- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Refinery Hydrogen Plant Market Size & Forecast 2034 | CAGR 7.6%

Global Refinery Hydrogen Plant Market Size, Share, Growth & Industry Analysis By Technology (Steam Methane Reforming (SMR), Autothermal Reforming (ATR), Partial Oxidation (POX) & Gasification, Electrolysis – Green & Blue Hydrogen), By Capacity (Large-Scale Above 50 MMSCFD, Medium-Scale 10–50 MMSCFD, Small-Scale Below 10 MMSCFD), By Application (Hydrodesulfurization, Hydrocracking, Catalytic Reforming, Others), By Component Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 7.64 Billion | USD 14.82 Billion | 7.6% | Asia Pacific, 35.4% |

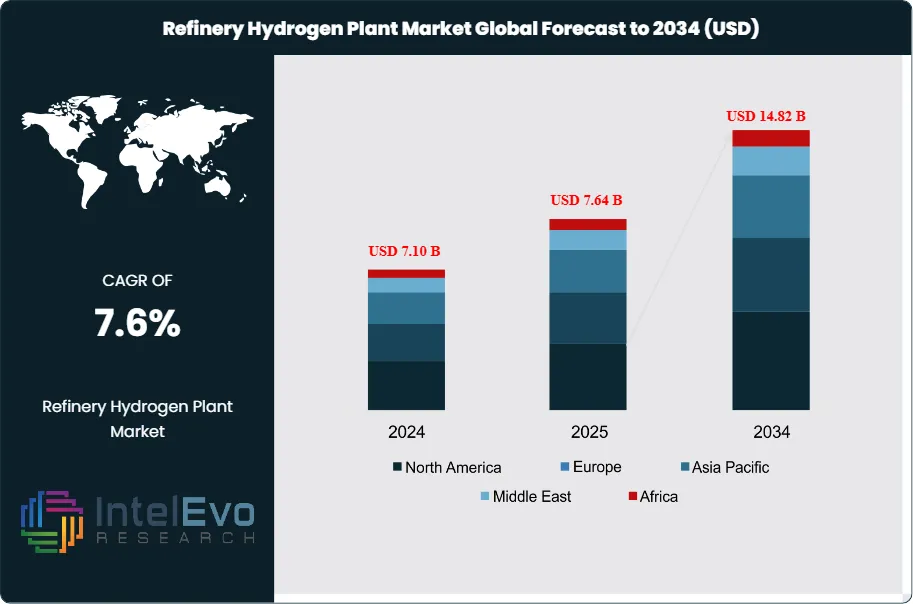

The Refinery Hydrogen Plant Market was valued at approximately USD 7.10 Billion in 2024 and reached USD 7.64 Billion in 2025. The market is projected to grow to USD 14.82 Billion by 2034, expanding at a CAGR of 7.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 7.18 Billion over the analysis period, driven by accelerating refinery hydrogen demand from ultra-low-sulfur fuel mandates, expanding hydrocracking capacity, and the integration of low-carbon hydrogen production pathways into downstream processing facilities globally.

Get More Information about this report -

Request Free Sample ReportRefinery hydrogen plants — predominantly steam methane reforming (SMR) units — are critical downstream infrastructure assets that supply the hydrogen required for hydrodesulfurization (HDS), catalytic reforming, and hydrocracking operations across petroleum refineries. As global transportation fuel sulfur standards have tightened — with IMO 2020 reducing marine fuel sulfur limits to 0.5%, Euro VI mandating less than 10 ppm sulfur in road diesel, and BS VI equivalent standards adopted across India and Southeast Asia — the hydrogen consumption per barrel of crude refined has increased structurally. IEA data estimates global refinery hydrogen demand at 40 million tonnes per year in 2025, of which approximately 70% is supplied by on-site SMR units, with the balance from hydrogen by-product recovery and merchant supply.

