- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Quantum Supply Chain Optimization Market Size, Share | CAGR 30.9%

Global Quantum Supply Chain Optimization Market Size, Share Analysis By Component (Solutions, Services), By Deployment (Cloud, On-Premises, Hybrid, QCaaS), By Tech (Gate-Based, Annealing, Classical-Hybrid, ML, Simulation), By Application (Forecasting, Inventory, Routing, Warehouse, Procurement, Risk Management), By End-User (Manufacturing, Retail, Automotive, Pharma, Logistics) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

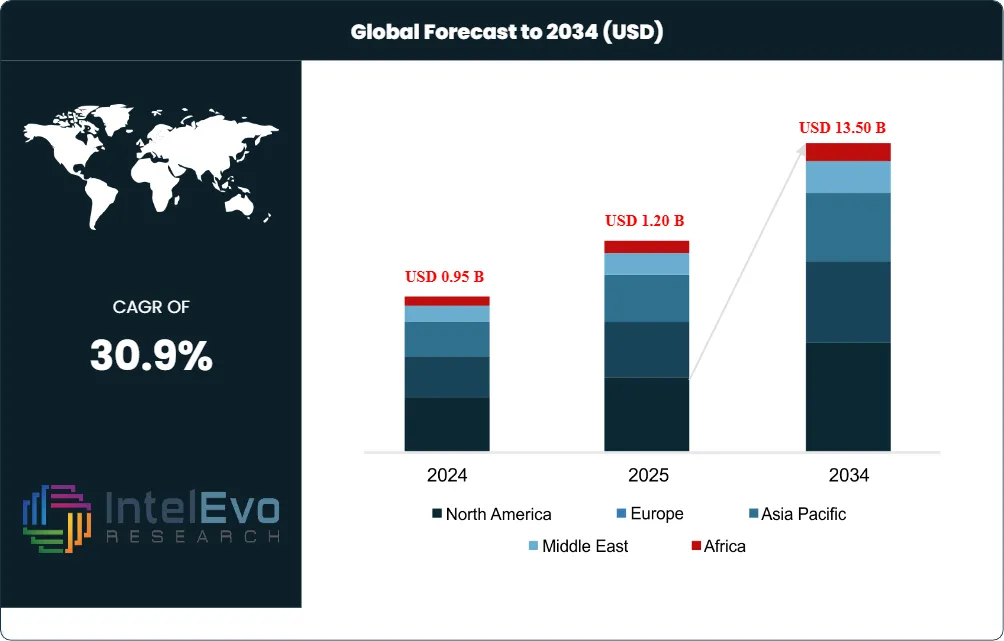

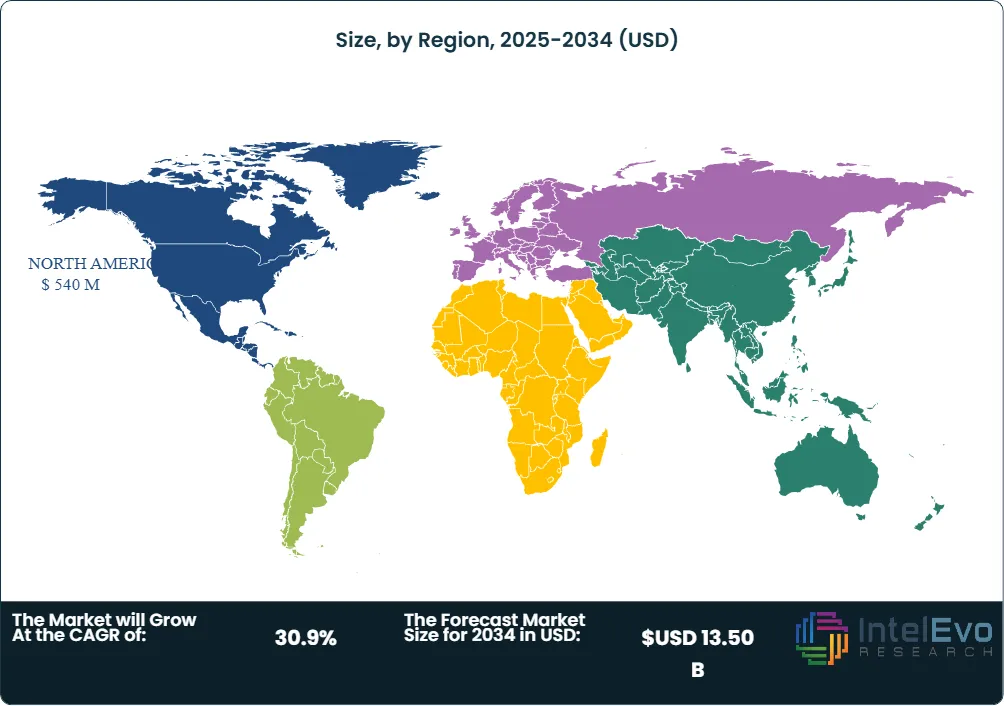

| USD 1.20 Billion | USD 13.50 Billion | 30.9% | North America, 45.0% |

The Quantum Supply Chain Optimization Market was valued at USD 0.95 Billion in 2024 and USD 1.20 Billion in 2025. The market is projected to reach USD 13.50 Billion by 2034, expanding at a CAGR of 30.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 12.30 Billion over the analysis period. Demand is driven by enterprise pilots converting combinatorial routing, scheduling, and resource-allocation problems into quantum-formulated workloads on D-Wave Advantage2, IBM Heron R2, and IonQ trapped-ion systems.

Get More Information about this report -

Request Free Sample ReportThe quantum supply chain optimization market sits at the intersection of quantum computing and operations research. Vendors apply Quantum Approximate Optimization Algorithm (QAOA), quantum annealing, and hybrid quantum-classical solvers to vehicle routing problems, container loading, production scheduling, demand-forecasting, and inventory rebalancing workloads. D-Wave's hybrid solver compressed BASF chemical-manufacturing scheduling from 10 hours to seconds during 2025 trials, while a 2025 D-Wave engagement with North Wales Police cut fleet-deployment planning from months to minutes.

