- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Remote Work Security Platform Market Size, Share | CAGR 20.5%

Global Remote Work Security Platform Market Size, Share Analysis By Offering (Software, Managed Services, Professional, Risk Assessment, Monitoring, Incident Response), By Type (Endpoint, IAM, Zero Trust, Cloud, SASE, VPN, DLP, Email, SIEM), By Model (Fully Remote, Hybrid, WFH, BYOD, Distributed), By Vertical (BFSI, IT & Telecom, Healthcare, Government, Retail, Manufacturing, Education) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 62.8 Billion | USD 336.4 Billion | 20.5% | North America, 36.7% |

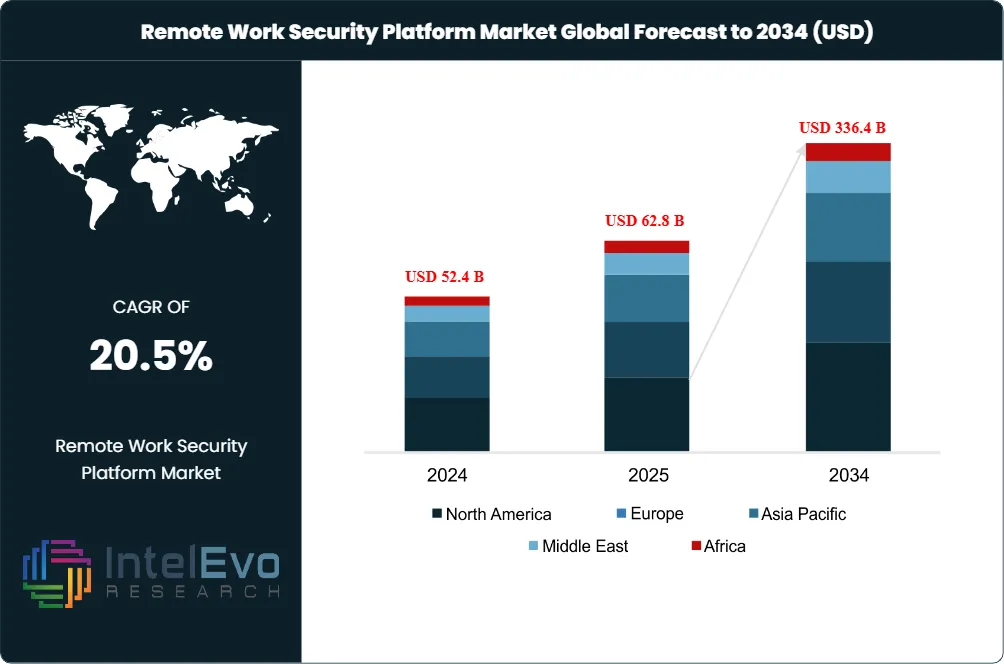

The Remote Work Security Platform Market was valued at USD 52.4 Billion in 2024 and USD 62.8 Billion in 2025. The market is projected to reach USD 336.4 Billion by 2034, expanding at a CAGR of 20.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 273.6 Billion over the analysis period, anchored by enterprise migration from legacy VPN architectures to cloud-delivered Zero Trust Network Access frameworks across hybrid workforces in North America, Europe, and Asia Pacific.

Get More Information about this report -

Request Free Sample ReportDemand expansion is driven by the persistence of distributed work models. According to Stanford WFH Research data referenced in early 2026, 58% of US knowledge workers operate remotely at least one day per week, while 32% of the US workforce remains fully remote. The IBM Cost of a Data Breach Report 2025 attributed an additional USD 1.07 Million per breach when remote work was a contributing factor, and Verizon DBIR data indicates 52% of 2025 security incidents involved a remote worker device or connection. These quantified loss figures have moved Zero Trust adoption from optional to budget-protected line item, with 63% of enterprises reporting Zero Trust as a strategic mandate in 2025.

Regulatory drivers reinforce the spend trajectory. The CISA Binding Operational Directive requires all US federal civilian agencies to implement Zero Trust Architecture by December 31, 2026, with internal applications restricted to identity-aware proxies by Q3 2026. The EU NIS2 Directive and Cyber Resilience Act extended mandatory cybersecurity controls across 18 critical sectors during 2025, while DORA enforcement for financial entities began January 17, 2025. SEC cyber-incident disclosure rules under Item 1.05 of Form 8-K continue to discipline corporate remote-access investment, since material breaches must be disclosed within four business days.

