- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Real-World Evidence Solutions Market Size, Share | CAGR 16.2%

Global Real-World Evidence Solutions Market Size, Share, Growth Analysis By Offering (Software & Technology Platforms, Data Services & Real-World Data Assets, Professional & Managed Services), By Application (Drug Development, Pharmacovigilance, HTA, Outcomes Research), By Data Source (EHR, Claims Data, Patient Registries, Wearables), By End-User, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

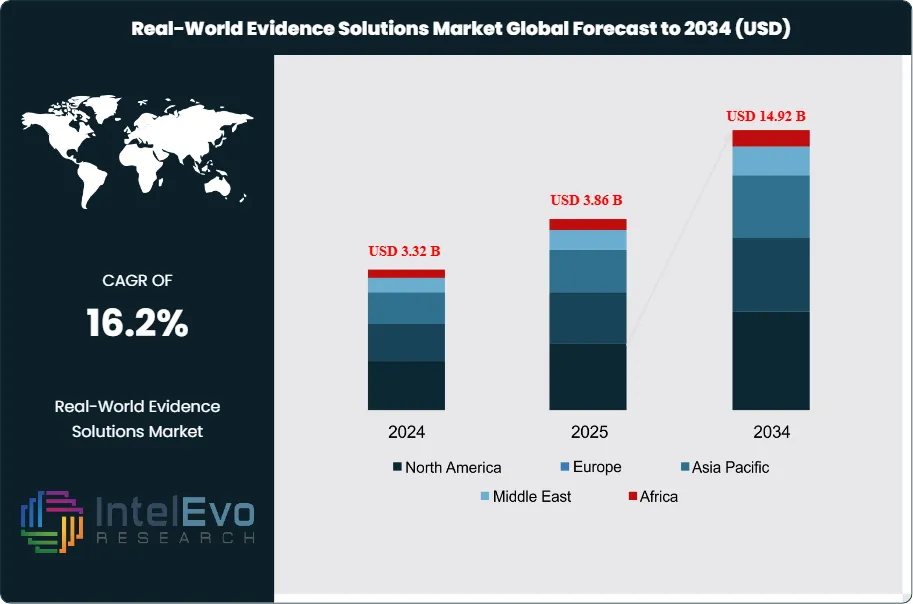

| USD 3.86 Billion | USD 14.92 Billion | 16.2% | North America, 46.9% |

The Real-World Evidence Solutions Market was valued at approximately USD 3.32 Billion in 2024 and reached USD 3.86 Billion in 2025. The market is projected to grow to USD 14.92 Billion by 2034, expanding at a CAGR of 16.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 11.06 Billion over the analysis period, driven by regulatory agency acceptance of real-world data in drug approval submissions, escalating pharmaceutical R&D costs that incentivize evidence generation from existing patient populations, and the maturation of electronic health record infrastructure producing the large-scale, longitudinal data assets that underpin RWE generation.

Get More Information about this report -

Request Free Sample ReportReal-world evidence solutions encompass the technologies, platforms, and professional services that enable the collection, curation, analysis, and regulatory submission of data derived from routine clinical practice rather than controlled clinical trial settings. The primary data sources feeding RWE platforms include electronic health records, administrative claims databases, patient registries, pharmacy dispensing records, wearable and remote monitoring device outputs, and patient-reported outcomes collected through digital health applications. RWE analysis applies epidemiological methods, propensity score matching, target trial emulation frameworks, and increasingly machine learning models to answer questions about treatment effectiveness, comparative safety, medication adherence, health economic outcomes, and disease natural history in real patient populations that are broader, older, and more comorbid than clinical trial populations.

Regulatory momentum has materially expanded the commercial rationale for real-world evidence solutions investment. The FDA’s 21st Century Cures Act and subsequent Real-World Evidence Framework, finalized in guidance documents through 2022 to 2024, established programmatic pathways for using RWE to support new indications, post-market safety commitments, and label modifications for approved drugs. The European Medicines Agency’s DARWIN EU federated real-world data network and the EMA’s updated RWE guidance for regulatory decision-making create parallel European demand for evidence-grade RWE platform capability. The International Coalition of Medicines Regulatory Authorities has advanced harmonization of RWE standards across FDA, EMA, PMDA, Health Canada, and TGA, extending the geographic scope of regulatory RWE acceptance.

