- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Reservoir Simulation Software Market Size, Share & Growth | CAGR 10.7%

Global Reservoir Simulation Software Market Size, Share, Analysis By Deployment (On-Premise, Cloud and Hybrid), By Reservoir Type (Conventional Oil & Gas Reservoirs, Unconventional & Tight Reservoirs, Offshore Deepwater Reservoirs, CCUS, Geothermal & Underground Storage), By Application (Field Development Planning, Production Optimization & EOR, Reserve Estimation & History Matching, Carbon Storage & Geothermal Modeling), By End-User (IOCs & NOCs, Oilfield Services & EPCs, Research Institutes, Energy Transition Developers) Industry Region & Key Players – Market Dynamics, Competitive Strategies & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 2.75 Billion, 2025 | USD 6.87 Billion, 2034 | 10.7%, 2026–2034 | North America, 36.5%, 2025 |

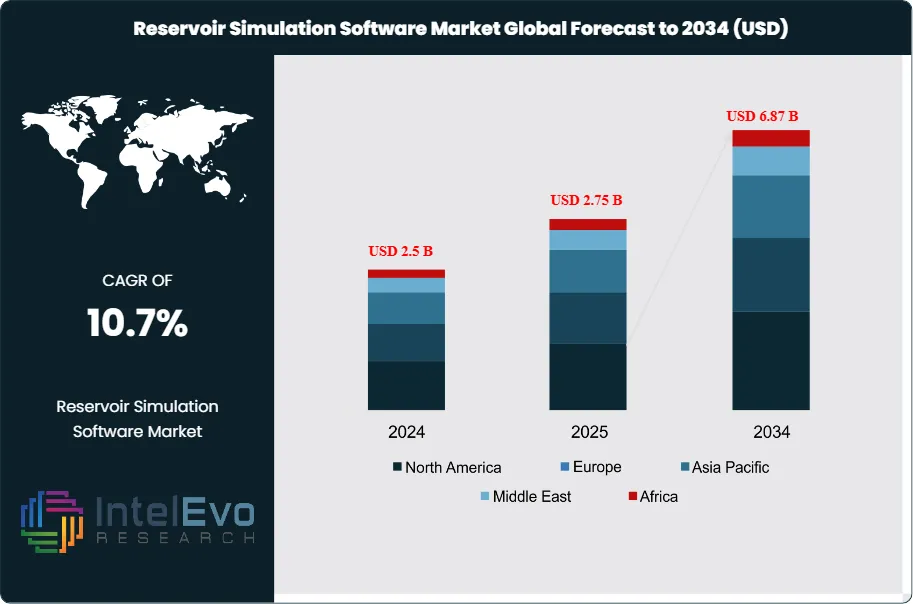

The Reservoir Simulation Software Market was valued at approximately USD 2.5 Billion in 2024 and increased to USD 2.75 Billion in 2025. The market is projected to reach nearly USD 6.87 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 10.7% during the forecast period from 2026 to 2034. The CAGR is mathematically consistent over nine years. The Reservoir Simulation Software Market is expanding because upstream operators, national oil companies, and subsurface teams are under pressure to improve recovery, shorten planning cycles, and model more complex reservoirs with greater speed and accuracy. Public market tracking already places the market at USD 2.75 Billion in 2025, while broader digital oilfield spending also shows software-led growth across upstream operations.

Get More Information about this report -

Request Free Sample ReportThe Reservoir Simulation Software Market is no longer tied only to conventional oilfield planning. It now sits inside a wider subsurface software stack that supports field development, production optimization, enhanced oil recovery, carbon storage, underground hydrogen storage, and geothermal workflows. SLB's Intersect 2025.1 release added faster embedded discrete fracture modeling and underground hydrogen storage functionality. AspenTech positions its subsurface suite across hydrocarbon, geothermal, and carbon projects. SPE's 2025 Reservoir Simulation Conference also framed the technology around AI, high-performance computing, and the energy transition. That shift is widening the software addressable market beyond legacy reservoir engineering use cases.

