- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Retrieval Augmented Generation Market Size, Share | CAGR of 49.40%

Global Retrieval Augmented Generation Market Size, Share & Analysis Report By Deployment Model (Cloud, On-Premises, Hybrid), Organization Size (Large & SMEs), Industry Vertical (Healthcare, Legal, Financial, IT & Telecom, Manufacturing, Education, Government, Others), Application (Q&A, Customer Service, Content, Knowledge, Decision Support, Research), Region & Key Players – Trends, Dynamics & Forecast 2025–2034

Report Overview

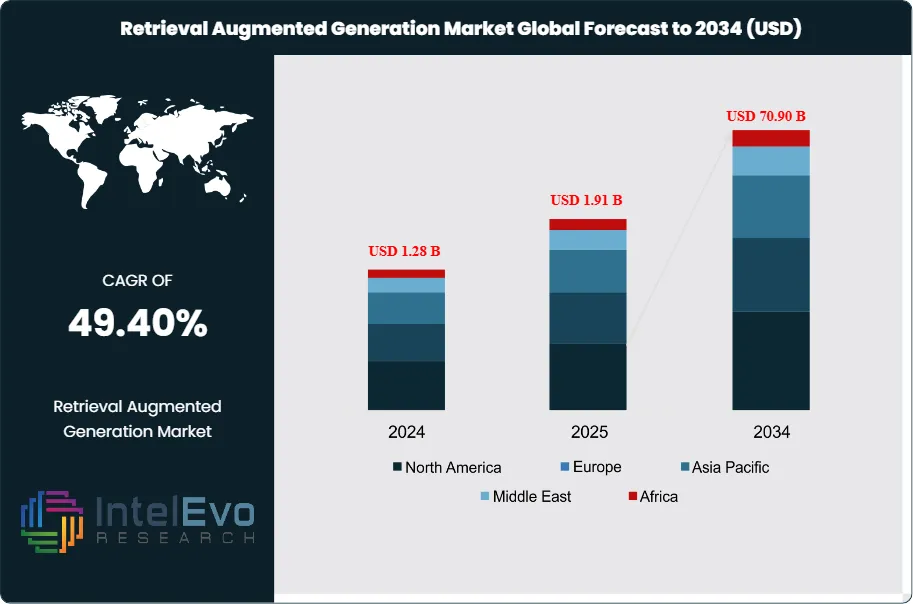

The Retrieval Augmented Generation Market size is expected to be worth around USD 70.90 Billion by 2034, from USD 1.28 Billion in 2024, growing at a CAGR of 49.40% during the forecast period from 2024 to 2034. The Retrieval Augmented Generation (RAG) market is an emerging and rapidly expanding segment within the artificial intelligence and machine learning technology landscape. RAG systems are sophisticated AI architectures that combine the generative capabilities of large language models with dynamic information retrieval from external knowledge bases, enabling more accurate, contextual, and up-to-date responses than traditional standalone AI models.

Get More Information about this report -

Request Free Sample ReportThese systems address critical limitations of conventional language models by accessing real-time data, proprietary knowledge bases, and domain-specific information sources to enhance response quality and factual accuracy. The growing demand for enterprise AI solutions that can leverage organizational knowledge while maintaining accuracy and reducing hallucinations is driving explosive growth in the RAG market globally. Such systems are increasingly integrated with existing business applications, customer service platforms, and knowledge management systems to provide intelligent automation while preserving data governance and security requirements.

Several factors influence the expansion and evolution of the retrieval augmented generation market. The primary driver is the enterprise adoption of generative AI solutions that require access to current, accurate, and organization-specific information beyond the training data limitations of base language models. The need for AI systems that can provide verifiable, source-attributed responses drives demand for RAG architectures that maintain transparency and accountability in automated decision-making. Additionally, advances in vector databases, embedding technologies, and semantic search capabilities continue to enhance RAG system performance, enabling faster retrieval speeds and more relevant context matching. The growing emphasis on AI safety, explainability, and bias reduction creates market opportunities for RAG solutions that provide audit trails and source verification. Cost-effectiveness compared to fine-tuning large models makes RAG solutions attractive to organizations seeking advanced AI capabilities without prohibitive computational requirements.