Steam methane reforming remains the dominant technology for refinery hydrogen production, accounting for 72.4% of installed capacity in 2025. Each SMR hydrogen plant involves a fired reformer furnace, shift converter, pressure swing adsorption (PSA) purification unit, and associated heat recovery systems. A modern large-scale refinery SMR unit producing 100-150 million standard cubic feet per day (MMSCFD) of 99.9% purity hydrogen represents a capital investment of USD 150-400 Million depending on feedstock availability, local engineering costs, and whether carbon capture provisions are incorporated. Autothermal reforming (ATR) and partial oxidation (POX) technologies are gaining market share in applications requiring feedstock flexibility or integration with carbon capture and storage (CCS) systems, as their concentrated CO2 product streams are more amenable to capture than the dilute flue gases produced by conventional SMR furnaces.

The Refinery Hydrogen Plant market is experiencing a structural expansion driven by two concurrent forces: near-term capacity additions to serve fuel quality mandates across Asia and the Middle East, and medium-term investment in low-carbon hydrogen production to comply with EU Emissions Trading Scheme obligations and SEC climate disclosure requirements for U.S. downstream operators. The EU Fit for 55 package and the U.S. Inflation Reduction Act's Section 45V hydrogen production tax credit — which provides up to USD 3.00 per kilogram for low-carbon hydrogen — are catalyzing investment in SMR units equipped with pre-combustion or post-combustion carbon capture, commonly termed blue hydrogen production.

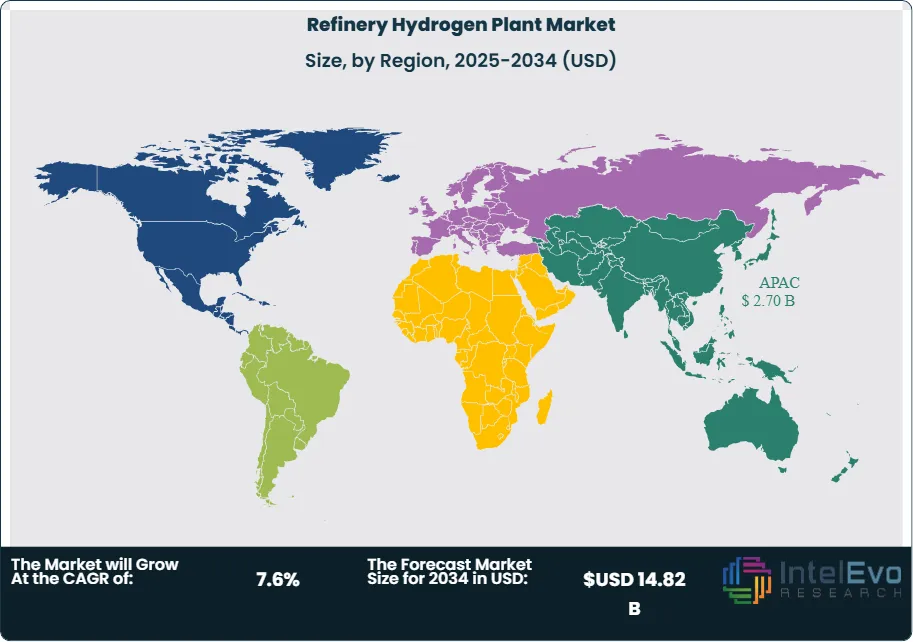

Asia Pacific leads the Refinery Hydrogen Plant market with 35.4% share at USD 2.70 Billion in 2025 and carries the highest regional CAGR at 8.8% through 2034. The Middle East and Africa hold 20.6% share and are growing at 8.2% CAGR, driven by Saudi Aramco, ADNOC, and Kuwait National Petroleum Company refinery expansion and conversion programs. The market is moderately consolidated, with Air Products, Linde, Air Liquide, and Technip Energies collectively holding approximately 58% of global EPC and technology licensing revenue in 2025.