Demand in the Reservoir Simulation Software Market is supported by three structural drivers. First, reservoir complexity is rising as operators work deeper offshore fields, tighter unconventional assets, and more mature brownfields. Second, digital oilfield budgets continue to favor software, with software holding 44.53% of digital transformation spending in oil and gas in 2025 and upstream operations accounting for 38.81% of that market. Third, AI adoption inside reservoir engineering is moving into mainstream use. A 2025 comparative survey found AI adoption among U.S.-based reservoir engineers rose from 43% in 2024 to 56% in 2025, while hybrid AI approaches reached 53% and reported the best success rates. Those numbers directly support higher spending on simulation platforms with automation, data integration, and rapid forecasting capability.

Competition in the Reservoir Simulation Software Market is moderately consolidated. SLB, Halliburton, CMG, and AspenTech hold the strongest positions because they combine simulators with broader geoscience and engineering workflows. Competitive intensity increased through 2025-2026. SLB expanded Petrel deployment with Shell in April 2025 and bought Stimline Digital in August 2025. Halliburton signed a subsurface modeling and reservoir management collaboration with PETRONAS in June 2025. CMG acquired SeisWare in July 2025 and signed a global multi-year licensing agreement in November 2025. Baker Hughes also expanded digital integration with CMG in June 2025. The main risks are slower upstream software budgets during price weakness, long enterprise sales cycles, and customer caution around data migration, model validation, and cloud security. Regionally, North America leads spending, Europe remains strong in offshore and CCS-linked modeling, Asia Pacific is rising through national oil companies and gas projects, and the Middle East is gaining through giant field management and digital transformation programs.

, By Reservoir Type (Conventional Oil & Gas Reservoirs, Unconventional & Tight Reservoirs, Offshore Deepwater Reservoirs, CCUS, Geothermal & Underground Storage), By Application (Field Development Planning, Production Optimization & EOR, Reserve Estimation & History Matching, Carbon Storage & Geothermal Modeling), By End-User (IOCs & NOCs, Oilfield Services & EPCs, Research Institutes, Energy Transition Developers) Industry Region & Key Players – Market Dynamics, Competitive Strategies & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Reservoir Simulation Software Market was worth USD 2.75 Billion in 2025 and is projected to reach USD 6.87 Billion by 2034 at a 10.7% CAGR over 2026-2034.

- Segment Dominance: On-premise software remained the largest delivery segment with an estimated 58.0% share in 2025, equal to about USD 1.60 Billion, 2025, because large operators still keep high-performance simulation and proprietary subsurface data inside controlled enterprise environments.

- Segment Dominance: Field development planning led by application with an estimated 34.0% share in 2025, equal to about USD 0.94 Billion, 2025, because simulation remains central to well placement, recovery forecasting, and development scenario ranking.

- Driver: The main driver is the widening use of digital subsurface workflows. In oil and gas digital transformation spending, software held 44.53% share in 2025 and upstream operations accounted for 38.81% of spending.

- Restraint: The main restraint is budget concentration and long enterprise buying cycles. Even with software growth, upstream oil investment is expected to fall 6.0% in 2025, which can delay large platform replacement decisions and new enterprise licenses.

- Opportunity: The strongest opportunity is in carbon storage, hydrogen storage, and geothermal modeling. SLB's Intersect 2025.1 added underground hydrogen storage capabilities, and AspenTech explicitly markets its subsurface platform for hydrocarbon, geothermal, and carbon projects.

- Trend: AI-enabled modeling is the dominant trend. AI adoption among surveyed U.S. reservoir engineers rose from 43% in 2024 to 56% in 2025, and hybrid AI approaches rose to 53% with the highest reported success rates.

- Regional Analysis: North America led the Reservoir Simulation Software Market with an estimated 36.5% share in 2025, equal to about USD 1.00 Billion, 2025, supported by the largest upstream software base, shale modeling intensity, and strong vendor presence.

Competitive Summary

The Reservoir Simulation Software Market is moderately consolidated. The top four suppliers, SLB, Halliburton, CMG, and AspenTech, held an estimated 62.0% of 2025 market revenue. Competition is mainly technology-driven and platform-based. Leaders win through simulator physics, high-performance computing, cloud delivery, AI features, and broader subsurface workflow integration. Competitive intensity increased through 2025-2026 with SLB's Shell partnership and Stimline Digital acquisition, Halliburton's PETRONAS collaboration, CMG's SeisWare acquisition, and ongoing product releases from tNavigator and Kongsberg Digital.