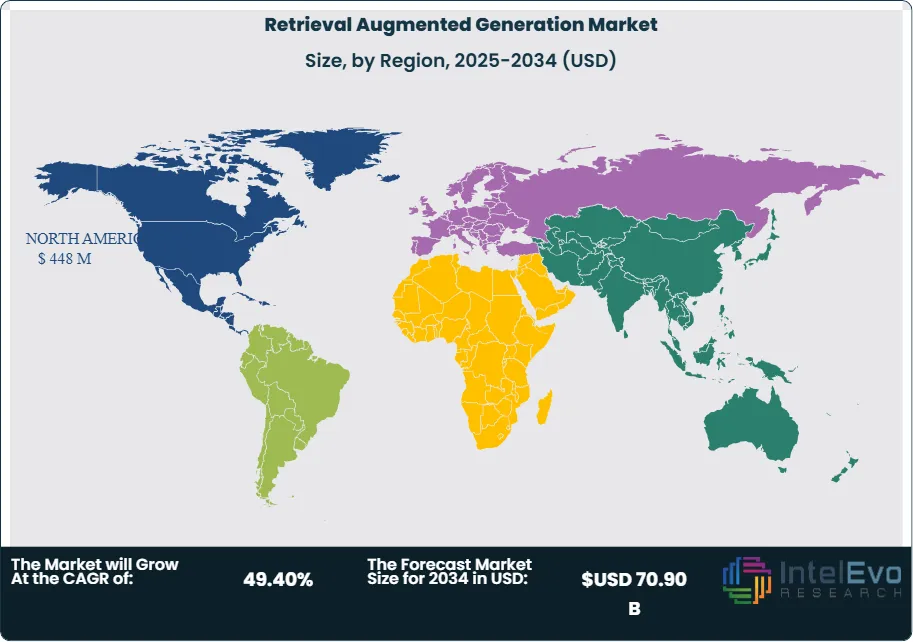

Regionally, the Retrieval Augmented Generation market shows concentrated growth patterns reflecting varying levels of AI adoption and technological infrastructure development. North America leads the market due to early enterprise AI adoption, substantial venture capital investment in AI startups, and the presence of major technology companies developing foundational RAG technologies. The region benefits from mature cloud computing infrastructure and regulatory frameworks that support AI innovation while addressing governance concerns. The Asia-Pacific region demonstrates rapid growth potential, particularly in China, India, and Japan, where government AI initiatives and technology sector expansion drive demand for advanced AI solutions. Europe maintains significant market presence through stringent data privacy requirements that favor RAG approaches for maintaining data sovereignty while leveraging AI capabilities. Latin America and the Middle East & Africa represent emerging markets with increasing AI awareness and growing digital transformation initiatives.

The COVID-19 pandemic accelerated digital transformation initiatives and highlighted the critical importance of accessible, intelligent information systems that could support remote work and automated customer service during unprecedented operational challenges. Organizations rapidly adopted AI-powered solutions including RAG systems to handle increased customer inquiries, support remote employees, and maintain business continuity amid workforce disruptions. The pandemic demonstrated the value of systems that could quickly access and synthesize information from multiple sources to provide accurate guidance on rapidly changing policies, procedures, and market conditions. Economic pressures during the pandemic also emphasized the cost-effectiveness of RAG solutions compared to developing custom AI models or hiring additional knowledge workers for information processing tasks.

Geopolitical tensions and technology transfer restrictions between major economies have created challenges affecting the RAG market through export controls on advanced AI technologies, semiconductor access limitations, and data sovereignty requirements that complicate international deployment strategies. Trade restrictions particularly between the United States and China affect access to cutting-edge hardware acceleration platforms and cloud computing services that support large-scale RAG implementations. Data localization requirements and cross-border information sharing restrictions necessitate regional deployment architectures and compliance frameworks that increase operational complexity. These tensions encourage domestic AI capability development and regional partnership strategies to reduce dependence on international technology providers.

, Organization Size (Large & SMEs), Industry Vertical (Healthcare, Legal, Financial, IT & Telecom, Manufacturing, Education, Government, Others), Application (Q&A, Customer Service, Content, Knowledge, Decision Support, Research), Region & Key Players – Trends, Dynamics & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Retrieval Augmented Generation Market is expected to reach USD 70.90 Billion by 2034, driven by enterprise AI adoption, knowledge management needs, and improved accuracy requirements for AI applications.

- Deployment Model Dominance: Cloud-based RAG solutions lead the market due to scalability, infrastructure efficiency, and integration capabilities with existing enterprise systems.

- Organization Size Dominance: Large enterprises dominate market revenue through complex implementations, while small and medium enterprises drive volume growth through simplified RAG-as-a-Service offerings.

- Industry Vertical Dominance: Healthcare holds the largest share with 28.8% market presence, driven by medical knowledge requirements and clinical decision support needs.

- Application Dominance: Content generation leads the RAG application market as businesses increasingly leverage AI-driven tools to create high-quality, contextually accurate, and scalable content for diverse industries.

- Drivers: Key drivers accelerating growth include AI democratization initiatives, enterprise knowledge management needs, and regulatory requirements for explainable AI that boost market expansion through enhanced accuracy and transparency.

