- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Regulatory Information Management Market Size, Share | CAGR 9.7%

Global Regulatory Information Management Market Size, Share, Growth Analysis By Component (Software, Implementation & Consulting Services, Training & Support, Managed Services), By Deployment (Cloud-Based, On-Premise, Hybrid), By Functionality (Submission Management, Regulatory Intelligence, Dossier Management, Document Management, Regulatory Analytics), By End User (Pharmaceutical, Biotechnology, Medical Device, CROs, Generics Manufacturers), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

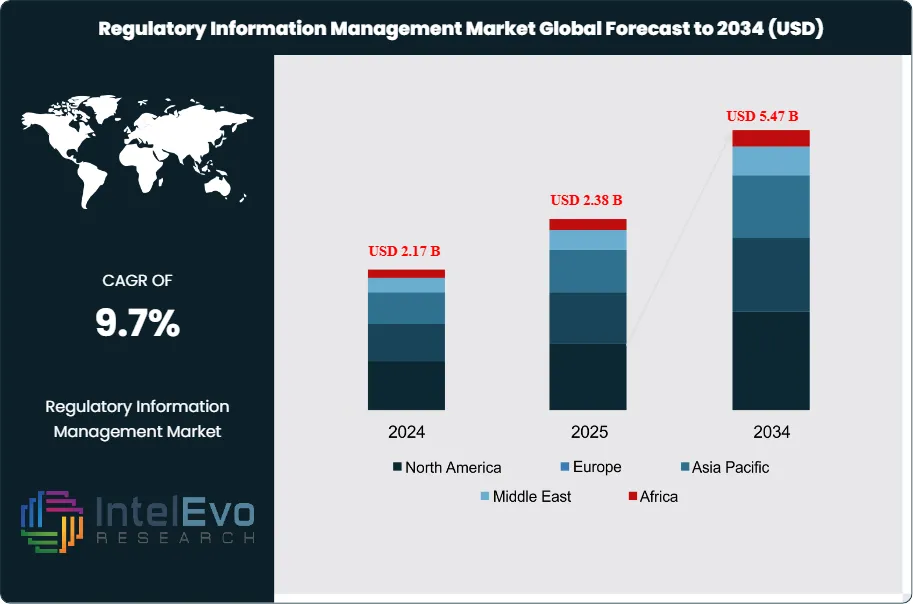

| USD 2.38 Billion | USD 5.47 Billion | 9.7% | North America, 41.2% |

The Regulatory Information Management Market was valued at approximately USD 2.17 Billion in 2024 and reached USD 2.38 Billion in 2025. The market is projected to grow to USD 5.47 Billion by 2034, expanding at a CAGR of 9.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.09 Billion over the analysis period, propelled by intensifying drug approval activity, expanding ICH eCTD submission mandates, and the accelerating digital transformation of regulatory affairs functions across global pharmaceutical, biotechnology, and medical device companies.

Get More Information about this report -

Request Free Sample ReportThe regulatory information management market occupies a critical compliance function within the life sciences industry, providing the software infrastructure required to author, assemble, track, submit, and maintain regulatory dossiers across the entire product lifecycle — from investigational new drug applications through post-approval variations and annual reports. Core regulatory information management workflows include eCTD submission management, regulatory intelligence monitoring, registration tracking across global health authority portals, and document lifecycle management aligned with ICH M4 CTD structure. The FDA's CDER and CBER divisions mandated eCTD-only submissions for all NDAs, BLAs, and ANDAs from 2017 onward, establishing eCTD-compliant submission management as a non-negotiable infrastructure requirement for US market access. The EMA extended similar mandates under its eSubmission Gateway, and the ICH M8 eCTD standard has now been adopted by regulatory authorities in 48 countries as of 2025.