Competitive Landscape Matrix

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | US | Leader | Intersect reservoir simulator | North America, Middle East, Europe | Expanded Petrel deployment with Shell in Apr 2025 and acquired Stimline Digital in Aug 2025 |

| Halliburton | US | Leader | DecisionSpace 365 Unified Ensemble Modeling | North America, Asia Pacific, Middle East | Signed a strategic collaboration with PETRONAS in Jun 2025 to deploy next-generation subsurface modeling tools |

| CMG | Canada | Leader | CMG IMEX / GEM / STARS and CoFlow | North America, Middle East, Latin America | Acquired SeisWare in Jul 2025 and signed a global multi-year simulation licensing agreement in Nov 2025 |

| AspenTech | US | Leader | Aspen RMS and Aspen Tempest | Europe, North America, Middle East | Continued rollout of AspenTech V15 in May 2025 across industrial AI and subsurface workflows |

| Baker Hughes | US | Challenger | JewelSuite Subsurface Modeling | Middle East, Latin America, Asia Pacific | Announced a digital integration agreement with CMG in Jun 2025 and expanded Leucipa deployment in Jan 2026 |

| Emerson | US | Challenger | Roxar RMS reservoir modeling | Europe, Middle East | Continued subsurface software transition into AspenTech SSE portfolio while maintaining RMS market relevance in 2025 |

| Rock Flow Dynamics | UK | Challenger | tNavigator | Europe, Middle East, Asia Pacific | Released tNavigator 25.2 in Jul 2025 and 25.4 in Jan 2026 with AI assistant, GPU, and automation upgrades |

| Kongsberg Digital | Norway | Niche Player | LedaFlow | Europe, Middle East | Released LedaFlow 2.13 in Jan 2026 and continued coupling development with CMG GEM for CO2 storage workflows |

| ResFrac Corporation | US | Niche Player | ResFracPro | North America | Continued commercial expansion of integrated hydraulic fracture and reservoir simulation workflows through 2025 technical releases |

| Seequent | New Zealand | Niche Player | Leapfrog Energy | Asia Pacific, Europe | Expanded geothermal and subsurface modeling use cases through 2025 energy transition workflow positioning |

By Deployment

On-Premise. On-premise software held an estimated 58.0% share of the Reservoir Simulation Software Market in 2025, equal to about USD 1.60 Billion, 2025. The segment remains dominant because large operators, national oil companies, and supermajors still run high-value subsurface models inside tightly governed IT environments. Reservoir simulation involves proprietary geoscience data, asset-level economics, reserve estimates, and development plans. Many customers still prefer local clusters, dedicated high-performance computing, or private infrastructure for those workflows. Halliburton's DecisionSpace 365 messaging highlights public, private, and hybrid cloud options, which implies that hybrid and controlled environments remain critical for customers not ready to move entire simulation stacks into public cloud. OSDU activity also shows that the industry is still standardizing data exchange for dynamic reservoir modeling, which supports a gradual rather than abrupt shift to full cloud-native deployment. Competitive strength in on-premise remains highest among SLB, Halliburton, CMG, and AspenTech because they have deeper enterprise integration, long installed bases, and proven support for large physics-heavy models. The segment will stay large through 2034, but its share will decline as cloud and hybrid delivery models gain traction in faster-turn planning, collaborative workflows, and energy transition projects.

Cloud and Hybrid. Cloud and hybrid deployment accounted for an estimated 42.0% share in 2025, equal to about USD 1.16 Billion, 2025. This segment is expanding faster because operators want broader model sharing, easier collaboration across geoscience and reservoir teams, and better access to elastic compute for history matching, uncertainty studies, and ensemble workflows. Halliburton's PETRONAS collaboration specifically references DecisionSpace 365 and Unified Ensemble Modeling, which highlights customer demand for integrated, remotely accessible modeling environments. AspenTech also emphasizes open data exchange and OSDU-connected workflows. SLB continues to scale digital subsurface tools across large global asset portfolios, and its Shell partnership reinforces the case for enterprise-wide digital deployment. Cloud and hybrid models are especially attractive for carbon storage screening, geothermal opportunity ranking, and rapid scenario evaluation, where collaboration matters as much as raw compute. The segment will likely be the fastest-growing delivery category through 2034 because it lowers infrastructure friction for new users and allows software vendors to bundle simulation with broader digital services. Growth, however, still depends on cybersecurity confidence, data sovereignty rules, and customer willingness to move critical reservoir models into shared digital environments.

