- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Radiopharmaceutical Market Size, Share & Growth Analysis | CAGR 9.8%

Global Radiopharmaceutical Market Size, Share, Analysis By Product Type (Diagnostic Radiopharmaceuticals, Therapeutic Radiopharmaceuticals), By Isotope Type (Technetium-99m, Fluorine-18, Gallium-68, Lutetium-177, Other Therapeutic Isotopes), By Application (Oncology, Cardiology, Neurology, Endocrinology & Thyroid Indications), By End-User (Hospitals, Diagnostic Imaging Centers, Academic & Research Institutes, Specialty Cancer Centers & Nuclear Pharmacies) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 11.9 Billion, 2025 | USD 27.6 Billion, 2034 | 9.8%, 2026–2034 | North America, 41.0%, 2025 |

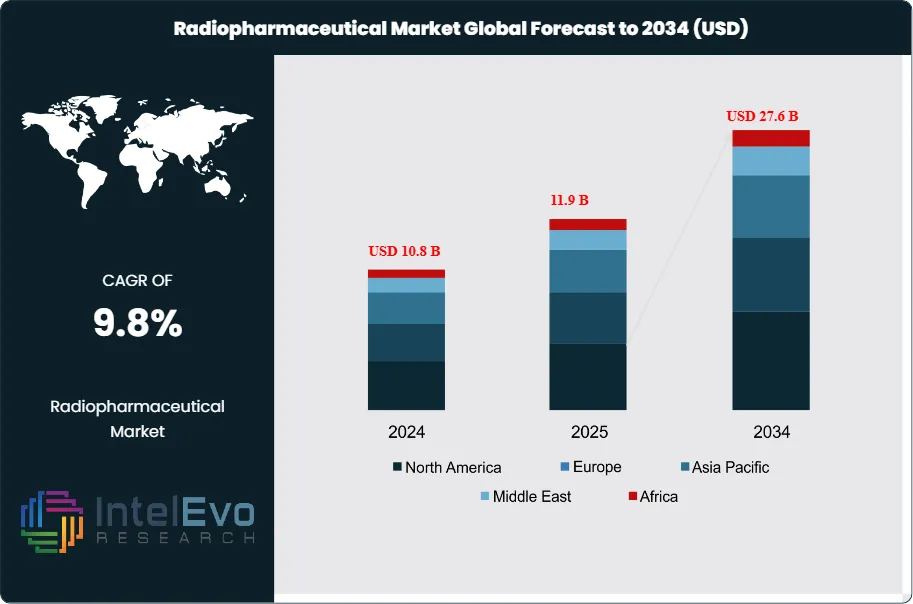

The Radiopharmaceutical Market was valued at approximately USD 10.8 Billion in 2024 and increased to USD 11.9 Billion in 2025. The market is projected to reach nearly USD 27.6 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 9.8% during the forecast period from 2026 to 2034. Market growth is primarily driven by the increasing prevalence of cancer and cardiovascular diseases, rising adoption of nuclear medicine for diagnostic and therapeutic applications, and growing demand for targeted radiotherapy. Additionally, advancements in imaging technologies, expanding pipeline of novel radiopharmaceuticals, and increasing investments in healthcare infrastructure are expected to further accelerate market expansion globally.

Get More Information about this report -

Request Free Sample ReportThe Radiopharmaceutical Market in 2025 was shaped by two clear forces. First, commercial radioligand therapies moved from early adoption into scaled demand. Second, PET imaging agents kept expanding in oncology, neurology, and cardiology. Novartis remained the market anchor. Its 2025 sales reached USD 2.0 Billion for Pluvicto and USD 0.8 Billion for Lutathera, confirming that therapeutic radiopharmaceuticals are now large commercial products rather than niche hospital-only agents. At the same time, Lantheus reported USD 1.54 Billion of full-year 2025 revenue, while Telix reported approximately USD 804 Million of 2025 group revenue, largely reflecting the strength of PSMA PET imaging and broader radiodiagnostic growth.