Pharmaceutical and biotechnology companies represent the largest buyer segment, integrating RWE into clinical development strategy from Phase II through post-market commitments. The average cost of bringing a new drug to market exceeded USD 2.5 Billion in 2025, and RWE-supported evidence generation strategies that reduce late-phase clinical trial requirements for secondary endpoints or label expansion indications are generating measurable development cost savings. Medical device manufacturers have parallel RWE needs tied to the FDA’s National Evaluation System for Health Technology and the EU MDR’s post-market clinical follow-up requirements that mandate ongoing real-world clinical performance evidence.

The commercial ecosystem has expanded rapidly through strategic acquisitions and venture capital deployment. Large data analytics companies, specialty pharma services firms, and health IT vendors have acquired real-world data asset owners and RWE technology platforms to build integrated evidence generation capabilities. The intersection of AI-powered data curation, federated learning across distributed health data networks, and large language model-based medical record abstraction is creating a new generation of RWE platforms that can generate evidence at speed and scale that was computationally impractical five years ago. Asia Pacific, particularly Japan and South Korea, is emerging as a high-growth regional market as regulatory agencies align with international RWE standards and national electronic health record infrastructure matures.

, By Application (Drug Development, Pharmacovigilance, HTA, Outcomes Research), By Data Source (EHR, Claims Data, Patient Registries, Wearables), By End-User, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global real-world evidence solutions market was valued at USD 3.86 Billion in 2025 and is projected to reach USD 14.92 Billion by 2034, growing at a CAGR of 16.2% during the forecast period 2026–2034.

- Segment Dominance: By offering, software and technology platforms account for the largest share at approximately 58.3% of market revenue in 2025, driven by enterprise licensing of RWE analytics platforms, EHR-linked data curation tools, and AI-powered evidence generation applications by pharmaceutical and biotechnology companies.

- Segment Dominance: By application, drug and biologics development represents the dominant application segment at approximately 52.7% of market revenue in 2025, reflecting pharmaceutical and biotech investment in RWE for regulatory submissions, label expansion, and comparative effectiveness evidence to support market access and reimbursement negotiations.

- Driver: FDA and EMA regulatory acceptance of RWE for supplemental drug approvals and post-market commitments, codified through the 21st Century Cures Act framework and EMA’s DARWIN EU initiative, has converted RWE from an academic research methodology into a regulatory-grade evidence generation standard that pharmaceutical companies must invest in to remain competitive in drug development.

- Restraint: Data quality, completeness, and standardization challenges across heterogeneous electronic health record systems, administrative claims databases, and international data sources limit the reliability and regulatory defensibility of RWE analyses, with data quality issues cited as the primary reason for FDA non-acceptance of RWE submissions in approximately 35% of reviewed applications between 2022 and 2024.

- Opportunity: AI-powered large language model extraction of unstructured clinical notes to generate structured RWE datasets represents an addressable opportunity exceeding USD 2.2 Billion by 2034, as unstructured narrative data in EHR notes captures clinical detail unavailable in structured fields that is critical for confounding adjustment and endpoint validation in regulatory-grade RWE studies.

- Trend: Federated data network architectures, where RWE analyses run on distributed health data without centralizing patient records, were adopted in approximately 38% of regulatory RWE submissions in 2025, up from approximately 12% in 2021, driven by GDPR compliance requirements in Europe and patient privacy protections that prohibit centralized data sharing.

