- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Real Estate Tokenization Market Size, Share & Forecast | CAGR 24.0%

Global Real Estate Tokenization Market Size, Share, Analysis By Type (Commercial Real Estate, Residential Real Estate, Industrial Real Estate, Single Asset, Multiple Asset), By Component (Platform, Services), By Deployment Mode (Cloud, On-Premises), By End-User (Institutional Investors, Individual Investors, Real Estate Developers, Property Management Companies) Industry Region & Key Players, Market Dynamics, Blockchain Adoption Trends, Competitive Strategies & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 3.80 Billion | USD 26.40 Billion | 24.0% | North America, 38.4% |

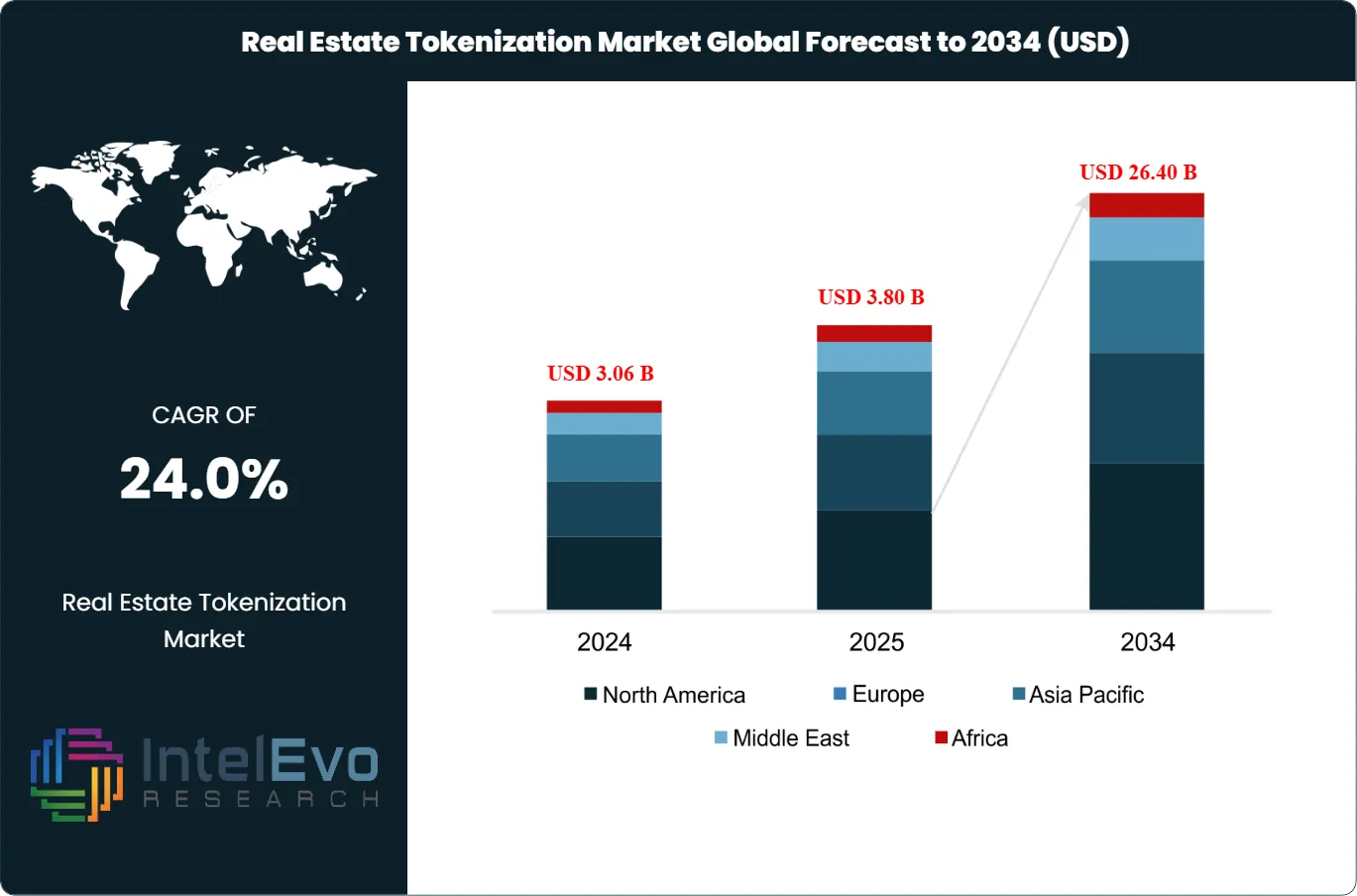

The Real Estate Tokenization Market was valued at approximately USD 3.06 Billion in 2024 and reached USD 3.80 Billion in 2025. The market is projected to grow to USD 26.40 Billion by 2034, expanding at a CAGR of 24.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 22.60 Billion over the analysis period. The real estate tokenization market is defined as the set of technology platforms, regulated intermediaries, and legal structures that convert ownership rights in physical property into digital securities recorded on blockchain networks such as Ethereum, Polygon, Avalanche, and Stellar. Aggregated platform disclosures and industry analysis indicate that more than USD 4.2 billion in property assets globally had been issued or were in active issuance as tokenized securities by mid-2025.

Get More Information about this report -

Request Free Sample ReportThe scope covers commercial, residential, industrial, and mixed-use properties structured through Regulation D, Regulation S, Regulation A+, or equivalent foreign exemptions, plus the enabling infrastructure layer of transfer agents, Alternative Trading Systems, and on-chain custodians. Excluded are unregulated utility token experiments, NFT art collections, and metaverse land assets with no underlying physical real estate. The market sits within the wider real-world asset tokenization category, which crossed USD 33.9 billion in total on-chain capitalization during 2025 per RWA.xyz data.