By Reservoir Type

Conventional Oil and Gas Reservoirs. Conventional oil and gas reservoirs represented the largest reservoir-type segment with an estimated 49.0% share in 2025, equal to about USD 1.35 Billion, 2025. This segment remains dominant because the installed base is huge and because national oil companies and integrated majors still rely on simulation to manage pressure depletion, waterflooding, reserve booking, recovery factor planning, and brownfield development. Conventional assets also generate repeat demand because models must be updated continuously as field conditions change. Most leading commercial simulators, including Intersect, CMG suites, Aspen Tempest-linked workflows, and DecisionSpace, were originally built around these use cases. Competitive intensity is highest here because the segment contains the longest-standing enterprise contracts and the greatest concentration of experienced users. Although growth is slower than in newer energy transition applications, conventional oil and gas will remain the core revenue base of the Reservoir Simulation Software Market through 2034 because operators continue to spend heavily on field-life extension and recovery improvement across large producing assets.

Unconventional and Tight Reservoirs. Unconventional and tight reservoirs accounted for an estimated 23.0% share in 2025, or about USD 0.63 Billion, 2025. This segment is highly technical and strongly tied to North American shale and selected Middle East gas developments. It is important because unconventional assets demand tighter coupling between geomechanics, fracture behavior, production forecasting, and development spacing analysis. ResFrac's positioning around fully integrated hydraulic fracture and reservoir simulation speaks directly to this niche, while SLB and Baker Hughes also support fracture-sensitive modeling through broader digital and subsurface platforms. Competitive advantage comes from speed, data integration, and the ability to model many scenarios quickly rather than from static model quality alone. The segment should grow faster than conventional modeling through 2034 in percentage terms, especially where shale gas and tight reservoir development expands. Still, it will remain smaller in absolute revenue than conventional reservoirs because the global installed base of conventional assets is much larger.

Offshore Deepwater Reservoirs. Offshore deepwater reservoirs held an estimated 17.0% share in 2025, equal to about USD 0.47 Billion, 2025. Offshore deepwater modeling generates high software value per asset because well count is smaller, but project economics are more sensitive to reservoir uncertainty, well placement, pressure support, and facility constraints. Europe, Brazil, the U.S. Gulf, West Africa, and Australia drive this demand. Halliburton's PETRONAS collaboration and AspenTech's production optimization positioning show how deepwater customers increasingly want integrated subsurface and surface workflows rather than isolated simulation runs. This segment tends to favor established enterprise vendors because offshore projects need validated physics, reliability, and close workflow integration across multiple teams. Growth is supported by brownfield optimization and pre-FID screening of new offshore developments, but budget cycles and project sanction delays can slow software expansion in any given year.

CCUS, Geothermal, and Underground Storage. CCUS, geothermal, and underground storage represented an estimated 11.0% share in 2025, equal to about USD 0.30 Billion, 2025. This is the smallest segment today, but it is the fastest structural growth pocket in the Reservoir Simulation Software Market. SPE's 2025 reservoir simulation coverage highlighted CCS development, AspenTech markets its suite for geothermal and carbon projects, and SLB's Intersect 2025.1 release added hydrogen storage and biochemical reaction modeling. Kongsberg's LedaFlow-GEM link also targets CO2 transport and storage workflows. This segment is expanding because subsurface energy transition projects need the same core capabilities as hydrocarbon modeling, but with new physics, risk questions, and regulatory reporting needs. The segment will gain share steadily through 2034 as carbon storage screening, monitoring design, geothermal resource evaluation, and underground hydrogen storage move from pilot to commercial scale.

