- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

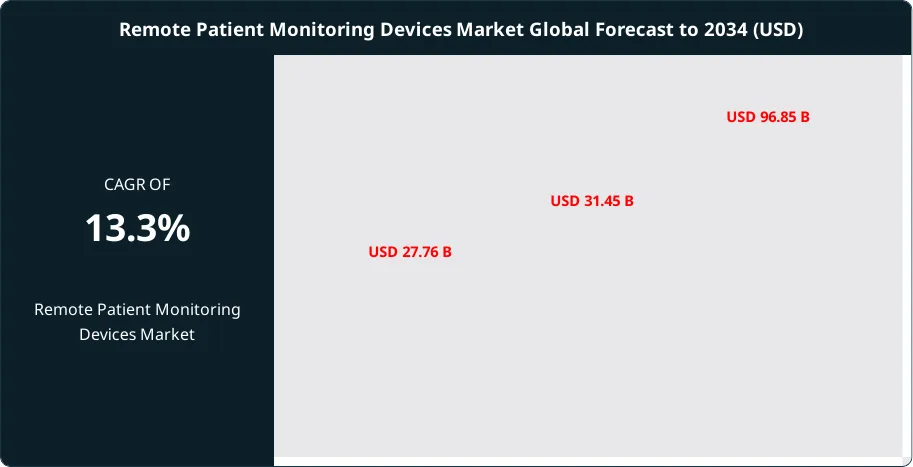

Global Remote Patient Monitoring Devices Market Size, Share | CAGR 13.3%

Global Remote Patient Monitoring Devices Market Size, Share & Industry Analysis By Product (Vital Sign Monitoring, Cardiac Monitoring, Glucose Monitoring, Neurological Monitoring, Fetal and Maternal Monitoring, Multiparameter Monitoring, Weight Monitoring and Remote Spirometers), By Application (Cardiovascular Diseases, Diabetes Management, COPD, Hypertension, Neurological Disorders, Sleep Disorders, Cancer Care and Elderly Care), By End-User (Hospitals, Home Healthcare, Ambulatory Care Centers, Specialty Clinics and Nursing Homes) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 31.45 Billion | USD 96.85 Billion | 13.3% | North America, 46.2% |

The Remote Patient Monitoring Devices Market was valued at USD 27.76 Billion in 2024 and USD 31.45 Billion in 2025. The market is projected to reach USD 96.85 Billion by 2034, expanding at a CAGR of 13.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 65.40 Billion over the analysis period. Remote patient monitoring (RPM) devices are FDA-cleared medical instruments that automatically collect and digitally transmit patient physiological data, including blood pressure, blood glucose, oxygen saturation, electrocardiogram readings, body weight, and continuous heart rhythm, from home and ambulatory settings to clinicians for real-time clinical decision-making and chronic disease management.

Get More Information about this report -

Request Free Sample ReportReimbursement expansion through CMS is the primary structural growth driver. The 2025 Medicare Physician Fee Schedule extended RPM CPT code billing privileges to Rural Health Clinics (RHCs) and Federally Qualified Health Centers (FQHCs) for the first time, opening reimbursement access to underserved patient populations. The 2026 Medicare Physician Fee Schedule introduced new shorter-duration RPM codes (CPT 99470 reimbursing USD 26 for the first 10 minutes of management time), reversing five years of conversion factor reductions with a 2026 CF of USD 33.40 for non-QPs. CMS approved 133 Hospital-at-Home programs across 37 states by April 2024, generating institutional procurement of FDA-cleared RPM devices for acute care delivery in residential settings. A typical Medicare RPM enrollment generates approximately USD 99 per patient per month in provider revenue, creating a sustainable economic foundation for device deployment.

The continuous glucose monitoring (CGM) subsegment, dominated by Abbott Laboratories (Freestyle Libre, Lingo) and Dexcom (G7), has emerged as the largest single product category. Abbott controlled 56.30% of CGM shipments in 2025, Dexcom held 35.10%, and Medtronic accounted for 6.88%, collectively delivering 98.28% of global continuous glucose monitor volume. The April 2025 FDA clearance of the Dexcom G7 15-Day CGM System extended sensor wear time and improved mean absolute relative difference accuracy to 8.0%. AI-driven wearable medical devices received FDA clearances throughout 2025, including Masimo's W1 medical watch for continuous SpO2 and pulse rate, Element Science's Jewel Patch Wearable Cardioverter Defibrillator (May 2025), and WHOOP's ECG feature (April 2025). VitalConnect's VitalRhythm biosensor was cleared in April 2025 for continuous ECG, heart rate, and respiratory monitoring.