Primary demand is driven by fractional ownership economics and institutional liquidity needs. Platforms such as RealT and HoneyBricks enabled retail investors to purchase property tokens from USD 50, while Securitize tokenized over USD 4 billion in institutional assets by October 2025 for partners including BlackRock, Apollo, Hamilton Lane, and KKR. The BlackRock USD Institutional Digital Liquidity Fund, tokenized by Securitize, crossed USD 2 billion in assets under management by March 2026, signaling deep institutional commitment to tokenized finance rails.

The regulatory environment shifted decisively in 2025. The US Securities and Exchange Commission issued its Staff Statement on Tokenized Securities on January 28, 2026, confirming that federal securities laws apply uniformly to tokenized instruments. The GENIUS Act, signed in July 2025, established stablecoin rules underpinning tokenized settlement. The European Union's Markets in Crypto-Assets regulation became fully operational across member states by December 30, 2024, and the Dubai Land Department launched its Real Estate Tokenization Project pilot in March 2025, coordinated with the Virtual Assets Regulatory Authority.

Technology innovation centers on compliance-native token standards, specifically ERC-3643 and ERC-7518, which embed transfer restrictions, KYC allow-listing, and jurisdictional controls at the smart contract level. Tokeny's T-REX platform and Polymath's Polymesh blockchain have deployed over 200 compliant security tokens, while Blocksquare standardized legal wrappers through its Corporate Resolution model. These technical stacks reduce issuance costs by approximately 30% compared with traditional private placement structures.