By Application

Field Development Planning. Field development planning was the largest application segment with an estimated 34.0% share in 2025, equal to about USD 0.94 Billion, 2025. This segment leads because reservoir simulation remains central to well placement, drainage strategy, facility sizing, development sequencing, and recovery scenario selection. SLB describes Intersect as reservoir simulation technology for today's most complex subsurface challenges, while AspenTech defines reservoir modeling in terms of reserve estimation, field development, and future production prediction. Halliburton's PETRONAS collaboration also explicitly connects subsurface modeling with accelerated time to first oil. Competitive strength is strongest among full-platform vendors because customers want development planning tied to geoscience, economics, and uncertainty analysis rather than a single stand-alone simulator. The segment will remain the largest through 2034 because every new field and many brownfield expansions still require model-driven development choices before capital is committed.

Production Optimization and EOR. Production optimization and EOR accounted for an estimated 30.0% share in 2025, or about USD 0.83 Billion, 2025. This segment covers history matching, waterflood design, pressure support, infill planning, intervention targeting, and forecast refinement in producing fields. It benefits from mature-field pressure, because operators are trying to recover more value from existing assets rather than only sanctioning new drilling. Baker Hughes' Leucipa reservoir management positioning and Aspen Tempest's production optimization language fit this demand directly. The segment also benefits from AI adoption because optimization workflows are more repetitive and data rich than greenfield model building, making them ideal for automation and ensemble methods. Demand is broad across conventional oil, offshore waterflood assets, and selected unconventional plays. Revenue growth should stay strong through 2034 as operators continue to prioritize production uplift, higher recovery factor, and lower decision cycle time.

Reserve Estimation and History Matching. Reserve estimation and history matching represented an estimated 21.0% share in 2025, equal to about USD 0.58 Billion, 2025. This segment remains important because reserve estimation, forecast confidence, and uncertainty reduction underpin both capital allocation and regulatory reporting. It is less visible commercially than field development planning, but it sits at the center of how operators decide where to spend and how to communicate asset quality internally. Halliburton's Unified Ensemble Modeling and CMG's long-standing strength in advanced simulation both support this use case well. The segment benefits from higher-performance computing and more automated ensemble workflows, but it also faces customer caution because reserve-related models often require strong validation and careful governance. Growth will remain healthy through 2034, though slightly below the pace of production optimization and energy transition use cases.

Carbon Storage and Geothermal Modeling. Carbon storage and geothermal modeling held an estimated 15.0% share in 2025, or about USD 0.41 Billion, 2025. This segment is smaller today, but it is increasingly strategic because governments, utilities, energy companies, and subsurface teams need simulation to assess injectivity, containment risk, pressure buildup, thermal behavior, and long-term storage performance. SPE's 2025 coverage framed cost-effective reservoir simulation as a tool for CCS development, and AspenTech and SLB now market subsurface tools explicitly for carbon and geothermal applications. The segment also benefits from users outside traditional upstream oil and gas, which broadens the customer base for simulation vendors. Through 2034, this segment should record one of the fastest growth rates in the entire market, especially in Europe, North America, and Asia Pacific where policy, decarbonization goals, and geothermal interest are building.

By End User

Integrated Oil Companies and National Oil Companies. Integrated oil companies and national oil companies held the largest end-user share at an estimated 46.0% in 2025, equal to about USD 1.27 Billion, 2025. This group dominates because it controls the largest producing asset bases, the biggest brownfield portfolios, and the most complex offshore and giant field projects. These customers also buy software at enterprise scale and typically need long-term support, training, model governance, and integration with other subsurface systems. SLB's Shell partnership and Halliburton's PETRONAS collaboration illustrate how leading vendors still win their most important contracts through large operator relationships. The segment will remain dominant through 2034 because big operators continue to drive the highest-value simulation spend across development planning, reserve management, and digital field operations.

Oilfield Service Companies, EPCs, and Consulting Firms. Oilfield service companies, EPCs, and consulting firms accounted for an estimated 28.0% share in 2025, or about USD 0.77 Billion, 2025. This group uses simulation software to support studies, integrated projects, production optimization, field development consulting, and technical service delivery. Baker Hughes' and CMG's 2025 integration agreement highlights how software vendors increasingly collaborate with broader technical service ecosystems. This segment is important because it expands software reach beyond asset owners and supports project-based licensing, consulting-led implementation, and niche technical workflows. Growth is solid, but the segment remains smaller than operator demand because many service firms license only selected modules or specific workflows.