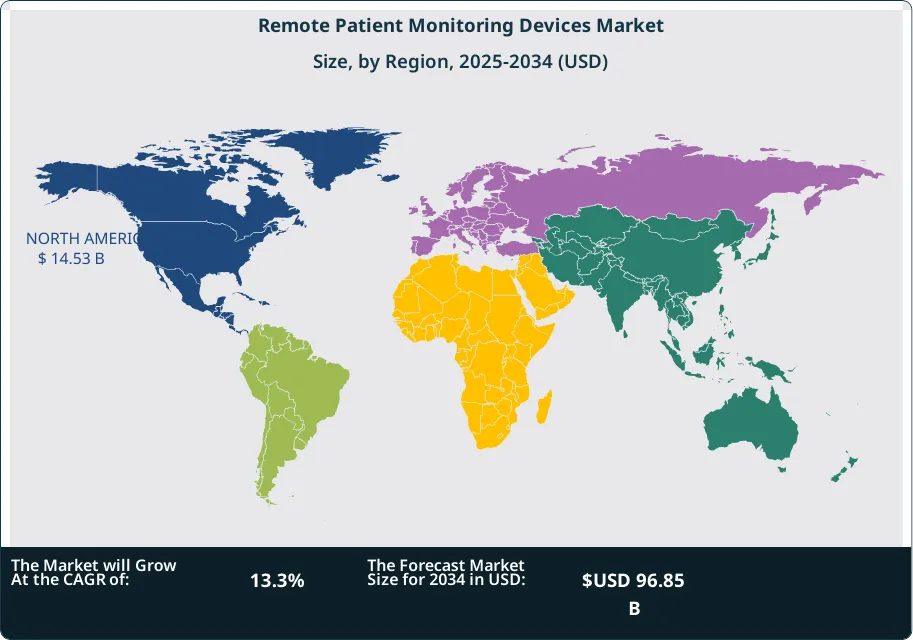

North America held 46.2% of the remote patient monitoring devices market in 2025 at approximately USD 14.53 Billion, anchored by the United States where Medicare RPM reimbursement, an aging population, and a 17.9 million annual cardiovascular death burden drive adoption. Europe accounted for 24.6% at USD 7.74 Billion, supported by Germany's chronic disease management programs and the UK NHS's Virtual Ward initiative. Asia Pacific represented 21.8% at USD 6.86 Billion and is projected to record the fastest CAGR of 16.4% through 2034, driven by 589 million adult diabetes patients across the region as of 2024 (International Diabetes Federation), India's expanding home healthcare market projected to reach USD 19.9 Billion by 2025, and Japanese partnerships such as Monidor Oy with Senko Medical for remote infusion therapy monitoring.

Market Definition & Scope

The remote patient monitoring devices market is defined as the global commercial segment for FDA-cleared, CE-marked, or otherwise regulated medical devices that automatically capture patient physiological data outside traditional clinical settings and transmit that data digitally to healthcare providers for clinical decision-making, chronic disease management, post-discharge follow-up, and acute care delivery. The market encompasses cardiac monitoring devices (Holter monitors, implantable loop recorders, mobile cardiac telemetry), blood pressure monitors, blood glucose monitors and continuous glucose monitoring systems, pulse oximeters and respiratory monitors, multiparameter vital signs monitors, fetal and neonatal monitors, sleep monitoring devices, and connected weight scales.

This analysis includes both clinician-prescribed RPM devices (eligible for Medicare CPT 99453, 99454, 99457, 99458, and 99470 reimbursement) and FDA-cleared consumer wearables marketed for medical use. The report explicitly excludes general consumer fitness trackers without FDA medical device clearance, hospital-only patient monitors fixed to bedside, manually entered self-reporting applications without automatic data transmission, and software-only RPM platforms without proprietary device hardware. The remote patient monitoring devices market is the device-hardware subset of the broader remote patient monitoring market (USD 39.97 to 59.92 Billion in 2025 depending on definition), which also includes platform software, services, and care management.