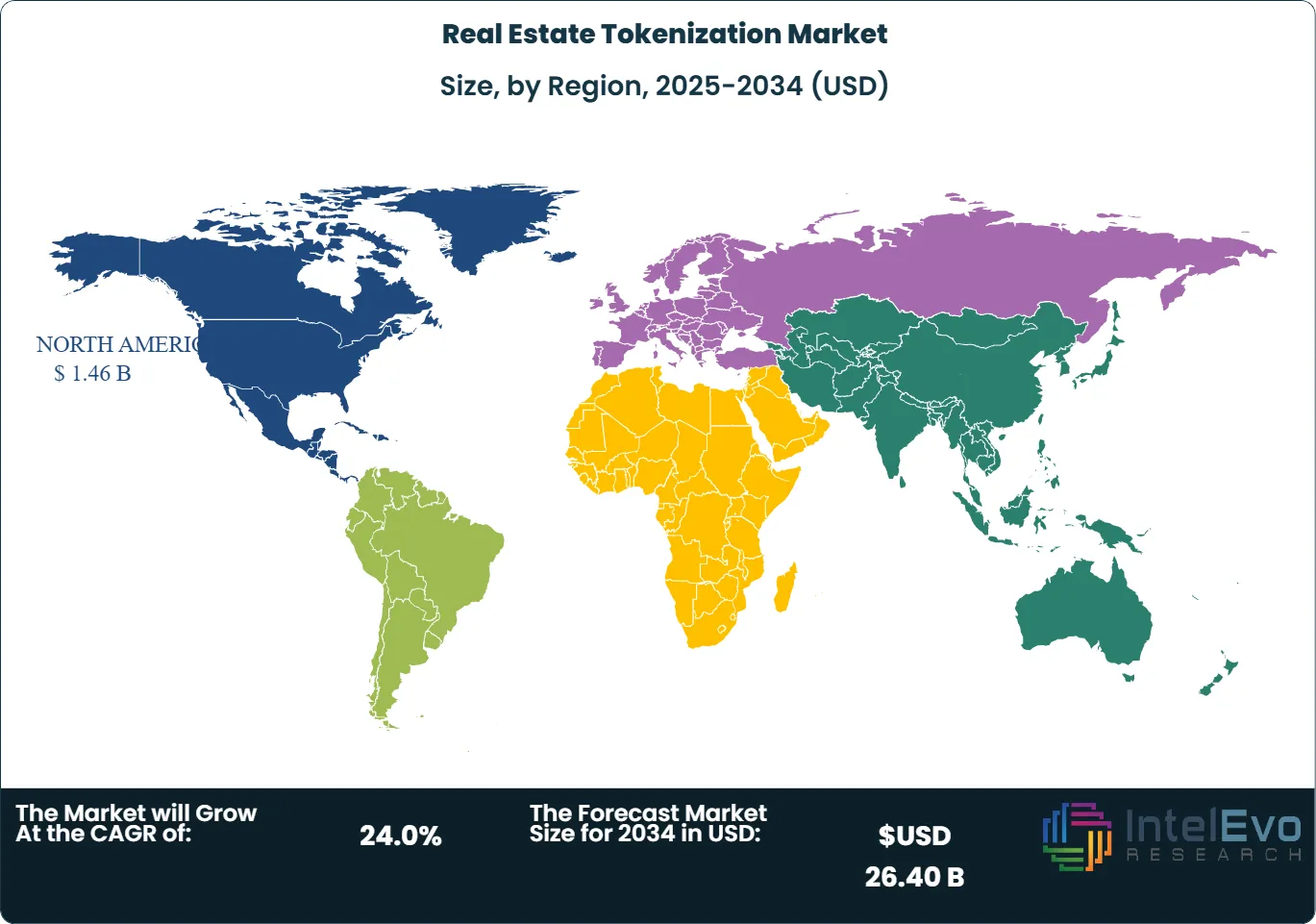

North America led regional demand at USD 1.46 Billion in 2025, supported by SEC-registered Alternative Trading Systems operated by Securitize and tZERO. Asia Pacific registered the fastest growth trajectory through 2034, anchored by Singapore's Project Guardian and Japan's Tokyo-based tokenization programs covering USD 75 million in initial commercial assets with ambitions to reach USD 200 billion. Europe benefits from MiCA harmonization, with more than 53 Crypto-Asset Service Provider licenses granted EU-wide by November 2025.

The competitive structure is moderately consolidated, with Securitize, tZERO, RealT, and Blocksquare accounting for a substantial share of live tokenized real estate volume. Secondary liquidity remains the principal bottleneck. Platform-native marketplaces currently clear most trades, but regulated venues including the New York Stock Exchange signed a Memorandum of Understanding with Securitize in March 2026 to support tokenized securities trading. Through 2034, the market is expected to shift toward income-bearing token structures backed by rental yields and debt tranches, with institutional portfolios serving as the primary growth engine.

, By Component (Platform, Services), By Deployment Mode (Cloud, On-Premises), By End-User (Institutional Investors, Individual Investors, Real Estate Developers, Property Management Companies) Industry Region & Key Players, Market Dynamics, Blockchain Adoption Trends, Competitive Strategies & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global real estate tokenization market expanded from USD 3.80 Billion in 2025 to a projected USD 26.40 Billion by 2034, growing at a CAGR of 24.0% during the forecast period.

