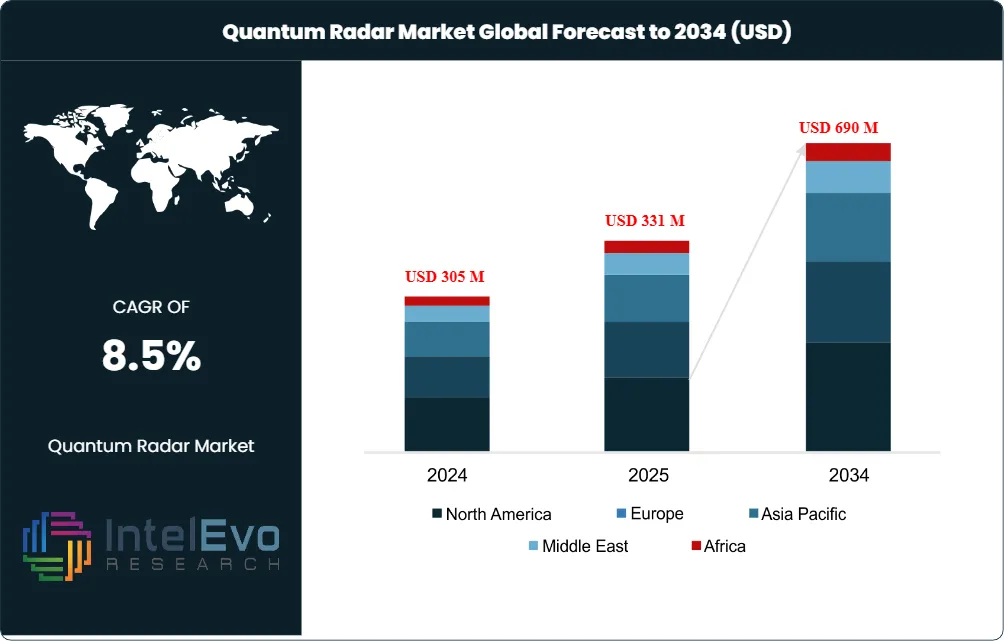

| USD 331 Million | USD 690 Million | 8.5% | North America, 36.5% |

The Quantum Radar Market was valued at USD 305 Million in 2024 and USD 331 Million in 2025. The market is projected to reach USD 690 Million by 2034, expanding at a CAGR of 8.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 359 Million over the analysis period. The Quantum Radar Market remains an emerging defense-electronics category, sitting at the intersection of single-photon detection, quantum entanglement physics, and conventional microwave radar engineering.

Get More Information about this report -

Request Free Sample ReportDemand is concentrated in stealth-detection use cases where conventional X-band and S-band radars face declining cross-section returns. The U.S. Department of Defense allocated more than USD 700 Million toward quantum-related R&D under FY 2025 budget lines, while the Department of Energy Quantum Leadership Act of 2025 proposed USD 2.5 Billion across fiscal years 2026-2030 for quantum information science programs.

Regulatory momentum accelerated in early 2026. The White House began drafting an executive order in February 2026 to update the 2018 National Quantum Strategy, directing OSTP, Commerce, Energy, and Defense to expand quantum sensing infrastructure within 180 days. Canada committed CAD 900 Million in March 2026 through its Defence Industrial Strategy. The Indian Navy launched a Sovereign Quantum Radar challenge under the ADITI 4.0 framework on March 17, 2026 with INR 25 Crore prize funding.

Technology dynamics favor entangled-photon architectures and quantum-illumination front ends. China Electronics Technology Group Corporation began mass production of a four-channel ultra-low-noise single-photon detector at its Anhui Province center on October 14, 2025, removing a major component bottleneck. The DARPA Robust Quantum Sensors program entered Phase 1 in August 2025 with helicopter-borne demonstrations across Q-CTRL, Lockheed Martin Corporation, and Safran Federal Systems.