Cloud-delivered quantum services hold the dominant share of the quantum supply chain optimization market in 2025 because enterprise pilots align with pay-per-shot pricing and zero-capex experimentation. Hybrid quantum-classical workflows captured the fastest-growing segment because near-term hardware lacks reliability for standalone production deployment. May 2025's IonQ partnership with Sweden-based Einride targets fleet routing, logistics planning, and emission-tracking integration with autonomous electric vehicles. The European Commission's TAXUD reported 152 million counterfeit goods seized in 2023 valued at USD 3.8 Billion, a 68% increase over 2022, reinforcing demand for quantum-enhanced traceability adjacent to routing-and-scheduling workloads.

North America led the quantum supply chain optimization market with 45.0% revenue share in 2025, equivalent to approximately USD 540 Million in regional revenue, anchored by D-Wave (Burnaby/Palo Alto), IBM (Armonk), IonQ (College Park), and AWS (Seattle) commercial activity. The U.S. National Quantum Initiative Act and the CHIPS and Science Act fund both research and pilot programs at UPS, Walmart, FedEx, and the Department of Defense. Asia Pacific is forecast as the fastest-growing region at a 36% CAGR through 2030, propelled by China's 14th Five-Year Plan quantum priority and India's National Quantum Mission. JPMorgan Chase's October 2025 USD 1.5 Trillion Security and Resiliency Initiative committed up to USD 10 Billion across 27 sub-areas including quantum, accelerating capital availability through 2030.

Market Definition & Scope

The quantum supply chain optimization market is defined as the global commercial activity covering quantum and quantum-inspired software platforms, hardware access, and managed services that solve combinatorial supply chain, logistics, and production-planning workloads. The market includes quantum annealing solvers (D-Wave Leap), gate-model QAOA implementations (IBM Qiskit, IonQ, Quantinuum), and quantum-inspired classical solvers (Multiverse Singularity, Terra Quantum TQ42 Studio) applied to vehicle routing, last-mile delivery, container loading, production scheduling, demand forecasting, and inventory rebalancing.