Demand-side forces are concentrated among large pharmaceutical companies, which accounted for 46.8% of regulatory information management market revenue in 2025. These organizations manage simultaneous regulatory submissions across 30 to 80+ national health authorities, creating demand for multi-jurisdiction workflow orchestration, automated format validation, and integrated regulatory intelligence feeds. Supply-side dynamics reflect a moderately consolidated software market where specialized RIM vendors compete against broader life sciences platform providers on depth of ICH compliance coverage, regional health authority connectivity, and AI-assisted authoring capabilities.

Regulatory influences are the primary structural driver. The FDA's Structured Product Labeling (SPL) requirements, the EMA's Product Lifecycle Management (PLM) initiative under its Regulatory Science Strategy to 2025, and Japan's PMDA eCTD gateway expansion have collectively increased the technical complexity of multi-jurisdictional submission management. Technology effects are reshaping competitive positions. AI-assisted dossier authoring, automated gap analysis against ICH M4 requirements, and machine learning-based regulatory intelligence classification are compressing submission preparation timelines by 30–45% in early deployment cases. Cloud-based regulatory information management deployment reached 54.6% of new implementations in 2025, up from 28% in 2019. North America holds the largest regional share at 41.2% in 2025, while Asia Pacific is the fastest-growing region as Indian and Chinese generics and biosimilar manufacturers build global regulatory infrastructure. The regulatory information management market is positioned for sustained compound growth through 2034 as post-approval change management complexity and global submission volumes expand.

, By Deployment (Cloud-Based, On-Premise, Hybrid), By Functionality (Submission Management, Regulatory Intelligence, Dossier Management, Document Management, Regulatory Analytics), By End User (Pharmaceutical, Biotechnology, Medical Device, CROs, Generics Manufacturers), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global regulatory information management market was valued at USD 2.38 Billion in 2025 and is projected to reach USD 5.47 Billion by 2034, reflecting a CAGR of 9.7% during the forecast period 2026–2034.

- Segment Dominance: By Component, the Software segment leads with a 65.1% share of regulatory information management market revenue in 2025, driven by persistent enterprise demand for owned RIM platforms with deep ICH compliance coverage.

- Segment Dominance: By Functionality, the Submission Management segment holds a 38.4% revenue share in 2025, underpinned by mandatory eCTD submission requirements from the FDA, EMA, PMDA, and 45 additional national health authorities.

- Driver: Global expansion of eCTD submission mandates across 48 countries in 2025, combined with FDA CDER processing 1,850+ NDA and BLA submissions annually, drives continuous platform investment among pharmaceutical companies managing concurrent multi-authority submissions.

- Restraint: Integration complexity between legacy electronic document management systems (EDMS) and modern RIM platforms restricts migration speed, with full enterprise transitions averaging 18 to 30 months and costing USD 4 Million to USD 22 Million for large pharmaceutical organizations.

- Opportunity: Generics and biosimilar manufacturers in Asia Pacific represent an underpenetrated expansion opportunity worth approximately USD 780 Million by 2034, as Indian and Chinese companies build multi-country regulatory infrastructure to support FDA ANDA and EMA variation submissions.

- Trend: AI-assisted regulatory dossier authoring and automated ICH gap analysis are deployed in 32% of top-50 global pharmaceutical companies in 2025 and are projected to reach 68% adoption by 2030, compressing median submission preparation timelines by 35–45%.