Regionally, North America holds the largest share at 36.5% in 2025, supported by DARPA, the Office of Naval Research, and the Missile Defense Agency. Asia Pacific follows at 33.0%, driven by the People's Republic of China and the 14th Research Institute of CETC. Europe contributes 19.5% under the EU Quantum Flagship. The forecast through 2034 reflects steady defense modernization spending, even after the Defense Science Board January 14, 2026 report cautioned that pure-play quantum radars may not deliver decisive military advantage absent hybrid quantum-classical fusion.

Market Definition & Scope

The Quantum Radar Market is defined as the global commercial and government activity in the design, manufacture, and deployment of radar systems that exploit quantum-mechanical phenomena, including entanglement, quantum illumination, photon-number squeezing, and single-photon detection, to improve target detection beyond classical Cramer-Rao bounds. The market encompasses entangled-photon transmitters, single-photon avalanche diode receivers, cryogenic photonic integrated circuits, quantum signal processors, and the systems integration revenue tied to airborne, ground-based, naval, and space-based platforms.

The scope of this analysis includes microwave-frequency quantum radar, optical quantum radar, hybrid quantum-classical detection chains, and quantum-enhanced LiDAR when fielded for radar-equivalent target tracking. Excluded from scope are conventional active electronically scanned array radars without quantum enhancement, gravity gradiometers used solely for navigation, atomic-clock-based positioning systems, and quantum key distribution links that perform no detection function. The Quantum Radar Market is a sub-segment of the broader USD 1.4 Billion quantum detector market and the USD 435 Million quantum sensors market reported by the QED-C Hyperion Research study for 2024.

, By Application (Military Surveillance, Missile Tracking, Stealth Detection, Border Security, Maritime, Air Traffic, Space Situational Awareness), By End-User (Defense, Government, Aerospace, Research, Space Agencies), By Platform (Ground, Airborne, Naval, Space) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Quantum Radar Market expands from USD 331 Million in 2025 to USD 690 Million by 2034, registering a CAGR of 8.5%.

- Segment Dominance by Type: Quantum Illumination Radar leads with approximately 42.5% revenue share in 2025, driven by demonstrated noise-rejection performance in laboratory and short-range field tests.

- Segment Dominance by Application: Military Defense (Stealth Detection) accounts for approximately 58.5% of 2025 revenue, anchored by U.S. Department of Defense and People's Liberation Army funding pipelines.

- Driver: Anti-stealth detection requirements drive demand growth, with global military spending exceeding USD 2.4 Trillion in 2024 per SIPRI data and approximately 12% directed at sensor and electronic warfare modernization.

- Restraint: Cryogenic cooling, photon decoherence over distance, and signal-to-noise scaling limit current operational ranges to roughly 100 kilometers in optimal lab conditions, restraining near-term naval and ballistic-missile-defense deployment.

- Opportunity: GPS-denied navigation and contested-airspace ISR represent an addressable opportunity exceeding USD 200 Million across 2025-2034, validated by the DARPA RoQS program and the Indian Navy Sovereign Quantum Radar challenge.

- Trend: Mass production of four-channel single-photon detectors at China's Quantum Information Engineering Technology Research Center in October 2025 is shifting the cost curve, with industry analysis indicating component price declines exceeding 30% for entangled-photon source modules across 2024-2026.

- Regional: North America held the largest revenue share at 36.5% in 2025 with USD 120.8 Million, while Asia Pacific captured 33.0% with USD 109.2 Million.

Key Insights Summary

- Quantum Radar Market shipments measured in operational units remain below 200 worldwide in 2025, with most installations classified as prototype under DARPA, Defence Research and Development Canada, and CETC research programs.

- China Electronics Technology Group Corporation reported on October 14, 2025 that its Anhui Province center began mass production of a four-channel ultra-low-noise single-photon detector capable of isolating individual photons.

- DARPA awarded Q-CTRL contracts valued at AUD 38 Million (USD 24.4 Million) on August 27, 2025 under the Robust Quantum Sensors program, with Lockheed Martin Corporation joining as subcontractor.

- The Department of Energy Quantum Leadership Act of 2025 proposed USD 2.5 Billion across fiscal years 2026-2030, including USD 875 Million for National Quantum Information Science Research Centers.