Technology consolidation is reshaping vendor positioning. Palo Alto Networks closed its USD 25 Billion acquisition of CyberArk on February 11, 2026, integrating privileged access management into Prisma SASE. CrowdStrike acquired SGNL on January 8, 2026 for USD 740 Million to extend continuous identity authorization across human, non-human, and AI agent identities. Zscaler reported FY 2025 ARR of USD 3.015 Billion and Q2 FY 2026 revenue growth of 26% year-over-year. Microsoft now operates a USD 37 Billion cybersecurity business, larger than CrowdStrike, Palo Alto Networks, and Zscaler combined, anchored by Defender, Entra, Purview, and Sentinel bundled into Microsoft 365 E5 contracts.

North America held the largest 2025 share at 36.7%, equating to USD 23.0 Billion in regional revenue, supported by federal Zero Trust mandates and concentrated enterprise spend. Asia Pacific is the fastest-growing region, projected at a 23.1% CAGR through the forecast period, driven by India's IT-services sector digitization and accelerated cloud migration in Japan, Singapore, and Australia. Europe demand is anchored by GDPR enforcement, NIS2, and sovereign-cloud requirements that favor in-region SASE control planes from Zscaler, Cato Networks, and Cisco. Forward-looking outlook through 2034 will be shaped by agentic AI security, non-human identity governance, browser-native runtime protection, and post-quantum cryptography readiness across remote-access stacks.

Market Definition & Scope

The Remote Work Security Platform Market is defined as the integrated portfolio of cloud-delivered and on-premises security technologies that protect users, devices, applications, and data across distributed workforces operating outside traditional corporate perimeters. The market encompasses Zero Trust Network Access, Secure Access Service Edge platforms, endpoint detection and response, identity and access management, secure web gateways, cloud access security brokers, data loss prevention, and managed security services tailored for hybrid and fully remote workforces.

This analysis covers solutions and services delivered to commercial, government, and educational organizations across all five global regions. Included are vendor revenues from subscription software, managed detection and response retainers, professional services tied to remote-access deployments, and hardware appliances configured for branch-to-cloud connectivity. Excluded are consumer antivirus products, generic IT operations software without security functions, traditional site-to-site VPN appliances sold for data-center interconnect, and standalone hardware token shipments. The market is a sub-segment of the global cybersecurity solutions market, which Cybersecurity Ventures estimated at approximately USD 248 Billion in 2026, giving Remote Work Security Platforms an approximate 25% share of total enterprise cybersecurity spend.

, By Type (Endpoint, IAM, Zero Trust, Cloud, SASE, VPN, DLP, Email, SIEM), By Model (Fully Remote, Hybrid, WFH, BYOD, Distributed), By Vertical (BFSI, IT & Telecom, Healthcare, Government, Retail, Manufacturing, Education) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Remote Work Security Platform Market grows from USD 62.8 Billion in 2025 to USD 336.4 Billion by 2034 at a 20.5% CAGR.

- Segment Dominance: The Solutions offering segment captured 65.0% of revenue in 2025, led by Zero Trust platforms, endpoint protection suites, and identity security.

- Segment Dominance: The Hybrid remote work model accounted for 56.0% of 2025 spending as enterprises maintained mixed in-office and home arrangements.

- Driver: Verizon DBIR data shows 52% of 2025 security incidents involved a remote worker device, and IBM reports breaches with remote work as a factor cost an additional USD 1.07 Million on average.

- Restraint: Vendor lock-in concerns and platform integration costs constrain SME adoption, with managed security services pricing averaging USD 18-32 per user per month for full SASE stacks.

- Opportunity: Non-human identity protection for AI agents represents a USD 4.5 Billion adjacent opportunity by 2030, given that 96% of organizations plan to expand AI agent deployments according to CrowdStrike customer surveys.

- Trend: Single-vendor SASE consolidation is accelerating, with Gartner projecting 60% of new SD-WAN purchases will be part of single-vendor SASE offerings by 2026.

