- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Raw, Fresh & Frozen Dog Food Market Size & Forecast 2034 | CAGR 5.1%

Global Raw, Fresh, & Frozen Dog Food Market Size, Share, Analysis By Food Type (Raw Food, Fresh Food, Frozen Food), By Breed Size (Small, Medium, Large), By Application (Dental Care, Digestive Health, Bone & Joint Support, Weight Management, Immune Support), By Flavor (Chicken, Beef, Lamb, Turkey, Fish), By Sales Channel (Online Retail, Pet Specialty Stores, Modern Trade) – Industry Trends & Forecast 2025–2034

Report Overview

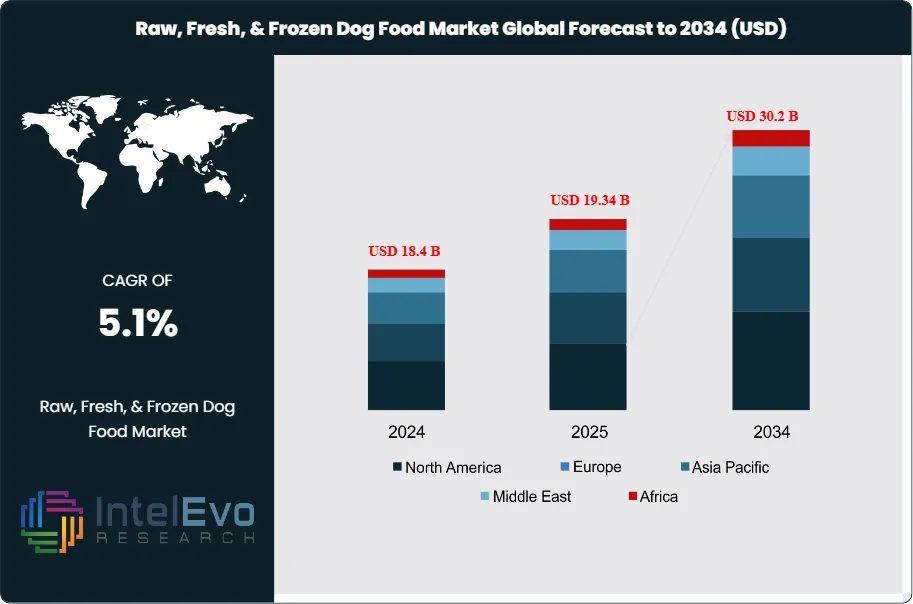

The Raw, Fresh, & Frozen Dog Food Market was valued at approximately USD 18.4 billion in 2024 and is projected to reach nearly USD 30.2 billion by 2034, reflecting steady expansion driven by rising pet humanization trends and demand for premium, natural pet nutrition products. Based on the projected growth trajectory, the market size for 2025 is estimated at around USD 19.34 billion. Beginning in 2026, the market is expected to grow at a compound annual growth rate (CAGR) of about 5.1% from 2026 to 2034, ultimately reaching an estimated valuation of approximately USD 30.2 billion by 2034.

Get More Information about this report -

Request Free Sample ReportRising attachment to companion animals and the shift from mass-market kibble to human-grade formulas drive this expansion. Raw, fresh, and frozen formats sit at the premium end of canine nutrition and account for about 18–20% of global dog food revenues, with share expected to exceed 25% by 2034.

Demand comes from health-focused owners who link minimally processed meat- and vegetable-based recipes with better digestion, coat quality, and vitality. Around 71% of owners now regard pets as family members, which supports willingness to trade up despite price premiums of 30–70% versus conventional dry food. A global dog population of about 900 million provides a wide volume base that supports category penetration, particularly in emerging markets.

On the supply side, specialized brands and integrated meat processors expand chilled and frozen lines, invest in cold-chain logistics, and scale direct-to-consumer subscription models. The market remains fragmented, with the top five suppliers together holding less than 35% share. This structure encourages innovation around novel proteins, breed-specific formulas, and functional benefits such as digestive or joint support. AI-driven formulation and digital demand forecasting improve recipe design and inventory planning, while automation in packaging raises consistency and lowers unit costs.

Regulation tightens across North America and Europe as authorities enforce stricter standards on pathogen control, traceability, and labeling. These measures raise compliance costs but enhance trust and act as a barrier to informal producers. Key risks include cold-chain disruption, raw material price volatility, and debate over the safety of raw diets, which can trigger localized restrictions or recalls.