, Autothermal Reforming (ATR), Partial Oxidation (POX) & Gasification, Electrolysis – Green & Blue Hydrogen), By Capacity (Large-Scale Above 50 MMSCFD, Medium-Scale 10–50 MMSCFD, Small-Scale Below 10 MMSCFD), By Application (Hydrodesulfurization, Hydrocracking, Catalytic Reforming, Others), By Component Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Global Refinery Hydrogen Plant Market was valued at USD 7.64 Billion in 2025 and is forecast to reach USD 14.82 Billion by 2034, at a CAGR of 7.6% during 2025–2034.

- Segment Dominance (By Technology): Steam Methane Reforming (SMR) is the dominant production technology with 72.4% market share in 2025 (USD 5.53 Billion), representing the established refinery hydrogen production standard across all major refining regions.

- Segment Dominance (By Capacity): Large-scale hydrogen plants (above 50 MMSCFD) represent the leading capacity segment at 52.8% of global revenue in 2025 (USD 4.03 Billion), reflecting the economics of scale that favor single large-train units over multiple smaller installations at integrated refinery complexes.

- Driver: Global refinery hydrogen demand of 40 million tonnes per year in 2025 — driven by ultra-low-sulfur fuel specifications including IMO 2020, Euro VI, and BS VI standards — is the primary market driver, requiring net new hydrogen production capacity across Asia, MEA, and North America.

- Restraint: Natural gas feedstock price volatility is the primary cost risk for SMR hydrogen plants: a USD 1.00/MMBtu increase in natural gas price raises SMR hydrogen production cost by approximately USD 0.06-0.08 per kilogram, materially affecting refinery hydrogen supply economics and project financial returns.

- Opportunity: The IRA Section 45V tax credit of up to USD 3.00 per kilogram for low-carbon hydrogen, combined with EU ETS-driven carbon cost pressure, creates an addressable market of USD 2.8 Billion for SMR-with-CCS (blue hydrogen) refinery hydrogen plant upgrades and new capacity through 2034.

- Trend: Integration of carbon capture provisions into new refinery hydrogen plant designs is accelerating, with 34.2% of new SMR hydrogen plant EPC contracts signed in 2025 including CCS-ready design provisions — up from 8% in 2021.

- Regional Analysis: Asia Pacific leads the Refinery Hydrogen Plant market with 35.4% share and USD 2.70 Billion in revenue in 2025, driven by Chinese refinery capacity expansion, Indian BS VI mandate compliance upgrades, and new refinery construction across Southeast Asia.

Competitive Landscape

The Refinery Hydrogen Plant market is moderately consolidated, with the top four technology and EPC providers — Air Products, Linde, Air Liquide, and Technip Energies — collectively holding approximately 58% of global EPC and technology licensing revenue in 2025. Competition is technology-driven in the reformer design and catalyst licensing segment, and project-bid-driven in EPC contract awards. The market has seen significant contract activity in 2025-2026, with major EPC awards in Saudi Arabia, Kuwait, Italy, and Indonesia confirming sustained capital commitment across all major refining regions. New entrants from the electrolysis sector are targeting niche applications but have not displaced SMR at commercial refinery scale.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Air Products and Chemicals | USA | Leader | SMR Hydrogen Plant (HyCO Technology) | North America / MEA | Awarded USD 1.1B SMR hydrogen plant EPC contract at Saudi Aramco Jazan complex (Mar 2025) |

| Linde plc | Ireland/USA | Leader | Linde HYDROCHEM SMR Systems | Europe / Asia Pacific | Commissioned 120 MMSCFD refinery hydrogen unit at Hengli Petrochemical, China (Jan 2025) |

| Air Liquide | France | Leader | AL SMR Hydrogen Plant — HYOS Platform | Europe / MEA | Signed long-term hydrogen supply agreement with TotalEnergies La Mede refinery (May 2025) |

| Technip Energies | France | Challenger | HTER-SMR Reforming Technology | Europe / Middle East | Won EPC for 80 MMSCFD hydrogen plant at Kuwait National Petroleum Company KNPC (Feb 2026) |

