- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global RAG Platform Market Size & Forecast 2034 | CAGR 32.6%

Global Retrieval Augmented Generation (RAG) Platform Market Size, Share, Growth & Industry Analysis By Offering (Software/Platforms, Services – Consulting, Integration, Support), By Deployment Mode (Cloud, On-Premise, Hybrid), By Organization Size (Large Enterprises, SMEs), By Application (Customer Support, Content Generation, Knowledge Management, Legal & Compliance, Data Research & Analytics), By Vertical (BFSI, Healthcare, IT & Telecom, Government, Retail, Manufacturing, Energy) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

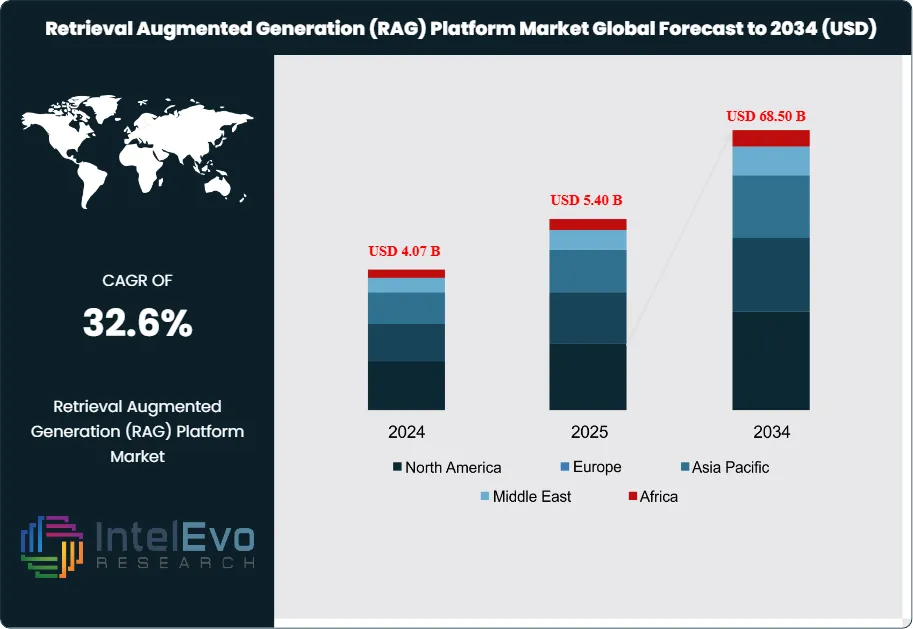

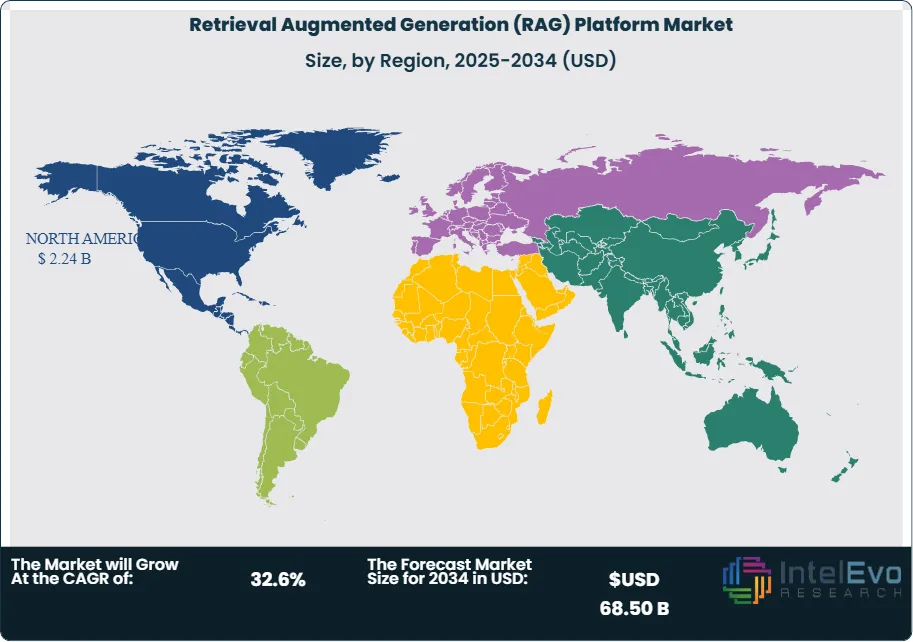

| USD 5.40 Billion | USD 68.50 Billion | 32.6% | North America, 41.5% |

The Retrieval Augmented Generation (RAG) Platform Market was valued at approximately USD 4.07 Billion in 2024 and reached USD 5.40 Billion in 2025. The market is projected to grow to USD 68.50 Billion by 2034, expanding at a CAGR of 32.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 63.10 Billion over the analysis period. Current market assessment shows that the integration of Retrieval Augmented Generation (RAG) has become the primary architectural standard for enterprise artificial intelligence. Organizations are shifting away from standalone large language models (LLMs) toward systems that prioritize data grounding to eliminate hallucinations. Industry analysis indicates that the demand for these platforms is catalyzed by the need for verifiable, real-time data retrieval in corporate decision-making environments. Based on supply-chain and demand-side evaluation, the market is maturing as enterprises move from experimental pilots to production-ready deployments that require robust security and high-speed vector retrieval.

Get More Information about this report -

Request Free Sample ReportMarket patterns suggest a significant transition toward unified RAG orchestrators that simplify the complexity of data ingestion, chunking, and embedding. Current market assessment shows that vector databases and semantic search technologies have evolved to handle petabyte-scale unstructured data with millisecond inference latency. Regulatory influences, such as the EU AI Act and the NIST AI Framework, are forcing enterprises to adopt RAG platforms that offer clear data lineage and citation transparency. Trade data suggests that industries with heavy compliance burdens, particularly BFSI and healthcare, are the fastest adopters of private RAG instances. These organizations leverage RAG to ground generative AI outputs in proprietary, secure datasets while maintaining strict adherence to GDPR and CCPA requirements.