This analysis includes hybrid quantum-classical workflows delivered through Amazon Braket, Microsoft Azure Quantum, IBM Quantum Network, and D-Wave Leap for supply chain workloads. Excluded are general quantum computing services without supply chain application focus, classical operations research software without quantum modules, post-quantum cryptography software, and pure academic research access. The quantum supply chain optimization market sits within the broader quantum computing as a service parent market valued at approximately USD 3.20 Billion in 2025, of which supply chain workloads represent roughly 37% of commercial enterprise pilots per industry analysis.

, By Deployment (Cloud, On-Premises, Hybrid, QCaaS), By Tech (Gate-Based, Annealing, Classical-Hybrid, ML, Simulation), By Application (Forecasting, Inventory, Routing, Warehouse, Procurement, Risk Management), By End-User (Manufacturing, Retail, Automotive, Pharma, Logistics) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The quantum supply chain optimization market grew from USD 1.20 Billion in 2025 toward a forecast value of USD 13.50 Billion by 2034 at a 30.9% CAGR.

- Segment Dominance: Quantum annealing captured approximately 41% revenue share in 2025, anchored by D-Wave Advantage2 production deployments at BASF, North Wales Police, and Mastercard.

- Segment Dominance: Logistics and transportation end-users held more than 38% of 2025 demand, anchored by UPS, FedEx, Maersk, Einride, and DHL pilot programs.

- Driver: Combinatorial complexity in vehicle routing, container loading, and production scheduling is the primary driver, with quantum solvers compressing BASF scheduling from 10 hours to seconds in 2025.

- Restraint: Hardware error rates and limited qubit counts remain the principal technical constraints, requiring hybrid classical-quantum architecture for any production-scale workload through 2030.

- Opportunity: Quantum-inspired tensor-network solvers represent the largest near-term opportunity, with Multiverse Computing's CompactifAI and Terra Quantum's TQ42 Studio targeting USD 2 Billion-plus addressable workloads.

- Trend: AI-quantum hybrid platforms are now standard, with D-Wave releasing PyTorch integration through 2025 and Terra Quantum's May 2025 TQ42 Studio closed beta.

- Regional: North America led with 45.0% share in 2025 equivalent to roughly USD 540 Million, while Asia Pacific is the fastest-growing region at a forecast 36% CAGR through 2030.

Key Insights Summary

- D-Wave's 2025 hybrid solver engagement with BASF reduced chemical-manufacturing production scheduling from 10 hours to seconds per company case study disclosure.

- IonQ partnered with Sweden-based Einride in May 2025 to develop quantum applications for fleet routing, logistics planning, and supply chain management with autonomous electric vehicles.

- D-Wave reported more than 200 million problems submitted to its quantum systems to date, with over 100 organizations using its hybrid quantum-classical solvers in production.

- Quantum companies raised approximately USD 3.77 Billion in equity financing during the first nine months of 2025, nearly tripling 2024 totals per industry reporting.

- Terra Quantum launched the closed beta of TQ42 Studio in May 2025, featuring QAI Hub no-code platform and Qode Engine Python SDK for hybrid quantum-classical AI development.

- D-Wave's North Wales Police deployment cut fleet-response planning from months to minutes and reduced response times by 50% during 2025 commercial pilots.

- More than USD 30 Billion in global public and private quantum investment has flowed through the National Quantum Initiative (USD 1.2 Billion), China (estimated USD 15 Billion), and the EU Quantum Flagship (EUR 1 Billion).

Competitive Landscape Overview

The quantum supply chain optimization market is moderately consolidated, with the top four vendors (D-Wave Quantum, IBM Corporation, IonQ Inc., and Multiverse Computing) collectively representing an estimated 55 to 62% of 2025 revenue. D-Wave holds the leading commercial position because its annealing architecture maps directly onto Quadratic Unconstrained Binary Optimization (QUBO) formulations used for vehicle routing and production scheduling, with more than 200 million problems submitted to its systems and 99.9% cloud uptime. IBM Quantum Network, AWS Braket, Microsoft Azure Quantum, and IonQ Cloud round out the hyperscaler-platform competitive set.

