- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global RegTech Solutions Market Size, Share & Forecast | CAGR 20.4%

Global RegTech Solutions Market Size, Share & Industry Analysis By Component (Solutions and Services), By Deployment Mode (Cloud-Based, On-Premises and Hybrid), By Enterprise Size (Large Enterprises and SMEs), By Application (AML & Financial Crime Management, KYC and Customer Onboarding, Regulatory Reporting, Risk Management, Fraud Detection and Identity Management), By End-User (BFSI, FinTech, Government, Healthcare, IT & Telecommunications, Retail and Manufacturing) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 19.8 Billion | USD 105.3 Billion | 20.4% | North America, 35.0% |

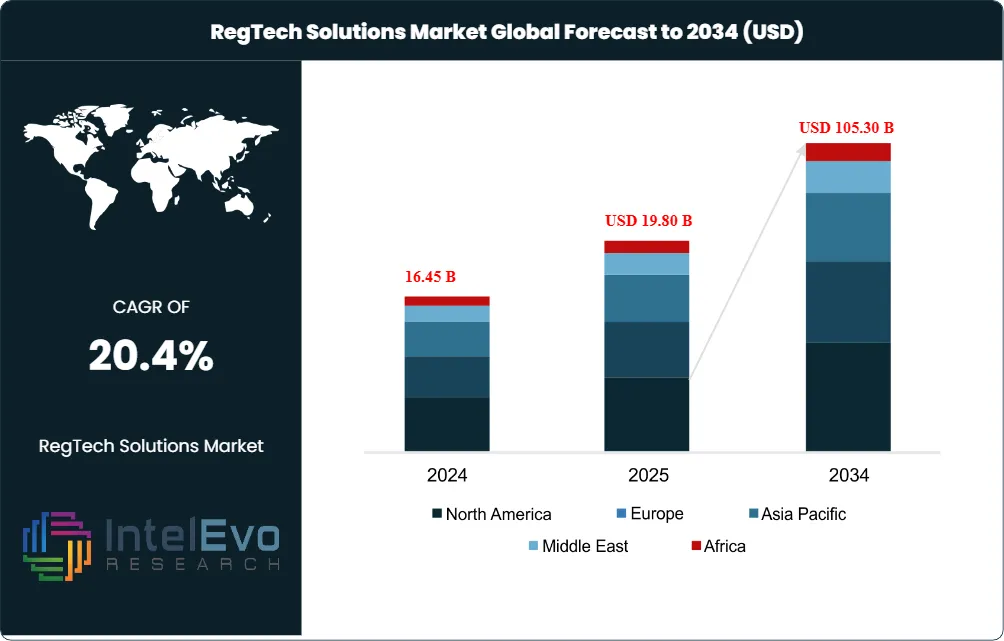

The RegTech Solutions Market was valued at USD 16.45 Billion in 2024 and USD 19.80 Billion in 2025. The market is projected to reach USD 105.30 Billion by 2034, expanding at a CAGR of 20.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 85.5 Billion over the analysis period, more than five times the 2025 base. The RegTech Solutions Market is being driven by escalating regulatory complexity, with global financial institutions paying USD 19.3 Billion in compliance penalties during 2024 alone, forcing accelerated migration from manual reviews to AI-native compliance platforms.

Get More Information about this report -

Request Free Sample ReportThree structural drivers anchor RegTech Solutions Market expansion through 2034. First, the EU Digital Operational Resilience Act (DORA) entered application on 17 January 2025, mandating ICT risk management for 20 categories of financial entities, with non-compliance fines reaching 2% of annual worldwide turnover. Second, the European Supervisory Authorities designated 19 critical ICT third-party providers under DORA on 18 November 2025, expanding direct supervisory scope to cloud and software vendors. Third, the FinCEN interim final rule of 26 March 2025 narrowed Corporate Transparency Act reporting to foreign reporting companies, redirecting compliance budgets from BOI filings toward sanctions screening and AML transaction monitoring.