- Segment Dominance (By Type): Commercial real estate tokenization accounted for approximately 38.2% of total market revenue in 2025, led by office buildings, hotels, and logistics assets issued through Regulation D exemptions.

- Segment Dominance (By End-User): Institutional investors including pension funds, family offices, and asset managers held approximately 69.1% share of deployed capital in 2025 across tokenized property structures.

- Driver: Fractional ownership economics enabled minimum ticket sizes as low as USD 50 on platforms such as RealT and HoneyBricks, unlocking an addressable retail investor pool valued at USD 12 trillion in US household real estate equity.

- Restraint: Regulatory fragmentation across 40+ national frameworks increased compliance costs by an estimated 15% to 25% of issuance value for cross-border tokenized real estate offerings.

- Opportunity: Tokenization of institutional real estate portfolios managed by pension funds, insurance companies, and sovereign wealth funds represents an addressable opportunity exceeding USD 750 billion at a 5% conversion rate of the USD 15 trillion direct real estate pool.

- Trend: Yield-bearing token structures backed by rental income and real estate debt represented approximately 42% of new issuances in 2025, replacing earlier equity-only fractional models.

- Regional Analysis: North America captured approximately 38.4% of global revenue in 2025, equivalent to USD 1.46 Billion, led by the United States under SEC oversight and Regulation D exemptions.

Key Insights Summary

- BlackRock's tokenized money market fund BUIDL, administered by Securitize, crossed USD 2 billion in assets under management by March 2026, a tenfold increase from its initial USD 200 million at launch in March 2024, per Securitize disclosures.

- Securitize reported USD 4 billion in tokenized assets under management across partnerships with Apollo, BlackRock, Hamilton Lane, KKR, and VanEck as of October 2025, with a pre-money equity value of USD 1.25 billion in its SPAC merger with Cantor Equity Partners II.

- The total value of on-chain real-world assets reached approximately USD 33.9 billion in 2025, with tokenized real estate representing the largest non-treasury asset class within that figure per RWA.xyz tracking data.

- Dubai recorded AED 66.8 billion, equivalent to USD 18.2 billion, in real estate sales during May 2025 alone, with the Dubai Land Department launching its Real Estate Tokenization Project pilot in March 2025 under the Real Estate Evolution Space initiative.

- The number of EU Crypto-Asset Service Provider licenses granted under the Markets in Crypto-Assets regulation exceeded 53 by November 2025, formalizing cross-border operation for tokenized real estate platforms across all 27 member states.

- Institutional investor allocation to tokenized assets is projected at 7% to 9% of portfolios by 2027 per public investor sentiment surveys, compared with less than 1% exposure in 2023.

- Tokenization reduces real estate transaction costs by approximately 30% through automated compliance, elimination of intermediaries, and faster settlement cycles, per industry implementation benchmarks.

Competitive Landscape Overview

The global real estate tokenization market is moderately consolidated, with Securitize, tZERO, RealT, and Blocksquare together estimated to control more than 55% of live tokenized real estate issuance volume in 2025 based on aggregated platform disclosures. Competition is increasingly platform-based and regulatory-native rather than purely technological. Securitize extended its lead following the March 2024 launch of BlackRock's BUIDL fund, now exceeding USD 2 billion, and its October 2025 SPAC merger with Cantor Equity Partners II at a USD 1.25 billion valuation. Competitive evolution is shifting from early-stage residential tokenization toward institutional-grade commercial real estate, private credit, and debt tranches. New entrants such as Zoniqx, StegX, and Kin Capital are targeting specialized verticals including cross-border institutional real estate and performing trust deeds. Regulatory licensing is becoming the decisive moat, with SEC-registered transfer agent status, ATS licenses, and VARA authorizations gating market access.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move (2024-2026) |

|---|---|---|---|---|---|

| Securitize Inc. | Miami, USA | Leader | BUIDL tokenization; SEC-registered ATS | North America, EU, UAE | Oct 2025: SPAC merger with Cantor Equity Partners II at USD 1.25B valuation |

| tZERO Group Inc. | New York, USA | Leader | tZERO ATS; tZERO Chain for tokenized securities | North America | Jul 2025: Announced tZERO Chain launch with up to USD 1B tokenized assets |