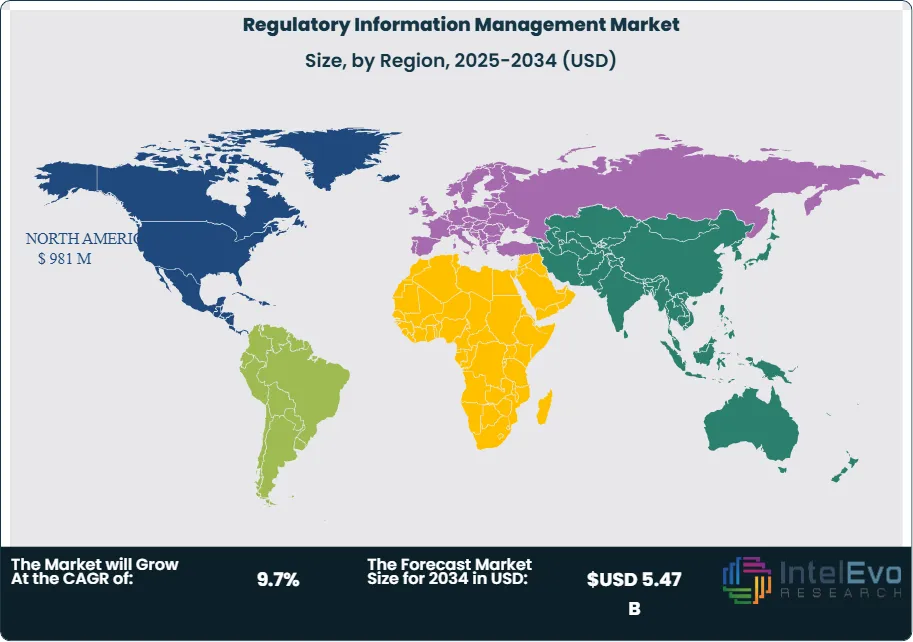

- Regional Analysis: North America leads the regulatory information management market with a 41.2% revenue share in 2025, equivalent to USD 981 Million, anchored by FDA submission volume requirements and the highest concentration of NDA and BLA originators globally.

Competitive Landscape Overview

The regulatory information management market is moderately consolidated, with the top four vendors — Veeva Systems, AMPLEXOR (Ennov Group), Lorenz Life Sciences, and Extedo — collectively holding approximately 52% of global software revenue in 2025. Competition centers on ICH compliance breadth, health authority portal connectivity, AI-assisted authoring depth, and cloud infrastructure quality. Strategic acquisitions accelerated between 2024 and 2026 as established vendors acquired specialist eCTD authoring firms and regulatory writing services providers to build integrated RIM-plus-services platforms. AI-native regulatory technology startups are entering the market with point-solution authoring tools, intensifying competitive pressure on traditional submission management vendors. Barriers to entry remain high due to extensive ICH and regional health authority certification requirements and multi-year enterprise implementation cycles.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product/Platform | Geographic Strength | Recent Strategic Move (2024–2026) |

|---|---|---|---|---|---|

| Veeva Systems | USA | Leader | Veeva Vault RIM | North America, Europe | Launched Vault RIM Suite 24.3 with AI-assisted dossier assembly and automated publishing workflows, Jan 2026 |

| AMPLEXOR (Ennov Group) | France | Leader | AMPLEXOR Life Sciences RIM | Europe, North America | Merged RIM and document management product lines under unified Ennov Life Sciences platform, Oct 2025 |

| Lorenz Life Sciences | Germany | Leader | docuBridge / Lorenz Regulatory Cloud | Europe, Asia Pacific | Expanded Lorenz Regulatory Cloud to support CDSCO eCTD v3.2.2 submissions for Indian market, Apr 2025 |

| Extedo | Germany | Leader | eCTD Manager | Europe, North America | Integrated AI-powered gap analysis module into eCTD Manager to identify submission deficiencies pre-filing, Sep 2025 |

| OpenText | Canada | Challenger | OpenText Documentum RIM | North America, Europe | Partnered with Pfizer to deploy cloud-based RIM infrastructure for global regulatory operations, Dec 2024 |

| Master Control | USA | Challenger | MasterControl Submissions | North America | Launched integrated quality-to-regulatory workflow module linking QMS and RIM submissions data, Mar 2025 |

| Instem | UK | Challenger | Instem Regulatory Submissions | Europe, North America | Acquired specialist eCTD authoring firm to strengthen regulatory technology stack, Jun 2025 |

| Aris Global | USA | Challenger | LifeSphere Regulatory | North America, Asia Pacific | Released LifeSphere Regulatory v4.2 with unified PV-RIM data bridge for post-market submissions, Nov 2025 |

| Samarth Life Sciences | India | Niche Player | RxSubmissions | Asia Pacific | Expanded RxSubmissions platform to support 18 additional national health authority submission portals, Aug 2025 |

| Certara | USA | Niche Player | Certara Regulatory Writing | North America, Europe | Won multi-year regulatory submission services contract with a top-20 global pharma company, Feb 2026 |