Cloud-based deployment now anchors approximately 64.0% of new RegTech Solutions Market deployments, reflecting buyer preference for elastic capacity and continuous regulatory rule updates. Generative AI adoption is reshaping the competitive set, with NICE Ltd. introducing three GenAI financial-crime solutions in February 2024 that cut suspicious activity report (SAR) drafting time substantially, and NICE Actimize launching the Actimize Insights Network in January 2026 to deliver real-time counterparty risk visibility for authorized push payment fraud. AI-powered platforms are crossing the chasm because legacy rules-based systems generate excessive false positives that consume compliance analyst time.

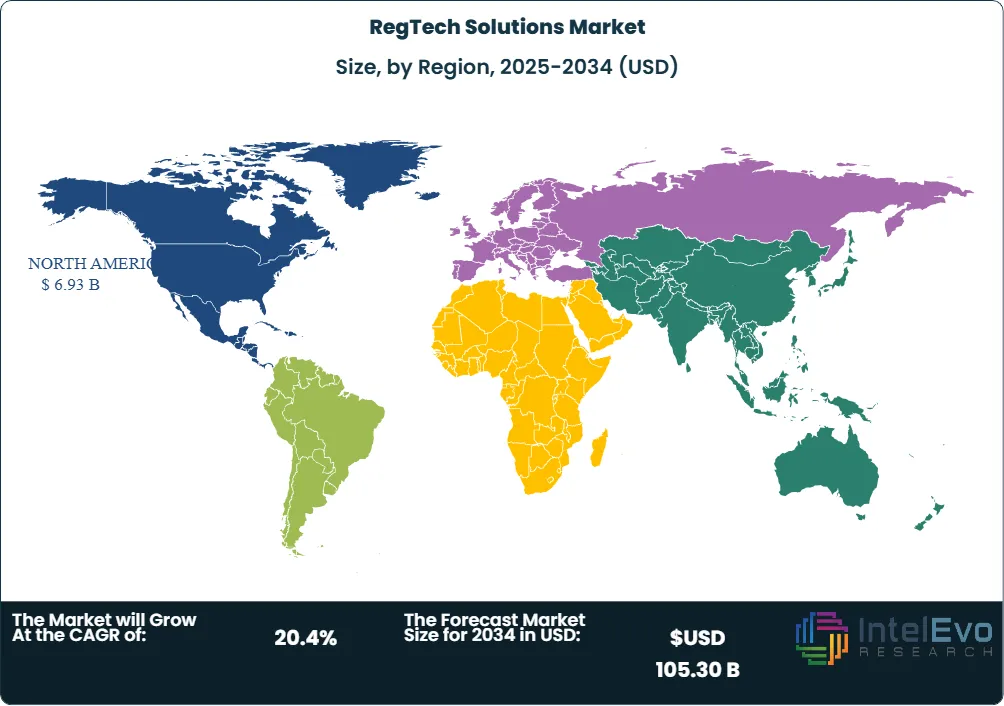

North America led the RegTech Solutions Market with 35.0% revenue share in 2025, driven by Dodd-Frank, Bank Secrecy Act, and OFAC sanctions enforcement combined with concentration of vendors including IBM Corporation, Thomson Reuters Corporation, and NICE Actimize. Asia Pacific is the fastest-growing region because India's Reserve Bank tightened digital lending norms and China's central bank expanded transaction monitoring requirements through 2025-2026. Europe sustains durable growth because DORA, the EU AI Act, and the Markets in Crypto-Assets Regulation (MiCA) compound vendor demand. The forward outlook through 2034 favors AI-native platforms that combine entity resolution, sanctions screening, and regulatory reporting in unified architecture.

Market Definition & Scope

The RegTech Solutions Market is defined as software platforms, cloud services, and managed offerings that automate regulatory compliance, anti-money laundering (AML) controls, transaction monitoring, sanctions screening, identity verification, and regulatory reporting for financial institutions, fintechs, insurers, and other regulated enterprises. The market encompasses solution components such as compliance management software and identity verification engines, alongside services covering implementation, advisory, and managed compliance operations.

This analysis includes risk and compliance management, AML and fraud management, identity management, regulatory reporting, and regulatory intelligence applications across BFSI, insurance, fintech, healthcare, and government end-users. The scope explicitly excludes general-purpose enterprise GRC software unrelated to financial regulation, traditional anti-virus cybersecurity tooling, and audit advisory services without a software component. The RegTech Solutions Market sits within the broader compliance and risk technology category, accounting for an estimated 18% of global compliance technology spend in 2025, with the remaining share split between cybersecurity, e-discovery, and audit platforms.