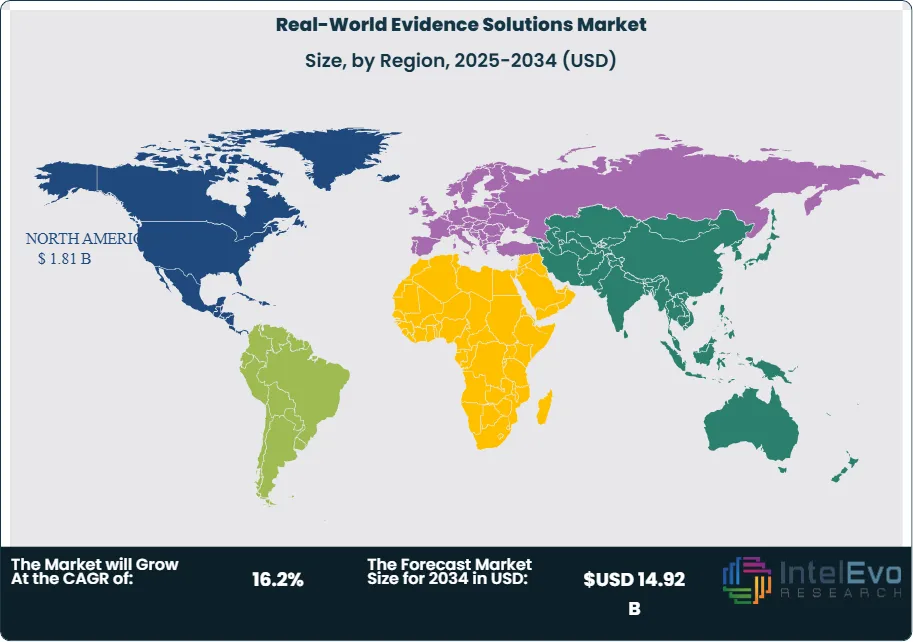

- Regional Analysis: North America leads with a 46.9% regional share, equivalent to approximately USD 1.81 Billion in 2025, supported by the FDA’s regulatory RWE framework, the world’s largest and most interoperable electronic health record ecosystem, and concentrated pharmaceutical industry R&D investment.

Competitive Landscape Overview

The global real-world evidence solutions market is moderately fragmented, with the top four companies holding a combined revenue share of approximately 43% in 2025. Competition spans technology platform capability, proprietary data asset scale, regulatory submission track record, and therapeutic area depth. The market has seen consistent acquisition activity as large analytics and health data companies build comprehensive RWE platform capabilities by acquiring specialty data owners, AI analytics startups, and contract research organizations with established regulatory RWE expertise. New entrants with AI-native RWE platforms are applying competitive pressure on established vendors through faster study execution timelines and cost-per-evidence metrics that established players are responding to with platform modernization programs.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Platform | Geo Strength | Recent Strategic Move |

| IQVIA Holdings | USA | Leader | IQVIA RWE Platform / Oculus | Global | Launched IQVIA AI-powered RWE evidence generation platform with LLM-based EHR abstraction; secured FDA pilot program for RWE submission support (Jan 2025) |

| Veeva Systems | USA | Leader | Veeva Compass / Evidence Engine | North America / Europe | Released Veeva Evidence Engine with integrated RWD sourcing and automated study protocol generation; expanded oncology RWE data partnerships (Mar 2025) |

| Optum (UnitedHealth Group) | USA | Leader | Optum Real World Solutions | North America | Expanded Optum RWE claims-to-EHR linked dataset to 100 million longitudinal patient records; launched federated network for multi-payer RWE studies (2025) |

| Parexel International | USA | Leader | Parexel RWE Services / PAREXEL Informatics | Global | Integrated AI-assisted target trial emulation into Parexel RWE service offering; expanded Europe RWE data partnerships with Nordic registries (Q2 2025) |

| Flatiron Health (Roche) | USA | Challenger | OncoEMR / Flatiron RWD Platform | North America / Europe | Launched cancer-specific RWE data curation platform update with genomic data linkage covering 4 million oncology patients (2025) |

| Komodo Health | USA | Challenger | Komodo Healthcare Map | North America | Closed USD 220 Million Series E; launched AI-powered patient journey analytics with specialty pharmacy data integration (2025) |

| TriNetX | USA | Niche Player | TriNetX Research Network | North America / Europe | Expanded federated EHR network to 180 health systems globally; launched trial-to-RWE matched cohort service (Jan 2026) |

| Medidata (Dassault Systèmes) | USA / France | Niche Player | Medidata Rave RWE | Global | Integrated RWE study design module into Medidata Rave clinical platform; launched adaptive trial-RWE hybrid design tooling (2025) |