- Industry analysis indicates the Quantum Radar Market accounts for approximately 23.6% of the broader quantum sensor market estimated at USD 1.4 Billion in 2025.

- Canada's National Research Council committed CAD 900 Million through the Defence Industrial Strategy in March 2026, with quantum sensing identified as a priority dual-use technology.

- The Indian Ministry of Defence launched the Sovereign Quantum Radar challenge on March 17, 2026 under ADITI 4.0, offering up to INR 25 Crore (USD 3 Million) for an indigenous prototype with applications open through May 4, 2026.

Competitive Landscape Overview

The Quantum Radar Market is highly consolidated around state-backed defense laboratories and the top tier of Western prime contractors. The four leading entities, China Electronics Technology Group Corporation, Lockheed Martin Corporation, RTX Corporation, and BAE Systems plc, collectively control an estimated 62-68% of disclosed quantum radar program revenue in 2025, although exact shares are not publicly reported. Competition is technology-based and contract-driven rather than price-based, since few systems trade on commercial terms outside classified procurement channels.

Competitive evolution is shifting from pure research toward fieldable prototypes. The DARPA Robust Quantum Sensors Phase 1 launch in August 2025 introduced new entrants such as Q-CTRL and Safran Federal Systems alongside incumbents. Indian deep-tech start-up QuBeats won an INR 25 Crore ADITI 2.0 grant in June 2025 for quantum positioning systems including Rydberg radars, signaling a multi-region scrambling effort. No major mergers occurred among quantum radar specialists in the trailing 18 months, although CIQTEK received STAR Market IPO approval in December 2025 at an implied valuation of approximately CNY 11.7 Billion (USD 1.6 Billion).

The matrix below summarizes the 10 most active organizations across the Quantum Radar Market in 2025, including their headquarters, market position, primary solution, geographic strength, and most recent strategic action verified through public filings, government announcements, and trade press.

Competitive Landscape Matrix

| Company | HQ | Position | Key Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| China Electronics Technology Group Corporation (CETC) | Beijing, China | Leader | YLC-8E anti-stealth radar, programmable quantum radar prototype | Asia Pacific, Middle East | Mass production of four-channel single-photon detector (Oct 2025) |

| Lockheed Martin Corporation | Bethesda, USA | Leader | Quantum-enhanced sensing for navigation and ISR platforms | North America, Europe | Subcontractor on DARPA RoQS program with Q-CTRL (Aug 2025) |

| RTX Corporation (Raytheon) | Arlington, USA | Leader | Quantum-enhanced synthetic aperture radar via Intelligence and Space segment | North America, Middle East | Photonic chip-scale quantum sensor research with BBN Technologies (2025) |

| BAE Systems plc | London, UK | Leader | Quantum Parametric Mode Sorting LiDAR for NASA, quantum sensing receivers | Europe, North America | DARPA quantum sensing contract activity (2025) |

| Northrop Grumman Corporation | Falls Church, USA | Challenger | Quantum-resistant stealth research, quantum sensing for missile defense | North America | Advanced Technology Laboratory quantum work continued through 2025 |

| Thales Group | Paris, France | Challenger | Quantum radar feasibility studies, quantum-secured radar networks | Europe | Pan-European quantum sensing R&D under EU Quantum Flagship |

| Q-CTRL | Sydney, Australia | Niche Player | AI-ruggedized quantum sensors for navigation and detection | APAC, North America | USD 24.4 Million DARPA RoQS contract (Aug 2025) |

| Safran Federal Systems | Rochester, USA | Niche Player | Ruggedized quantum PNT sensors for GPS-denied environments | North America | DARPA RoQS Phase 1 contract award (Oct 2025) |

| Hensoldt AG | Taufkirchen, Germany | Niche Player | Next-generation passive radar with quantum-enhanced receivers | Europe | Continued investment in TwInvis platform R&D through 2025 |

| Guoyao Quantum Radar Technology Co., Ltd | Hefei, China | Niche Player | Entangled-photon and single-photon quantum radar systems | Asia Pacific | Expansion of photon-detector manufacturing capacity (2025) |

Segmentation Analysis

The Quantum Radar Market is segmented across four primary axes: technology type, application, end-user, and deployment platform. Each axis is analyzed below with revenue share, sub-segment growth dynamics, and named players.