, By Deployment Mode (Cloud-Based, On-Premises and Hybrid), By Enterprise Size (Large Enterprises and SMEs), By Application (AML & Financial Crime Management, KYC and Customer Onboarding, Regulatory Reporting, Risk Management, Fraud Detection and Identity Management), By End-User (BFSI, FinTech, Government, Healthcare, IT & Telecommunications, Retail and Manufacturing) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The RegTech Solutions Market grows from USD 19.8 Billion in 2025 to USD 105.3 Billion by 2034 at a CAGR of 20.4%, generating USD 85.5 Billion in absolute new revenue.

- Segment Dominance: The Solutions component held 67.0% share of the RegTech Solutions Market in 2025, capturing roughly USD 13.3 Billion as buyers prioritize integrated software over standalone advisory services.

- Segment Dominance: Risk and Compliance Management led applications with 32.0% share in 2025, driven by Basel III/IV capital reporting and the 17 January 2025 DORA application date.

- Driver: DORA mandatory enforcement covers approximately 22,000 EU financial entities and now extends to 19 designated critical ICT third-party providers, lifting RegTech Solutions Market budgets by an estimated 12-15% across affected institutions.

- Restraint: Legacy core banking integration costs add 28% to typical implementation budgets, with 65% of large banks operating shadow IT systems that delay real-time data orchestration for AML platforms.

- Opportunity: Small and medium enterprise (SME) compliance-as-a-service represents a USD 9 Billion forecast opportunity by 2034 as cloud-first vendors like Vanta and ComplyAdvantage scale subscription models below USD 50,000 annual contract value.

- Trend: Agentic AI compliance is replacing rules-based monitoring; NICE Actimize processes more than 5 billion transactions daily across over 1,000 clients while protecting approximately USD 6 Trillion in assets each day.

- Regional: North America held 35.0% RegTech Solutions Market share in 2025, equivalent to USD 6.93 Billion, with the United States contributing USD 4.71 Billion or roughly 68% of the regional total.

Key Insights Summary

- Global RegTech investment funding reached approximately USD 3.0 Billion across the first quarter of 2026, with US RegTech alone capturing USD 2.0 Billion across 103 deals, a 28% year-over-year funding increase per FinTech Global research.

- DORA designated 19 critical ICT third-party providers on 18 November 2025, with 38% of major incidents reported by EU banks in 2025 traceable to IT change as the root cause, per ECB Banking Supervision.

- FinCEN issued an interim final rule on 26 March 2025 exempting domestic US reporting companies from Beneficial Ownership Information filing under the Corporate Transparency Act, redirecting RegTech budgets toward sanctions and AML use cases.

- The average financial-sector data breach cost reached USD 6.08 Million in 2025, while institutions face DORA fines of up to 2.0% of annual worldwide turnover, materially raising the ROI on RegTech procurement.

- Cloud deployment captured 64.0% of RegTech Solutions Market revenue in 2025, with cloud RegTech buyers reporting 6-12 month bank implementation timelines versus 12-18 months for on-premises deployments.

- Banks paid USD 19.3 Billion in compliance penalties globally in 2024, anchoring the business case for predictive transaction monitoring across the BFSI vertical that holds approximately 50% of RegTech Solutions Market end-user spend.

- The European Central Bank confirmed in March 2026 that DORA threat-led penetration testing (TLPT) is now mandatory at least every three years for systemically important banks, expanding the addressable spend on continuous compliance monitoring.

Competitive Landscape Overview

The RegTech Solutions Market is moderately consolidated, with the top four vendors IBM Corporation, Thomson Reuters Corporation, NICE Actimize (a subsidiary of NICE Ltd.), and Wolters Kluwer N.V. estimated to hold a combined 42-46% share of disclosed enterprise RegTech revenue in 2025. Competition is increasingly platform-based rather than price-based because buyers shortlist vendors on regulatory coverage, configurability of alerts, and the explainability of AI-driven decisions for regulator examinations. Specialist challengers Quantexa, ComplyAdvantage, Fenergo, and Chainalysis are gaining share in entity resolution, AML, client lifecycle management, and crypto compliance respectively.