Research Institutes and Academia. Research institutes and academia represented an estimated 14.0% share in 2025, equal to about USD 0.39 Billion, 2025. This segment stays relevant because reservoir simulation is heavily research driven and because universities, public institutes, and technical centers train the next generation of reservoir engineers and modelers. Baker Hughes' JewelSuite package deployment at Curtin Malaysia in 2025 shows how academic access remains a pipeline for future commercial adoption. The segment is smaller in revenue terms, but it matters strategically because new workflows in unconventionals, CCS, geothermal, and uncertainty methods often emerge here first.

CCUS, Geothermal, and Energy Transition Developers. CCUS, geothermal, and energy transition developers held an estimated 12.0% share in 2025, equal to about USD 0.33 Billion, 2025. This segment is still early, but it is gaining importance as simulation tools spread beyond traditional hydrocarbon producers. AspenTech, SLB, Kongsberg, and tNavigator all now position parts of their offering around carbon storage, geothermal, or underground storage workflows. Growth is strong because these users often start from smaller software bases and need rapid access to advanced subsurface modeling tools. This segment should gain share steadily through 2034.

Regional Analysis

North America Reservoir Simulation Software Market

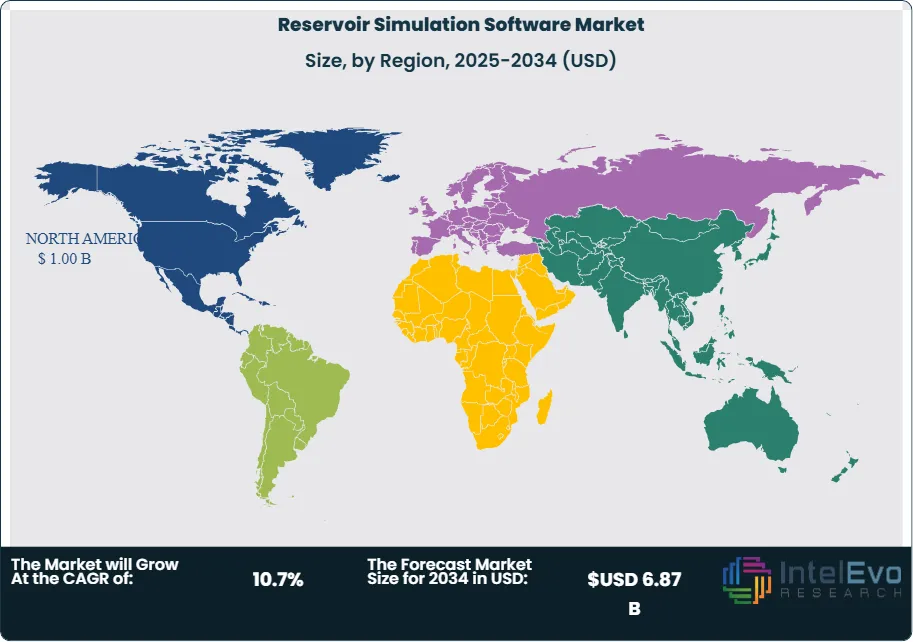

North America held an estimated 36.5% share of the Reservoir Simulation Software Market in 2025, equal to about USD 1.00 Billion, 2025. The region leads because it combines the largest installed upstream software base with strong unconventional activity, deep technical talent, and high enterprise software penetration. The United States dominates regional demand through shale modeling, field redevelopment, production optimization, and a growing set of CCS and geothermal use cases. AI adoption data among U.S.-based reservoir engineers also points to faster acceptance of digital modeling tools, with adoption rising from 43% in 2024 to 56% in 2025. Canada remains strategically important through oil sands, conventional field management, and the strong home-market presence of CMG. Mexico is smaller, but it is relevant through offshore development planning and maturing digital upstream workflows.

The region's regulatory environment is less about direct software control and more about data security, reserve governance, and energy transition support. North America also benefits from the heaviest vendor concentration, including SLB, Halliburton, AspenTech, Baker Hughes, and ResFrac. Because customers here are early adopters of cloud, AI, and high-performance computing, North America should remain the largest market through 2034 even as Asia Pacific and the Middle East grow faster in percentage terms.