By Type

The Quantum Radar Market by type is led by Quantum Illumination Radar, which captured approximately 42.5% revenue share in 2025 and contributed roughly USD 140.7 Million. Quantum illumination architectures use entangled signal-idler photon pairs and correlation measurement to extract weak target returns from thermal noise, validated in MIT Lincoln Laboratory studies and CETC field demonstrations. Lockheed Martin Corporation and RTX Corporation maintain active quantum-illumination research programs, while CETC has publicly demonstrated programmable quantum-illumination prototypes since June 2025.

Entangled-Photon Quantum Radar held approximately 31.0% share, contributing USD 102.6 Million in 2025. This category covers radars that transmit microwave or optical photons paired with retained quantum twins, including the canonical Lloyd architecture from the 2008 MIT Science paper. Single-Photon Quantum Radar held approximately 19.5% share at USD 64.5 Million, supported by China's October 2025 mass-production milestone for four-channel detectors. Hybrid Quantum-Classical Radar held the remaining 7.0% share at USD 23.2 Million, with growing interest after the Defense Science Board January 14, 2026 finding that hybrid integration is the more probable near-term deployment pathway. Single-Photon Quantum Radar is projected to grow fastest as detector unit costs decline.

By Application

The Quantum Radar Market by application is dominated by Military Defense (Stealth Detection), which accounted for approximately 58.5% of revenue in 2025, equivalent to USD 193.6 Million. This category bundles anti-stealth surveillance, ballistic-missile early warning, and counter-low-observable air defense. The U.S. Air Force, Office of Naval Research, Missile Defense Agency, and the People's Liberation Army Air Force are the primary funders. Compared to Maritime Navigation at 12.5% share (USD 41.4 Million), Military Defense generates roughly 4.7 times the revenue and dictates technology roadmaps.

Environmental Monitoring and Weather contributed 11.0% share at USD 36.4 Million, driven by partnerships such as BAE Systems' Quantum Parametric Mode Sorting LiDAR with NASA's Earth Science Technology Office. Air Traffic Control held 8.5% at USD 28.1 Million, with EUROCONTROL and the Federal Aviation Administration evaluating quantum-enhanced surveillance for low-radar-cross-section drones. Communications and Industrial applications combined for 5.5% and 4.0% respectively, with Raymarine's solid-state quantum-branded radar lines targeting commercial maritime shipping. ETSI's Quantum Technologies Committee held its first formal meeting in December 2025 to begin drafting compliance requirements.

By End-User

Defense end-users dominated the Quantum Radar Market with approximately 64.0% revenue share in 2025, equivalent to USD 211.8 Million across Air Force, Navy, and Army procurement. The U.S. Department of Defense, the Chinese People's Liberation Army, the UK Ministry of Defence, the Indian Ministry of Defence, and the Canadian Armed Forces collectively account for the bulk of contracted spend. Government Research Institutions captured 18.5% at USD 61.2 Million, including DARPA, Defence Research and Development Canada, the Fraunhofer Society, and the Chinese Academy of Sciences.

Commercial Aviation accounted for 9.5% at USD 31.4 Million, anchored by airport perimeter and runway-debris detection pilots. Maritime and Shipping captured 5.0% at USD 16.6 Million, led by Raymarine's quantum-branded coastal navigation product line. Other Civilian applications completed the segmentation at 3.0%. The Air Force end-user category alone is forecast to outpace overall market CAGR through 2034 because anti-stealth requirements drive Lockheed Martin Corporation, RTX Corporation, and Northrop Grumman Corporation R&D pipelines. Procurement implementation timeline from contract award to field deployment currently averages 28-36 months across DARPA RoQS performers.