Competitive evolution is moving toward agentic AI architectures that resolve routine alerts autonomously while escalating typology-novel cases to human analysts. Strategic acquisition activity has intensified: Entrust completed its acquisition of Onfido to integrate biometric identity verification into a broader compliance suite, and Regnology acquired Vizor Software in Q2 2025 to expand regulatory reporting coverage. Market entry continues at the SME tier where cloud-first vendors price below USD 50,000 annual contract value, fragmenting the competitive map.

The competitive matrix below summarizes the leading players in the RegTech Solutions Market, their headquarters, market position, primary product offering, geographic strength, and most recent strategic move verified through public disclosures during the trailing 18 months.

Competitive Landscape Matrix

| Company | HQ Country | Position | Key Product | Geographic Strength | Recent Strategic Move (Trailing 18 Months) |

|---|---|---|---|---|---|

| IBM Corporation | USA | Leader | Watson AI compliance, OpenPages GRC | Global, US-led | Expanded watsonx.governance for regulatory monitoring (2025) |

| Thomson Reuters Corp. | Canada | Leader | ONESOURCE, Regulatory Intelligence | North America, EU | Backed Bretton AI Series B via Thomson Reuters Ventures (Q1 2026) |

| NICE Actimize (NICE Ltd.) | USA / Israel | Leader | Actimize IFM, SURVEIL-X | Global, BFSI core | Launched Actimize Insights Network for counterparty risk (Jan 2026) |

| Wolters Kluwer N.V. | Netherlands | Leader | OneSumX regulatory reporting | Europe, US | Expanded OneSumX for DORA reporting (2025) |

| Broadridge Financial Solutions | USA | Challenger | Compliance and reporting suite | North America | Expanded post-trade compliance modules (2025) |

| MetricStream Inc. | USA | Challenger | Enterprise GRC platform | Global | Launched AI-driven risk insights module (2025) |

| Chainalysis Inc. | USA | Niche Player | KYT, Crypto Investigations | Global crypto | Closed USD 436M cumulative funding; expanded enterprise tier (2025) |

| ComplyAdvantage | UK | Niche Player | AI-driven AML and screening | EMEA, North America | Expanded transaction monitoring with AI agents (2025) |

| Fenergo | Ireland | Niche Player | Client Lifecycle Management | Global banking | Partnership with BNP Paribas for CLM automation (2025) |

| Quantexa | UK | Challenger | Decision Intelligence platform | EMEA, US, APAC | Reported revenue near USD 173M; deployed at HSBC and BNY Mellon (2025) |

Segmentation Analysis

The RegTech Solutions Market segments along five primary axes: by component, by deployment mode, by enterprise size, by application, and by end-user vertical. Segment shares below are aggregated from disclosed company filings, regulator submissions, and trade body data, then normalized to sum to 100% within each category.

By Component

Solutions captured 67.0% of the RegTech Solutions Market in 2025, equivalent to USD 13.27 Billion, while Services held 33.0% or USD 6.53 Billion. Solutions dominate because banks need integrated software platforms that combine sanctions screening, transaction monitoring, and regulatory reporting on a single data fabric, reducing the integration burden that point tools impose.

The Services segment is growing at a faster rate of approximately 22% as institutions outsource implementation and managed compliance operations to vendors like Deloitte and PwC. RegTech procurement checklists from buyers including HSBC and BNP Paribas now require 12-18 months of post-go-live managed services, lifting services attach rates above 0.45 of total contract value. Solutions buyers prioritize APIs that integrate with core banking systems from Temenos, Finastra, and FIS, while services buyers prioritize regulatory subject-matter expertise in DORA, MiCA, and Bank Secrecy Act compliance.

By Deployment Mode

Cloud-based deployments held 64.0% of RegTech Solutions Market revenue in 2025, totaling USD 12.67 Billion, while on-premises retained 36.0% or USD 7.13 Billion. Cloud is winning new deployments because rapid regulatory updates such as DORA Regulatory Technical Standards require continuous patching that cloud vendors deliver without customer intervention. Hyperscaler partnerships with AWS, Microsoft Azure, and Google Cloud also enable elastic transaction monitoring for institutions like Stripe and Adyen processing variable payment volumes.