The Radiopharmaceutical Market still derives more 2025 revenue from diagnostics than therapeutics, but the growth mix is shifting. PET radiodiagnostics remain the volume leader because prostate cancer imaging, amyloid imaging, and established nuclear medicine workflows support broad recurring demand. Therapeutics are growing faster because radioligand therapy is moving earlier in treatment pathways. In March 2025, the FDA approved Pluvicto for use before chemotherapy in eligible PSMA-positive metastatic castration-resistant prostate cancer. In March 2025, the FDA also approved Telix’s Gozellix, adding another PSMA PET imaging product to the U.S. market. These approvals widened both the treatment and imaging sides of the Radiopharmaceutical Market in the same year.

Supply remains the main structural constraint. Radiopharmaceuticals require isotope access, short-cycle logistics, specialized pharmacies, hot-cell manufacturing, and tightly coordinated dose scheduling. Novartis stated in its 2025 annual report that radioligand therapy relies on highly specialized raw materials including radioisotopes and carries supply continuity risk. Curium responded by completing the Monrol acquisition in March 2025 to expand lutetium-177 capacity and PET reach. Cardinal Health also highlighted in August 2025 that TerraPower Isotopes, working with Cardinal Health, had developed a process to produce much larger quantities of actinium-225. These moves show that the Radiopharmaceutical Market is increasingly constrained by nuclear supply chain execution rather than only by drug discovery.

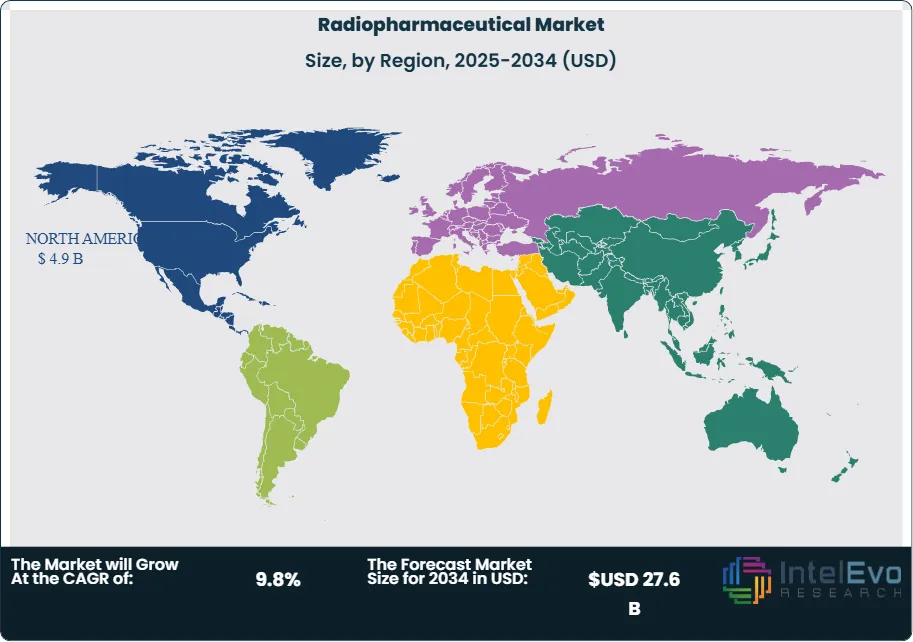

Technology is also changing the market’s economics. Companies are building more vertically integrated manufacturing, automating dose production, and using digital scheduling systems to reduce decay losses and failed deliveries. Telix pointed to cyclotron upgrades, GMP facility expansion, and supply-chain control investments during 2025. Lantheus sharpened its focus in February 2026 toward innovative PET radiodiagnostics and stated that it would pursue value-maximizing alternatives for radiotherapeutic assets. These signals suggest that automation, network design, and manufacturing control will shape share as strongly as product science over the next cycle. Regionally, North America held 41.0% of the Radiopharmaceutical Market in 2025, equal to USD 4.9 Billion. Europe held 29.0%, or USD 3.5 Billion, while Asia Pacific held 20.0%, or USD 2.4 Billion. Latin America and Middle East & Africa together accounted for the remaining 10.0%.