| Haldor Topsoe (Topsoe A/S) | Denmark | Challenger | SynCOR Autothermal Reformer (ATR) | Europe / Asia Pacific | Licensed SynCOR ATR to three Asian refinery hydrogen projects (Sep 2025) |

| Johnson Matthey | UK | Niche Player | KATALCO SMR Catalyst Systems | Europe / North America | Launched KATALCO 57 high-activity reforming catalyst for ultra-low S feedgas (Apr 2025) |

| Thyssenkrupp Uhde | Germany | Challenger | Uhde SMR / POX Hydrogen Plants | Europe / MEA | Secured EPC for 60 MMSCFD hydrogen plant at Eni Livorno refinery, Italy (Nov 2025) |

| KBR Inc. | USA | Niche Player | KRES Steam Reforming Technology | North America / MEA | Licensed KRES technology to two Middle East refinery hydrogen expansions (Aug 2025) |

| McDermott International | USA | Niche Player | Lummus SMR Reformer Technology | North America / Asia Pacific | Finalized EPC for 50 MMSCFD unit at Pertamina Balikpapan refinery, Indonesia (Mar 2026) |

By Technology

| Technology | Market Share (2025) | Revenue (2025) |

| Steam Methane Reforming (SMR) | 72.4% | USD 5.53 Billion |

| Autothermal Reforming (ATR) | 12.6% | USD 0.96 Billion |

| Partial Oxidation (POX) / Gasification | 9.8% | USD 0.75 Billion |

| Electrolysis (Green Hydrogen) | 5.2% | USD 0.40 Billion |

Steam methane reforming dominates the Refinery Hydrogen Plant market with 72.4% technology share at USD 5.53 Billion in 2025. The SMR process converts natural gas or naphtha feedstock with steam over a nickel-based catalyst in an externally fired tubular reformer furnace, producing a synthesis gas (syngas) mixture of hydrogen, carbon monoxide, and carbon dioxide. The syngas passes through a high-temperature shift converter where water-gas shift reactions increase hydrogen yield, followed by a PSA unit that delivers 99.9% purity hydrogen for refinery consumption. A large-scale SMR unit of 150 MMSCFD capacity requires a reformer furnace with 300-500 catalyst-filled tubes operating at 850-950 degrees Celsius and 20-30 bar pressure, representing a mechanically and metallurgically demanding piece of capital equipment. The SMR technology licensor landscape is concentrated: Air Products' HyCO process, Linde's HYDROCHEM system, Air Liquide's HYOS platform, and Technip Energies' licensed SMR design collectively cover the majority of new SMR refinery hydrogen plant installations globally. The thermal efficiency of modern SMR units — achieving 78-83% efficiency on a lower heating value basis through advanced heat integration — is a key competitive differentiator between technology providers.

Autothermal reforming captures 12.6% of the market at USD 0.96 Billion in 2025 and is the fastest-growing technology segment at 11.4% CAGR through 2034. ATR combines partial oxidation and steam reforming in a single adiabatic reactor, eliminating the externally fired furnace and producing a syngas stream with a CO2 concentration of 20-25% — significantly higher than the 6-8% CO2 concentration in SMR flue gas. This concentrated CO2 product makes ATR ideal for pre-combustion carbon capture, as the CO2 can be separated at high pressure using Selexol or Rectisol physical absorption rather than the energy-intensive amine-based capture required for dilute SMR flue gases. Topsoe's SynCOR autothermal reformer — which scales to 300-600 MMSCFD in a single train — is commercially proven in ammonia and methanol production and is being actively licensed for large-scale blue hydrogen refinery applications where CCS is mandated by regulatory or corporate net-zero commitments.