On-premises retains share among Tier 1 banks where data residency under DORA Article 28 and the German BAIT framework requires local control. Notably, BAIT remains in force for non-DORA-scope institutions until 31 December 2026, sustaining on-premises deployment demand in Germany. Cloud deployments deploy in 6-12 months versus 12-18 months for on-premises in banks, a fact often cited in RegTech vendor RFPs and now built into procurement timelines.

By Enterprise Size

Large enterprises captured 68.0% of the RegTech Solutions Market in 2025 at USD 13.46 Billion, while small and medium enterprises (SMEs) held 32.0% at USD 6.34 Billion. Large enterprises dominate because Tier 1 banks including JPMorgan, HSBC, and BNP Paribas process billions of transactions daily and operate across multiple regulatory jurisdictions, demanding enterprise platforms from NICE Actimize and Wolters Kluwer.

The SME segment is the fastest-growing cohort and is forecast to expand at roughly 23% CAGR through 2034 because cloud-first vendors like Vanta, ComplyAdvantage, and Sumsub price entry tiers below USD 50,000 ACV. SMEs face the same AML/KYC obligations as large institutions but lack dedicated compliance teams, making subscription RegTech solutions decisively more cost-effective than building in-house. The implementation timeline for SME deployments runs 6-9 months versus 12-18 months for enterprise, accelerating revenue recognition for vendors.

By Application

Risk and Compliance Management led RegTech Solutions Market applications with 32.0% share in 2025, equivalent to USD 6.34 Billion, followed by AML and Fraud Management at 28.0% (USD 5.54 Billion), Identity Management at 18.0% (USD 3.56 Billion), Regulatory Reporting at 14.0% (USD 2.77 Billion), and Regulatory Intelligence at 8.0% (USD 1.58 Billion). Risk and compliance management dominates because it spans Basel III/IV, DORA, and Sarbanes-Oxley use cases inside a single platform.

AML and Fraud Management is the fastest-growing application at approximately 23% CAGR because of authorized push payment scams in the UK, FinCEN sanctions enforcement against Russian and North Korean networks, and the rise of crypto laundering investigated by Chainalysis and TRM Labs. Identity Management benefits from KYC/KYB onboarding mandates under PSD2 and India's RBI digital lending guidelines. Sumsub now supports more than 14,000 document types across 220 countries, while Fenergo serves over 150 global banks for identity orchestration. Regulatory Intelligence captures the smallest share but is foundational because it tracks new rules and maps them to internal policy.

By End-User Vertical

Banking and Financial Services held approximately 50.0% of RegTech Solutions Market end-user spend in 2025, totaling USD 9.90 Billion, followed by Insurance at 14.0% (USD 2.77 Billion), FinTech and Payments at 12.0% (USD 2.38 Billion), Healthcare at 9.0% (USD 1.78 Billion), Government at 8.0% (USD 1.58 Billion), and IT and Telecom plus other regulated sectors at 7.0% (USD 1.39 Billion). BFSI dominates because banks operate under Dodd-Frank, Basel III/IV, DORA, BSA/AML, and OFAC sanctions simultaneously.

FinTech and Payments is forecast to expand at a 17% CAGR, the fastest end-user trajectory, because providers including Stripe, Adyen, and Wise face the same KYC and AML obligations as banks while serving thousands of sub-merchants. Healthcare RegTech adoption is rising as HIPAA-equivalent rules globalize and patient data privacy enforcement intensifies, with AI-driven billing fraud detection becoming standard. The Insurance segment is benefiting from EIOPA digital operational resilience rules under DORA, which now apply to reinsurers and brokers as of January 2025.

Regional Analysis

The RegTech Solutions Market demonstrates sharp regional differentiation in 2025, anchored by North America at 35.0% share, Europe at 27.0%, Asia Pacific at 24.0%, Latin America at 7.0%, and Middle East and Africa at 7.0%. Regional shares sum to 100% of 2025 revenue.