, By Isotope Type (Technetium-99m, Fluorine-18, Gallium-68, Lutetium-177, Other Therapeutic Isotopes), By Application (Oncology, Cardiology, Neurology, Endocrinology & Thyroid Indications), By End-User (Hospitals, Diagnostic Imaging Centers, Academic & Research Institutes, Specialty Cancer Centers & Nuclear Pharmacies) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Radiopharmaceutical Market stood at USD 11.9 Billion in 2025 and is projected to reach USD 27.6 Billion by 2034 at a 9.8% CAGR across 2026–2034. The forecast reflects continued PET imaging demand, broader radioligand therapy use, and rising isotope infrastructure investment.

- Segment Dominance: By product type, diagnostic radiopharmaceuticals led with 57.0% share in 2025, or USD 6.8 Billion. This segment remained ahead because PET and SPECT imaging agents are used across larger patient pools and more care settings than therapeutic radiopharmaceuticals.

- Segment Dominance: By application, oncology held the largest share at 52.0% in 2025, equal to USD 6.2 Billion. Prostate cancer imaging, neuroendocrine tumor therapy, and metastatic prostate cancer radioligand therapy kept oncology well ahead of cardiology and neurology.

- Driver: The main driver is expanding commercial radioligand therapy revenue. Novartis generated USD 2.8 Billion in combined 2025 Pluvicto and Lutathera sales, which materially increased therapeutic radiopharmaceutical weight in the market.

- Restraint: The primary restraint is isotope and logistics bottlenecks. Novartis flagged supply risks tied to specialized raw materials and radioisotopes, while manufacturers across the market responded with capacity expansion and vertical integration moves in 2025.

- Opportunity: The strongest opportunity sits in theranostics and alpha-emitter pipelines. Curium’s Monrol deal, Cardinal Health’s actinium-225 production collaboration, and new investment into targeted radiotherapy platforms point to more than USD 7.5 Billion of incremental addressable market expansion between 2025 and 2034.

- Trend: Vertical integration is the dominant trend. Telix invested in cyclotrons and GMP production upgrades in 2025, while Lantheus bought Evergreen and Life Molecular Imaging and then refocused its portfolio in 2026.

- Regional Analysis: North America led the Radiopharmaceutical Market with 41.0% share and USD 4.9 Billion revenue in 2025. The region benefited from strong FDA approval activity, advanced PET infrastructure, and earlier access to Pluvicto, Gozellix, PYLARIFY, and other premium nuclear medicine products.

Competitive Landscape Overview

The Radiopharmaceutical Market is moderately consolidated. The top four companies controlled an estimated 45.0% of 2025 revenue. Competition is driven by platform depth, isotope access, radiopharmacy networks, and geographic delivery capability rather than price alone. Novartis led because it already sells blockbuster therapeutic radiopharmaceuticals. Curium remained the largest independent nuclear medicine platform, serving more than 14 million patients in over 70 countries. Lantheus delivered USD 1.54 Billion in 2025 revenue, while Telix reached approximately USD 804 Million, confirming that scaled diagnostic franchises now matter nearly as much as therapeutic headlines.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

|---|---|---|---|---|---|

| NOVARTIS | Switzerland | Leader | Pluvicto / Lutathera radioligand therapy franchise | North America, Europe, Japan | FDA approved Pluvicto for earlier pre-chemotherapy use in March 2025. |

| CURIUM | France | Leader | Pylclari / nuclear medicine diagnostic and RLT platform | Europe, North America | Completed Monrol acquisition in March 2025 to expand Lu-177 capacity and PET footprint. |

| LANTHEUS | US | Leader | PYLARIFY radiodiagnostic platform | North America | Completed Evergreen acquisition in April 2025 and reported USD 1.54 Billion in 2025 revenue. |

| TELIX PHARMACEUTICALS | Australia | Leader | Illuccix / Gozellix / PSMA PET platform | North America, Europe, Australia | Won FDA approval for Gozellix in March 2025 and reported approximately USD 804 Million of 2025 revenue. |

| BAYER | Germany | Challenger | Xofigo | Europe, North America | Continued to generate new Xofigo data at ASCO 2025 to defend its alpha-radiopharmaceutical position. |

| BRISTOL MYERS SQUIBB | US | Challenger | RayzeBio actinium-based targeted radiopharmaceutical platform | North America | Continued RayzeBio integration in 2025 and opened a new Indianapolis hub. |

