- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Refurbished Data Centers Market Size & Forecast 2024–2034 | 13.1% CAGR

Global Refurbished Data Centers Market Size, Share & Industry Analysis By Component (Hardware, DCIM Software, Services), By Hardware Type (Power Systems, Cooling Systems, Servers, Networking Devices, Racks), By Deployment Model (On-Premises, Cloud), By Data Center Type (Colocation, Hyperscale, Edge, Modular), By Tier Level (Tier I–IV), By Industry (BFSI, IT & Telecom, Healthcare, Government), Competitive Landscape, Market Trends & Forecast 2025–2034

Report Overview

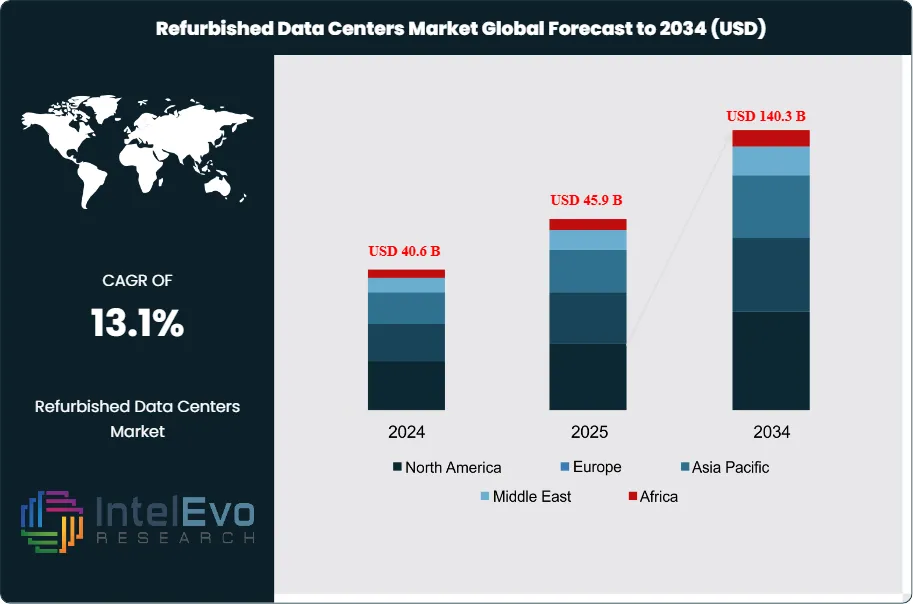

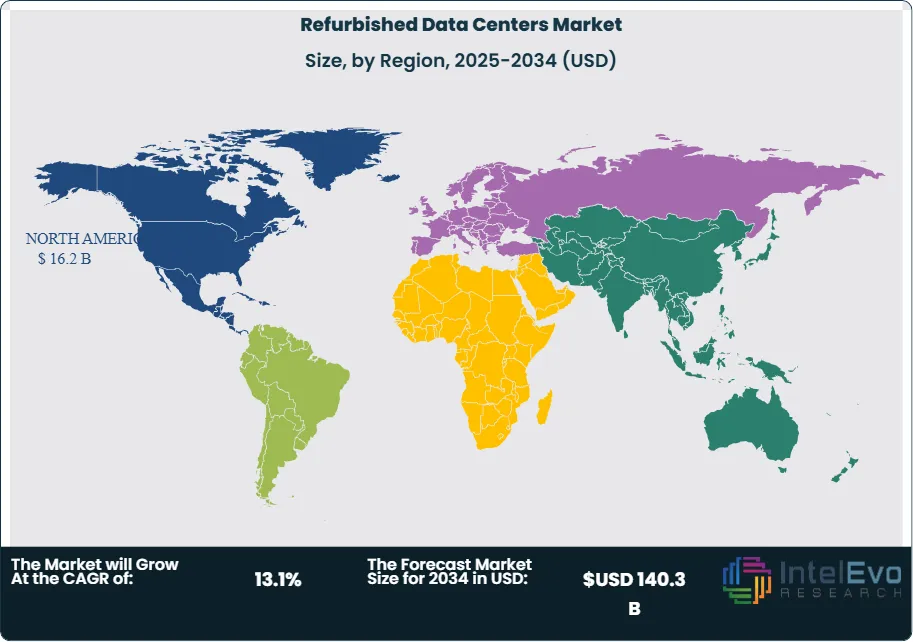

The Refurbished Data Centers Market was valued at USD 40.6 Billion in 2024 and is projected to reach approximately USD 140.3 Billion by 2034. The market is estimated to grow to around USD 45.9 Billion in 2025. Based on projected expansion from 2026 onward, the industry is expected to register a compound annual growth rate (CAGR) of approximately 13.1% during 2026–2034.

Get More Information about this report -

Request Free Sample ReportRefurbished data centers extend asset life through targeted modernization, capacity refresh, and reuse of restored equipment that performs to near-new specifications. This model lowers total project cost and shortens deployment cycles versus greenfield builds. Buyers also value waste reduction and lower embodied carbon, since reuse limits demand for newly manufactured components and reduces end-of-life disposal volumes.