Partial oxidation and gasification processes account for 9.8% of market revenue at USD 0.75 Billion in 2025. POX is particularly relevant for refineries with excess fuel oil, vacuum residue, or petroleum coke — heavy hydrocarbons that cannot be processed in SMR units — enabling hydrogen production from low-value residue streams that would otherwise require external disposal or blending. Electrolysis — the splitting of water using electrical energy — holds 5.2% share at USD 0.40 Billion in 2025. At commercial refinery scale, electrolysis remains more expensive than SMR on a levelized hydrogen cost basis except where renewable electricity prices fall below USD 20-25 per MWh. The IRA Section 45V tax credit and EU Hydrogen Bank auctions are accelerating electrolyzer deployment at refineries with access to low-cost renewable power, but SMR retains structural cost advantages at the majority of global refinery sites through the forecast period.

By Capacity

| Capacity Range | Market Share (2025) | Revenue (2025) |

| Large-Scale (>50 MMSCFD) | 52.8% | USD 4.03 Billion |

| Medium-Scale (10–50 MMSCFD) | 30.6% | USD 2.34 Billion |

| Small-Scale (<10 MMSCFD) | 16.6% | USD 1.27 Billion |

Large-scale refinery hydrogen plants — defined as those producing more than 50 MMSCFD (approximately 100,000 Nm3/h) of hydrogen — account for 52.8% of Global Refinery Hydrogen Plant Market revenue at USD 4.03 Billion in 2025. These units serve integrated refinery complexes processing 200,000 bpd or more of crude oil, where hydrogen demand for hydrodesulfurization, hydrocracking, and catalytic reforming can reach 80-200 MMSCFD in aggregate. The capital efficiency of large-scale SMR units — where the cost per unit of hydrogen capacity decreases substantially above 50 MMSCFD due to fixed engineering, heat recovery, and PSA system costs — drives operators toward fewer, larger units rather than distributed smaller installations. Major EPC contracts in this segment typically range from USD 200 Million to USD 1.1 Billion for the most complex large-scale installations.

Medium-scale plants between 10-50 MMSCFD capture 30.6% of revenue at USD 2.34 Billion in 2025. These units serve mid-size refineries processing 50,000-150,000 bpd of crude and are the most common installation type across Asia Pacific's numerous mid-scale refinery expansions. Small-scale units below 10 MMSCFD represent 16.6% at USD 1.27 Billion, serving smaller regional refineries, specialty chemical plants requiring high-purity hydrogen, and early-stage refinery hydrogen expansion projects in emerging markets where CAPEX constraints limit initial unit sizing.

By Application

| Application | Market Share (2025) | Revenue (2025) |

| Hydrodesulfurization (HDS) | 44.2% | USD 3.38 Billion |

| Hydrocracking | 31.8% | USD 2.43 Billion |

| Catalytic Reforming | 14.6% | USD 1.12 Billion |

| Other Refinery Applications | 9.4% | USD 0.72 Billion |

Hydrodesulfurization is the largest hydrogen-consuming application in the Refinery Hydrogen Plant market, accounting for 44.2% of market revenue at USD 3.38 Billion in 2025. HDS units remove sulfur from naphtha, kerosene, diesel, and fuel oil streams by reacting sulfur-containing organic compounds with hydrogen over a cobalt-molybdenum or nickel-molybdenum catalyst to form hydrogen sulfide, which is subsequently removed in an amine absorber and converted to elemental sulfur in a Claus plant. IMO 2020 marine fuel sulfur limits, Euro VI road diesel specifications (less than 10 ppm sulfur), and equivalent standards across Asia are the primary regulatory drivers for HDS hydrogen demand. Each percentage point increase in refinery crude slate heaviness — as lighter sweet crudes are replaced by heavier, higher-sulfur alternatives — increases HDS hydrogen consumption by approximately 1.5-2.0 kg of H2 per barrel of crude processed.