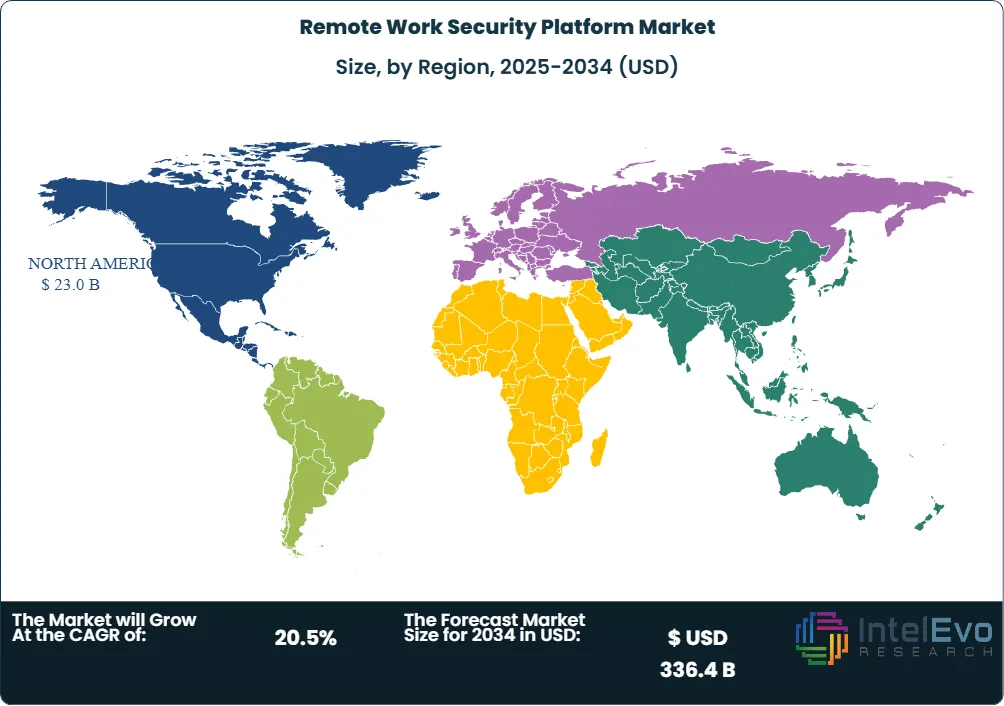

- Regional: North America led 2025 with a 36.7% share equivalent to USD 23.0 Billion, while Asia Pacific is the fastest-growing region at a projected 23.1% CAGR.

Key Insights Summary

- The Verizon Data Breach Investigations Report 2025 attributes 52% of security incidents to remote worker devices or connections, while phishing-initiated breaches increased 41% versus 2023 baselines.

- CrowdStrike Q4 FY 2026 financial results (March 2026) reported ending ARR of USD 5.3 Billion, up 24% year-over-year, with USD 331 Million in net new ARR contributed during the quarter.

- Zscaler Q2 FY 2026 results released February 26, 2026 showed revenue growth of 26% to USD 815.8 Million, with ARR growth of 25% year-over-year and FY 2026 ARR guidance raised to 24%.

- Palo Alto Networks closed its USD 25 Billion acquisition of CyberArk on February 11, 2026, the largest pure-play cybersecurity transaction recorded in 2025-2026.

- CISA Binding Operational Directive requires all US federal civilian agencies to complete Zero Trust Architecture implementation by December 31, 2026, with identity-aware proxies enforced for internal applications by Q3 2026.

- CrowdStrike data published in Q1 2026 indicates 91% of enterprises mandated multi-factor authentication for remote access in 2025, while 63% reported Zero Trust as their strategic security model.

- Microsoft's cybersecurity business reached USD 37 Billion in annual revenue in 2025, exceeding the combined revenue of CrowdStrike, Palo Alto Networks, and Zscaler within the same fiscal period.