Competitive evolution centers on three axes: solver speed at QUBO-formulated workloads, hybrid quantum-classical orchestration depth, and supply chain domain expertise. D-Wave appointed Jack Sears Jr. as Vice President of U.S. Government Solutions in 2025 to expand defense and logistics-related procurement. Multiverse Computing competes through tensor-network compression and the Singularity SDK targeting financial and supply chain workloads. ParityQC's parity architecture targets logistics-specific QAOA acceleration. IonQ's pending USD 1.8 Billion SkyWater Technology acquisition and March 2026 Quantum Circuits Inc. acquisition expand its full-stack capability. Strategic moves through 2025 included Terra Quantum's TQ42 Studio launch, D-Wave's CES 2026 sponsorship, and IBM's Poughkeepsie fault-tolerant data center commitment announced in June 2025.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| D-Wave Quantum Inc. | Canada/USA | Leader | Advantage2 annealer, Leap cloud, hybrid solver | North America, Europe | Dec 2025 announced Qubits 2026 conference, CES 2026 sponsor |

| IBM Corporation | USA | Leader | IBM Quantum Network, Heron R2, Qiskit | North America, Europe | Jun 2025 announced fault-tolerant quantum at Poughkeepsie |

| IonQ Inc. | USA | Leader | Trapped-ion processors, Einride solution | North America, Europe, Asia Pacific | May 2025 partnered with Einride for fleet routing |

| Multiverse Computing | Spain | Leader | Singularity SDK, CompactifAI, Tensor networks | Europe, North America | 2025 raised Series B financing for AI compression |

| Microsoft Corporation | USA | Challenger | Azure Quantum platform, Q# language | North America, Europe | Feb 2025 unveiled Majorana 1 topological chip |

| Amazon Web Services | USA | Challenger | Amazon Braket, Ocelot chip, Emerald 54-qubit | North America, Europe | Jul 2025 launched Emerald superconducting processor |

| Quantinuum Ltd. | UK/USA | Challenger | H2 trapped-ion, InQuanto, hybrid solvers | North America, Europe | Continued Honeywell-backed scaling through 2025 |

| Terra Quantum AG | Switzerland | Niche Player | TQ42 Studio, QAI Hub, Qode Engine | Europe | May 2025 launched TQ42 Studio closed beta |

| QC Ware Corp. | USA | Niche Player | Forge platform, supply chain solvers | North America | 2025 expanded enterprise pilots in finance and logistics |

| ParityQC GmbH | Austria | Niche Player | ParityOS, parity architecture for logistics | Europe | 2025 expanded logistics architecture deployments |

Segmentation Analysis

The quantum supply chain optimization market is segmented by component, deployment mode, technology, application, and end-user industry, each producing distinct competitive and adoption patterns across the forecast period.

By Component

Software platforms captured approximately 58% of quantum supply chain optimization market revenue in 2025, anchored by D-Wave Leap subscription tiers, IBM Quantum Network access fees, IonQ pay-per-shot pricing, and Multiverse Singularity licensing. Services accounted for the remaining 42%, including quantum-readiness consulting, custom QUBO formulation, and hybrid-solver integration delivered by IBM Consulting, Capgemini Quantum Lab, and Atos Quantum Advisory. The software-services revenue split is forecast to shift toward software through 2030 because pre-built supply chain templates from D-Wave, Multiverse, and ParityQC reduce custom formulation hours. ROI calculations for QSCO pilots typically run 12 to 24 months.

By Deployment Mode

Cloud deployment captured approximately 78% of quantum supply chain optimization market revenue in 2025 because enterprise pilots align with hyperscaler pay-per-use models and zero-capex experimentation. D-Wave Leap, AWS Braket, Microsoft Azure Quantum, IBM Quantum Network, and IonQ Cloud anchor the cloud segment. On-premises and hybrid deployments retain the remaining 22% revenue share, dominated by defense applications, financial-services workloads with data-residency constraints, and D-Wave on-premises Advantage2 installations. Cloud is forecast to grow at a 33% CAGR through 2030 versus 22% for on-premises, driven by total-cost-of-ownership advantages and continuous solver-version updates.