By Deployment Platform

Ground-Based Fixed installations led the Quantum Radar Market by deployment platform with approximately 52.0% share in 2025, contributing USD 172.1 Million. Fixed installations dominate because cryogenic cooling and shielding requirements remain incompatible with high-vibration mobile platforms outside DARPA RoQS-grade ruggedization. Airborne deployments, including unmanned aerial vehicles, helicopters, and high-altitude platforms, contributed 21.5% at USD 71.2 Million, supported by China's near-space airship trials and DARPA's helicopter-borne RoQS validation campaign.

Naval and Maritime quantum radar deployments captured 16.0% share at USD 53.0 Million, anchored by the Indian Navy ADITI 4.0 program, the U.S. Navy's GPS-denied submarine quantum navigation tests in 2025, and Royal Navy Quantum Technology Centre work on submarine magnetic-signature detection. Space-Based applications held 10.5% at USD 34.8 Million, the smallest but fastest-growing deployment category, supported by Capella Space (acquired into the IonQ portfolio in 2025) and emerging quantum payload programs at the U.S. Space Force. Compared to Ground-Based Fixed, Space-Based deployments require an order-of-magnitude tighter timing precision but benefit from lower atmospheric photon loss.

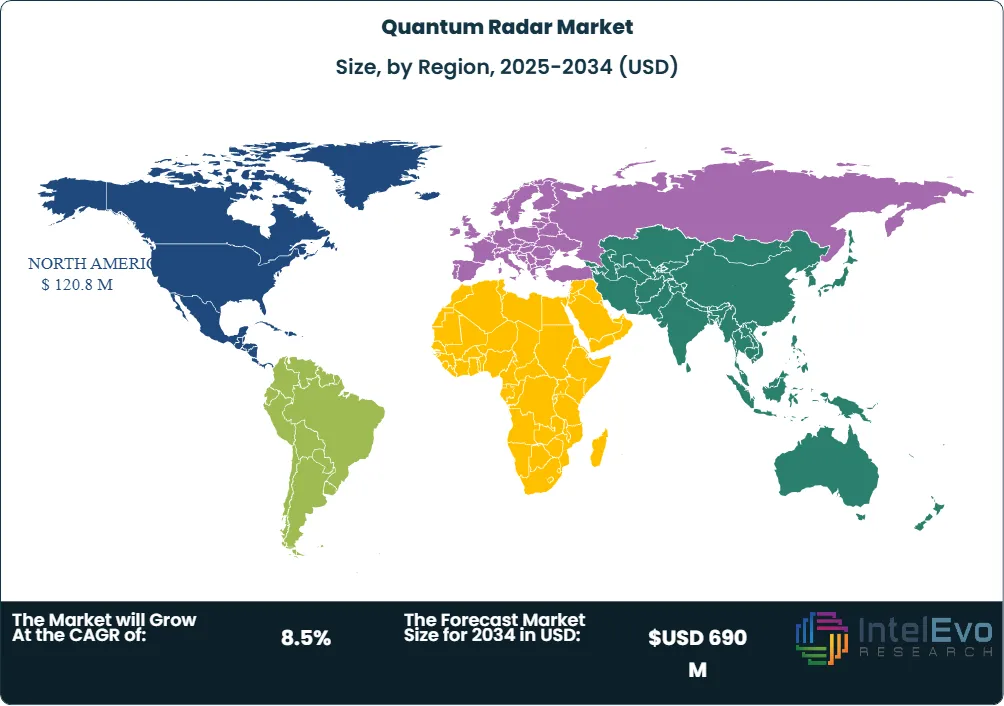

Regional Analysis

The Quantum Radar Market shows pronounced regional concentration, with North America, Asia Pacific, and Europe together accounting for approximately 89.0% of 2025 revenue. Each region's defense procurement ecosystem and quantum policy framework drive distinct adoption patterns, summarized below across the five reporting regions.

North America:

North America held the largest Quantum Radar Market share at 36.5% in 2025, generating approximately USD 120.8 Million. The United States dominates regional spend through DARPA Robust Quantum Sensors, the Office of Naval Research Quantum Information Science portfolio, and Missile Defense Agency early-warning research. Canada contributed via the National Research Council's CAD 900 Million Defence Industrial Strategy commitment in March 2026, with the University of Waterloo coordinating quantum-illumination Arctic surveillance research. Mexico's contribution remains negligible. The U.S. National Quantum Initiative reauthorization is in active congressional drafting following the February 2026 White House executive order draft.