, By Application (Cardiovascular Diseases, Diabetes Management, COPD, Hypertension, Neurological Disorders, Sleep Disorders, Cancer Care and Elderly Care), By End-User (Hospitals, Home Healthcare, Ambulatory Care Centers, Specialty Clinics and Nursing Homes) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The remote patient monitoring devices market grew from USD 31.45 Billion in 2025 to a projected USD 96.85 Billion by 2034, at a 13.3% CAGR, representing USD 65.40 Billion in absolute dollar opportunity.

- Segment Dominance (By Product): Blood glucose monitoring devices held the largest share at 32.6% in 2025 at approximately USD 10.25 Billion, dominated by Abbott (56.30% CGM share), Dexcom (35.10%), and Medtronic (6.88%) following the April 2025 FDA clearance of the Dexcom G7 15-Day system.

- Segment Dominance (By End-Use): Home-care settings accounted for 69.1% of end-use revenue in 2025 at approximately USD 21.73 Billion, reflecting the structural shift toward decentralized care delivery and the 1.5 billion-person elderly population projected by 2050 per WHO.

- Driver: CMS's 2025 expansion of RPM CPT codes to Rural Health Clinics and Federally Qualified Health Centers, combined with the 2026 introduction of CPT 99470 for shorter monitoring durations, broadens the reimbursable patient population and creates predictable monthly revenue of approximately USD 99 per Medicare beneficiary.

- Restraint: Cybersecurity and data privacy concerns under HIPAA in the U.S. and GDPR in Europe constrain provider adoption rates, with FDA flagging connected medical devices as expanding the attack surface for ransomware and unauthorized access.

- Opportunity: AI-driven predictive monitoring represents the largest opportunity, with Validic's February 2025 generative AI launch automating EHR-integrated patient data analysis and the U.S. Department of Veterans Affairs deploying AI-driven RPM systems across multiple VA centers in 2025.

- Trend: Consumer-grade wearables are crossing into medical-device classification through FDA 510(k) clearances, including Masimo W1, WHOOP ECG (April 2025), and VitalConnect VitalRhythm (April 2025), expanding the addressable RPM market beyond traditional medical device manufacturers.

- Regional: North America led the remote patient monitoring devices market with 46.2% share valued at USD 14.53 Billion in 2025, supported by CMS reimbursement infrastructure and the U.S. RPM market's projected growth from USD 16.09 Billion in 2025 to USD 29.13 Billion by 2030.

Key Insights Summary

- Abbott Laboratories led the continuous glucose monitoring market with 56.30% of 2025 shipment volume, followed by Dexcom at 35.10% and Medtronic at 6.88%, with the top three controlling 98.28% of global CGM unit volume (industry analysis, January 2026).

- CMS approved 133 Hospital-at-Home programs across 37 states by April 2024, generating institutional procurement demand for FDA-cleared RPM devices to enable acute care delivery in residential settings.

- Medicare 2026 Physician Fee Schedule introduces new RPM CPT code 99470 reimbursing USD 26 for the first 10 minutes of management time, alongside the existing CPT 99457 (USD 52 monthly) and CPT 99458 (USD 41 additional monthly), making 2026 the first year with two separate Medicare conversion factors (USD 33.57 for QPs, USD 33.40 for non-QPs).

- Approximately 589 million adults aged 20–79 were living with diabetes worldwide in 2024, projected to reach 853 million by 2050 according to the International Diabetes Federation, expanding the addressable patient population for blood glucose monitoring devices.

- Dexcom G7 15-Day CGM System received FDA clearance in April 2025 with mean absolute relative difference (MARD) accuracy of 8.0% for adults with diabetes, extending sensor wear duration by 50% over the previous 10-day generation.

- Element Science's Jewel Patch Wearable Cardioverter Defibrillator received FDA approval in May 2025 for patients at temporary risk of sudden cardiac arrest, expanding the RPM device category into life-critical interventional applications.