By Technology

Quantum annealing dominated the quantum supply chain optimization market with approximately 41% revenue share in 2025, anchored by D-Wave Advantage and Advantage2 production deployments solving QUBO-formulated routing and scheduling workloads. Gate-model superconducting systems held 28% share through IBM Heron R2 156-qubit, AWS Emerald 54-qubit, and Rigetti Ankaa-2 84-qubit cloud access. Trapped-ion systems captured 18% share led by IonQ and Quantinuum with the highest gate fidelity in the market. Quantum-inspired classical solvers held 13% share through Multiverse Singularity, Terra Quantum TQ42, and Fujitsu Digital Annealer, providing GPU-accelerated tensor-network alternatives. Annealing remains the leading commercial technology for 2025-2027 production workloads given its direct QUBO mapping.

By Application

Vehicle routing and last-mile delivery captured approximately 28% of quantum supply chain optimization market revenue in 2025, addressing the classical Travelling Salesman Problem (TSP) and Vehicle Routing Problem (VRP) on quantum solvers. Production scheduling held 22% share following D-Wave's BASF case study compressing scheduling from 10 hours to seconds. Demand forecasting and inventory rebalancing represented 19% share through hybrid quantum-classical AI workflows. Container loading and bin packing captured 12% share at maritime carriers including Maersk and CMA CGM. Supplier selection and procurement held 11% share, with the remaining 8% covering quantum-enhanced traceability and counterfeit detection. Vehicle routing is forecast as the fastest-growing application through 2030 driven by e-commerce and quick-commerce penetration.

By End-User Industry

Logistics and transportation captured approximately 38% of quantum supply chain optimization market revenue in 2025, the largest end-user segment, anchored by UPS, FedEx, DHL, Maersk, and Einride pilot programs. Manufacturing held 26% share, anchored by BASF chemical scheduling, Volkswagen production planning, and Toyota supplier-network workloads. Retail and e-commerce represented 14% share through Walmart, Amazon, and JD.com inventory and fulfillment pilots. Pharmaceutical supply chains accounted for 9% share at Pfizer, Roche, and Boehringer Ingelheim. Defense and government held 7% share following D-Wave's 2025 U.S. government solutions business unit formation. Energy and utilities, food and beverage, and aerospace round out the remaining 6% demand. Implementation timelines for production-scale QSCO deployments typically run 9 to 18 months.

Regional Analysis

The global quantum supply chain optimization market shows distinct regional revenue and growth profiles across North America, Europe, Asia Pacific, Latin America, and Middle East and Africa, with North American hyperscaler concentration and European industrial-pilot density driving the geographic mix.

North America

North America led the quantum supply chain optimization market with 45.0% share in 2025, equivalent to approximately USD 540 Million in regional revenue. The United States anchors regional demand at UPS, FedEx, Walmart, Amazon, Boeing, and the Department of Defense. The U.S. National Quantum Initiative Act, the CHIPS and Science Act, and Department of Energy National Quantum Information Science Research Centers fund both research and commercial pilots. Canada anchors regional supply through D-Wave Systems (Burnaby), Xanadu (Toronto), and Photonic Inc. (Coquitlam). D-Wave's December 2025 formation of a U.S. government solutions business unit, with Jack Sears Jr. appointed Vice President, expanded federal procurement positioning.

Europe

Europe held approximately 27% of quantum supply chain optimization market revenue in 2025, valued near USD 324 Million. Germany leads regional demand through BASF chemical-scheduling deployment, Volkswagen production planning, and Mercedes-Benz supplier optimization pilots. France anchors regional vendor supply through Pasqal, Quandela, and Atos Eviden, supported by the EUR 1.8 Billion Plan Quantique. The UK contributes through Quantinuum (Cambridge), the National Quantum Strategy GBP 2.5 Billion commitment, and North Wales Police fleet-deployment commercial pilots. Spain hosts Multiverse Computing (San Sebastian) and Switzerland anchors Terra Quantum (St. Gallen). The European Union Quantum Flagship committed EUR 1 Billion over ten years.