Hydrocracking accounts for 31.8% of market revenue at USD 2.43 Billion in 2025. Hydrocracker units convert vacuum gas oil and atmospheric residue into lighter, higher-value products including diesel, jet fuel, and naphtha, consuming 800-1,400 standard cubic feet of hydrogen per barrel of feedstock processed. New hydrocracker capacity additions — particularly in Asia and the Middle East, where refiners are investing to shift product slates from fuel oil toward higher-value middle distillates — drive proportional hydrogen plant capacity additions. Catalytic reforming hydrogen — largely a by-product of the reforming reaction rather than a primary consumption point — contributes 14.6% of market revenue through the naphtha reforming unit design and net hydrogen recovery balance engineering included in refinery hydrogen plant projects.

Regional Analysis

| Region | Share (2025) | Revenue (2025) | CAGR (2025–2034) |

| Asia Pacific | 35.4% | USD 2.70 Billion | 8.8% |

| North America | 26.2% | USD 2.00 Billion | 6.8% |

| Middle East & Africa | 20.6% | USD 1.57 Billion | 8.2% |

| Europe | 13.8% | USD 1.05 Billion | 6.2% |

| Latin America | 4.0% | USD 0.31 Billion | 7.4% |

Asia Pacific

Asia Pacific leads the Refinery Hydrogen Plant market with 35.4% share and USD 2.70 Billion in revenue in 2025, growing at an 8.8% CAGR through 2034 — the highest regional rate. China is the single largest country market, with SINOPEC and CNPC operating over 30 major refineries with aggregate capacity exceeding 16 million barrels per day. China's 14th Five-Year Plan targets completion of several integrated refinery petrochemical complexes — including expansions at Hengli Petrochemical, Rongsheng Petrochemical, and Shandong Yulong — each requiring large-scale SMR hydrogen plants. Linde's January 2025 commissioning of a 120 MMSCFD unit at Hengli's Dalian complex exemplifies the scale of Chinese refinery hydrogen investment. India is the second-largest Asia Pacific market: the BS VI transition — which reduced permitted diesel sulfur from 50 ppm to 10 ppm in 2020 and continues to drive HDS capacity additions at Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum refineries — sustains strong hydrogen plant procurement. Indonesia's Pertamina New Refinery Development at Balikpapan and Vietnam's expanding refining sector are growing secondary demand centers, collectively supported by ASEAN energy access mandates driving new refinery construction.

North America

North America accounts for 26.2% of the Refinery Hydrogen Plant market at USD 2.00 Billion in 2025, growing at a 6.8% CAGR through 2034. The United States is the region's dominant market, with its 130+ operating refineries processing a combined 18 million barrels per day. The U.S. IRA Section 45V hydrogen production tax credit — providing up to USD 3.00 per kilogram for hydrogen produced with lifecycle greenhouse gas emissions below 0.45 kg CO2-equivalent per kilogram — is the most significant near-term policy driver for hydrogen plant investment, creating economic incentives for SMR-with-CCS blue hydrogen installations at major refinery sites in the Gulf Coast and Midwest. EPA Tier 3 gasoline sulfur standards and California's LCFS are additional regulatory drivers sustaining HDS hydrogen demand across the U.S. refinery complex. Canada's Irving Oil, Suncor, and Imperial Oil operate refineries with active hydrogen plant investment programs, with Suncor's Pathways Alliance targeting CCS integration at its Fort McMurray oil sands upgrader hydrogen plants. Mexico's Pemex, constrained by capital availability, is selectively upgrading hydrogen plants at the Tula and Salina Cruz refineries under its 2024-2030 refinery modernization plan.