- Restraints: Growth is hindered by data integration complexities, computational infrastructure requirements, and AI governance challenges that create implementation barriers and operational risks.

- Opportunities: The market is positioned for expansion through opportunities like agentic RAG systems, multimodal information retrieval, and industry-specific knowledge specialization that enable sophisticated AI applications.

- Trends: Emerging trends including vector database optimization, hybrid retrieval strategies, and AI agent integration are reshaping the market by enabling more sophisticated and autonomous knowledge-driven AI systems.

- Regional Analysis: North America leads with 37.4% market share due to enterprise AI adoption and technology infrastructure maturity. Asia-Pacific shows highest growth potential driven by AI investment and digital transformation initiatives.

Deployment Model Analysis:

Cloud-Based Solutions Lead With Over 65% Market Share In Retrieval Augmented Generation Market, Cloud-based RAG solutions maintain market leadership through compelling advantages in computational scalability, infrastructure cost optimization, and seamless integration with existing cloud-native applications that align with modern enterprise architecture strategies. The dominance of cloud deployment reflects the substantial computational requirements for vector similarity searches, large language model inference, and real-time data indexing that benefit from elastic cloud resources and specialized AI acceleration hardware. Organizations benefit from managed vector database services, automatic scaling capabilities, and integrated security protocols that reduce operational complexity while ensuring performance consistency. The distributed nature of cloud infrastructure enables global deployment of RAG systems with regional data compliance while maintaining centralized management and governance controls. While on-premises solutions retain relevance for organizations with strict data sovereignty requirements or air-gapped environments, the trend toward cloud-first AI strategies continues strengthening market share for cloud-based offerings through superior economics and faster innovation cycles.

Organization Size Analysis:

Large enterprises represent the primary revenue drivers in the RAG market through comprehensive implementations that address complex knowledge management requirements and integration with sophisticated IT ecosystems including legacy systems and specialized workflows. Enterprise adoption reflects the critical need for AI solutions that can access proprietary knowledge bases, maintain data governance standards, and provide audit trails for regulated industries and compliance requirements. These organizations require extensive customization capabilities, enterprise-grade security features, and integration with existing business intelligence and document management systems. Small and medium enterprises demonstrate the highest growth rates through adoption of simplified RAG-as-a-Service offerings that provide advanced AI capabilities without requiring substantial infrastructure investment or specialized technical expertise. The SME segment benefits from vendor focus on pre-configured solutions, industry-specific templates, and user-friendly interfaces that accelerate time-to-value while minimizing training requirements.

Industry Vertical Analysis:

Healthcare sector leads RAG adoption due to unique characteristics including vast medical knowledge requirements, regulatory compliance needs, and clinical decision support applications that benefit significantly from evidence-based information retrieval and synthesis capabilities. Medical professionals require access to current research, treatment guidelines, and patient-specific information that RAG systems can aggregate and present in contextually relevant formats. The sector's emphasis on accuracy, source attribution, and liability considerations aligns with RAG capabilities for providing traceable, verifiable information sources. Legal and professional services represent another significant vertical driven by requirements for accessing case law, regulatory guidance, and precedent analysis that requires sophisticated document retrieval and synthesis capabilities. Financial services increasingly adopt RAG solutions for regulatory compliance, risk assessment, and customer advisory applications that demand current market information and regulatory guidance.

Application Analysis:

Content generation represents the largest application of retrieval-augmented generation, driven by demand for AI-based writing assistants, marketing copy solutions, and knowledge-sensitive drafting tools. By combining retrieval with natural language generation, RAG enhances factual consistency, ensuring that outputs are reliable and contextually anchored, which is especially critical for enterprises producing blogs, reports, or research summaries. Question-answering systems form another significant segment, powering smart assistants and enterprise chatbots that can draw from large knowledge bases. Customer service automation benefits from RAG through more accurate, context-aware responses, reducing human intervention while increasing customer satisfaction. Knowledge management applications are also key, as organizations use RAG to organize and surface internal documents more effectively. Decision support systems and research analysis leverage the technology to provide contextual insights and evidence-backed recommendations. While all sub-segments show strong adoption, content generation dominates due to its scalability, cost efficiency, and immediate impact on industries reliant on written communication.

Regional Analysis

North America Leads With More Than 35% Market Share In Retrieval Augmented Generation Market, North America maintains market leadership through established AI research institutions, substantial venture capital investment in AI startups, and early enterprise adoption of advanced language model technologies that create favorable conditions for RAG market development. The region benefits from presence of major cloud service providers, AI research organizations, and technology companies that drive innovation and provide foundational infrastructure for RAG deployments. Regulatory frameworks around AI governance and explainability create demand for transparent AI systems that can provide source attribution and audit trails. Cultural emphasis on innovation and competitive advantage drives enterprise willingness to invest in cutting-edge AI technologies despite implementation challenges.