Competitive Landscape Overview

The remote patient monitoring devices market is moderately consolidated, with the top five players holding approximately 70% combined market share in 2025: Abbott Laboratories (over 35%), Dexcom, Boston Scientific, Medtronic, and Koninklijke Philips. Competition operates across three dimensions: clinical accuracy (FDA-cleared MARD scores for CGMs, ECG sensitivity for cardiac monitors), platform integration (electronic health record interoperability, fleet management software, AI-driven analytics), and reimbursement coverage (CMS, commercial payers, and 42 state Medicaid programs as of January 2025). Strategic partnerships have intensified throughout 2025: Tenovi and Validic partnered in April 2025 to integrate cellular-connected RPM infrastructure with EHR-connected platforms; Circadian Health partnered with Tenovi in March 2025 to enhance chronic disease care; Teladoc Health acquired Catapult Health in February 2025 to combine at-home testing with telehealth. Consumer technology companies including Apple, Alphabet (Google), Samsung, Garmin, and Withings are crossing into the medical device segment through FDA 510(k) pathways, intensifying competitive pressure on traditional players. The Apple-Masimo patent dispute over pulse oximetry technology illustrates the contested boundary between consumer wearables and regulated medical devices.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product/Platform | Geo Strength | Founded | Recent Strategic Move |

| Abbott Laboratories | US | Leader | FreeStyle Libre, Lingo OTC CGM | Global | 1888 | Dual glucose/ketone sensor advances (2025) |

| Dexcom Inc. | US | Leader | G7 15-Day CGM, Stelo OTC | Global | 1999 | FDA G7 15-Day clearance (Apr 2025) |

| Medtronic | Ireland/US | Leader | LINQ II ICM, CareLink, Guardian | Global | 1949 | AccuRhythm AI for cardiac monitoring (2025) |

| Koninklijke Philips | Netherlands | Leader | BioTel mobile cardiac telemetry | Global | 1891 | Virtual care management portfolio expansion |

| Boston Scientific | US | Leader | HeartLogic, LATITUDE NXT | Global | 1979 | AI-driven heart failure monitoring scaling (2025) |

| Masimo Corporation | US | Challenger | W1 medical watch, SafetyNet | Global | 1989 | Cleveland Clinic RPM partnership (2025) |

| GE HealthCare | US | Challenger | Portrait Mobile, Carescape | Global | 1994 | Masimo SET integration (2025) |

| iRhythm Technologies | US | Challenger | Zio AT, Zio Monitor | NA, Europe | 2006 | Long-term continuous ECG market leader |

By Product

Blood glucose monitoring devices dominated the remote patient monitoring devices market with 32.6% share in 2025 at approximately USD 10.25 Billion. Continuous glucose monitoring systems (CGMs) drive segment growth: Abbott's FreeStyle Libre family achieved 56.30% global CGM share, Dexcom's G7 platform held 35.10%, and Medtronic's Guardian sensors maintained 6.88%. The April 2025 FDA clearance of Dexcom G7 15-Day extended sensor life and improved 8.0% MARD accuracy. Abbott's over-the-counter Lingo CGM expanded the addressable market beyond diagnosed diabetes patients to wellness-oriented consumers. The 589 million global diabetes population projected to reach 853 million by 2050 underwrites sustained segment growth at a projected 14.1% CAGR through 2034.

Cardiac monitoring devices held 22.4% share at approximately USD 7.04 Billion in 2025. The category includes implantable loop recorders (Medtronic LINQ II), mobile cardiac telemetry monitors (Philips BioTel, iRhythm Zio), event monitors, Holter monitors, and wearable cardioverter defibrillators (Element Science Jewel WCD, FDA-approved May 2025). Medtronic's AccuRhythm AI algorithm integrated into the LINQ II identifies and classifies arrhythmias with reduced false-positive rates. Boston Scientific's HeartLogic algorithm provides multi-parameter heart failure prediction. The cardiac segment generated USD 5.1 Billion in 2025 specifically from cardiac RPM devices.