Middle East & Africa

The Middle East and Africa account for 20.6% of Refinery Hydrogen Plant revenue at USD 1.57 Billion in 2025, growing at an 8.2% CAGR through 2034. Saudi Arabia is the region's dominant market, with Saudi Aramco's Jazan Integrated Gasification and Power Company complex — one of the world's largest integrated downstream facilities — representing a USD 1.1 Billion single hydrogen plant EPC award in 2025. Saudi Aramco's Vision 2030 refinery expansion program targets processing of 8-10 million bpd of crude through domestic and international refining assets, requiring substantial hydrogen plant capacity across HDS and hydrocracking operations. The UAE's ADNOC is investing in hydrogen production at its Ruwais refinery complex under its CarbonCure carbon capture program, which targets 10 million tonnes per year of CO2 storage by 2030 and designates refinery SMR plants as primary CO2 capture sources. Kuwait's Kuwait National Petroleum Company is expanding its Al-Zour and Mina Al-Ahmadi refineries, with Technip Energies winning an 80 MMSCFD hydrogen plant EPC in early 2026. In Africa, Egypt's MIDOR and EGYPT LNG refineries, South Africa's Sasol Secunda, and Nigeria's Dangote Refinery are active refinery hydrogen plant procurement centers.

Europe

Europe holds 13.8% of the Refinery Hydrogen Plant market at USD 1.05 Billion in 2025, growing at a 6.2% CAGR — the lowest regional rate, reflecting structural headwinds from refinery rationalization under EU energy transition policy. The EU Emissions Trading Scheme, with carbon prices reaching USD 70-80 per tonne in 2025, creates a structural incentive to install carbon capture on existing SMR hydrogen plants, as the avoided carbon cost for a 100 MMSCFD SMR unit (which emits approximately 0.9 million tonnes of CO2 per year) represents USD 63-72 Million of annual ETS cost at current allowance prices. Germany's major refiners — including Shell Rheinland and TotalEnergies Leuna — are evaluating SMR retrofit with post-combustion carbon capture under the German H2Global program. The Netherlands, home to Europe's largest refining complex at Rotterdam (Shell, BP, Q8, and ExxonMobil), is integrating hydrogen plant upgrades with port-scale CO2 transport and storage infrastructure under the Porthos CCS project. Thyssenkrupp Uhde's November 2025 EPC win at Eni's Livorno refinery in Italy, incorporating CCS-ready design provisions, illustrates the direction of European refinery hydrogen plant investment.

Latin America

Latin America holds 4.0% of Refinery Hydrogen Plant revenue at USD 0.31 Billion in 2025, growing at a 7.4% CAGR through 2034. Brazil is the region's dominant market, with Petrobras operating 13 refineries with aggregate capacity of 2.1 million bpd. The Petrobras Strategic Plan 2024-2028 targets USD 7 Billion in downstream investment, including hydrogen plant upgrades and capacity expansions at the Replan, Repar, and REVAP refinery complexes to support pre-salt crude processing. Colombia's Ecopetrol is expanding hydrogen production at its Barrancabermeja refinery — the largest in Colombia — under a modernization program targeting 220,000 bpd processing capacity. Argentina's YPF and Chile's ENAP are secondary demand centers, with their refinery hydrogen requirements driven by domestic fuel quality regulations aligned with Euro V equivalent sulfur standards.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Technology

- Steam Methane Reforming (SMR)

- Autothermal Reforming (ATR)

- Partial Oxidation (POX) / Gasification

- Electrolysis (Green / Blue Hydrogen)

By Capacity

- Large-Scale (Above 50 MMSCFD)

- Medium-Scale (10–50 MMSCFD)

- Small-Scale (Below 10 MMSCFD)

By Application

- Hydrodesulfurization (HDS)