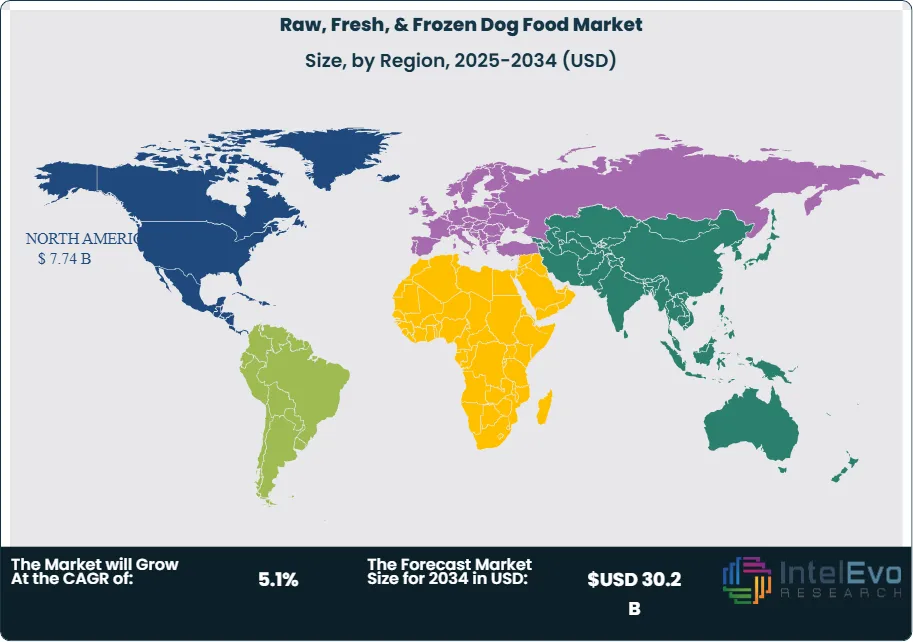

Regionally, North America represents roughly 35% of category revenues, supported by high spending per pet and mature retail and online channels. Europe contributes close to 30%, driven by rigorous oversight and preference for natural formulations. Asia Pacific is the fastest-growing region, with an estimated CAGR of 6.5% through 2034 as pet ownership climbs in China, India, and Southeast Asia and modern trade expands chilled shelf space. These dynamics position raw, fresh, and frozen dog food as a structurally attractive growth niche within global pet nutrition.

, By Breed Size (Small, Medium, Large), By Application (Dental Care, Digestive Health, Bone & Joint Support, Weight Management, Immune Support), By Flavor (Chicken, Beef, Lamb, Turkey, Fish), By Sales Channel (Online Retail, Pet Specialty Stores, Modern Trade) – Industry Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Raw, Fresh, & Frozen Dog Food Market was valued at 17.5 billion USD, 2023 and is projected to reach USD 30.2 billion by 2034. This trajectory implies a 5.1% CAGR, 2026-2034.

- Segment Dominance: Fresh Food led the food type segment with an estimated: 38.0% segment share, 2023 as owners prioritized visible ingredient quality. This share could rise to an estimated: 42.0% segment share, 2034 as premium formulations scale across retail and digital channels.

- Segment Dominance: Medium Breeds accounted for an estimated: 40.0% volume share, 2023, making them the largest breed-size segment in the category. Digestive Care held an estimated: 35.0% revenue share, 2023, underscoring health-focused purchasing behavior.

- Driver: Health-focused feeding behavior shapes demand, with digestive care needs influencing an estimated: 45.0% of purchase decisions, 2024. Preference for quality proteins such as chicken, the leading flavor, supports unit price premiums of an estimated: 15.0% above standard dry food, 2024.

- Restraint: High product and logistics costs constrain penetration, as an estimated: 30.0% of owners, 2024 remain price-sensitive and retain conventional dry or wet formats. Cold-chain and frozen storage limitations restrict availability in an estimated: 25.0% of emerging-market retail outlets, 2024.

- Opportunity: Online retailers, which led the channel mix in 2023, captured an estimated: 35.0% revenue share, 2023 by offering assortment depth and convenient fulfillment. Expanding e-commerce in emerging economies could add an estimated: 4.0 billion USD, 2034 in incremental sales over 2024-2034.

- Trend: Digital platforms increasingly use recommendation engines and pet-profile data, with an estimated: 50.0% of online buyers, 2024 engaging with tailored feeding plans. Subscription-based deliveries in raw and fresh formats are set to grow at an estimated: 7.0% CAGR, 2024-2034 as convenience and reliability become core expectations.

- Regional Analysis: North America likely holds an estimated: 40.0% revenue share, 2024 given high spending per pet and strong online penetration. Asia Pacific, led by China and India, is positioned to deliver an estimated: 6.0% CAGR, 2024-2034 as pet ownership and digital retail expand.

By Type

High-performance concrete, self-consolidating concrete, and other specialized mixes continue to gain traction as construction firms raise expectations for durability and workability. Demand in 2025 reflects a shift toward materials that improve placement efficiency and reduce labor requirements. High-performance concrete holds the largest share, supported by its ability to deliver high strength with lower permeability. Market participants report adoption rates above 40 percent across major infrastructure programs.

Self-consolidating concrete expands steadily as contractors seek mix designs that reduce vibration needs and improve surface finish. Its use grows in high-density projects and complex geometries where precision is critical. Other concrete types, including fiber-reinforced and lightweight variants, attract interest in regions with active housing development and climate-resilience mandates. These categories together signal broader movement toward materials that support efficient onsite execution and tighter project timelines.

Through 2030, demand remains influenced by rising investment in transport networks, data centers, and industrial parks. Material suppliers prepare for stricter regulatory expectations on embodied carbon, which may accelerate the shift toward advanced concrete formulations.