Competitive Landscape Overview

The Remote Work Security Platform Market is moderately consolidated, with the top four vendors — Microsoft, Palo Alto Networks, Cisco Systems, and Zscaler — estimated to control approximately 38-42% of combined 2025 revenue based on disclosed cybersecurity-segment revenues. Competition is shifting from feature-by-feature differentiation to platform consolidation, with strategic acquirers absorbing identity, browser, and AI-security specialists. The Palo Alto Networks acquisition of CyberArk for USD 25 Billion (closed February 11, 2026) and ServiceNow's USD 7.75 Billion Armis acquisition signal that platform breadth now outweighs point-product depth as the buying criterion. Microsoft maintains a structural pricing advantage through Microsoft 365 E5 bundling, where Defender, Entra, Purview, and Sentinel are activated at minimal incremental cost. Pure-play vendors such as Zscaler and CrowdStrike compete through architectural depth in Zero Trust Exchange and Falcon platforms. Recent entrants including Cato Networks, Netskope, and 1Password are pressing into the mid-market through modular adoption pricing.

Competitive Landscape Matrix

| Company | Headquarters | Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Microsoft | USA | Leader | Defender, Entra, Purview, Sentinel | Global enterprise | Security Copilot Capacity Credits added to M365 E5, Jan 2026 |

| Palo Alto Networks | USA | Leader | Prisma SASE, Prisma Browser, Cortex XSIAM | North America, EMEA | Closed USD 25B CyberArk acquisition, Feb 2026 |

| Cisco Systems | USA | Leader | Cisco Secure Access, Umbrella, Duo, Splunk | Global enterprise | Integrated Splunk telemetry into Secure Access, 2025 |

| Zscaler | USA | Leader | Zero Trust Exchange, ZIA, ZPA | North America, APAC | Expanded data sovereignty platform, March 2026 |

| CrowdStrike | USA | Challenger | Falcon Identity Protection, Falcon Flex | North America, APAC | Acquired SGNL for USD 740M, Jan 2026 |

| Fortinet | USA | Challenger | FortiSASE, FortiClient, FortiGate | EMEA, APAC | Hotfix for FortiClient EMS zero-day CVE-2026-35616, Apr 2026 |

| Check Point | Israel | Challenger | Harmony SASE, Quantum SD-WAN | EMEA, APAC | Acquired Veriti exposure management, May 2025 |

| Cloudflare | USA | Challenger | Cloudflare One, Zero Trust | North America, EMEA | Expanded Zero Trust offering with browser isolation, 2025 |

| Netskope | USA | Niche | Netskope One SASE, SD-WAN | North America, EMEA | IPO filing as NTSK on NASDAQ, 2025 |

| Cato Networks | Israel | Niche | Cato SASE Cloud | Global | Launched modular SASE adoption model, March 2026 |

Segmentation Analysis

The Remote Work Security Platform Market is segmented across four dimensions: by offering, by security type, by remote work model, and by industry vertical. Cross-segment patterns indicate that Solutions on a Hybrid work model in BFSI verticals concentrate the largest single revenue pool, while Services attached to Cloud Security in Education represent the fastest-growing combination. Procurement leads benchmarking remote-access stacks should treat segment growth deltas as the primary input to vendor short-listing rather than headline market size.

By Offering

Solutions accounted for 65.0% of Remote Work Security Platform Market revenue in 2025, equivalent to USD 40.8 Billion, anchored by subscription software for Zero Trust Network Access, endpoint detection and response, secure web gateways, and identity governance. The dominance of Solutions reflects multi-year licensing commitments at platform vendors including Microsoft Defender, Palo Alto Prisma Access, Cisco Secure Access, and Zscaler Zero Trust Exchange. Microsoft 365 E5 bundling pulls Defender for Endpoint, Defender for Identity, and Sentinel into existing enterprise agreements at incremental cost, structurally compressing per-seat unit economics for competitors. Remote work security pricing benchmarks for full-stack SASE deployments range from USD 18 to USD 32 per user per month at enterprise scale, with discounts of 25-40% common on three-year platform commitments.

Services represented 35.0% of 2025 revenue at USD 22.0 Billion and is the faster-growing offering category, driven by managed security service providers serving small and mid-sized enterprises. CompTIA data shows 54% of organizations now outsource at least part of remote worker IT support to a managed service provider, and managed endpoint services reduce per-device management costs by 42% versus in-house teams. Professional services for SASE migration projects average USD 250,000 to USD 1.2 Million for enterprises with 5,000-25,000 endpoints, reflecting the policy-engineering effort required during VPN-to-ZTNA cutovers. Vendor-led co-managed offerings from Cisco Talos, Palo Alto Unit 42, and CrowdStrike Falcon Complete are capturing premium spend at the upper enterprise end.