Asia Pacific

Asia Pacific captured approximately 19% of quantum supply chain optimization market revenue in 2025, valued near USD 228 Million, and is forecast as the fastest-growing region at a 36% CAGR through 2030. China leads regional demand through the 14th Five-Year Plan quantum priority, with Origin Quantum (Hefei) and SpinQ Technology providing domestic supply. Japan anchors industrial pilots at Toyota, Hitachi, NEC, Toshiba, and Mitsubishi Chemical Holdings, supported by the Q-LEAP program and Cabinet Office Moonshot Goal 6. India's National Quantum Mission allocated INR 6,003 Crore through the Department of Science and Technology, supporting quantum pilot clusters in Delhi, Mumbai, and Chennai. South Korea contributes through KISTI quantum cloud and Samsung Electronics quantum-program investments.

Latin America

Latin America accounted for approximately 5% of quantum supply chain optimization market revenue in 2025. Brazil leads regional adoption through SENAI Innovation Institute logistics pilots and Embraer aerospace supply-chain modeling. Mexico contributes through CINVESTAV academic research and emerging Tecnologico de Monterrey programs. Argentina, Chile, and Colombia represent emerging demand pockets supported by mining-logistics and energy-distribution pilots. Regional growth is constrained by limited local quantum vendor presence and Spanish-language developer toolchain coverage, although hyperscaler cloud platforms offer accessible entry points for enterprise pilots through 2027.

Middle East & Africa

Middle East and Africa held approximately 4% of quantum supply chain optimization market revenue in 2025. The United Arab Emirates anchors regional demand through the Quantum Research Center at Technology Innovation Institute (Abu Dhabi) and DP World logistics pilots. Saudi Arabia's KAUST quantum initiative and Saudi Green Initiative drive secondary demand. Israel contributes through Quantum Machines and Classiq Technologies commercial offerings. South Africa's national quantum technology initiative supports African demand. Regional growth is constrained by limited cryogenic infrastructure availability, although Vision 2030 funding accelerates capacity additions through 2027.

Country Analysis

United States

The United States quantum supply chain optimization market reached approximately USD 480 Million in 2025, with country CAGR tracking near 32% through 2034. Demand concentrates at UPS, FedEx, Walmart, Amazon, Boeing, and Lockheed Martin logistics and production-planning pilots. The Department of Defense, through the Defense Logistics Agency, evaluates quantum solvers for force-deployment and supply-chain resilience workloads. The U.S. National Quantum Initiative Act funded more than USD 1.2 Billion through fiscal year 2025. The Inflation Reduction Act battery-supply-chain audits indirectly drive QSCO adoption at automotive Tier-1 suppliers. June 2025's IBM announcement of a fault-tolerant quantum computer at Poughkeepsie marks the largest single-site quantum capacity commitment to date.

Germany

Germany's quantum supply chain optimization market reached approximately USD 95 Million in 2025, the largest single-country market within Europe with country CAGR near 31% through 2034. The Federal Ministry of Education and Research (BMBF) committed EUR 3 Billion through 2026 for quantum technology, with the Munich Quantum Valley initiative anchoring regional infrastructure. BASF anchors industrial demand through D-Wave hybrid-solver deployment for chemical-manufacturing scheduling. Volkswagen, BMW, Mercedes-Benz, and Siemens drive automotive and industrial demand-side adoption. Domestic vendors include IQM Quantum (Espoo, Finland with German operations), ParityQC (Innsbruck), and Quantum Brilliance. The Lieferkettensorgfaltspflichtengesetz (LkSG) supply-chain due diligence law indirectly drives traceability and supplier-selection workloads.

China

China's quantum supply chain optimization market reached approximately USD 110 Million in 2025, with country CAGR near 38% through 2034, the highest among major economies. The 14th Five-Year Plan prioritizes quantum-information science as a strategic priority. Domestic vendors include Origin Quantum (Hefei) operating the Wuyuan superconducting cloud and SpinQ Technology delivering desktop and cloud quantum systems. Demand concentrates at Sinopec for refinery scheduling, BYD for battery-supply-chain workloads, JD.com for fulfillment routing, and Alibaba Cloud for hybrid quantum-AI services. China's estimated USD 15 Billion in cumulative quantum investment through 2025 funds both research and commercial supply-chain applications.