Asia Pacific:

Asia Pacific captured 33.0% Quantum Radar Market share in 2025 at USD 109.2 Million. The People's Republic of China leads regionally and globally in deployed prototypes, with CETC's 14th Research Institute, Guoyao Quantum Radar Technology, the University of Science and Technology of China, and Nanjing University driving development. India entered the field with the Defence Research and Development Organisation Quantum Technology Research Centre, the QuBeats ADITI 2.0 grant in June 2025, and the Indian Navy ADITI 4.0 Sovereign Quantum Radar challenge launched March 17, 2026. Japan and South Korea support quantum sensing through METI and the Korea Institute of Science and Technology Information respectively.

Europe:

Europe contributed 19.5% share at USD 64.5 Million in 2025. The United Kingdom Defence Science and Technology Laboratory leads applied research alongside the Quantum Technology Hub. Germany and France advance quantum sensing under the EU Quantum Flagship program with cumulative funding exceeding EUR 1 Billion, joined by the Netherlands. ETSI's Quantum Technologies Committee held its inaugural meeting in December 2025, advancing pan-European quantum sensor standards. BAE Systems, Hensoldt AG, and Thales Group anchor commercial activity, while Fraunhofer Society laboratories conduct receiver-side research.

Latin America:

Latin America accounted for 4.5% Quantum Radar Market share at USD 14.9 Million in 2025. Brazil leads via the Brazilian Center for Research in Physics and limited Embraer-affiliated quantum sensing research. Argentina and Mexico maintain academic programs without significant commercial deployment. Regional growth is constrained by limited defense quantum budgets and a small domestic supplier base, though dual-use civilian aviation applications are emerging in Sao Paulo and Mexico City test sites.

Middle East and Africa:

Middle East and Africa held 6.5% share at USD 21.5 Million in 2025. The United Arab Emirates leads through Masdar City smart-infrastructure initiatives and Mubadala-backed quantum investments. Israel's defense-focused quantum research at the Weizmann Institute of Science and Israel Aerospace Industries spills into civilian air traffic management. Saudi Arabia's Vision 2030 includes quantum technology pilots through KAUST and SDAIA. South Africa's mining sector is exploring quantum subterranean mapping. Regional growth potential is significant, but regulatory frameworks remain underdeveloped.

Country Analysis

Country-level Quantum Radar Market analysis identifies the United States, China, the United Kingdom, and India as the four most consequential national markets in 2025, accounting for approximately 71% of global revenue. Procurement teams considering quantum radar should align vendor selection with the country-specific defense programs, regulations, and incentives outlined below.

United States:

The U.S. Quantum Radar Market generated approximately USD 92 Million in 2025, growing at a country-specific CAGR of 8.7% through 2034. Federal funding flows through DARPA Robust Quantum Sensors, the Office of Naval Research Long Range Broad Agency Announcement covering quantum information science applications through September 2026, the Defense Innovation Unit emerging-tech portfolio, and Missile Defense Agency early-warning research. The Department of Energy committed USD 575 Million across five National Quantum Information Science Research Centers and announced an additional USD 625 Million for these centers. Lockheed Martin Corporation, RTX Corporation, Northrop Grumman Corporation, and BAE Systems Inc. lead industry participation.

China:

China's Quantum Radar Market reached approximately USD 78 Million in 2025 with a country-specific CAGR of 11.2%, the highest among major markets. The 15th Five-Year Plan adopted in March 2026 designated quantum technology as the first of seven future industries. State-owned CETC, particularly its 14th Research Institute, leads deployed prototypes including the YLC-8E anti-stealth radar and the programmable quantum radar revealed in June 2025. The Quantum Information Engineering Technology Research Center in Anhui Province began four-channel single-photon detector mass production on October 14, 2025. Q1 2026 quantum technology funding inside China reached approximately CNY 2.2 Billion (USD 305 Million).