Blood pressure monitors and multiparameter vital signs monitors held 18.7% share at approximately USD 5.88 Billion in 2025. OMRON Healthcare leads the consumer blood pressure monitor segment with FDA-cleared connected devices. Pulse oximeters, respiratory monitors, and SpO2 wearables (including Masimo W1) accounted for 12.1% at USD 3.81 Billion. Sleep monitoring devices held 6.4% at USD 2.01 Billion, driven by ResMed's CPAP-integrated monitors. Fetal and neonatal monitors, neurological monitoring devices, and other categories comprised the remaining 7.8% at USD 2.46 Billion.

By Application

Diabetes management was the largest application segment of the remote patient monitoring devices market in 2025, holding 35.4% share at approximately USD 11.13 Billion, driven by the 589 million-person global diabetes population and the structural shift to continuous glucose monitoring. Cardiovascular diseases held 28.8% at USD 9.06 Billion, with Boston Scientific projecting the cardiovascular RPM device category could reach USD 6 Billion globally by 2030. Respiratory diseases including COPD and sleep apnea accounted for 14.2% at USD 4.47 Billion. Cancer-related monitoring (chemotherapy adherence, post-surgical recovery) held 8.5% at USD 2.67 Billion. Neurological disorders, post-acute care, and other applications comprised the remaining 13.1% at USD 4.12 Billion.

By End-User

Home-care settings dominated the remote patient monitoring devices market by end-user in 2025 with 69.1% share at approximately USD 21.73 Billion. Patient self-administration of FDA-cleared monitoring devices, supported by CMS Medicare reimbursement, has become the dominant care model for chronic disease management. Long-term care facilities and skilled nursing facilities accounted for 18.3% at USD 5.76 Billion, where RPM devices reduce transfer-to-hospital rates and improve resident outcomes. Hospitals and ambulatory care centers held 12.6% at USD 3.96 Billion, primarily for post-discharge monitoring and Hospital-at-Home program execution under the 133 CMS-approved programs across 37 states.

Regional Analysis

North America held the largest share of the remote patient monitoring devices market at 46.2% in 2025, valued at approximately USD 14.53 Billion. The United States represents over 92% of regional demand, with the U.S. RPM market projected to grow from USD 16.09 Billion in 2025 to USD 29.13 Billion by 2030 at a 12.6% CAGR. CMS Medicare reimbursement under CPT 99453, 99454, 99457, 99458, and the new 2026 CPT 99470 created a stable per-patient monthly revenue stream of approximately USD 99 that anchors device procurement. The 133 CMS-approved Hospital-at-Home programs across 37 states drive institutional purchasing. The U.S. Department of Veterans Affairs deployed AI-driven RPM systems across multiple VA centers in 2025. Canada contributes approximately USD 1.1 Billion in regional demand.

Europe accounted for 24.6% of the remote patient monitoring devices market at approximately USD 7.74 Billion in 2025. Germany leads regional demand with strong chronic disease management programs and an aging population. The UK National Health Service Virtual Ward initiative deploys remote monitoring across post-acute care pathways. EU MDR (Medical Device Regulation) compliance shapes device certification timelines and creates barriers to entry for new RPM device manufacturers. Cambridge University Hospitals NHS Foundation Trust adopted Masimo W1 for telehealth and virtual health discharge programs. Philips, headquartered in Amsterdam, holds significant regional market share through integrated RPM and acute care monitoring portfolios.

Asia Pacific represented 21.8% of the remote patient monitoring devices market at approximately USD 6.86 Billion in 2025 and is projected to record the fastest regional CAGR of 16.4% through 2034. China leads regional demand through expanding chronic disease management programs and a 140 million-person diabetes population. India's home healthcare market is projected to reach USD 19.9 Billion by 2025 from USD 5.4 Billion in 2022, creating substantial RPM device demand alongside India's projected 134 million diabetes patients by 2045. Japan's aging population (29% over age 65) drives strong wearable monitoring adoption, with partnerships such as Monidor Oy and Senko Medical (March 2023) representing the country's regional distribution model.

Latin America held 4.8% of the remote patient monitoring devices market at approximately USD 1.51 Billion in 2025, with Brazil and Mexico as primary markets. Middle East and Africa accounted for 2.6% at approximately USD 818 million. Both regions face cold chain logistics constraints and reimbursement infrastructure gaps that limit RPM device penetration despite high underlying chronic disease burdens.