By Offering

The real-world evidence solutions market by offering is segmented into software and technology platforms, data services and real-world data assets, and professional and managed services. Software and technology platforms hold the dominant revenue share at approximately 58.3% of market revenue in 2025, valued at roughly USD 2.25 Billion. This segment includes RWE study design and protocol automation tools, data curation and harmonization platforms, statistical analysis environments incorporating epidemiological methods, regulatory submission documentation software, and AI-powered evidence generation applications. Enterprise licensing of RWE analytics platforms by top-20 pharmaceutical companies, with annual contracts ranging from USD 3 Million to USD 15 Million depending on data volume and study throughput, drives the revenue concentration in this segment. AI-native RWE platforms incorporating large language model abstraction of unstructured EHR notes are growing at a materially higher rate within the software segment than legacy structured data analytics tools, reflecting the decisive competitive shift toward AI-augmented evidence generation workflows.

Data services and real-world data assets account for approximately 27.4% of market revenue in 2025 at USD 1.06 Billion. This segment encompasses proprietary claims and EHR linked databases, patient registries, pharmacy dispensing data networks, and laboratory results data assets licensed to pharmaceutical and health system customers on a subscription or per-study basis. The competitive moat in this segment is proprietary data depth, longitudinality, and linkage quality. Vendors with longitudinal patient records spanning 10 to 20 years provide richer confounding adjustment data than shorter-window datasets, and EHR-to-claims linkage that captures both clinical detail and reimbursement outcomes is significantly more valuable per patient record than either data type alone. Data asset pricing is shifting from per-study transaction models to enterprise subscription arrangements that allow unlimited query access within contracted patient population boundaries.

Professional and managed services represent approximately 14.3% of market revenue at USD 552 Million in 2025. This segment includes study design consulting, statistical analysis plan development, regulatory submission preparation, health technology assessment dossier development, and managed RWE study execution services provided by contract research organizations and specialized evidence generation consultancies. Professional services are particularly important for smaller biotechnology companies that lack internal RWE scientific and regulatory expertise, and for pharmaceutical companies requiring therapeutic area-specific expertise in cancer, rare disease, or cardiovascular medicine where RWE study design complexity exceeds general analytical capability.

By Application

Drug and biologics development represents the dominant application for real-world evidence solutions at approximately 52.7% of market revenue in 2025, valued at USD 2.03 Billion. Pharmaceutical and biotechnology companies use RWE across the full drug development lifecycle, from disease epidemiology characterization in early development through label expansion evidence generation for approved products. The FDA’s acceptance of RWE for supplemental NDA and BLA submissions has created direct regulatory value for RWE investment, with approved supplemental indications supported by RWE generating incremental revenues that directly fund platform investment. Oncology represents the single largest therapeutic area within drug development RWE, accounting for approximately 38% of drug development RWE spending in 2025, driven by the FDA’s broad acceptance of RWE in oncology post-market commitments and the high unmet clinical need that motivates accelerated approval pathways with real-world confirmatory requirements.

Medical device and diagnostics development accounts for approximately 18.4% of market revenue in 2025 at USD 710 Million. The EU MDR’s mandatory post-market clinical follow-up requirements and the FDA’s National Evaluation System for Health Technology have created regulatory mandates for ongoing RWE generation by device manufacturers that drive sustained annual spending. Comparative effectiveness and value-based health technology assessment represent approximately 15.6% of market revenue at USD 602 Million in 2025, driven by national health technology assessment agencies including NICE, the German IQWiG, France’s HAS, and ICER in the United States that increasingly require comparative RWE to support formulary coverage and pricing negotiations for new treatments. Safety and pharmacovigilance applications account for approximately 13.3% of revenue at USD 513 Million, while payer and outcomes research applications represent the remaining approximately 8.4% of market revenue at USD 324 Million.