Demand rises as enterprises face higher prices for new servers, networking, and power infrastructure, while also tightening capital discipline. Refurbished servers and related systems can cost up to 80% less than new equivalents, enabling faster capacity additions for storage, enterprise applications, and disaster recovery. Medium to large enterprises drive adoption, with healthcare, financial services, and technology among the most active users due to rising data volumes, compliance needs, and uptime requirements. Supply growth follows the steady release of decommissioned assets from hyperscale operators and large colocation providers, which supports a deeper secondary market and more consistent quality tiers.

Technology shifts also shape procurement. AI, automation, and digitalization increase rack density and monitoring requirements, and refurbishment providers respond with upgrades to power distribution, cooling, and DCIM tooling. Predictive maintenance based on telemetry and AI-assisted operations improves reliability and reduces unplanned downtime. At the same time, AI-centric workloads can expose limits in older architectures, pushing demand toward certified refurbishment with stress testing, firmware governance, and performance validation.

North America led in 2024 with more than 40.0% share and USD 16.2 billion in revenue, supported by the US market at USD 12.99 billion. Secondary US hubs with strong fiber access and power availability attract incremental retrofit capital. Europe benefits from stricter ESG reporting, right-to-repair momentum, and e-waste controls that favor circular procurement. Asia-Pacific shows accelerating interest, with India and Southeast Asia emerging as investment hotspots as enterprises seek faster capacity without long permitting cycles.

Competitive dynamics track adjacent markets. The AI Data Center Market reached USD 14.3 billion in 2024 and targets USD 157.3 billion by 2034, while global colocation expands from USD 57.2 billion in 2023 to USD 227.4 billion by 2033, reinforcing demand for scalable infrastructure. Key risks include supply variability, warranty quality, cybersecurity exposure from legacy components, and evolving energy-efficiency rules that raise retrofit scope and compliance costs.

, By Hardware Type (Power Systems, Cooling Systems, Servers, Networking Devices, Racks), By Deployment Model (On-Premises, Cloud), By Data Center Type (Colocation, Hyperscale, Edge, Modular), By Tier Level (Tier I–IV), By Industry (BFSI, IT & Telecom, Healthcare, Government), Competitive Landscape, Market Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The U.S. refurbished data center market grows at 11.5% CAGR, 2024-2034. North America delivers 16.2 billion USD revenue, 2024.

- Segment Dominance : Hardware leads with 45.6% share, 2024, driven by refurbished servers, storage, and networking demand. Large-scale sites dominate with 52.8% share, 2024.

- Segment Dominance: Colocation secures 35.7% share, 2024, as firms prioritize lower build costs. Tier 3 facilities hold 43.6% share, 2024, balancing resilience and price.

- Driver: Buyers adopt refurbishment to cut infrastructure outlay, estimated: 30.0% capex savings, 2024. Sustainability mandates also influence procurement, estimated: 25.0% increase in circular-IT adoption, 2024.

- Restraint: Operators face quality and warranty variability, estimated: 2.0% higher failure risk vs. new equipment, 2024. Cybersecurity exposure from legacy components adds risk, estimated: 12.0% higher patch-lag incidence, 2024.

- Opportunity: Providers can expand certified refurbishment and lifecycle services, estimated: 18.0% services revenue uplift potential, 2024-2034. AI-ready retrofits for power and cooling create incremental demand, estimated: 3.0 billion USD incremental TAM, 2034.

- Trend: Enterprises accelerate consolidation into Tier 3 footprints and colocation-based refresh cycles, estimated: 15.0% annual retrofit activity growth, 2024-2034. Automation in monitoring and maintenance rises, estimated: 40.0% DCIM adoption rate, 2024.

- Regional Analysis: North America leads with 40.0% share, 2024, and 16.2 billion USD revenue, 2024. The U.S. contributes 12.99 billion USD, 2024, anchoring regional scale and procurement velocity.

By Type

Hardware continues to represent the core of spending in the refurbished data center market as the industry moves through 2025 and beyond. In 2024, hardware accounted for 45.6% of total revenue, driven by sustained demand for refurbished servers, storage systems, networking devices, power units, and racks. You see this preference because refreshed hardware delivers comparable throughput and reliability at a fraction of the cost of new equipment, often lowering acquisition expenses by 50% to 80%.

As AI inference, edge workloads, and data-intensive enterprise applications expand, you increasingly require hardware with higher core density, faster interconnects, and improved power efficiency. Refurbished systems that incorporate updated processors, solid-state storage, and energy-efficient networking meet these needs while aligning with sustainability targets. This balance positions hardware as the primary value contributor within refurbished deployments through the next decade.

By Application

Infrastructure hosting and enterprise workload support remain the primary applications for refurbished data centers. In 2024, colocation-related usage dominated, accounting for 35.7% of deployments, as you seek reliable capacity without committing to new builds. Refurbished facilities supply ready-to-use power, cooling, and security while shortening deployment timelines.

Hybrid environments also expand rapidly. You increasingly pair refurbished on-premise or colocation assets with public cloud platforms to control latency and cost. This approach supports disaster recovery, AI model training support, and regional data residency needs, especially as digital services scale across sectors.