By Component

The regulatory information management market by component divides into Software and Services. The Software segment commands a 65.1% share in 2025, equivalent to USD 1.550 Billion, reflecting the strategic priority pharmaceutical and biotechnology companies place on purpose-built RIM platforms over service-only arrangements. Core software capabilities include eCTD assembly and validation engines, regulatory dossier lifecycle management, product registration tracking, regulatory intelligence aggregation, and integration with health authority submission portals such as the FDA's ESG (Electronic Submissions Gateway), EMA's eSubmission Gateway, and PMDA's eCTD gateway. Enterprise software contracts for large pharmaceutical companies average USD 1.8 Million to USD 4.5 Million annually in 2025, reflecting the mission-critical nature of submission management and the deep regulatory validation requirements imposed by FDA 21 CFR Part 11 and EU GxP Annex 11. The Services segment, encompassing implementation and consulting, training and support, and managed regulatory services, holds 34.9% of revenue in 2025 or USD 831 Million. Services intensity peaks during initial platform deployment and during major ICH standard transitions — such as the ongoing migration from eCTD v3.2 to v4.0 — when pharmaceutical companies require external expertise to manage system reconfiguration, data migration, and revalidation. Managed regulatory services are the fastest-growing services sub-segment, growing at 12.3% annually in 2025 as mid-size pharmaceutical companies outsource RIM operations rather than building in-house regulatory IT teams.

By Deployment Mode

Cloud-Based deployment accounts for 54.6% of the regulatory information management market in 2025, valued at USD 1.300 Billion. The shift to cloud reflects pharmaceutical companies' desire for continuous regulatory update propagation — a critical operational requirement as health authorities regularly revise eCTD technical specifications, MedDRA medical coding versions, and submission portal APIs. Cloud-hosted RIM platforms receive regulatory compliance updates on a vendor-managed schedule, eliminating the revalidation burden that accompanies on-premise software upgrades and reducing annual IT compliance costs by an estimated 20–35% compared with on-premise equivalents. Cloud growth is concentrated among mid-size and clinical-stage pharmaceutical companies that lack internal IT infrastructure for on-premise deployment and validation. On-Premise deployment retains 32.8% of market revenue in 2025 (USD 781 Million), concentrated among large established pharmaceutical organizations that hold legacy EDMS investments, have completed system validations, and operate stringent data residency policies that restrict cloud hosting of regulatory submission content. Hybrid deployment, combining on-premise document management with cloud-based submission processing and regulatory intelligence, holds 12.6% of the market in 2025 (USD 300 Million) and represents the primary migration pathway for large companies transitioning from full on-premise environments.

By Functionality

Submission Management leads the regulatory information management market by functionality with a 38.4% share in 2025, generating USD 914 Million. This sub-segment encompasses eCTD authoring, validation, publishing, and electronic gateway submission capabilities — the functions with the most direct regulatory compliance dependency. FDA CDER processes approximately 1,850 NDA, BLA, and ANDA submissions annually, while the EMA's centralized procedure receives over 600 marketing authorization applications and 4,200 post-approval variation submissions per year. The sheer volume and format-specificity of these submissions make purpose-built Submission Management software non-negotiable for pharmaceutical companies seeking consistent submission quality. Regulatory Intelligence holds 21.7% share in 2025 (USD 517 Million), covering software platforms that monitor, classify, and distribute regulatory guidance documents, health authority communications, and regional labeling requirement updates. With pharmaceutical companies monitoring regulatory activity across 40 to 80 national markets, automated regulatory intelligence feeds save regulatory affairs teams an estimated 2,400 to 3,600 analyst-hours per year in manual monitoring. Registration and Dossier Management accounts for 18.9% (USD 450 Million), tracking product registration status, license renewal deadlines, and variation submission timelines across multi-country portfolios. Document Management and Regulatory Reporting and Analytics contribute 12.4% (USD 295 Million) and 8.6% (USD 205 Million) respectively, with Analytics growing fastest as companies build executive dashboards tracking submission KPIs and approval timelines.