North America

North America held 35.0% of the RegTech Solutions Market in 2025, generating USD 6.93 Billion. The United States accounted for approximately 68% of the regional total at USD 4.71 Billion, with Canada near USD 1.52 Billion and Mexico at USD 0.69 Billion. Demand is concentrated in Tier 1 banks, fintechs, and broker-dealers responding to FinCEN, OFAC, SEC, and FINRA enforcement priorities. The FinCEN interim final rule of 26 March 2025 exempting domestic US entities from Beneficial Ownership Information filing has redirected RegTech procurement budgets toward sanctions screening and AML transaction monitoring. Innovate Finance in Canada and the US Treasury Office of Foreign Assets Control sanctioned over 750 individuals and entities tied to Russia and Iran during 2025, lifting screening platform demand.

Europe

Europe held 27.0% RegTech Solutions Market share in 2025 at USD 5.35 Billion, led by the United Kingdom, Germany, and France. The 17 January 2025 DORA application date triggered a step-change in spending, and BaFin in Germany rescinded KAIT, VAIT, and ZAIT circulars on 16 January 2025, channeling all ICT compliance demand into DORA-aligned RegTech. The European Supervisory Authorities published the DORA oversight guide on 15 July 2025 and designated 19 critical ICT third-party providers on 18 November 2025, expanding direct supervisory perimeter. Innovate Finance launched the UK RegTech Strategy Group with the City of London Corporation and EY in April 2025 to coordinate vendor scaling, signaling concentrated UK industry support.

Asia Pacific

Asia Pacific held 24.0% RegTech Solutions Market share in 2025 at USD 4.75 Billion, with China, India, Japan, Singapore, and Australia driving most regional spend. India's Reserve Bank tightened digital lending and KYC norms across 2025, lifting Fenergo and Sumsub adoption among non-banking financial companies. ComplySci expanded into Japan in January 2026 with a localized RegTech platform incorporating AI-driven conflict-of-interest monitoring and ESG compliance tools aligned with FSA stablecoin regulations. Refinitiv (a London Stock Exchange Group company) rolled out enhanced OnDemand KYC Verification in Japan during October 2025 under Payment Services Act amendments. Asia Pacific is forecast to grow fastest among the five regions through 2034, supported by digital transformation in Indonesia, Thailand, and the Philippines.

Latin America

Latin America held 7.0% RegTech Solutions Market share in 2025 at USD 1.39 Billion. Brazil leads regional demand because Banco Central do Brasil enforces strict AML rules under Resolution 4,968/2021 and the Pix instant-payment platform drives transaction monitoring volumes. Mexico's Comisión Nacional Bancaria y de Valores requires fintechs to deploy KYC platforms under the 2018 Fintech Law, while Colombia's Superintendencia Financiera adopted updated cyber-resilience rules in 2025. RegTech adoption remains uneven across Argentina and Chile, where macroeconomic constraints limit IT spend, but cross-border remittance fraud is lifting demand for ComplyAdvantage and Trulioo identity verification.

Middle East and Africa

Middle East and Africa held 7.0% RegTech Solutions Market share in 2025 at USD 1.39 Billion. The United Arab Emirates Central Bank, Dubai Financial Services Authority, and Saudi Arabia's SAMA pushed AML and sanctions screening adoption among regional banks. Emirates NBD announced a strategic collaboration with GSS in May 2025 to deploy AI-powered sanctions screening across domestic and cross-border transactions, signaling appetite for AI-native compliance among GCC institutions. South Africa's Financial Sector Conduct Authority issued conduct standards for crypto-asset service providers in 2025, expanding the addressable RegTech market into digital asset exchanges. Nigeria, Kenya, and Egypt are emerging adopter markets driven by CBN, CBK, and CBE digital payment expansion.

Country Analysis

Country-level dynamics in the RegTech Solutions Market diverge sharply because each jurisdiction enforces distinct rule sets and houses a different vendor concentration.

United States

The United States RegTech Solutions Market reached USD 4.71 Billion in 2025 and is projected to expand at a country-specific CAGR of 20.5% through 2034. FinCEN, OFAC, SEC, FINRA, and the Federal Reserve enforce overlapping rule sets that drive concentrated platform spending, with banks like JPMorgan Chase and Citigroup deploying NICE Actimize and IBM platforms across global operations. The Federal Reserve and Office of the Comptroller of the Currency issued joint guidance on third-party risk management in 2025, and the New York Department of Financial Services Part 500 cybersecurity rules require continuous compliance monitoring at all licensed entities. RegTech vendor concentration is heaviest in New York, San Francisco, and Boston, with USD 2.0 Billion of Q1 2026 funding flowing primarily to AI-native platforms.