By Data Source

Electronic health records are the largest data source powering real-world evidence solutions at approximately 41.2% of market revenue in 2025, valued at USD 1.59 Billion. EHR data contains granular clinical information including diagnoses, procedures, laboratory results, medication orders, clinical notes, and imaging reports that provide the endpoint and covariate richness required for regulatory-grade RWE studies. The United States benefits from the highest rate of EHR adoption globally, with over 96% of non-federal acute care hospitals using certified EHR systems as of 2024 per the Office of the National Coordinator for Health Information Technology, creating a data infrastructure that supports large-scale RWE cohort assembly. Administrative claims and insurance data account for approximately 28.7% of market revenue at USD 1.11 Billion, valued for their population completeness, longitudinality, and coverage of care utilization patterns across all healthcare settings. Patient registries represent approximately 18.4% of revenue at USD 710 Million, particularly important in rare disease, oncology, and specific chronic condition research where registry data captures treatment sequences and outcomes with depth exceeding claims and EHR sources. Patient-reported outcomes and wearable data represent approximately 11.7% of market revenue at USD 452 Million, a growing source reflecting the expansion of digital biomarker collection in decentralized clinical and post-market settings.

By End-User

Pharmaceutical and biotechnology companies represent the dominant end-user segment at approximately 54.8% of market revenue in 2025, valued at USD 2.12 Billion. Top-20 global pharmaceutical companies have established dedicated RWE centers of excellence that operate enterprise platform contracts, employing internal teams of epidemiologists, biostatisticians, and regulatory scientists who use RWE solutions as core drug development infrastructure. Medical device and diagnostics companies account for approximately 19.3% of market revenue at USD 745 Million in 2025. Healthcare payers and health technology assessment bodies represent approximately 13.6% of revenue at USD 525 Million, using RWE solutions for formulary decision support, value-based contract design, and health economic model validation. Government agencies, academic medical centers, and public health organizations collectively account for the remaining approximately 12.3% of market revenue at USD 475 Million.

Regional Analysis

North America

North America holds the largest share of the global real-world evidence solutions market at approximately 46.9%, equivalent to USD 1.81 Billion in 2025. The United States dominates regional revenue through the combined effect of FDA regulatory frameworks that formally accept RWE in drug approval submissions, the most advanced and interoperable electronic health record ecosystem globally, and the highest concentration of pharmaceutical and biotechnology R&D investment of any geography. The 21st Century Cures Act mandate for the FDA to develop RWE guidance has been implemented through a series of guidance documents covering EHR-based RWE studies, registry-based randomized trials, and single-arm trials with RWE external control arms, creating specific regulatory pathways that generate defined commercial demand for validated RWE solutions. The Centers for Medicare and Medicaid Innovation’s value-based payment model programs have created payer demand for comparative effectiveness RWE that supports outcomes-based contracting. Canada contributes to regional growth through the Canadian Network for Observational Drug Effect Studies and provincial health data linkage programs that provide nationally representative longitudinal data assets increasingly licensed to pharmaceutical customers. United States pharmaceutical company R&D investment exceeding USD 100 Billion annually in 2025 generates the primary commercial demand for North American RWE platform adoption.

Europe

Europe accounts for approximately 27.8% of global market revenue at USD 1.07 Billion in 2025. The European Medicines Agency’s DARWIN EU federated real-world data network, operational across 10 European countries as of 2025, provides a regulatory-endorsed data infrastructure for EMA-initiated and sponsor-requested RWE studies that is directly stimulating vendor investment in Europe-compatible RWE platform capabilities. Germany leads European adoption through the German National Electronic Health Record initiative expanding EHR data availability and the IQWiG’s established practice of requiring comparative effectiveness evidence from real-world settings for AMNOG drug benefit assessments. The United Kingdom’s NICE evidence standards framework explicitly accepts RWE for technology appraisals under specific methodological conditions, and the NHS Business Services Authority’s comprehensive prescribing and hospital episode data assets are among the most complete national health databases globally. France’s Health Data Hub (Plateforme des Données de Santé) has expanded access to linked EHR and claims data for regulatory and health technology assessment RWE studies. GDPR compliance requirements for health data use have driven adoption of federated network architectures across European RWE programs, creating specialized platform demand for privacy-preserving analytics infrastructure.