By Security Type

Endpoint and IoT Security held the largest 2025 share at 33.4%, generating USD 21.0 Billion in revenue, anchored by CrowdStrike Falcon, Microsoft Defender for Endpoint, and SentinelOne Singularity. The proliferation of personal devices, contractor laptops, and unmanaged IoT assets behind home networks expanded endpoint attack surface materially after 2023. CrowdStrike disclosed Q4 FY 2026 ARR of USD 5.3 Billion and identity protection ARR of USD 435 Million as of mid-2025, indicating that endpoint vendors now derive growing revenue from identity-adjacent modules deployed on the same agent. The endpoint segment is benefiting from runtime browser protection extensions following CrowdStrike's Seraphic Security acquisition in early 2026.

Network Security captured approximately 27.0% of 2025 revenue at USD 17.0 Billion, while Cloud Security held 24.0% at USD 15.1 Billion and is projected to grow at the fastest CAGR within security types as SaaS workloads concentrate in Microsoft 365, Google Workspace, AWS, and Azure. Application Security and Identity Security captured the remaining 15.6%, with identity rising sharply after the Palo Alto Networks acquisition of CyberArk and CrowdStrike's USD 740 Million SGNL acquisition. Procurement teams evaluating remote work compliance requirements for SOC 2 Type II, ISO 27001, and FedRAMP Moderate should prioritize vendors holding current authorizations because re-authorization timelines materially extend implementation schedules.

By Remote Work Model

The Hybrid remote work model dominated 2025 with 56.0% of Remote Work Security Platform Market revenue at USD 35.2 Billion, reflecting enterprise standardization on 3.1 days in-office and 1.9 days remote schedules according to Gable workplace analytics. Hybrid environments require duplicated security policy enforcement across corporate networks and home connections, increasing per-seat platform spend versus single-mode deployments. The Fully Remote model represented 28.0% of 2025 revenue at USD 17.6 Billion and grows at a faster 21.3% CAGR, with digital-first organizations including GitLab, Automattic, and 1Password operating without central offices. The Temporary Remote segment, covering business continuity and contingent workforce scenarios, captured the remaining 16.0% and is increasingly bundled into broader hybrid licensing.

By Industry Vertical

BFSI accounted for the largest 2025 vertical share at approximately 23.0% of Remote Work Security Platform Market revenue, equivalent to USD 14.4 Billion, driven by DORA compliance for European financial entities effective January 17, 2025 and SEC cyber-disclosure rules. Financial institutions including JPMorgan Chase, HSBC, Goldman Sachs, and DBS Bank deploy multi-vendor stacks combining Microsoft Defender, CrowdStrike Falcon, and Zscaler Zero Trust Exchange. IT and ITeS represented 19.0% of revenue at USD 11.9 Billion, reflecting concentrated demand from offshore service exporters across India, the Philippines, and Eastern Europe. Education is the fastest-growing vertical at an estimated 24.5% CAGR through 2034, propelled by hybrid learning platforms and FERPA-driven student data protection. Government, Healthcare, Retail, and Manufacturing represent the remaining segment combining for 33.6% of 2025 revenue, with Healthcare adoption accelerating after HIPAA enforcement actions averaged USD 1.5 Million in 2024-2025 settlements.

Regional Analysis

The Remote Work Security Platform Market spans five regions, with North America, Europe, and Asia Pacific accounting for approximately 87% of 2025 revenue. Regional growth differentials are driven by federal mandates, sovereign data requirements, and cloud-migration timing. Procurement leads should map vendor regional points-of-presence to data-residency obligations before signing multi-year agreements.