By End User

Pharmaceutical Companies are the dominant end-user segment with a 46.8% share of the regulatory information management market in 2025 (USD 1.114 Billion). These companies manage the largest and most complex regulatory portfolios, with a top-10 global pharmaceutical company typically maintaining 3,000 to 8,000 active product registrations across 80+ countries simultaneously. Each registration requires ongoing maintenance through variation submissions, periodic safety update reports, and labeling harmonization — all workflows dependent on integrated RIM software. Biotechnology Companies account for 24.3% (USD 578 Million), a segment growing at approximately 11.8% annually as the FDA's biologics approval pipeline expands and BLA submission volumes increase with novel cell and gene therapy approvals. Medical Device Manufacturers hold 14.6% (USD 348 Million), driven by EU MDR 2017/745 technical documentation requirements and FDA 510(k) and De Novo submission management needs. Contract Research Organizations (CROs) represent 8.7% (USD 207 Million), with growth linked to expanding regulatory submission outsourcing as pharmaceutical companies contract out IND, NDA, and variation filing management to specialized CRO regulatory affairs units. Generics Manufacturers contribute the remaining 5.6% (USD 133 Million), a segment growing rapidly in Asia Pacific as Indian and Chinese generics manufacturers invest in RIM infrastructure to support multi-country ANDA and ASMF filing programs.

Regional Analysis

North America

North America leads the regulatory information management market with a 41.2% revenue share in 2025, equivalent to USD 981 Million. The United States accounts for approximately 90% of regional revenue, driven by the FDA's comprehensive electronic submission infrastructure and the highest global concentration of NDA, BLA, and ANDA originators. FDA CDER's eCTD-only mandate, in effect since 2017, established a structural floor for RIM software investment that continues to generate upgrade and replacement cycles as ICH eCTD v4.0 adoption advances. The Center for Devices and Radiological Health (CDRH) extended eMDR and eSTAR submission requirements through 2024–2025, expanding RIM software demand into the medical device segment. Canada contributes approximately 8% of North American revenue, with Health Canada's aligned eCTD submission requirements and its Vanessa's Law amendments strengthening post-market regulatory reporting obligations that expand RIM platform utilization. The United States hosts the largest global base of pharmaceutical regulatory affairs professionals — over 35,000 FDA-registered regulatory affairs practitioners — representing a high-density customer pool for RIM software vendors. Investment in AI-assisted regulatory authoring among US-headquartered pharmaceutical companies is generating premium licensing premiums of 15–25% above standard RIM platform pricing in 2025, as demonstrated by early deployment results at Merck, Eli Lilly, and AstraZeneca's US regulatory operations.

Europe

Europe represents 28.6% of the global regulatory information management market in 2025, valued at USD 681 Million. The regulatory framework is anchored by EMA centralized procedures, EU MRP and DCP national authorization routes, and the EMA's ongoing Product Lifecycle Management (PLM) initiative, which aims to digitize and standardize the full product information lifecycle across all EU member states. Germany is the largest national market, contributing approximately 21% of European revenue, supported by BfArM and PEI oversight and Germany's role as home to Bayer, Boehringer Ingelheim, and a dense network of pharmaceutical manufacturers. France accounts for 17% of European revenue, driven by ANSM oversight and Sanofi's extensive global regulatory operation. The United Kingdom, operating independently post-Brexit through the MHRA, has established its own Innovative Licensing and Access Pathway (ILAP) and maintains distinct submission format requirements, creating additional RIM infrastructure demand for companies seeking concurrent UK and EU marketing authorizations. Switzerland, home to Roche and Novartis, contributes approximately 11% of European revenue and hosts some of the world's most technically sophisticated in-house RIM deployments. The EU's Product Information Management (PIM) standards under HMA-EMA joint initiatives and the ePI (electronic product information) standard are driving RIM platform upgrades across Europe, adding incremental demand through 2028.