Japan

Japan's quantum supply chain optimization market reached approximately USD 65 Million in 2025, with country CAGR near 28% through 2034. The Ministry of Economy, Trade and Industry (METI) Q-LEAP program and Cabinet Office Moonshot Goal 6 target fault-tolerant quantum computing by 2050. Toyota anchors automotive supply-chain pilots, Hitachi targets manufacturing, NEC delivers quantum cloud services, and Mitsubishi Chemical Holdings deploys quantum chemistry workloads. Fujitsu's Digital Annealer (a quantum-inspired classical solver) competes with D-Wave Advantage2 for QUBO-formulated workloads at Japanese manufacturers. The Japanese government's Green Innovation Fund allocated JPY 2 Trillion through 2030 for industrial decarbonization, with quantum-supply-chain projects eligible for grant funding.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Component

- Solutions

- Quantum Optimization Software

- Supply Chain Analytics Platforms

- Quantum Simulation Solutions

- Inventory Optimization Solutions

- Route and Logistics Optimization Platforms

- Demand Forecasting Solutions

- Warehouse Optimization Systems

- Risk Management and Resilience Solutions

- Others

- Services

- Consulting Services

- Integration and Deployment Services

- Managed Services

- Support and Maintenance Services

- Training and Professional Services

By Deployment Mode

- Cloud-Based Deployment

- On-Premises Deployment

- Hybrid Deployment

- Multi-Cloud Deployment

- Quantum Computing as a Service (QCaaS)