Europe Reservoir Simulation Software Market

Europe represented an estimated 24.0% share in 2025, equal to about USD 0.66 Billion, 2025. Europe is smaller than North America in pure upstream software base, but it is one of the highest-value regions for advanced reservoir simulation because of offshore complexity, mature field redevelopment, CCS projects, and broader energy transition activity. Norway and the UK anchor regional demand through North Sea reservoir management, late-life asset planning, and carbon storage modeling. Germany and the Netherlands are smaller in hydrocarbon scale but more visible in energy transition and subsurface storage workflows.

Europe's strength comes from its mix of legacy offshore assets and emerging decarbonization projects, which requires simulation across both production and storage use cases. SLB, AspenTech, Kongsberg Digital, Halliburton, and Rock Flow Dynamics all have strong relevance here. The region also benefits from advanced industrial data standards and broad interest in OSDU-linked workflows. Europe should remain the second-largest regional market through 2034 because CCS, geothermal, and offshore brownfield projects require increasingly sophisticated simulation capability.

Asia Pacific Reservoir Simulation Software Market

Asia Pacific held an estimated 21.5% share in 2025, equal to about USD 0.59 Billion, 2025. The region is expanding quickly because national oil companies, gas producers, and offshore operators are investing in digital subsurface workflows to shorten planning cycles and improve recovery. China is the largest country market because of the scale of its conventional and unconventional asset base. India is rising through digital modernization across upstream operations and growing energy security concerns. Australia matters through LNG-linked offshore modeling, geothermal interest, and broader digital subsurface investment. Malaysia is also a major strategic country, highlighted by Halliburton's 2025 collaboration with PETRONAS to deploy DecisionSpace 365 and Unified Ensemble Modeling.

Asia Pacific benefits from a large pipeline of brownfield redevelopment and gas-focused projects, which creates steady demand for simulation in both development planning and production optimization. The region also has a strong medium-term growth case in carbon storage and underground gas storage. Asia Pacific should record one of the highest growth rates through 2034 because it is moving from selective high-end use toward broader enterprise adoption.

Latin America Reservoir Simulation Software Market

Latin America accounted for an estimated 9.5% share in 2025, equal to about USD 0.26 Billion, 2025. The region remains smaller than North America or Europe in software spend, but it is strategically important because reservoir uncertainty has high economic value in deepwater and large conventional assets. Brazil dominates by a wide margin. Pre-salt offshore fields and the need for integrated field planning support steady demand for high-end simulation. Baker Hughes' digital integration work with CMG and SLB's broader subsurface software presence both reinforce the region's importance. Mexico follows through offshore planning and field redevelopment use cases, while Argentina adds unconventional modeling demand linked to shale development.

Latin America's main opportunity is that simulation can directly influence large capital decisions in offshore and resource-dense projects, making software value per asset high even when user numbers are smaller. The main risk is slower software adoption at smaller operators and greater budget volatility than in North America. Even so, the region should grow steadily through 2034 because Brazil's subsurface complexity and Argentina's unconventional development both support stronger simulation demand.

Middle East & Africa Reservoir Simulation Software Market

Middle East & Africa held an estimated 8.5% share in 2025, equal to about USD 0.23 Billion, 2025. The region is smaller in current software revenue than North America, Europe, or Asia Pacific, but it has one of the strongest structural growth profiles. Saudi Arabia is the main driver because giant fields, unconventional gas, and large-scale digital transformation programs all require advanced subsurface modeling. The UAE follows through large brownfield assets and integrated digital field programs. South Africa is smaller today but retains long-term relevance in offshore and subsurface energy transition work. Oman is strategically important because it combines mature fields with carbon storage and underground storage potential.

Regional growth is supported by strong national operator spending and long-field-life assets where even small gains in recovery or forecasting accuracy matter economically. Halliburton, SLB, Baker Hughes, AspenTech, and Kongsberg Digital are well placed here because enterprise software contracts tend to favor established vendors with strong local support and deep workflow integration. The Middle East & Africa share should increase by 2034 as gas projects and digital field management expand.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment

- On-Premise

- Cloud and Hybrid

By Reservoir Type

- Conventional Oil and Gas Reservoirs

- Unconventional and Tight Reservoirs

- Offshore Deepwater Reservoirs

- CCUS, Geothermal, and Underground Storage

By Application

- Field Development Planning

- Production Optimization and EOR

- Reserve Estimation and History Matching

- Carbon Storage and Geothermal Modeling

By End User

- Integrated Oil Companies and National Oil Companies

- Oilfield Service Companies, EPCs, and Consulting Firms

- Research Institutes and Academia

- CCUS, Geothermal, and Energy Transition Developers

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.75 B |

| Forecast Revenue (2034) | USD 6.87 B |

| CAGR (2025-2034) | 10.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment (On-Premise, Cloud and Hybrid), By Reservoir Type (Conventional Oil and Gas Reservoirs, Unconventional and Tight Reservoirs, Offshore Deepwater Reservoirs, CCUS, Geothermal, and Underground Storage), By Application (Field Development Planning, Production Optimization and EOR, Reserve Estimation and History Matching, Carbon Storage and Geothermal Modeling), By End User (Integrated Oil Companies and National Oil Companies, Oilfield Service Companies, EPCs, and Consulting Firms, Research Institutes and Academia, CCUS, Geothermal, and Energy Transition Developers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, HALLIBURTON, CMG, ASPENTECH, BAKER HUGHES, EMERSON, ROCK FLOW DYNAMICS, KONGSBERG DIGITAL, RESFRAC CORPORATION, SEEQUENT, NOV, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Reservoir Type (Conventional Oil & Gas Reservoirs, Unconventional & Tight Reservoirs, Offshore Deepwater Reservoirs, CCUS, Geothermal & Underground Storage), By Application (Field Development Planning, Production Optimization & EOR, Reserve Estimation & History Matching, Carbon Storage & Geothermal Modeling), By End-User (IOCs & NOCs, Oilfield Services & EPCs, Research Institutes, Energy Transition Developers) Industry Region & Key Players – Market Dynamics, Competitive Strategies & Forecast 2026–2034")

, By Reservoir Type (Conventional Oil & Gas Reservoirs, Unconventional & Tight Reservoirs, Offshore Deepwater Reservoirs, CCUS, Geothermal & Underground Storage), By Application (Field Development Planning, Production Optimization & EOR, Reserve Estimation & History Matching, Carbon Storage & Geothermal Modeling), By End-User (IOCs & NOCs, Oilfield Services & EPCs, Research Institutes, Energy Transition Developers) Industry Region & Key Players – Market Dynamics, Competitive Strategies & Forecast 2026–2034")

, By Reservoir Type (Conventional Oil & Gas Reservoirs, Unconventional & Tight Reservoirs, Offshore Deepwater Reservoirs, CCUS, Geothermal & Underground Storage), By Application (Field Development Planning, Production Optimization & EOR, Reserve Estimation & History Matching, Carbon Storage & Geothermal Modeling), By End-User (IOCs & NOCs, Oilfield Services & EPCs, Research Institutes, Energy Transition Developers) Industry Region & Key Players – Market Dynamics, Competitive Strategies & Forecast 2026–2034")

Frequently Asked Questions

How big is the Reservoir Simulation Software Market?

The Global Reservoir Simulation Software Market was valued at USD 2.75 Billion in 2025, projected to reach USD 6.87 Billion by 2034 at a CAGR of 10.7% (2026–2034). Growth is driven by increasing demand for advanced reservoir modeling, AI-powered simulation, digital oilfield adoption, and efficient hydrocarbon recovery optimization.

Who are the major players in the Reservoir Simulation Software Market?

SLB, HALLIBURTON, CMG, ASPENTECH, BAKER HUGHES, EMERSON, ROCK FLOW DYNAMICS, KONGSBERG DIGITAL, RESFRAC CORPORATION, SEEQUENT, NOV, Others

Which segments covered the Reservoir Simulation Software Market?

By Deployment (On-Premise, Cloud and Hybrid), By Reservoir Type (Conventional Oil and Gas Reservoirs, Unconventional and Tight Reservoirs, Offshore Deepwater Reservoirs, CCUS, Geothermal, and Underground Storage), By Application (Field Development Planning, Production Optimization and EOR, Reserve Estimation and History Matching, Carbon Storage and Geothermal Modeling), By End User (Integrated Oil Companies and National Oil Companies, Oilfield Service Companies, EPCs, and Consulting Firms, Research Institutes and Academia, CCUS, Geothermal, and Energy Transition Developers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Reservoir Simulation Software Market

Published Date : 18 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date