Asia-Pacific represents the highest growth potential region, fueled by government AI development initiatives, massive technology sector investment, and rapid digital transformation across emerging markets that create substantial demand for intelligent information systems. China leads regional growth through national AI strategy implementation and substantial technology company investment in generative AI capabilities. Countries like India, Japan, and South Korea demonstrate accelerating RAG adoption as multinational corporations establish AI centers of excellence and local companies develop domain-specific AI applications. The region's diverse languages and cultural contexts drive demand for multilingual RAG systems and localized knowledge base development.

Europe demonstrates strong growth driven by GDPR compliance requirements, emphasis on AI ethics and explainability, and increasing focus on data sovereignty that favors RAG approaches for maintaining control over organizational knowledge while leveraging AI capabilities. The region's regulatory environment encourages development of transparent, auditable AI systems that can provide clear reasoning and source attribution. Brexit-related changes and EU digital sovereignty initiatives influence deployment strategies toward regional data processing and European-based service providers.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

Deployment Model

- Cloud-Based Solutions

- On-Premises Solutions

- Hybrid Deployments

Organization Size

- Large Enterprises

- Small and Medium Enterprises

Industry Vertical

- Healthcare

- Legal and Professional Services

- Financial Services

- IT & Telecom

- Manufacturing

- Education

- Government

- Other Industry Verticals

Application

- Question-Answering Systems

- Customer Service Automation

- Content Generation

- Knowledge Management

- Decision Support Systems

- Research and Analysis

Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.91 B |

| Forecast Revenue (2034) | USD 70.90 B |

| CAGR (2025-2034) | 49.40% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Deployment Model (Cloud-Based Solutions, On-Premises Solutions, Hybrid Deployments); Organization Size (Large Enterprises, Small and Medium Enterprises), Industry Vertical (Healthcare, Legal and Professional Services, Financial Services, IT & Telecom, Manufacturing, Education, Government, Other Industry Verticals), Application (Question-Answering Systems, Customer Service Automation, Content Generation, Knowledge Management, Decision Support Systems, Research and Analysis) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | OpenAI, Microsoft Corporation, Google LLC, Amazon Web Services, Anthropic, Meta Platforms, Inc., NVIDIA Corporation, Hugging Face, Pinecone Systems Inc., Weaviate, Chroma, LangChain, IBM Corporation, Oracle Corporation, Databricks |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Organization Size (Large & SMEs), Industry Vertical (Healthcare, Legal, Financial, IT & Telecom, Manufacturing, Education, Government, Others), Application (Q&A, Customer Service, Content, Knowledge, Decision Support, Research), Region & Key Players – Trends, Dynamics & Forecast 2025–2034")

, Organization Size (Large & SMEs), Industry Vertical (Healthcare, Legal, Financial, IT & Telecom, Manufacturing, Education, Government, Others), Application (Q&A, Customer Service, Content, Knowledge, Decision Support, Research), Region & Key Players – Trends, Dynamics & Forecast 2025–2034")

, Organization Size (Large & SMEs), Industry Vertical (Healthcare, Legal, Financial, IT & Telecom, Manufacturing, Education, Government, Others), Application (Q&A, Customer Service, Content, Knowledge, Decision Support, Research), Region & Key Players – Trends, Dynamics & Forecast 2025–2034")

Frequently Asked Questions

How big is the Retrieval Augmented Generation Market?

By 2034, the Retrieval Augmented Generation Market is projected to hit USD 70.90B, up from USD 1.28B in 2024. Discover key growth drivers, trends, and insights, innovations, and opportunities.

Who are the major players in the Retrieval Augmented Generation Market?

OpenAI, Microsoft Corporation, Google LLC, Amazon Web Services, Anthropic, Meta Platforms, Inc., NVIDIA Corporation, Hugging Face, Pinecone Systems Inc., Weaviate, Chroma, LangChain, IBM Corporation, Oracle Corporation, Databricks

Which segments covered the Retrieval Augmented Generation Market?

Deployment Model (Cloud-Based Solutions, On-Premises Solutions, Hybrid Deployments); Organization Size (Large Enterprises, Small and Medium Enterprises), Industry Vertical (Healthcare, Legal and Professional Services, Financial Services, IT & Telecom, Manufacturing, Education, Government, Other Industry Verticals), Application (Question-Answering Systems, Customer Service Automation, Content Generation, Knowledge Management, Decision Support Systems, Research and Analysis)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Retrieval Augmented Generation Market

Published Date : 28 Aug 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date