| RealT Inc. | Florida, USA | Leader | Fractional US rental property tokens on Ethereum | North America, Europe | 2025: Tokenized over USD 150M in multifamily units across 20,000+ investors |

| Blocksquare Ltd. | Ljubljana, Slovenia | Leader | White-label tokenization; Corporate Resolution legal model | Europe, Global | 2025: Standardized Corporate Resolution framework across all deployed assets |

| Tokeny Solutions SA | Luxembourg | Challenger | T-REX onchain finance OS; ERC-3643 standard | Europe, MENA | 2025: Expanded multi-chain deployment across EVM-compatible networks |

| Polymath Research Inc. | Toronto, Canada | Challenger | Polymesh permissioned blockchain; ST-20 standard | North America, Europe | 2025: Deployed 200+ security tokens on Polymesh chain |

| Zoniqx Inc. | Silicon Valley, USA | Niche Player | Tokenized Asset Lifecycle Management platform | Asia Pacific, UAE | 2025: Partnered with StegX to tokenize over USD 100M in institutional real estate |

| Elevated Returns LLC | New York, USA | Niche Player | Hospitality and emerging-market tokenization | Asia Pacific, North America | 2025: Continued hotel tokenization pipeline via Thailand and St. Regis Aspen |

| DigiShares ApS | Copenhagen, Denmark | Challenger | White-label real estate tokenization; 90+ wallet integrations | Europe, Global | Mid-2025: Crossed USD 1B in streamlined tokenized securities across 40+ countries |

| RedSwan CRE | Texas, USA | Niche Player | Large-scale commercial real estate tokenization | North America | 2025: Maintained focus on tokenized institutional commercial properties |

By Type

By type, the real estate tokenization market is segmented into Commercial Real Estate, Residential Real Estate, Industrial Real Estate, Single Asset, and Multiple Asset structures, with commercial real estate holding the dominant 38.2% share in 2025. Commercial properties generated approximately USD 1.45 billion in tokenized issuance value in 2025 across office towers, hospitality assets, retail centers, and trophy mixed-use developments. Institutional demand drives the category because commercial leases produce predictable cash flows suitable for yield-bearing token structures. Platforms such as RedSwan CRE, Elevated Returns, and Securitize focused on Class A office and hotel tokenizations throughout 2025, with multi-hundred-million-dollar transactions completed via SEC-registered Regulation D 506(c) exemptions.

Residential real estate accounted for approximately 26.8% of market revenue in 2025, equivalent to USD 1.02 billion, growing rapidly as retail platforms scaled investor bases. RealT tokenized over USD 150 million in US multifamily properties with more than 20,000 onboarded investors by end-2025, while HoneyBricks, now operating via EquityMultiple, closed USD 180 million in deals for 3,500 investors. Industrial real estate captured approximately 12.5% share through logistics park tokenization, a segment accelerated by e-commerce demand. The Multiple Asset sub-segment, covering tokenized portfolios rather than single properties, represented approximately 14.5% share in 2025 and grew fastest at an estimated 27% CAGR because portfolio tokens offer built-in diversification to investors. Single Asset structures held the remaining 8.0% and are typically used for trophy hotel or marquee office tokenizations such as the 2018 St. Regis Aspen benchmark transaction.

By Component

By component, the market divides into Platform and Services, with Platform accounting for approximately 59.1% of revenue in 2025. Platform revenue includes middleware, tokenization engines, compliance modules, and transfer agent software delivered by Securitize, Tokeny, Polymath, DigiShares, and Blocksquare. The tokenized issuance workflow spans KYC onboarding, legal structuring, smart contract deployment, cap table management, and distribution, all priced on a mixture of one-time setup fees and recurring AUM-linked charges. Securitize disclosed USD 18 million of platform revenue in Q2 2025 alone, reflecting the economics of scaled platform operations.

Services captured approximately 40.9% of market revenue in 2025, spanning legal structuring, tax advisory, fund administration, compliance audits, and investor relations. Services revenue grows proportionally with average transaction size because larger tokenized offerings demand more extensive due diligence, valuation, and regulatory coordination. The acquisition of MG Stover's fund administration business by Securitize in April 2025 illustrates the strategic integration of services capacity into platform companies. Compliance and legal-technology sub-services are expanding fastest at an estimated 47% CAGR through 2034, driven by MiCA, VARA, and SEC reporting mandates that require continuous regulatory-maintenance cycles.