North America held 36.7% of the Remote Work Security Platform Market in 2025 at USD 23.0 Billion, anchored by the United States, Canada, and Mexico. The CISA Binding Operational Directive requiring federal Zero Trust by December 31, 2026 has activated multi-billion-dollar federal procurement cycles benefiting Zscaler, Palo Alto Networks, and Cisco. The US federal cybersecurity market is estimated at USD 25 Billion in 2025 by Palo Alto Networks, with Deltek projecting USD 18.8 Billion in 2026 and USD 20.7 Billion by 2028. Canada has expanded its Canadian Centre for Cyber Security advisories on industrial control system threats during October 2025, increasing federal and critical-infrastructure spend. State-level data privacy laws including the California Consumer Privacy Act, Virginia Consumer Data Protection Act, and Colorado Privacy Act extend remote-work compliance scope.

Europe represented approximately 27.0% of 2025 Remote Work Security Platform Market revenue at USD 17.0 Billion, with Germany, the United Kingdom, France, and the Netherlands as primary demand pools. The NIS2 Directive transposition completed across 18 critical-infrastructure sectors during 2024-2025, with maximum administrative fines of EUR 10 Million or 2% of global turnover for essential entities. The EU AI Act, effective in phases from 2025, creates incremental compliance scope for AI-augmented security platforms. Sovereign-cloud requirements drive demand for in-region SASE control planes from Zscaler, Cato Networks, and Cisco, particularly in Germany where 60% of companies operate permanent hybrid models. The UK Online Safety Act and Cyber Security and Resilience Bill expand remote-access governance for service providers.

Asia Pacific captured approximately 24.0% of 2025 revenue at USD 15.1 Billion and is the fastest-growing region at a projected 23.1% CAGR. India led regional revenue, supported by USD 245 Billion in IT-services exports during FY 2025 and accelerating digitization under the Digital India initiative. Japan's METI and Personal Information Protection Commission expanded cyber-resilience requirements during 2025, while Singapore's Cyber Security Agency enforced revised Cybersecurity Code of Practice in early 2026. Australian Signals Directorate Essential Eight controls remain mandatory for Australian Government entities and influence private-sector procurement. China's enterprise spend is concentrated in domestic vendors including Qi An Xin and Topsec, with foreign vendor share constrained by data-export restrictions under the Data Security Law and Personal Information Protection Law.

Latin America accounted for approximately 7.0% of 2025 Remote Work Security Platform Market revenue at USD 4.4 Billion, with Brazil and Mexico as primary markets. Brazilian LGPD enforcement and Mexico's LFPDPPP framework drive enterprise spend, while ransomware incident frequency targeting financial services in Argentina, Chile, and Colombia accelerates managed detection and response adoption. Middle East and Africa contributed approximately 5.3% at USD 3.3 Billion, with the United Arab Emirates Cybersecurity Council and Saudi Arabia's National Cybersecurity Authority anchoring Gulf Cooperation Council spend. The UAE Federal Decree-Law 45 of 2021 on Personal Data Protection and Saudi Arabia's Personal Data Protection Law create remote-access compliance scope. South African POPIA enforcement and Kenya's Data Protection Act 2019 sustain southern and eastern African momentum.

Country Analysis

The Remote Work Security Platform Market exhibits sharp country-level variation driven by federal mandates, vertical concentration, and cloud-migration timing. Procurement leads operating multi-country deployments should sequence rollouts by regulatory complexity rather than employee headcount.

United States: The US Remote Work Security Platform Market reached USD 19.5 Billion in 2025, representing approximately 31% of global revenue, and is projected to grow at a 20.8% CAGR through 2034. Demand is anchored by the CISA Binding Operational Directive on Zero Trust, the OMB M-22-09 Federal Zero Trust Strategy, and FedRAMP authorization requirements for cloud-delivered SASE. Federal civilian agencies must implement identity-aware proxies for internal applications by Q3 2026, channeling procurement toward FedRAMP-High authorized vendors including Zscaler and Palo Alto Prisma Access. The US Department of Defense Zero Trust Reference Architecture v2.0 and the NIST SP 800-207 framework establish technical baselines that influence private-sector procurement decisions. State-level disclosure laws and the SEC Item 1.05 cyber-incident rule discipline corporate spending.