- Others

By Technology

- Gate-Based Quantum Computing

- Quantum Annealing

- Hybrid Quantum-Classical Computing

- Quantum Machine Learning

- Quantum Simulation

- Quantum Optimization Algorithms

- Superconducting Quantum Computing

- Trapped Ion Quantum Computing

- Photonic Quantum Computing

- Others

By Application

- Demand Forecasting

- Inventory Optimization

- Production Planning and Scheduling

- Transportation and Route Optimization

- Warehouse and Distribution Management

- Procurement and Supplier Management

- Network Design and Optimization

- Supply Chain Risk Management

- Last-Mile Delivery Optimization

- Cold Chain Optimization

- Carbon Footprint and Sustainability Optimization

- Real-Time Supply Chain Visibility

- Others

By End-User Industry

- Manufacturing

- Retail and E-Commerce

- Automotive

- Healthcare and Pharmaceuticals

- Food and Beverage

- Logistics and Transportation

- Consumer Goods

- Energy and Utilities

- Aerospace and Defense

- Chemicals

- Technology and Electronics

- Government and Public Sector

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.20 B |

| Forecast Revenue (2034) | USD 13.50 B |

| CAGR (2025-2034) | 30.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Solutions, Services), By Deployment Mode, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment, Multi-Cloud Deployment, Quantum Computing as a Service (QCaaS), Others), By Technology, (Gate-Based Quantum Computing, Quantum Annealing, Hybrid Quantum-Classical Computing, Quantum Machine Learning, Quantum Simulation, Quantum Optimization Algorithms, Superconducting Quantum Computing, Trapped Ion Quantum Computing, Photonic Quantum Computing, Others), By Application, (Demand Forecasting, Inventory Optimization, Production Planning and Scheduling, Transportation and Route Optimization, Warehouse and Distribution Management, Procurement and Supplier Management, Network Design and Optimization, Supply Chain Risk Management, Last-Mile Delivery Optimization, Cold Chain Optimization, Carbon Footprint and Sustainability Optimization, Real-Time Supply Chain Visibility, Others), By End-User Industry, (Manufacturing, Retail and E-Commerce, Automotive, Healthcare and Pharmaceuticals, Food and Beverage, Logistics and Transportation, Consumer Goods, Energy and Utilities, Aerospace and Defense, Chemicals, Technology and Electronics, Government and Public Sector, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | D-WAVE QUANTUM INC., IBM CORPORATION, IONQ INC., MULTIVERSE COMPUTING SL, MICROSOFT CORPORATION, AMAZON WEB SERVICES INC., QUANTINUUM LTD., TERRA QUANTUM AG, QC WARE CORP., PARITYQC GMBH, RIGETTI COMPUTING INC., GOOGLE LLC (ALPHABET INC.), FUJITSU LIMITED, QUANDELA SAS, PASQAL SAS, IQM QUANTUM COMPUTERS, ATOS SE (EVIDEN), NEC CORPORATION, ALIRO QUANTUM INC., CLASSIQ TECHNOLOGIES LTD., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud, On-Premises, Hybrid, QCaaS), By Tech (Gate-Based, Annealing, Classical-Hybrid, ML, Simulation), By Application (Forecasting, Inventory, Routing, Warehouse, Procurement, Risk Management), By End-User (Manufacturing, Retail, Automotive, Pharma, Logistics) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Deployment (Cloud, On-Premises, Hybrid, QCaaS), By Tech (Gate-Based, Annealing, Classical-Hybrid, ML, Simulation), By Application (Forecasting, Inventory, Routing, Warehouse, Procurement, Risk Management), By End-User (Manufacturing, Retail, Automotive, Pharma, Logistics) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Deployment (Cloud, On-Premises, Hybrid, QCaaS), By Tech (Gate-Based, Annealing, Classical-Hybrid, ML, Simulation), By Application (Forecasting, Inventory, Routing, Warehouse, Procurement, Risk Management), By End-User (Manufacturing, Retail, Automotive, Pharma, Logistics) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the ?

The Global Quantum Supply Chain Optimization Market was valued at USD 0.95 Billion in 2024 and USD 1.20 Billion in 2025, and is projected to reach USD 13.50 Billion by 2034, growing at a CAGR of 30.9% from 2026 to 2034. Market growth is driven by increasing adoption of quantum computing for logistics, inventory management, route optimization, and supply chain analytics.

Who are the major players in the ?

D-WAVE QUANTUM INC., IBM CORPORATION, IONQ INC., MULTIVERSE COMPUTING SL, MICROSOFT CORPORATION, AMAZON WEB SERVICES INC., QUANTINUUM LTD., TERRA QUANTUM AG, QC WARE CORP., PARITYQC GMBH, RIGETTI COMPUTING INC., GOOGLE LLC (ALPHABET INC.), FUJITSU LIMITED, QUANDELA SAS, PASQAL SAS, IQM QUANTUM COMPUTERS, ATOS SE (EVIDEN), NEC CORPORATION, ALIRO QUANTUM INC., CLASSIQ TECHNOLOGIES LTD., Others

Which segments covered the ?

By Component, (Solutions, Services), By Deployment Mode, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment, Multi-Cloud Deployment, Quantum Computing as a Service (QCaaS), Others), By Technology, (Gate-Based Quantum Computing, Quantum Annealing, Hybrid Quantum-Classical Computing, Quantum Machine Learning, Quantum Simulation, Quantum Optimization Algorithms, Superconducting Quantum Computing, Trapped Ion Quantum Computing, Photonic Quantum Computing, Others), By Application, (Demand Forecasting, Inventory Optimization, Production Planning and Scheduling, Transportation and Route Optimization, Warehouse and Distribution Management, Procurement and Supplier Management, Network Design and Optimization, Supply Chain Risk Management, Last-Mile Delivery Optimization, Cold Chain Optimization, Carbon Footprint and Sustainability Optimization, Real-Time Supply Chain Visibility, Others), By End-User Industry, (Manufacturing, Retail and E-Commerce, Automotive, Healthcare and Pharmaceuticals, Food and Beverage, Logistics and Transportation, Consumer Goods, Energy and Utilities, Aerospace and Defense, Chemicals, Technology and Electronics, Government and Public Sector, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Quantum Supply Chain Optimization Market

Published Date : 18 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date