| ASTRAZENECA | UK | Challenger | Fusion radioconjugate platform | North America, Europe | Completed Fusion acquisition in June 2024 to build actinium-based radioconjugate capability. |

| ELI LILLY | US | Challenger | POINT Biopharma radioligand pipeline | North America | Continued integrating POINT into Lilly’s oncology strategy through 2025. |

| GE HEALTHCARE | US | Niche Player | Vizamyl / Cerianna / Flyrcado molecular imaging agents | North America, Europe | Won FDA expanded indications for Vizamyl in June 2025. |

| ITM | Germany | Niche Player | n.c.a. Lu-177 edotreotide and medical radioisotopes | Europe | Secured up to USD 262.5 Million in debt financing in May 2025 to prepare for commercial launch readiness. |

By Product Type

By product type, diagnostic radiopharmaceuticals led the Radiopharmaceutical Market with 57.0% share in 2025, or USD 6.8 Billion. This segment includes PET and SPECT imaging agents used in prostate cancer, neurodegenerative disease, cardiology, and general nuclear medicine workflows. Diagnostics remained ahead because they serve larger patient volumes, require shorter treatment decision cycles, and fit more naturally into routine hospital and imaging-center operations. Lantheus, Telix, Curium, and GE HealthCare all benefited from this structure through products such as PYLARIFY, Illuccix, Gozellix, Pylclari, and Vizamyl. PET was the strongest part of the segment, especially in oncology, where PSMA imaging continued to expand. Therapeutic radiopharmaceuticals held 43.0%, equal to USD 5.1 Billion, but they grew faster because blockbuster radioligand products are now established. Novartis alone generated USD 2.8 Billion from Pluvicto and Lutathera in 2025. Over time, the market mix will continue moving toward therapeutics, but diagnostics will remain the broader revenue base in 2025 because of installed scanner infrastructure, wider reimbursement pathways, and higher procedure volume.

By Isotope Type

By isotope type, technetium-99m and legacy SPECT isotopes accounted for 31.0% of the Radiopharmaceutical Market in 2025, or USD 3.7 Billion. This segment stayed large because hospitals still rely on broad SPECT procedure volumes even as PET expands faster. Fluorine-18 PET isotopes represented 25.0%, or USD 3.0 Billion, supported by prostate cancer and neurology imaging agents. Gallium-68 PET isotopes held 12.0%, or USD 1.4 Billion, driven mainly by PSMA imaging products such as Illuccix and Gozellix. On the therapeutic side, lutetium-177 was the most important growth isotope at 18.0%, or USD 2.1 Billion, thanks to Pluvicto, Lutathera, and broad pipeline expansion across Curium, ITM, and Telix. Other therapeutic isotopes, including iodine-131, yttrium-90, radium-223, samarium-153, astatine-211, and actinium-225, represented 14.0%, or USD 1.7 Billion. This segment is strategically important because alpha emitters and next-generation targeted radiotherapies are attracting new capital, even though current commercial revenue is still smaller than Lu-177.

By Application

By application, oncology dominated the Radiopharmaceutical Market with 52.0% share in 2025, or USD 6.2 Billion. Oncology led because both the fastest-growing diagnostics and the largest therapeutic products are concentrated in prostate cancer and neuroendocrine tumors. Novartis, Telix, Lantheus, and Curium all have strong oncology exposure. Cardiology held 19.0%, or USD 2.3 Billion, supported by legacy nuclear imaging volumes and newer PET imaging interest. Neurology represented 14.0%, or USD 1.7 Billion, with amyloid imaging gaining strength after GE HealthCare’s June 2025 Vizamyl label expansion. Endocrinology and thyroid indications accounted for 9.0%, or USD 1.1 Billion, driven mainly by long-established iodine-based nuclear medicine use. Other applications made up 6.0%, or USD 0.7 Billion, including infection imaging, bone imaging, and research-linked use.