Asia Pacific

Asia Pacific represents approximately 17.4% of global market revenue at USD 672 Million in 2025 and is the second-fastest-growing regional segment. Japan leads Asia Pacific adoption through the Pharmaceuticals and Medical Devices Agency’s progressive acceptance of RWE in post-approval drug safety commitments and device performance monitoring, supported by the Japan Medical Informatics Association’s national EHR database consortium that provides longitudinal patient data assets across university hospital networks. The PMDA’s participation in the International Coalition of Medicines Regulatory Authorities RWE working group aligns Japanese standards with FDA and EMA frameworks, creating a harmonized evidence pathway that reduces per-country study replication costs for multinational pharmaceutical customers. South Korea’s Health Insurance Review and Assessment Service database, covering over 50 million patients with comprehensive claims and clinical data, is among the most complete national health datasets in the world and is increasingly licensed for pharmaceutical RWE studies. China’s National Medical Products Administration has advanced RWE guidance for supplemental indications in line with international standards, creating domestic demand from both Chinese pharmaceutical companies and multinational sponsors seeking NMPA approval. Australia’s Therapeutic Goods Administration and Pharmaceutical Benefits Advisory Committee have incorporated RWE into health technology assessment processes, creating Australasian demand aligned with developed market standards.

Latin America

Latin America represents approximately 5.1% of global market revenue at USD 197 Million in 2025. Brazil holds the dominant Latin American position through the DATASUS national health information system, which provides population-level administrative health data supporting public health research and pharmaceutical company pharmacovigilance studies, and through the active clinical research infrastructure of major Brazilian academic medical centers including Hospital das Clínicas and INCA. Brazil’s ANVISA regulatory agency has engaged with RWE standards harmonization through Panamerican Health Organization coordination, creating a regional regulatory trajectory that will progressively formalize RWE acceptance. Mexico and Colombia represent secondary markets with growing private sector pharmaceutical company RWE investment. Regional growth through the forecast period is constrained by EHR adoption rates that remain below 50% in most Latin American public health systems, limiting the primary data source available for high-quality EHR-based RWE. Pharmaceutical company-sponsored patient registries in oncology and rare disease are the primary commercial application driving near-term regional RWE revenue.

Middle East & Africa

The Middle East and Africa region accounts for approximately 2.8% of global market revenue at USD 108 Million in 2025. The Gulf Cooperation Council countries, particularly the UAE and Saudi Arabia, lead regional RWE investment through well-funded national health data infrastructure programs and pharmaceutical company medical affairs operations targeting reimbursement evidence generation for the Gulf’s expanding specialty pharmaceutical markets. The UAE’s Malaffi health information exchange in Abu Dhabi has created a federated clinical data asset covering the emirate’s hospital population that is being evaluated for RWE platform integration. Saudi Arabia’s Vision 2030 health transformation includes health data infrastructure investment that will materially expand the country’s RWE data asset availability. Israel contributes to regional totals through Clalit Health Services’ nationally representative electronic health records covering over 4 million patients, which are licensed for pharmaceutical RWE studies and have been used in more than 100 peer-reviewed publications forming the basis of regulatory submissions. South Africa leads Sub-Saharan African adoption through academic hospital research programs and pharmaceutical company pharmacovigilance studies.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software and Technology Platforms

- Data Services and Real-World Data Assets

- Professional and Managed Services

By Application

- Drug and Biologics Development

- Medical Device and Diagnostics Development

- Comparative Effectiveness and Health Technology Assessment

- Safety and Pharmacovigilance

- Payer and Outcomes Research

By Data Source

- Electronic Health Records (EHR)