By End-Use

Large enterprises continue to lead adoption, representing 52.8% of refurbished data center demand in 2024. You favor large-scale sites because they deliver stronger connectivity options, access to multiple carriers, and higher power availability. These attributes support data-heavy workloads across analytics, cloud services, and content delivery.

Mid-sized enterprises follow closely as budget pressure intensifies. Refurbished environments allow you to expand processing capacity without absorbing the financial risk of new infrastructure, while still meeting uptime and compliance expectations.

By Region

North America remains the largest regional market, holding over 40.0% share and generating USD 16.2 billion in revenue in 2024. You benefit from a mature digital ecosystem, strong hyperscale presence, and strict energy and e-waste regulations that favor reuse. The United States alone contributed USD 12.99 billion and continues to anchor regional demand.

Europe advances steadily as sustainability regulation tightens, while Asia Pacific emerges as the fastest-growing region beyond 2025. You see rising adoption in India, Southeast Asia, and parts of the Middle East as enterprises pursue rapid capacity expansion without long construction cycles. These regions increasingly view refurbished data centers as a practical route to support cloud growth, AI workloads, and national digital programs.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Hardware

- Power Systems

- Cooling Systems

- Servers

- Networking Devices

- Others (Racks)

- DCIM (Data Center Infrastructure Management) Software

- On-premises

- Cloud

- Services

By Data Center Type

- Colocation

- Hyperscale

- Edge

- Others (Managed, Modular)

By Tier Level

- Tier 1 and Tier 2

- Tier 3

- Tier 4

By Data Center Size

- Small

- Medium

- Large

By Industry

- BFSI

- IT & Telecom

- Healthcare

- Government

- Manufacturing

- Retail & E-commerce

- Others (Media & Entertainment)

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 45.9 B |

| Forecast Revenue (2034) | USD 140.3 B |

| CAGR (2025-2034) | 13.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Hardware, DCIM (Data Center Infrastructure Management) Software, Services), By Data Center Type (Colocation, Hyperscale, Edge, Others (Managed, Modular)), By Tier Level (Tier 1 and Tier 2, Tier 3, Tier 4), By Data Center Size (Small, Medium, Large), By Industry (BFSI, IT & Telecom, Healthcare, Government, Manufacturing, Retail & E-commerce, Others (Media & Entertainment)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Huawei Technologies Co., Ltd., Dell Technologies Inc., Apto Solutions Inc., Inspur Group, Cisco Systems, Inc., Fujitsu, Lenovo, Super Micro Computer, Inc., Hewlett Packard Enterprise Development LP, International Business Machines Corporation, Others, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Hardware Type (Power Systems, Cooling Systems, Servers, Networking Devices, Racks), By Deployment Model (On-Premises, Cloud), By Data Center Type (Colocation, Hyperscale, Edge, Modular), By Tier Level (Tier I–IV), By Industry (BFSI, IT & Telecom, Healthcare, Government), Competitive Landscape, Market Trends & Forecast 2025–2034")

, By Hardware Type (Power Systems, Cooling Systems, Servers, Networking Devices, Racks), By Deployment Model (On-Premises, Cloud), By Data Center Type (Colocation, Hyperscale, Edge, Modular), By Tier Level (Tier I–IV), By Industry (BFSI, IT & Telecom, Healthcare, Government), Competitive Landscape, Market Trends & Forecast 2025–2034")

, By Hardware Type (Power Systems, Cooling Systems, Servers, Networking Devices, Racks), By Deployment Model (On-Premises, Cloud), By Data Center Type (Colocation, Hyperscale, Edge, Modular), By Tier Level (Tier I–IV), By Industry (BFSI, IT & Telecom, Healthcare, Government), Competitive Landscape, Market Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Refurbished Data Centers Market?

The Global Refurbished Data Centers Market was valued at USD 40.6 Billion in 2024 and is projected to reach USD 140.3 Billion by 2034, expanding at a CAGR of 13.1% from 2026–2034. Explore market trends, cost-efficient data center upgrades, sustainability drivers, and future growth opportunities in refurbished infrastructure.

Who are the major players in the Refurbished Data Centers Market?

Huawei Technologies Co., Ltd., Dell Technologies Inc., Apto Solutions Inc., Inspur Group, Cisco Systems, Inc., Fujitsu, Lenovo, Super Micro Computer, Inc., Hewlett Packard Enterprise Development LP, International Business Machines Corporation, Others,

Which segments covered the Refurbished Data Centers Market?

By Component (Hardware, DCIM (Data Center Infrastructure Management) Software, Services), By Data Center Type (Colocation, Hyperscale, Edge, Others (Managed, Modular)), By Tier Level (Tier 1 and Tier 2, Tier 3, Tier 4), By Data Center Size (Small, Medium, Large), By Industry (BFSI, IT & Telecom, Healthcare, Government, Manufacturing, Retail & E-commerce, Others (Media & Entertainment))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Refurbished Data Centers Market

Published Date : 02 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date