United Kingdom

The United Kingdom RegTech Solutions Market reached approximately USD 1.55 Billion in 2025 and is forecast at a 22.0% country CAGR through 2034. The Financial Conduct Authority and Prudential Regulation Authority published PS24/16 on Critical Third Parties in November 2024 (effective 1 January 2025), creating a UK-specific operational resilience perimeter complementary to DORA. London continues as the global RegTech venture capital hub, with combined UK RegTech funding exceeding GBP 100 Million in early 2026 alone. Innovate Finance launched RegTech UK in February 2025 to coordinate industry scaling and competitiveness.

Germany

The Germany RegTech Solutions Market reached approximately USD 1.20 Billion in 2025 and is forecast at a 19.0% country CAGR through 2034. BaFin held a DORA implementation review on 4 December 2025, classifying the first year as a transformation period and signaling intensified on-site inspections in 2026. Germany hosts ACTICO GmbH, a leading vendor for intelligent automation in compliance decisions, and the country's manufacturing-bank crossover demand supports specialized RegTech for export-finance KYC. The Financial Market Digitization Act complements DORA and the Markets in Crypto-Assets Regulation domestically.

India

The India RegTech Solutions Market reached approximately USD 0.95 Billion in 2025 and is forecast at a 22.6% country CAGR through 2034, the fastest among major economies. The Reserve Bank of India tightened digital lending norms during 2025 and is rolling out a Central Bank Digital Currency pilot, creating new compliance use cases. SEBI updated KYC norms for foreign portfolio investors in 2025. IndiaMART acquired a 10% stake in Baldor Technologies (IDfy) in May 2024 for approximately USD 10.9 Million to strengthen digital onboarding capabilities, signaling consolidation among Indian RegTech vendors.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Component

- Solutions

- Regulatory Reporting Solutions

- Risk and Compliance Management Solutions

- Anti-Money Laundering (AML) Solutions

- Know Your Customer (KYC) and Customer Due Diligence Solutions

- Fraud Detection and Prevention Solutions

- Identity Verification Solutions

- Transaction Monitoring Solutions

- Governance, Risk, and Compliance (GRC) Solutions

- Regulatory Intelligence and Change Management Solutions

- Data Protection and Privacy Management Solutions

- Others

- Services

- Consulting Services

- Implementation and Integration Services

- Managed Services

- Support and Maintenance Services

- Training and Education Services

By Deployment Mode

- Cloud-Based Deployment

- On-Premises Deployment

- Hybrid Deployment

By Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises (SMEs)

By Application

- Anti-Money Laundering (AML) and Financial Crime Management

- Know Your Customer (KYC) and Customer Onboarding

- Regulatory Reporting and Compliance Management

- Risk Management

- Fraud Detection and Prevention

- Identity and Access Management

- Transaction Monitoring

- Data Governance and Privacy Compliance

- Tax Compliance and Reporting

- ESG and Sustainability Compliance

- Cybersecurity Compliance

- Audit and Internal Controls Management

- Others

By End-User

- Banking, Financial Services, and Insurance (BFSI)