By Deployment Mode

By deployment, Cloud-based platforms held approximately 72.4% share in 2025 compared with On-Premises at 27.6%, a ratio expected to widen further by 2034. Cloud deployment dominates because tokenization workflows require 24/7 global investor access, continuous smart contract monitoring, and rapid scaling during issuance events. Platforms including Securitize, Tokeny, and DigiShares run on AWS, Azure, and Google Cloud infrastructure, integrating with public blockchains such as Ethereum, Polygon, Avalanche, and Stellar. On-Premises deployments serve tier-one banks and sovereign wealth funds with strict data residency rules, with JPMorgan's Kinexys network being a notable example of private permissioned infrastructure that processed USD 1.5 trillion in tokenized transactions through 2024.

By End-User

By end-user, Institutional Investors held approximately 69.1% of deployed capital in 2025, followed by Individual Investors at 18.4%, Real Estate Developers at 8.7%, and Property Management Companies at 3.8%. Institutional dominance reflects the concentration of BlackRock, Apollo, KKR, Hamilton Lane, and VanEck allocations through Securitize-administered vehicles. Individual investor activity is concentrated on RealT, Binaryx, and HoneyBricks, with average ticket sizes under USD 500. Real Estate Developers increasingly use tokenization as a capital-raising alternative, as demonstrated by Dar Global's plan to finance up to 70% of a Maldives luxury resort project via token sales announced in late 2025. The Individual Investor segment is projected to grow fastest at approximately 50.2% CAGR through 2031, narrowing the institutional share over time as retail platforms expand secondary liquidity.

Regional Analysis

North America

North America held the largest real estate tokenization market share at approximately 38.4% in 2025, equivalent to USD 1.46 Billion. The United States anchors regional demand through SEC-registered infrastructure operated by Securitize and tZERO, supported by Regulation D 506(c), Regulation A+, and Regulation S exemptions. The January 28, 2026 SEC Staff Statement on Tokenized Securities formalized securities-law treatment of digital property tokens, while the GENIUS Act enacted in July 2025 established stablecoin rules underpinning settlement rails. Canada contributed through Polymath's Toronto headquarters and provincial sandbox programs under National Instrument 45-106. Venture capital committed USD 2.4 billion of fresh blockchain-focused capital in 2024, reinforcing the regional innovation loop.

Europe

Europe captured approximately 31.2% of the global market in 2025, equivalent to USD 1.19 Billion, led by Germany, Switzerland, France, and the United Kingdom. The European Union's Markets in Crypto-Assets regulation became fully applicable on December 30, 2024, and more than 53 Crypto-Asset Service Provider licenses were granted across member states by November 2025. Switzerland remains the leading tokenization-friendly jurisdiction through its DLT Act, with Zug serving as a blockchain cluster. The DLT Pilot Regime under EU Regulation 2022/858 was extended into 2026, enabling sandbox testing for tokenized securities settlement by regulated institutions. Luxembourg emerged as a preferred domicile for cross-border tokenized funds, supported by Tokeny Solutions SA.

Asia Pacific

Asia Pacific represented approximately 18.6% of the market in 2025, equivalent to USD 0.71 Billion, and is projected as the fastest-growing region through 2034 at an estimated 27.6% CAGR. Singapore's Project Guardian, governed by the Monetary Authority of Singapore, involves more than 40 financial institutions testing tokenized bonds, deposits, and funds on interoperable ledgers. Japan launched one of the largest tokenized real estate projects in 2025, with a Tokyo-based firm tokenizing USD 75 million in commercial properties and targeting USD 200 billion in scale. Hong Kong's Securities and Futures Commission extended tokenization guidelines, while India's SEBI framework continues to evolve under FEMA restrictions. Australia's ASIC sandbox supported early-stage platform pilots throughout 2025.