- Hydrocracking

- Catalytic Reforming

- Other Refinery Applications

By Component

- Reformer Furnace and Reactor

- Shift Converter

- Pressure Swing Adsorption (PSA) Unit

- Heat Recovery and Steam Generation

- Carbon Capture and Storage Integration

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.64 B |

| Forecast Revenue (2034) | USD 14.82 B |

| CAGR (2025-2034) | 7.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Steam Methane Reforming (SMR), Autothermal Reforming (ATR), Partial Oxidation (POX) / Gasification, Electrolysis (Green / Blue Hydrogen)), By Capacity, (Large-Scale (Above 50 MMSCFD), Medium-Scale (10–50 MMSCFD), Small-Scale (Below 10 MMSCFD)), By Application, (Hydrodesulfurization (HDS), Hydrocracking, Catalytic Reforming, Other Refinery Applications), By Component, (Reformer Furnace and Reactor, Shift Converter, Pressure Swing Adsorption (PSA) Unit, Heat Recovery and Steam Generation, Carbon Capture and Storage Integration) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | AIR PRODUCTS AND CHEMICALS, LINDE PLC, AIR LIQUIDE, TECHNIP ENERGIES, HALDOR TOPSOE (TOPSOE A/S), THYSSENKRUPP UHDE, JOHNSON MATTHEY, KBR INC., MCDERMOTT INTERNATIONAL (LUMMUS TECHNOLOGY), HONEYWELL UOP, FOSTER WHEELER (WOOD GROUP), HOWE-BAKER INTERNATIONAL, CALORIC ANLAGENBAU GmbH, PETROCHEMICAL INDUSTRIES COMPANY (PIC, KUWAIT), TOYO ENGINEERING CORPORATION, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Autothermal Reforming (ATR), Partial Oxidation (POX) & Gasification, Electrolysis – Green & Blue Hydrogen), By Capacity (Large-Scale Above 50 MMSCFD, Medium-Scale 10–50 MMSCFD, Small-Scale Below 10 MMSCFD), By Application (Hydrodesulfurization, Hydrocracking, Catalytic Reforming, Others), By Component Industry Trends & Forecast 2026–2034")

, Autothermal Reforming (ATR), Partial Oxidation (POX) & Gasification, Electrolysis – Green & Blue Hydrogen), By Capacity (Large-Scale Above 50 MMSCFD, Medium-Scale 10–50 MMSCFD, Small-Scale Below 10 MMSCFD), By Application (Hydrodesulfurization, Hydrocracking, Catalytic Reforming, Others), By Component Industry Trends & Forecast 2026–2034")

, Autothermal Reforming (ATR), Partial Oxidation (POX) & Gasification, Electrolysis – Green & Blue Hydrogen), By Capacity (Large-Scale Above 50 MMSCFD, Medium-Scale 10–50 MMSCFD, Small-Scale Below 10 MMSCFD), By Application (Hydrodesulfurization, Hydrocracking, Catalytic Reforming, Others), By Component Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Refinery Hydrogen Plant Market?

Global Refinery hydrogen plant market valued at USD 7.10B in 2024, reaching USD 14.82B by 2034, growing at a CAGR of 7.6% from 2026–2034.

Who are the major players in the Refinery Hydrogen Plant Market?

AIR PRODUCTS AND CHEMICALS, LINDE PLC, AIR LIQUIDE, TECHNIP ENERGIES, HALDOR TOPSOE (TOPSOE A/S), THYSSENKRUPP UHDE, JOHNSON MATTHEY, KBR INC., MCDERMOTT INTERNATIONAL (LUMMUS TECHNOLOGY), HONEYWELL UOP, FOSTER WHEELER (WOOD GROUP), HOWE-BAKER INTERNATIONAL, CALORIC ANLAGENBAU GmbH, PETROCHEMICAL INDUSTRIES COMPANY (PIC, KUWAIT), TOYO ENGINEERING CORPORATION, Others

Which segments covered the Refinery Hydrogen Plant Market?

By Technology, (Steam Methane Reforming (SMR), Autothermal Reforming (ATR), Partial Oxidation (POX) / Gasification, Electrolysis (Green / Blue Hydrogen)), By Capacity, (Large-Scale (Above 50 MMSCFD), Medium-Scale (10–50 MMSCFD), Small-Scale (Below 10 MMSCFD)), By Application, (Hydrodesulfurization (HDS), Hydrocracking, Catalytic Reforming, Other Refinery Applications), By Component, (Reformer Furnace and Reactor, Shift Converter, Pressure Swing Adsorption (PSA) Unit, Heat Recovery and Steam Generation, Carbon Capture and Storage Integration)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Refinery Hydrogen Plant Market

Published Date : 31 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date