United Kingdom:

The UK Quantum Radar Market reached approximately USD 22 Million in 2025 with a country-specific CAGR of 8.0%. The UK Defence Science and Technology Laboratory funds applied quantum radar feasibility research, while the National Quantum Computing Centre and the Quantum Technology Hub at the University of York advance receiver and entanglement work. Imperial College London demonstrated GPS-free quantum navigation with the Royal Navy in May 2023, with subsequent maritime trials continuing through 2025. BAE Systems plc, Thales UK, and QinetiQ Group plc lead industry contracts. The UK has allocated GBP 2.5 Billion across its 10-year National Quantum Strategy through 2034.

India:

India's Quantum Radar Market reached approximately USD 12 Million in 2025 with a country-specific CAGR of 14.5%, the fastest among reported countries from a low base. The Defence Research and Development Organisation opened its first Quantum Technology Research Centre in Delhi in 2025. Hyderabad-based QuBeats secured the INR 25 Crore ADITI 2.0 grant in June 2025 for quantum positioning systems. The Indian Navy launched the Sovereign Quantum Radar challenge under ADITI 4.0 on March 17, 2026, with applications open through May 4, 2026. The National Mission on Quantum Technologies and Applications targets domestic quantum sensor production by 2030.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Type

- Entanglement-Based Quantum Radar

- Quantum Illumination Radar

- Photon Detection Quantum Radar

- Superconducting Quantum Radar

- Hybrid Quantum Radar Systems

- Quantum Microwave Radar

- Quantum LiDAR-Radar Integrated Systems

- Portable Quantum Radar Systems

- Fixed Quantum Radar Systems

- Others

By Application

- Military Surveillance and Reconnaissance

- Missile Detection and Tracking

- Stealth Aircraft Detection

- Border Security and Monitoring

- Maritime Surveillance

- Air Traffic Management

- Space Situational Awareness

- Critical Infrastructure Protection

- Weather Monitoring and Atmospheric Research

- Autonomous Navigation Systems

- Search and Rescue Operations

- Scientific Research and Experimental Applications

- Others

By End-User

- Defense and Military Organizations

- Government Security Agencies

- Aerospace Organizations

- Research and Academic Institutions

- Space Agencies

- Homeland Security Agencies

- Maritime Security Organizations

- Air Traffic Control Authorities

- Technology and Quantum Computing Companies

- Industrial Research Organizations

- Others

By Deployment Platform

- Ground-Based Platforms

- Airborne Platforms

- Naval Platforms

- Space-Based Platforms

- Mobile Tactical Platforms

- Unmanned Aerial Vehicles (UAVs)