The Middle East and Africa

The Middle East and Africa region accounted for approximately 7.3% share in 2025, equivalent to USD 0.28 Billion, led by the United Arab Emirates and Saudi Arabia. Dubai's Virtual Assets Regulatory Authority introduced the Asset-Referenced Virtual Assets classification in May 2025, while the Dubai Land Department launched Phase One of its Real Estate Tokenization Project pilot in March 2025 in partnership with the Dubai Future Foundation. Phase Two commenced in February 2026 through a joint initiative with Ctrl Alt, enabling secondary market trading of ten tokenized assets with on-chain land registry updates. Saudi Arabia's Dar Global announced a tokenized luxury resort financing for up to 70% of project value in late 2025. South Africa contributed through FSCA digital asset guidelines issued in 2025.

Latin America

Latin America captured approximately 4.5% of global revenue in 2025, equivalent to USD 0.17 Billion, anchored by Brazil and Mexico. Brazil's COFECI issued Resolution 1.551 in 2025, establishing the first specific real estate tokenization rules at the broker level, while the CVM ran regulatory sandbox projects under Instrução CVM 626 that completed full tokenized securities issuance-distribution-burn cycles. Mexico and Colombia progressed on fintech-law amendments covering digital securities, and Argentina piloted stablecoin-linked property offerings in 2025. Regional growth is constrained by currency volatility and limited investor accreditation infrastructure but benefits from strong retail interest in dollarized yield tokens.

Country Analysis

United States

The United States real estate tokenization market was valued at approximately USD 1.36 Billion in 2025 and is projected to expand at a CAGR of 23.4% through 2034, retaining the largest single-country share globally. Demand is driven by institutional allocations through Securitize-administered vehicles including BlackRock BUIDL, Apollo ACRED private credit tokens, and Hamilton Lane's Senior Credit Opportunities Fund. The SEC Staff Statement on Tokenized Securities issued on January 28, 2026 confirmed that federal securities laws apply without modification to tokenized property, while Regulation D 506(c), Regulation A+, and Regulation S remain the dominant issuance exemptions. The GENIUS Act signed in July 2025 formalized stablecoin infrastructure used for on-chain settlement. Leading platforms such as Securitize, tZERO, RealT, and HoneyBricks completed multiple transactions exceeding USD 100 million each in 2025. The New York Stock Exchange signed a Memorandum of Understanding with Securitize in March 2026 to support tokenized securities settlement.

United Arab Emirates

The UAE real estate tokenization market reached approximately USD 0.17 Billion in 2025, expanding at an estimated CAGR of 32.1% through 2034, the fastest among tracked jurisdictions. Growth is led by the Dubai Land Department's Real Estate Tokenization Project, which launched its pilot in March 2025 under the Real Estate Evolution Space program and entered Phase Two in February 2026 with Ctrl Alt opening secondary market trading for ten tokenized properties. The Virtual Assets Regulatory Authority introduced the Asset-Referenced Virtual Assets licensing regime in May 2025, requiring whitepapers, proof of reserves, and redemption rights for token issuers. Dubai recorded AED 66.8 billion, or USD 18.2 billion, in property sales in May 2025 alone, with 44% year-on-year growth. DAMAC signed an agreement with MANTRA in 2025 to tokenize up to USD 1 billion in real estate and debt.

Singapore

Singapore's real estate tokenization market was valued at approximately USD 0.12 Billion in 2025 with an estimated CAGR of 29.4% through 2034. The Monetary Authority of Singapore's Project Guardian anchors the ecosystem, involving over 40 financial institutions testing tokenized bonds, deposits, and property funds on interoperable ledgers. The Guardian Funds Framework enables compliant tokenization of real estate investment trusts, and the Guardian Composable Token Economy allows cross-jurisdictional transfers between Singapore, Japan, and Switzerland. Project Ubin legacy infrastructure supports settlement, while STACS and ADDX provide local issuance platforms. Real estate tokenization demand is concentrated in commercial office and hospitality assets, with institutional investors including sovereign wealth allocators participating alongside retail accredited investors under MAS licensing.