Germany: The German Remote Work Security Platform Market reached approximately USD 5.2 Billion in 2025 with a projected CAGR of 19.2% through 2034, anchored by enterprise hybrid-work standardization in manufacturing, automotive, and finance. Over 60% of German companies operate permanent hybrid models, driving sustained demand for ZTNA and endpoint protection from SAP, Siemens, Deutsche Bank, and Volkswagen. The BSI IT-Grundschutz catalog and the NIS2 transposition into German law during 2024 created compliance obligations across 18 sectors. Federal Office for Information Security cyber-resilience guidance and BaFin financial-sector requirements channel spend toward GDPR-compliant solutions with localized data residency.

India: The Indian Remote Work Security Platform Market reached approximately USD 2.4 Billion in 2025 with a projected CAGR of 26.3%, the fastest among the country group analyzed, driven by accelerated digitization and the Digital Personal Data Protection Act 2023 enforcement. The Computer Emergency Response Team India directives on cyber-incident reporting within six hours and the CERT-In SBOM mandate effective from 2024 increased compliance scope. IT-services exporters Tata Consultancy Services, Infosys, Wipro, and HCLTech operate global remote-delivery centers requiring SASE platforms across 50-plus countries. The Reserve Bank of India cyber-resilience framework for banks and the SEBI Cybersecurity and Cyber Resilience Framework released in August 2024 sustain BFSI demand.

United Kingdom: The UK Remote Work Security Platform Market reached approximately USD 3.4 Billion in 2025 with a projected CAGR of 19.6%, anchored by financial-services concentration in London and the Cyber Security and Resilience Bill expanding NIS Regulations during 2025. The Information Commissioner's Office enforcement of UK GDPR and the Online Safety Act 2023 implementation through 2024-2025 drive remote-access governance investment. The National Cyber Security Centre Cyber Assessment Framework and the Financial Conduct Authority operational resilience rules apply across BFSI deployments, channeling spend toward platforms with FCA-aligned audit trails.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Offering

- Software Solutions

- Security Services

- Managed Security Services

- Professional Security Services

- Consulting and Risk Assessment Services

- Implementation and Integration Services

- Training and Awareness Solutions

- Security Monitoring and Incident Response Services

- Others

By Security Type

- Endpoint Security

- Identity and Access Management (IAM)

- Zero Trust Security

- Cloud Security

- Secure Access Service Edge (SASE)

- Virtual Private Network (VPN) Security

- Data Loss Prevention (DLP)

- Email Security

- Network Security

- Multi-Factor Authentication (MFA)

- Security Information and Event Management (SIEM)

- Threat Detection and Response

- Others

By Remote Work Model

- Fully Remote Workforce

- Hybrid Workforce

- Work-from-Home (WFH) Model

- Bring Your Own Device (BYOD) Workforce

- Remote Contract and Freelance Workforce

- Distributed Global Workforce

- Field Workforce Operations

- Others

By Industry Vertical

- Banking, Financial Services, and Insurance (BFSI)