- Autonomous Defense Systems

- Fixed Surveillance Installations

- Multi-Domain Integrated Platforms

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 331 M |

| Forecast Revenue (2034) | USD 690 M |

| CAGR (2025-2034) | 8.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type, (Entanglement-Based Quantum Radar, Quantum Illumination Radar, Photon Detection Quantum Radar, Superconducting Quantum Radar, Hybrid Quantum Radar Systems, Quantum Microwave Radar, Quantum LiDAR-Radar Integrated Systems, Portable Quantum Radar Systems, Fixed Quantum Radar Systems, Others), By Application, (Military Surveillance and Reconnaissance, Missile Detection and Tracking, Stealth Aircraft Detection, Border Security and Monitoring, Maritime Surveillance, Air Traffic Management, Space Situational Awareness, Critical Infrastructure Protection, Weather Monitoring and Atmospheric Research, Autonomous Navigation Systems, Search and Rescue Operations, Scientific Research and Experimental Applications, Others), By End-User, (Defense and Military Organizations, Government Security Agencies, Aerospace Organizations, Research and Academic Institutions, Space Agencies, Homeland Security Agencies, Maritime Security Organizations, Air Traffic Control Authorities, Technology and Quantum Computing Companies, Industrial Research Organizations, Others), By Deployment Platform, (Ground-Based Platforms, Airborne Platforms, Naval Platforms, Space-Based Platforms, Mobile Tactical Platforms, Unmanned Aerial Vehicles (UAVs), Autonomous Defense Systems, Fixed Surveillance Installations, Multi-Domain Integrated Platforms, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CHINA ELECTRONICS TECHNOLOGY GROUP CORPORATION (CETC), LOCKHEED MARTIN CORPORATION, RTX CORPORATION (RAYTHEON), BAE SYSTEMS PLC, NORTHROP GRUMMAN CORPORATION, THALES GROUP, Q-CTRL, SAFRAN FEDERAL SYSTEMS, HENSOLDT AG, GUOYAO QUANTUM RADAR TECHNOLOGY CO., LTD, RAYMARINE (FLIR/TELEDYNE), QINETIQ GROUP PLC, LEONARDO S.P.A., QUBEATS, QUANTUM DIAMOND TECHNOLOGIES INC., ID QUANTIQUE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Military Surveillance, Missile Tracking, Stealth Detection, Border Security, Maritime, Air Traffic, Space Situational Awareness), By End-User (Defense, Government, Aerospace, Research, Space Agencies), By Platform (Ground, Airborne, Naval, Space) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Application (Military Surveillance, Missile Tracking, Stealth Detection, Border Security, Maritime, Air Traffic, Space Situational Awareness), By End-User (Defense, Government, Aerospace, Research, Space Agencies), By Platform (Ground, Airborne, Naval, Space) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Application (Military Surveillance, Missile Tracking, Stealth Detection, Border Security, Maritime, Air Traffic, Space Situational Awareness), By End-User (Defense, Government, Aerospace, Research, Space Agencies), By Platform (Ground, Airborne, Naval, Space) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Quantum Radar Market?

The Global Quantum Radar Market was valued at USD 305 Million in 2024 and USD 331 Million in 2025, and is projected to reach USD 690 Million by 2034, growing at a CAGR of 8.5% from 2026 to 2034. Market growth is driven by quantum sensing technologies, defense modernization programs, stealth detection capabilities, and advanced surveillance systems.

Who are the major players in the Quantum Radar Market?

CHINA ELECTRONICS TECHNOLOGY GROUP CORPORATION (CETC), LOCKHEED MARTIN CORPORATION, RTX CORPORATION (RAYTHEON), BAE SYSTEMS PLC, NORTHROP GRUMMAN CORPORATION, THALES GROUP, Q-CTRL, SAFRAN FEDERAL SYSTEMS, HENSOLDT AG, GUOYAO QUANTUM RADAR TECHNOLOGY CO., LTD, RAYMARINE (FLIR/TELEDYNE), QINETIQ GROUP PLC, LEONARDO S.P.A., QUBEATS, QUANTUM DIAMOND TECHNOLOGIES INC., ID QUANTIQUE, Others

Which segments covered the Quantum Radar Market?

By Type, (Entanglement-Based Quantum Radar, Quantum Illumination Radar, Photon Detection Quantum Radar, Superconducting Quantum Radar, Hybrid Quantum Radar Systems, Quantum Microwave Radar, Quantum LiDAR-Radar Integrated Systems, Portable Quantum Radar Systems, Fixed Quantum Radar Systems, Others), By Application, (Military Surveillance and Reconnaissance, Missile Detection and Tracking, Stealth Aircraft Detection, Border Security and Monitoring, Maritime Surveillance, Air Traffic Management, Space Situational Awareness, Critical Infrastructure Protection, Weather Monitoring and Atmospheric Research, Autonomous Navigation Systems, Search and Rescue Operations, Scientific Research and Experimental Applications, Others), By End-User, (Defense and Military Organizations, Government Security Agencies, Aerospace Organizations, Research and Academic Institutions, Space Agencies, Homeland Security Agencies, Maritime Security Organizations, Air Traffic Control Authorities, Technology and Quantum Computing Companies, Industrial Research Organizations, Others), By Deployment Platform, (Ground-Based Platforms, Airborne Platforms, Naval Platforms, Space-Based Platforms, Mobile Tactical Platforms, Unmanned Aerial Vehicles (UAVs), Autonomous Defense Systems, Fixed Surveillance Installations, Multi-Domain Integrated Platforms, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date