Germany

Germany's real estate tokenization market was valued at approximately USD 0.28 Billion in 2025, with a projected CAGR of 25.2% through 2034. The Electronic Securities Act, known as eWpG, recognizes DLT-based securities registries, and the DEEP framework supports tokenized bearer bonds and real estate fund units. BaFin issued guidance through 2025 aligning MiCA implementation with national securities law under MiFID II. Berlin and Frankfurt serve as principal issuance hubs, with platforms such as Tangany, Finexity, and Brickwise enabling fractional property tokens starting at EUR 1,000. Institutional adoption is led by Commerzbank and DekaBank pilot programs, and the German Investment Fund Act allows tokenized fund units issued through registered KVGs.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Commercial Real Estate

- Residential Real Estate

- Industrial Real Estate

- Single Asset

- Multiple Asset

By Component

- Platform

- Services

By Deployment Mode

- Cloud

- On-Premises

By End-User

- Institutional Investors

- Individual Investors

- Real Estate Developers

- Property Management Companies

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.80 B |

| Forecast Revenue (2034) | USD 26.40 B |

| CAGR (2025-2034) | 24.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type, (Commercial Real Estate, Residential Real Estate, Industrial Real Estate, Single Asset, Multiple Asset), By Component, (Platform, Services), By Deployment Mode, (Cloud, On-Premises), By End-User, (Institutional Investors, Individual Investors, Real Estate Developers, Property Management Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SECURITIZE, INC., TZERO GROUP, INC., REALT, INC., BLOCKSQUARE LTD., TOKENY SOLUTIONS SA, POLYMATH RESEARCH INC., ZONIQX, INC., ELEVATED RETURNS LLC, DIGISHARES APS, REDSWAN CRE MARKETPLACE LLC, HONEYBRICKS (EQUITYMULTIPLE), REALBLOCKS INC., PROPY INC., BRICKKEN SOLUTIONS S.L., STOBOX TECHNOLOGIES INC., SLICE MARKETS INC., SOLIDBLOCK INC., BINARYX LTD., STEGX LTD., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Component (Platform, Services), By Deployment Mode (Cloud, On-Premises), By End-User (Institutional Investors, Individual Investors, Real Estate Developers, Property Management Companies) Industry Region & Key Players, Market Dynamics, Blockchain Adoption Trends, Competitive Strategies & Forecast 2026-2034")

, By Component (Platform, Services), By Deployment Mode (Cloud, On-Premises), By End-User (Institutional Investors, Individual Investors, Real Estate Developers, Property Management Companies) Industry Region & Key Players, Market Dynamics, Blockchain Adoption Trends, Competitive Strategies & Forecast 2026-2034")

, By Component (Platform, Services), By Deployment Mode (Cloud, On-Premises), By End-User (Institutional Investors, Individual Investors, Real Estate Developers, Property Management Companies) Industry Region & Key Players, Market Dynamics, Blockchain Adoption Trends, Competitive Strategies & Forecast 2026-2034")

Frequently Asked Questions

How big is the Real Estate Tokenization Market?

The Global Real Estate Tokenization Market was valued at USD 3.06 Billion in 2024 and is projected to reach USD 26.40 Billion by 2034, growing at a CAGR of 24.0% from 2026 to 2034. Growth is driven by increasing adoption of blockchain technology, fractional property ownership, smart contracts, digital asset-backed securities, decentralized finance (DeFi), enhanced liquidity solutions, and growing institutional investment in tokenized commercial and residential real estate assets worldwide.

Who are the major players in the Real Estate Tokenization Market?

SECURITIZE, INC., TZERO GROUP, INC., REALT, INC., BLOCKSQUARE LTD., TOKENY SOLUTIONS SA, POLYMATH RESEARCH INC., ZONIQX, INC., ELEVATED RETURNS LLC, DIGISHARES APS, REDSWAN CRE MARKETPLACE LLC, HONEYBRICKS (EQUITYMULTIPLE), REALBLOCKS INC., PROPY INC., BRICKKEN SOLUTIONS S.L., STOBOX TECHNOLOGIES INC., SLICE MARKETS INC., SOLIDBLOCK INC., BINARYX LTD., STEGX LTD., OTHERS

Which segments covered the Real Estate Tokenization Market?

By Type, (Commercial Real Estate, Residential Real Estate, Industrial Real Estate, Single Asset, Multiple Asset), By Component, (Platform, Services), By Deployment Mode, (Cloud, On-Premises), By End-User, (Institutional Investors, Individual Investors, Real Estate Developers, Property Management Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Real Estate Tokenization Market

Published Date : 01 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date