Country Analysis

The United States dominates the remote patient monitoring devices market with an estimated value of USD 13.42 Billion in 2025 and a country-level CAGR of 13.8% through 2034. Medicare CPT code reimbursement under the 2025 Physician Fee Schedule, expanded in 2026 with new shorter-duration codes, anchors provider economics. CMS conversion factors increased to USD 33.40 (non-QPs) and USD 33.57 (QPs) in 2026, reversing five years of payment reductions. Forty-two state Medicaid programs cover RPM as of January 2025, alongside growing commercial payer adoption. Abbott Laboratories (Abbott Park, Illinois), Dexcom (San Diego, California), Boston Scientific (Marlborough, Massachusetts), Medtronic (Minneapolis, Minnesota), Masimo (Irvine, California), and iRhythm Technologies (San Francisco, California) operate domestic manufacturing and headquarters. The 133 CMS-approved Hospital-at-Home programs across 37 states create institutional demand exceeding USD 800 million annually for FDA-cleared RPM device fleets.

Germany represents Europe's largest national market at approximately USD 1.85 Billion in 2025 with a CAGR of 11.6%. The country's statutory health insurance (GKV) system provides reimbursement coverage for diabetes management devices, cardiac monitors, and respiratory monitors. Germany's chronic disease management programs (DMPs) for diabetes, COPD, and coronary heart disease integrate RPM data into structured clinical workflows. The German Hospital Future Act (Krankenhauszukunftsgesetz) allocated EUR 4.3 billion for digital health infrastructure including RPM platforms.

China is the third-largest national market valued at approximately USD 2.1 Billion in 2025, with a projected CAGR of 17.9%. The country's diabetes population exceeds 140 million, and government-supported chronic disease management initiatives are integrating RPM devices into community health networks. Domestic manufacturers including Guangdong Transtek Medical Electronics compete with international leaders on cost. China's 14th Five-Year Plan prioritizes telemedicine and remote monitoring infrastructure expansion.

Japan contributes approximately USD 1.4 Billion to the remote patient monitoring devices market in 2025 with a CAGR of 12.4%. The country's 29% population over age 65 drives strong wearable medical device adoption. OMRON Healthcare, headquartered in Kyoto, leads the domestic blood pressure monitor segment globally. Senko Medical's distribution partnership with Monidor Oy (March 2023) for remote infusion therapy monitoring represents the country's import-distribution model for specialized RPM devices.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Product

- Vital Sign Monitoring Devices

- Blood Pressure Monitors

- Heart Rate Monitors

- Pulse Oximeters

- Temperature Monitoring Devices

- Respiratory Monitoring Devices

- Cardiac Monitoring Devices

- Electrocardiogram (ECG) Monitors

- Implantable Cardiac Monitors

- Cardiac Event Monitors

- Glucose Monitoring Devices

- Continuous Glucose Monitoring (CGM) Systems

- Blood Glucose Meters

- Neurological Monitoring Devices

- Electroencephalogram (EEG) Monitors

- Sleep Monitoring Devices

- Fetal and Maternal Monitoring Devices

- Multiparameter Monitoring Devices

- Weight Monitoring Devices

- Remote Spirometers

- Others

By Application

- Cardiovascular Diseases

- Diabetes Management

- Chronic Obstructive Pulmonary Disease (COPD)