By End User

By end user, hospitals accounted for 46.0% of the Radiopharmaceutical Market in 2025, equal to USD 5.5 Billion. Hospitals led because therapeutic radiopharmaceutical administration, inpatient nuclear medicine procedures, and specialist oncology workflows remain heavily hospital-based. Diagnostic imaging centers held 28.0%, or USD 3.3 Billion, supported by PET imaging growth in prostate cancer and brain imaging. Academic and research centers represented 14.0%, or USD 1.7 Billion, reflecting their role in trials, isotope innovation, and early adoption of next-generation theranostics. Specialty cancer centers, nuclear pharmacies, and outpatient specialty clinics held 12.0%, or USD 1.4 Billion. This segment is becoming more important as more radiopharmaceutical procedures shift into specialized outpatient networks.

Regional Analysis

North America Radiopharmaceutical Market

North America held 41.0% of the Radiopharmaceutical Market in 2025, equal to USD 4.9 Billion. The United States led the region, followed by Canada and Mexico. North America remained the largest market because it combined earlier approvals, broader reimbursement, deeper PET infrastructure, and stronger specialist oncology adoption than any other region. The U.S. approved Pluvicto for earlier pre-chemotherapy use in March 2025 and approved Gozellix in March 2025. Lantheus reported USD 1.54 Billion of 2025 revenue, while Novartis continued scaling Pluvicto and Lutathera. Canada remained strategically relevant through nuclear medicine infrastructure and isotope distribution, though smaller in revenue than the U.S. Mexico was still an early-stage commercial market by comparison, with growth shaped more by urban specialty access than by national scale.

Europe Radiopharmaceutical Market

Europe accounted for 29.0% of the Radiopharmaceutical Market in 2025, or USD 3.5 Billion. Germany, France, the UK, and Italy were the most relevant countries. Europe held a large share because nuclear medicine use is broad, infrastructure is mature, and several leading radiopharmaceutical companies operate from the region. Curium is headquartered in Europe and serves more than 14 million patients in over 70 countries. Novartis has a major radioligand manufacturing footprint in Italy, and Telix continued European rollout of Illuccix across multiple countries during 2025. Germany and France are core demand centers due to strong hospital networks and oncology adoption. The UK combines good clinical capability with tighter procurement dynamics. Italy is strategically important because it is both a demand market and a manufacturing hub for radioligand therapy.

Asia Pacific Radiopharmaceutical Market

Asia Pacific held 20.0% of the Radiopharmaceutical Market in 2025, equal to USD 2.4 Billion. China, Japan, India, and South Korea were the most strategically relevant countries. The region remained smaller than North America and Europe in current commercial value, but it is becoming one of the fastest-growing radiopharmaceutical markets. Japan is important because Novartis reported Lutathera growth in Japan and had 2025 approvals for earlier Pluvicto use there. China also matters because Novartis stated that Pluvicto gained approval in China for pre-chemotherapy use during 2025, and Telix’s Illuccix China filing was accepted in January 2026 after positive Phase 3 results. India and South Korea remain earlier in full-scale theranostic adoption but are becoming more important for imaging growth, manufacturing, and regional distribution.

Latin America Radiopharmaceutical Market

Latin America represented 6.0% of the Radiopharmaceutical Market in 2025, or USD 0.7 Billion. Brazil dominated the region, followed by Mexico and Argentina. Brazil led because it has the region’s largest oncology base, strongest nuclear medicine infrastructure, and greatest ability to absorb premium PET imaging and therapeutic radiopharmaceuticals. Mexico followed at smaller scale, supported mainly by specialist urban care networks. Argentina remained more constrained by reimbursement and broader healthcare budget pressure. Latin America continues to under-index global demand because advanced isotope logistics and same-day distribution are harder to scale than in North America or Europe.

Middle East & Africa Radiopharmaceutical Market

Middle East & Africa held 4.0% of the Radiopharmaceutical Market in 2025, equal to USD 0.5 Billion. The UAE, Saudi Arabia, and South Africa were the region’s most relevant countries. The Gulf states led because they have stronger tertiary hospital systems, faster adoption of premium oncology diagnostics, and more policy support for specialized care. South Africa remained the largest sub-Saharan market for nuclear medicine access. The rest of the region stayed limited by payment infrastructure, isotope handling capacity, and specialist-site concentration.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Diagnostic Radiopharmaceuticals