- Administrative Claims and Insurance Data

- Patient Registries

- Patient-Reported Outcomes and Wearable Data

By End-User

- Pharmaceutical and Biotechnology Companies

- Medical Device and Diagnostics Companies

- Healthcare Payers and HTA Bodies

- Government Agencies and Academic Medical Centers

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.86 B |

| Forecast Revenue (2034) | USD 14.92 B |

| CAGR (2025-2034) | 16.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Software and Technology Platforms, Data Services and Real-World Data Assets, Professional and Managed Services), By Application, (Drug and Biologics Development, Medical Device and Diagnostics Development, Comparative Effectiveness and Health Technology Assessment, Safety and Pharmacovigilance, Payer and Outcomes Research), By Data Source, (Electronic Health Records (EHR), Administrative Claims and Insurance Data, Patient Registries, Patient-Reported Outcomes and Wearable Data), By End-User, (Pharmaceutical and Biotechnology Companies, Medical Device and Diagnostics Companies, Healthcare Payers and HTA Bodies, Government Agencies and Academic Medical Centers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | IQVIA HOLDINGS, FLATIRON HEALTH (ROCHE), KOMODO HEALTH, PAREXEL INTERNATIONAL, VEEVA SYSTEMS, OPTUM (UNITEDHEALTH GROUP), TRINETX, MEDIDATA (DASSAULT SYSTÈMES), IBM WATSON HEALTH (MERATIVE), CLINIGEN GROUP, REAL ENDPOINTS, EVIDERA (PPD / THERMO FISHER SCIENTIFIC), SYNEOS HEALTH, ARCADIA DATA HEALTH, OPEN HEALTH, CYTEL, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Drug Development, Pharmacovigilance, HTA, Outcomes Research), By Data Source (EHR, Claims Data, Patient Registries, Wearables), By End-User, Industry Trends & Forecast 2026-2034")

, By Application (Drug Development, Pharmacovigilance, HTA, Outcomes Research), By Data Source (EHR, Claims Data, Patient Registries, Wearables), By End-User, Industry Trends & Forecast 2026-2034")

, By Application (Drug Development, Pharmacovigilance, HTA, Outcomes Research), By Data Source (EHR, Claims Data, Patient Registries, Wearables), By End-User, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Real-World Evidence Solutions Market?

The Global Real-World Evidence Solutions Market was valued at USD 3.32 Billion in 2024 and is projected to reach USD 14.92 Billion by 2034, growing at a CAGR of 16.2% from 2026 to 2034, driven by rising adoption of real-world data analytics, increasing demand for evidence-based healthcare decision-making, expanding use of electronic health records and claims databases, and growing investments in AI-powered healthcare analytics, personalized medicine, and value-based care solutions.

Who are the major players in the Real-World Evidence Solutions Market?

IQVIA HOLDINGS, FLATIRON HEALTH (ROCHE), KOMODO HEALTH, PAREXEL INTERNATIONAL, VEEVA SYSTEMS, OPTUM (UNITEDHEALTH GROUP), TRINETX, MEDIDATA (DASSAULT SYSTÈMES), IBM WATSON HEALTH (MERATIVE), CLINIGEN GROUP, REAL ENDPOINTS, EVIDERA (PPD / THERMO FISHER SCIENTIFIC), SYNEOS HEALTH, ARCADIA DATA HEALTH, OPEN HEALTH, CYTEL, Others

Which segments covered the Real-World Evidence Solutions Market?

By Offering, (Software and Technology Platforms, Data Services and Real-World Data Assets, Professional and Managed Services), By Application, (Drug and Biologics Development, Medical Device and Diagnostics Development, Comparative Effectiveness and Health Technology Assessment, Safety and Pharmacovigilance, Payer and Outcomes Research), By Data Source, (Electronic Health Records (EHR), Administrative Claims and Insurance Data, Patient Registries, Patient-Reported Outcomes and Wearable Data), By End-User, (Pharmaceutical and Biotechnology Companies, Medical Device and Diagnostics Companies, Healthcare Payers and HTA Bodies, Government Agencies and Academic Medical Centers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Real-World Evidence Solutions Market

Published Date : 20 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date