- Hypertension Management

- Neurological Disorders

- Sleep Disorders

- Cancer Care

- Maternal and Fetal Health Monitoring

- Post-Acute and Post-Operative Care

- Elderly Care and Assisted Living

- Infectious Disease Monitoring

- Others

By End-User

- Hospitals and Health Systems

- Home Healthcare Settings

- Ambulatory Care Centers

- Long-Term Care Facilities and Nursing Homes

- Specialty Clinics

- Rehabilitation Centers

- Payers and Insurance Providers

- Research and Academic Institutions

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 31.45 B |

| Forecast Revenue (2034) | USD 96.85 B |

| CAGR (2025-2034) | 13.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product, (Vital Sign Monitoring Devices, Cardiac Monitoring Devices, Glucose Monitoring Devices, Neurological Monitoring Devices, Fetal and Maternal Monitoring Devices, Multiparameter Monitoring Devices, Weight Monitoring Devices, Remote Spirometers, Others), By Application, (Cardiovascular Diseases, Diabetes Management, Chronic Obstructive Pulmonary Disease (COPD), Hypertension Management, Neurological Disorders, Sleep Disorders, Cancer Care, Maternal and Fetal Health Monitoring, Post-Acute and Post-Operative Care, Elderly Care and Assisted Living, Infectious Disease Monitoring, Others), By End-User, (Hospitals and Health Systems, Home Healthcare Settings, Ambulatory Care Centers, Long-Term Care Facilities and Nursing Homes, Specialty Clinics, Rehabilitation Centers, Payers and Insurance Providers, Research and Academic Institutions, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ABBOTT LABORATORIES, DEXCOM, INC., MEDTRONIC PLC, KONINKLIJKE PHILIPS N.V., BOSTON SCIENTIFIC CORPORATION, MASIMO CORPORATION, GE HEALTHCARE, IRHYTHM TECHNOLOGIES, INC., OMRON HEALTHCARE, INC., RESMED INC., BIOTELEMETRY (PHILIPS), VITALCONNECT, INC., BIOTRICITY INC., WITHINGS, INSULET CORPORATION, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Cardiovascular Diseases, Diabetes Management, COPD, Hypertension, Neurological Disorders, Sleep Disorders, Cancer Care and Elderly Care), By End-User (Hospitals, Home Healthcare, Ambulatory Care Centers, Specialty Clinics and Nursing Homes) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Application (Cardiovascular Diseases, Diabetes Management, COPD, Hypertension, Neurological Disorders, Sleep Disorders, Cancer Care and Elderly Care), By End-User (Hospitals, Home Healthcare, Ambulatory Care Centers, Specialty Clinics and Nursing Homes) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Application (Cardiovascular Diseases, Diabetes Management, COPD, Hypertension, Neurological Disorders, Sleep Disorders, Cancer Care and Elderly Care), By End-User (Hospitals, Home Healthcare, Ambulatory Care Centers, Specialty Clinics and Nursing Homes) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Remote Patient Monitoring Devices Market?

The Global Remote Patient Monitoring Devices Market was valued at USD 27.76 Billion in 2024 and USD 31.45 Billion in 2025, and is projected to reach USD 96.85 Billion by 2034, growing at a CAGR of 13.3% from 2026 to 2034. Market growth is driven by the rising prevalence of chronic diseases, increasing telehealth adoption, and growing demand for continuous remote patient care.

Who are the major players in the Remote Patient Monitoring Devices Market?

ABBOTT LABORATORIES, DEXCOM, INC., MEDTRONIC PLC, KONINKLIJKE PHILIPS N.V., BOSTON SCIENTIFIC CORPORATION, MASIMO CORPORATION, GE HEALTHCARE, IRHYTHM TECHNOLOGIES, INC., OMRON HEALTHCARE, INC., RESMED INC., BIOTELEMETRY (PHILIPS), VITALCONNECT, INC., BIOTRICITY INC., WITHINGS, INSULET CORPORATION, Others

Which segments covered the Remote Patient Monitoring Devices Market?

By Product, (Vital Sign Monitoring Devices, Cardiac Monitoring Devices, Glucose Monitoring Devices, Neurological Monitoring Devices, Fetal and Maternal Monitoring Devices, Multiparameter Monitoring Devices, Weight Monitoring Devices, Remote Spirometers, Others), By Application, (Cardiovascular Diseases, Diabetes Management, Chronic Obstructive Pulmonary Disease (COPD), Hypertension Management, Neurological Disorders, Sleep Disorders, Cancer Care, Maternal and Fetal Health Monitoring, Post-Acute and Post-Operative Care, Elderly Care and Assisted Living, Infectious Disease Monitoring, Others), By End-User, (Hospitals and Health Systems, Home Healthcare Settings, Ambulatory Care Centers, Long-Term Care Facilities and Nursing Homes, Specialty Clinics, Rehabilitation Centers, Payers and Insurance Providers, Research and Academic Institutions, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Remote Patient Monitoring Devices Market

Published Date : 11 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date