Asia Pacific

Asia Pacific accounts for 19.4% of the global regulatory information management market in 2025, valued at USD 462 Million, and is the fastest-growing region with a projected CAGR of 12.4% during 2025–2034. India leads regional market growth, representing approximately 29% of Asia Pacific revenue, driven by CDSCO's eCTD adoption mandate from 2023, the rapid expansion of India's generic and biosimilar export programs requiring simultaneous FDA ANDA and EMA variation submissions, and the concentration of CDMO regulatory affairs operations. China represents approximately 27% of regional revenue, with NMPA reforms under the 2020 ICH implementation roadmap compelling Chinese pharmaceutical companies to invest in RIM systems capable of supporting China-specific submissions alongside global eCTD filings. Japan holds 25% of Asia Pacific revenue, anchored by PMDA's eCTD gateway and Japan's position as a top-5 global pharmaceutical market requiring dedicated regulatory submission management. South Korea accounts for 11% of regional revenue, supported by MFDS ICH alignment and Korea's growing biosimilar export industry. Government investment in regulatory digitalization across ASEAN markets — including Thailand, Indonesia, and Vietnam — represents an emerging growth frontier within Asia Pacific RIM adoption between 2025 and 2030.

Latin America

Latin America holds a 6.4% share of the regulatory information management market in 2025, valued at USD 152 Million. Brazil is the dominant national market at approximately 46% of regional revenue, driven by ANVISA's structured electronic submission requirements and Brazil's role as Latin America's largest pharmaceutical market with a regulated product registration system covering over 15,000 active marketing authorizations. ANVISA's progressive alignment with ICH technical guidelines, including eCTD adoption for new product submissions, is driving pharmaceutical companies operating in Brazil to upgrade legacy regulatory dossier systems. Mexico contributes approximately 22% of regional revenue, supported by COFEPRIS electronic submission infrastructure and Mexico's increasing strategic importance as a pharmaceutical manufacturing and distribution hub for North and Latin American markets. Argentina accounts for 16% of regional revenue, with ANMAT's pharmacovigilance and regulatory reporting requirements creating ongoing document management and submission software demand. The broader Latin American market remains at an early stage of RIM software penetration, with most mid-size regional pharmaceutical companies still managing regulatory submissions through fragmented manual and semi-automated workflows. Harmonization efforts under the Pan American Network on Drug Regulatory Harmonization (PANDRH) represent a medium-term catalyst for structured RIM adoption across the region.

Middle East and Africa

The Middle East and Africa region accounts for 4.4% of the global regulatory information management market in 2025, generating USD 105 Million in annual revenue. The United Arab Emirates leads regional revenue with approximately 37% share, driven by the Dubai Health Authority and Abu Dhabi Department of Health's electronic submission requirements and the UAE's role as a regional pharmaceutical registration hub for multinational companies seeking GCC market access through a single initial registration. Saudi Arabia accounts for approximately 31% of MEA revenue, supported by the SFDA's progressive adoption of ICH guidelines from 2022 onward and Vision 2030's healthcare investment programs that are expanding local pharmaceutical manufacturing and regulatory compliance infrastructure. South Africa represents approximately 20% of MEA revenue, anchored by SAHPRA's structured marketing authorization process and South Africa's dual role as Africa's most developed regulatory market and a gateway for pharmaceutical companies seeking broader Sub-Saharan African distribution. The African Medicines Regulatory Harmonization (AMRH) initiative, supported by the African Union and WHO, is advancing harmonized regulatory submission standards across ECOWAS, EAC, and SADC regional blocs — creating structured medium-term RIM software demand as continental regulatory digitalization progresses. GCC regulatory alignment with ICH eCTD standards from 2024 is accelerating software procurement among Saudi and Emirati regulatory affairs teams.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Software