- FinTech Companies

- Government and Regulatory Authorities

- Healthcare and Life Sciences

- Information Technology and Telecommunications

- Retail and E-commerce

- Energy and Utilities

- Manufacturing

- Real Estate

- Legal Services

- Transportation and Logistics

- Media and Entertainment

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 19.80 B |

| Forecast Revenue (2034) | USD 105.30 B |

| CAGR (2025-2034) | 20.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Solutions, Services), By Deployment Mode, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment), By Enterprise Size, (Large Enterprises, Small and Medium-Sized Enterprises (SMEs)), By Application, (Anti-Money Laundering (AML) and Financial Crime Management, Know Your Customer (KYC) and Customer Onboarding, Regulatory Reporting and Compliance Management, Risk Management, Fraud Detection and Prevention, Identity and Access Management, Transaction Monitoring, Data Governance and Privacy Compliance, Tax Compliance and Reporting, ESG and Sustainability Compliance, Cybersecurity Compliance, Audit and Internal Controls Management, Others), By End-User, (Banking, Financial Services, and Insurance (BFSI), FinTech Companies, Government and Regulatory Authorities, Healthcare and Life Sciences, Information Technology and Telecommunications, Retail and E-commerce, Energy and Utilities, Manufacturing, Real Estate, Legal Services, Transportation and Logistics, Media and Entertainment, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | IBM CORPORATION, THOMSON REUTERS CORPORATION, NICE ACTIMIZE (NICE LTD.), WOLTERS KLUWER N.V., BROADRIDGE FINANCIAL SOLUTIONS, INC., METRICSTREAM INC., ACTICO GMBH, FENERGO, CHAINALYSIS INC., COMPLYADVANTAGE, TRULIOO, JUMIO CORPORATION, LONDON STOCK EXCHANGE GROUP PLC, QUANTEXA, SUMSUB, NAPIER AI, THETARAY, TRM LABS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud-Based, On-Premises and Hybrid), By Enterprise Size (Large Enterprises and SMEs), By Application (AML & Financial Crime Management, KYC and Customer Onboarding, Regulatory Reporting, Risk Management, Fraud Detection and Identity Management), By End-User (BFSI, FinTech, Government, Healthcare, IT & Telecommunications, Retail and Manufacturing) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premises and Hybrid), By Enterprise Size (Large Enterprises and SMEs), By Application (AML & Financial Crime Management, KYC and Customer Onboarding, Regulatory Reporting, Risk Management, Fraud Detection and Identity Management), By End-User (BFSI, FinTech, Government, Healthcare, IT & Telecommunications, Retail and Manufacturing) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premises and Hybrid), By Enterprise Size (Large Enterprises and SMEs), By Application (AML & Financial Crime Management, KYC and Customer Onboarding, Regulatory Reporting, Risk Management, Fraud Detection and Identity Management), By End-User (BFSI, FinTech, Government, Healthcare, IT & Telecommunications, Retail and Manufacturing) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the RegTech Solutions Market?

The Global RegTech Solutions Market was valued at USD 16.45 Billion in 2024 and USD 19.80 Billion in 2025, and is projected to reach USD 105.30 Billion by 2034, growing at a CAGR of 20.4% from 2026 to 2034. Market growth is driven by increasing regulatory complexity, rising demand for compliance automation, and the adoption of AI-powered fraud detection and risk management solutions.

Who are the major players in the RegTech Solutions Market?

IBM CORPORATION, THOMSON REUTERS CORPORATION, NICE ACTIMIZE (NICE LTD.), WOLTERS KLUWER N.V., BROADRIDGE FINANCIAL SOLUTIONS, INC., METRICSTREAM INC., ACTICO GMBH, FENERGO, CHAINALYSIS INC., COMPLYADVANTAGE, TRULIOO, JUMIO CORPORATION, LONDON STOCK EXCHANGE GROUP PLC, QUANTEXA, SUMSUB, NAPIER AI, THETARAY, TRM LABS, Others

Which segments covered the RegTech Solutions Market?

By Component, (Solutions, Services), By Deployment Mode, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment), By Enterprise Size, (Large Enterprises, Small and Medium-Sized Enterprises (SMEs)), By Application, (Anti-Money Laundering (AML) and Financial Crime Management, Know Your Customer (KYC) and Customer Onboarding, Regulatory Reporting and Compliance Management, Risk Management, Fraud Detection and Prevention, Identity and Access Management, Transaction Monitoring, Data Governance and Privacy Compliance, Tax Compliance and Reporting, ESG and Sustainability Compliance, Cybersecurity Compliance, Audit and Internal Controls Management, Others), By End-User, (Banking, Financial Services, and Insurance (BFSI), FinTech Companies, Government and Regulatory Authorities, Healthcare and Life Sciences, Information Technology and Telecommunications, Retail and E-commerce, Energy and Utilities, Manufacturing, Real Estate, Legal Services, Transportation and Logistics, Media and Entertainment, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date