- Information Technology and Telecommunications

- Healthcare and Life Sciences

- Government and Public Sector

- Retail and E-Commerce

- Manufacturing

- Education

- Energy and Utilities

- Media and Entertainment

- Transportation and Logistics

- Professional Services

- Hospitality and Travel

- Aerospace and Defense

- Consumer Goods

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 62.8 B |

| Forecast Revenue (2034) | USD 336.4 B |

| CAGR (2025-2034) | 20.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Software Solutions, Security Services, Managed Security Services, Professional Security Services, Consulting and Risk Assessment Services, Implementation and Integration Services, Training and Awareness Solutions, Security Monitoring and Incident Response Services, Others), By Security Type, (Endpoint Security, Identity and Access Management (IAM), Zero Trust Security, Cloud Security, Secure Access Service Edge (SASE), Virtual Private Network (VPN) Security, Data Loss Prevention (DLP), Email Security, Network Security, Multi-Factor Authentication (MFA), Security Information and Event Management (SIEM), Threat Detection and Response, Others), By Remote Work Model, (Fully Remote Workforce, Hybrid Workforce, Work-from-Home (WFH) Model, Bring Your Own Device (BYOD) Workforce, Remote Contract and Freelance Workforce, Distributed Global Workforce, Field Workforce Operations, Others), By Industry Vertical, (Banking, Financial Services, and Insurance (BFSI), Information Technology and Telecommunications, Healthcare and Life Sciences, Government and Public Sector, Retail and E-Commerce, Manufacturing, Education, Energy and Utilities, Media and Entertainment, Transportation and Logistics, Professional Services, Hospitality and Travel, Aerospace and Defense, Consumer Goods, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT CORPORATION, PALO ALTO NETWORKS INC., CISCO SYSTEMS INC., ZSCALER INC., CROWDSTRIKE HOLDINGS INC., FORTINET INC., CHECK POINT SOFTWARE TECHNOLOGIES LTD., CLOUDFLARE INC., BROADCOM INC., INTERNATIONAL BUSINESS MACHINES CORPORATION, OKTA INC., NETSKOPE INC., CATO NETWORKS, SOPHOS LTD., PROOFPOINT INC., SENTINELONE INC., TREND MICRO INCORPORATED, FORCEPOINT LLC, 1PASSWORD, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Type (Endpoint, IAM, Zero Trust, Cloud, SASE, VPN, DLP, Email, SIEM), By Model (Fully Remote, Hybrid, WFH, BYOD, Distributed), By Vertical (BFSI, IT & Telecom, Healthcare, Government, Retail, Manufacturing, Education) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Type (Endpoint, IAM, Zero Trust, Cloud, SASE, VPN, DLP, Email, SIEM), By Model (Fully Remote, Hybrid, WFH, BYOD, Distributed), By Vertical (BFSI, IT & Telecom, Healthcare, Government, Retail, Manufacturing, Education) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Type (Endpoint, IAM, Zero Trust, Cloud, SASE, VPN, DLP, Email, SIEM), By Model (Fully Remote, Hybrid, WFH, BYOD, Distributed), By Vertical (BFSI, IT & Telecom, Healthcare, Government, Retail, Manufacturing, Education) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Remote Work Security Platform Market?

The Global Remote Work Security Platform Market was valued at USD 52.4 Billion in 2024 and USD 62.8 Billion in 2025, and is projected to reach USD 336.4 Billion by 2034, growing at a CAGR of 20.5% from 2026 to 2034. Market growth is driven by remote work adoption, zero-trust security, cloud security, and rising cyber threats.

Who are the major players in the Remote Work Security Platform Market?

MICROSOFT CORPORATION, PALO ALTO NETWORKS INC., CISCO SYSTEMS INC., ZSCALER INC., CROWDSTRIKE HOLDINGS INC., FORTINET INC., CHECK POINT SOFTWARE TECHNOLOGIES LTD., CLOUDFLARE INC., BROADCOM INC., INTERNATIONAL BUSINESS MACHINES CORPORATION, OKTA INC., NETSKOPE INC., CATO NETWORKS, SOPHOS LTD., PROOFPOINT INC., SENTINELONE INC., TREND MICRO INCORPORATED, FORCEPOINT LLC, 1PASSWORD, Others

Which segments covered the Remote Work Security Platform Market?

By Offering, (Software Solutions, Security Services, Managed Security Services, Professional Security Services, Consulting and Risk Assessment Services, Implementation and Integration Services, Training and Awareness Solutions, Security Monitoring and Incident Response Services, Others), By Security Type, (Endpoint Security, Identity and Access Management (IAM), Zero Trust Security, Cloud Security, Secure Access Service Edge (SASE), Virtual Private Network (VPN) Security, Data Loss Prevention (DLP), Email Security, Network Security, Multi-Factor Authentication (MFA), Security Information and Event Management (SIEM), Threat Detection and Response, Others), By Remote Work Model, (Fully Remote Workforce, Hybrid Workforce, Work-from-Home (WFH) Model, Bring Your Own Device (BYOD) Workforce, Remote Contract and Freelance Workforce, Distributed Global Workforce, Field Workforce Operations, Others), By Industry Vertical, (Banking, Financial Services, and Insurance (BFSI), Information Technology and Telecommunications, Healthcare and Life Sciences, Government and Public Sector, Retail and E-Commerce, Manufacturing, Education, Energy and Utilities, Media and Entertainment, Transportation and Logistics, Professional Services, Hospitality and Travel, Aerospace and Defense, Consumer Goods, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Remote Work Security Platform Market

Published Date : 24 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date