- Therapeutic Radiopharmaceuticals

By Isotope Type

- Technetium-99m and Legacy SPECT Isotopes

- Fluorine-18 PET Isotopes

- Gallium-68 PET Isotopes

- Lutetium-177

- Other Therapeutic Isotopes

By Application

- Oncology

- Cardiology

- Neurology

- Endocrinology and Thyroid Indications

- Other Applications

By End User

- Hospitals

- Diagnostic Imaging Centers

- Academic and Research Centers

- Specialty Cancer Centers, Nuclear Pharmacies, and Outpatient Specialty Clinics

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | 11.9 B |

| Forecast Revenue (2034) | USD 27.6 B |

| CAGR (2025-2034) | 9.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Diagnostic Radiopharmaceuticals, Therapeutic Radiopharmaceuticals), By Isotope Type (Technetium-99m and Legacy SPECT Isotopes, Fluorine-18 PET Isotopes, Gallium-68 PET Isotopes, Lutetium-177, Other Therapeutic Isotopes), By Application (Oncology, Cardiology, Neurology, Endocrinology and Thyroid Indications, Other Applications), By End User, Hospitals (Diagnostic Imaging Centers, Academic and Research Centers, Specialty Cancer Centers, Nuclear Pharmacies, and Outpatient Specialty Clinics) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NOVARTIS, CURIUM, LANTHEUS, TELIX PHARMACEUTICALS, BAYER, BRISTOL MYERS SQUIBB, ASTRAZENECA, ELI LILLY, GE HEALTHCARE, ITM, CARDINAL HEALTH, SIEMENS HEALTHINEERS, NORDION, SHINE TECHNOLOGIES, ECKERT & ZIEGLER, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Isotope Type (Technetium-99m, Fluorine-18, Gallium-68, Lutetium-177, Other Therapeutic Isotopes), By Application (Oncology, Cardiology, Neurology, Endocrinology & Thyroid Indications), By End-User (Hospitals, Diagnostic Imaging Centers, Academic & Research Institutes, Specialty Cancer Centers & Nuclear Pharmacies) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

, By Isotope Type (Technetium-99m, Fluorine-18, Gallium-68, Lutetium-177, Other Therapeutic Isotopes), By Application (Oncology, Cardiology, Neurology, Endocrinology & Thyroid Indications), By End-User (Hospitals, Diagnostic Imaging Centers, Academic & Research Institutes, Specialty Cancer Centers & Nuclear Pharmacies) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

, By Isotope Type (Technetium-99m, Fluorine-18, Gallium-68, Lutetium-177, Other Therapeutic Isotopes), By Application (Oncology, Cardiology, Neurology, Endocrinology & Thyroid Indications), By End-User (Hospitals, Diagnostic Imaging Centers, Academic & Research Institutes, Specialty Cancer Centers & Nuclear Pharmacies) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Radiopharmaceutical Market?

The Global Radiopharmaceutical Market was valued at USD 11.9 Billion in 2025, projected to reach USD 27.6 Billion by 2034 at a CAGR of 9.8% (2026–2034). Growth is driven by rising cancer prevalence, increasing adoption of nuclear medicine, advancements in imaging technologies, and expanding demand for targeted radiotherapy and innovative radiopharmaceuticals.

Who are the major players in the Radiopharmaceutical Market?

NOVARTIS, CURIUM, LANTHEUS, TELIX PHARMACEUTICALS, BAYER, BRISTOL MYERS SQUIBB, ASTRAZENECA, ELI LILLY, GE HEALTHCARE, ITM, CARDINAL HEALTH, SIEMENS HEALTHINEERS, NORDION, SHINE TECHNOLOGIES, ECKERT & ZIEGLER, Others

Which segments covered the Radiopharmaceutical Market?

By Product Type (Diagnostic Radiopharmaceuticals, Therapeutic Radiopharmaceuticals), By Isotope Type (Technetium-99m and Legacy SPECT Isotopes, Fluorine-18 PET Isotopes, Gallium-68 PET Isotopes, Lutetium-177, Other Therapeutic Isotopes), By Application (Oncology, Cardiology, Neurology, Endocrinology and Thyroid Indications, Other Applications), By End User, Hospitals (Diagnostic Imaging Centers, Academic and Research Centers, Specialty Cancer Centers, Nuclear Pharmacies, and Outpatient Specialty Clinics)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date