- Services (Implementation & Consulting, Training & Support, Managed Services)

By Deployment

- Cloud-Based

- On-Premise

- Hybrid

By Functionality

- Submission Management

- Regulatory Intelligence

- Registration & Dossier Management

- Document Management

- Regulatory Reporting & Analytics

By End User

- Pharmaceutical Companies

- Biotechnology Companies

- Medical Device Manufacturers

- Contract Research Organizations (CROs)

- Generics Manufacturers

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.38 B |

| Forecast Revenue (2034) | USD 5.47 B |

| CAGR (2025-2034) | 9.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Software, Services (Implementation & Consulting, Training & Support, Managed Services)), By Deployment (Cloud-Based, On-Premise, Hybrid), By Functionality (Submission Management, Regulatory Intelligence, Registration & Dossier Management, Document Management, Regulatory Reporting & Analytics), By End User (Pharmaceutical Companies, Biotechnology Companies, Medical Device Manufacturers, Contract Research Organizations (CROs), Generics Manufacturers), By Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | VEEVA SYSTEMS, AMPLEXOR (ENNOV GROUP), LORENZ LIFE SCIENCES, EXTEDO, OPENTEXT, MASTERCONTROL, INSTEM, ARIS GLOBAL, SAMARTH LIFE SCIENCES, CERTARA, NAVITAS LIFE SCIENCES, REGNOLOGY, YSEOP, CATO RESEARCH, REGULATORY COMPLIANCE ASSOCIATES (RCA), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud-Based, On-Premise, Hybrid), By Functionality (Submission Management, Regulatory Intelligence, Dossier Management, Document Management, Regulatory Analytics), By End User (Pharmaceutical, Biotechnology, Medical Device, CROs, Generics Manufacturers), Industry Trends & Forecast 2026-2034")

, By Deployment (Cloud-Based, On-Premise, Hybrid), By Functionality (Submission Management, Regulatory Intelligence, Dossier Management, Document Management, Regulatory Analytics), By End User (Pharmaceutical, Biotechnology, Medical Device, CROs, Generics Manufacturers), Industry Trends & Forecast 2026-2034")

, By Deployment (Cloud-Based, On-Premise, Hybrid), By Functionality (Submission Management, Regulatory Intelligence, Dossier Management, Document Management, Regulatory Analytics), By End User (Pharmaceutical, Biotechnology, Medical Device, CROs, Generics Manufacturers), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Regulatory Information Management Market?

The Global Regulatory Information Management Market was valued at USD 2.17 Billion in 2024 and is projected to reach USD 5.47 Billion by 2034, growing at a CAGR of 9.7% from 2026 to 2034, driven by increasing regulatory compliance requirements, rising digital transformation in life sciences, and growing adoption of cloud-based RIM solutions.

Who are the major players in the Regulatory Information Management Market?

VEEVA SYSTEMS, AMPLEXOR (ENNOV GROUP), LORENZ LIFE SCIENCES, EXTEDO, OPENTEXT, MASTERCONTROL, INSTEM, ARIS GLOBAL, SAMARTH LIFE SCIENCES, CERTARA, NAVITAS LIFE SCIENCES, REGNOLOGY, YSEOP, CATO RESEARCH, REGULATORY COMPLIANCE ASSOCIATES (RCA), Others

Which segments covered the Regulatory Information Management Market?

By Component (Software, Services (Implementation & Consulting, Training & Support, Managed Services)), By Deployment (Cloud-Based, On-Premise, Hybrid), By Functionality (Submission Management, Regulatory Intelligence, Registration & Dossier Management, Document Management, Regulatory Reporting & Analytics), By End User (Pharmaceutical Companies, Biotechnology Companies, Medical Device Manufacturers, Contract Research Organizations (CROs), Generics Manufacturers), By Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Regulatory Information Management Market

Published Date : 11 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date