By Application

Pavers represent the largest application category as cities expand public spaces and non-motorized mobility infrastructure. Municipal programs in North America and Europe continue to upgrade pavements using high-durability concrete to reduce long-term maintenance. Retaining walls also see strong activity, supported by hillside development, flood-control upgrades, and logistics-facility expansion. Their annual demand rises in the Asia Pacific region where large-scale industrial zoning increases site-grading requirements.

Other applications—including precast components, utility structures, and building façades—demonstrate solid growth as offsite construction gains adoption. Manufacturers report higher orders for modular concrete units that shorten project cycles and improve quality control.

The application mix reflects priorities around resilience and lifecycle cost. Governments continue to fund structural reinforcements, while private developers invest in materials that maintain performance under heavier loads and frequent environmental stress.

By End-Use

Residential building activity benefits from recovering housing starts in 2025. Developers adopt advanced concrete formulations for foundations, structural frames, and exterior elements to improve energy performance and support multi-story designs. This segment accounts for more than one-third of market demand.

Commercial building remains the second-largest end-use category. Data centers, logistics hubs, and mixed-use developments all require materials with high load-bearing capacity and controlled shrinkage. Contractors in these projects increasingly specify high-performance and self-consolidating concrete to meet exacting structural requirements.

Industrial facilities display sustained demand as manufacturers expand capacity for electronics, pharmaceuticals, and automotive components. These projects rely on concrete solutions that withstand vibration, chemical exposure, and thermal stress. The industrial share grows notably in emerging markets as supply-chain diversification accelerates.

By Region

North America leads the global market due to strong investment in transportation upgrades, warehouse development, and urban revitalization. The United States accounts for the majority of regional demand, supported by multi-year federal funding packages for bridges, highways, and water systems. Canada follows with steady activity in residential construction and public infrastructure repair.

Europe maintains a significant share as countries prioritize climate-resilient structures and advance low-carbon construction programs. Adoption of high-performance mixes rises in Germany, France, and the Nordics, where regulations emphasize durability and reduced material waste.

Asia Pacific records the fastest growth. China, India, and Southeast Asia continue to expand industrial corridors, metro networks, and housing. Local suppliers scale production of specialized concrete types to meet increasing project complexity. Latin America and the Middle East & Africa show moderate but improving demand, driven by urban expansion, energy projects, and industrial diversification.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Food Type

- Raw Food

- Fresh Food

- Frozen Food

By Breed Size

- Small Breeds

- Medium Breeds

- Large Breeds

By Application

- Dental Care

- Digestive Care

- Bone and Joint Health

- Weight Management

- Immune Support

- Energy and Muscle Support

- Other Applications

By Flavor Type

- Chicken

- Beef

- Lamb

- Turkey

- Fish

- Other Flavors

By Sales Channel

- Wholesalers and Distributors

- Modern Trade

- Convenience Stores

- Pharmacy and Drug Stores

- Online Retailers

- Pet Specialty Stores

- Other Sales Channels

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 19.34 B |

| Forecast Revenue (2034) | USD 30.2 B |

| CAGR (2025-2034) | 5.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Food Type (Raw Food, Fresh Food, Frozen Food), By Breed Size (Small Breeds, Medium Breeds, Large Breeds), By Application (Dental Care, Digestive Care, Bone and Joint Health, Weight Management, Immune Support, Energy and Muscle Support, Other Applications), By Flavor Type (Chicken, Beef, Lamb, Turkey, Fish, Other Flavors), By Sales Channel (Wholesalers and Distributors, Modern Trade, Convenience Stores, Pharmacy and Drug Stores, Online Retailers, Pet Specialty Stores, Other Sales Channels) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | The Farmers Dog, Vital Essentials, Smallbatch Pets, Nature’s Variety Instinct, K9 Natural, Primal Pet Foods, Stella & Chewy’s, BARF World, Raw Paws Pet Food, Steve’s Real Food, Ollie Pets, Darwin’s Natural Pet Products, Open Farm, Northwest Naturals, Answers Pet Food |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Breed Size (Small, Medium, Large), By Application (Dental Care, Digestive Health, Bone & Joint Support, Weight Management, Immune Support), By Flavor (Chicken, Beef, Lamb, Turkey, Fish), By Sales Channel (Online Retail, Pet Specialty Stores, Modern Trade) – Industry Trends & Forecast 2025–2034")

, By Breed Size (Small, Medium, Large), By Application (Dental Care, Digestive Health, Bone & Joint Support, Weight Management, Immune Support), By Flavor (Chicken, Beef, Lamb, Turkey, Fish), By Sales Channel (Online Retail, Pet Specialty Stores, Modern Trade) – Industry Trends & Forecast 2025–2034")

, By Breed Size (Small, Medium, Large), By Application (Dental Care, Digestive Health, Bone & Joint Support, Weight Management, Immune Support), By Flavor (Chicken, Beef, Lamb, Turkey, Fish), By Sales Channel (Online Retail, Pet Specialty Stores, Modern Trade) – Industry Trends & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Raw, Fresh, & Frozen Dog Food Market

Published Date : 27 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date