Risk factors including data privacy breaches, high computational costs for embedding updates, and the complexity of managing latent space drift are key considerations for board-level decision-makers. Technology effects including the rise of multi-modal RAG and agentic workflows are introducing new complexities in tracking data provenance. Regional highlights show that North America maintains a dominant position due to early enterprise adoption and high venture capital activity, while Asia Pacific is emerging as a high-growth investment hotspot. Trade data and regulatory filings suggest that enterprise AI budgets are increasingly being reallocated toward retrieval-based architectures to ensure reliability. Current market assessment shows that by late 2025, approximately 75% of new enterprise generative AI applications will utilize a RAG-based architecture to provide factual grounding.

Platform Market Size, Share, Growth & Industry Analysis By Offering (Software/Platforms, Services – Consulting, Integration, Support), By Deployment Mode (Cloud, On-Premise, Hybrid), By Organization Size (Large Enterprises, SMEs), By Application (Customer Support, Content Generation, Knowledge Management, Legal & Compliance, Data Research & Analytics), By Vertical (BFSI, Healthcare, IT & Telecom, Government, Retail, Manufacturing, Energy) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Global Retrieval Augmented Generation Platform Market is projected to grow from USD 5.40 Billion in 2025 to USD 68.50 Billion by 2034, maintaining a CAGR of 32.6%.

- Segment Dominance: The Software/Platform segment held a dominant 68.2% market share in 2025, worth USD 3.68 Billion, driven by the shift toward end-to-end automated orchestration tools.

- Segment Dominance: The BFSI vertical emerged as the top end-user in 2025 with a 26.4% share, as banks prioritize anti-hallucination protocols for customer-facing digital assistants.

- Driver: Demand for factual grounding in large language models is the primary driver, with enterprise adoption rates for grounded AI systems increasing by 45.0% year-over-year in 2025.

- Restraint: High computational overhead and latent space complexity act as a restraint, potentially increasing customer acquisition cost by 18.5% for platform providers.

- Opportunity: The emergence of Industry-Specific RAG for the legal and medical sectors presents a USD 12.40 Billion untapped opportunity as firms seek hyper-accurate domain knowledge.

- Trend: Integration of multi-modal retrieval is a dominant trend, with platforms capable of processing video and audio embeddings seeing a 30.0% surge in demand in late 2025.

- Regional Analysis: North America remains the leading regional market with a 41.5% share in 2025, valued at USD 2.24 Billion, supported by Silicon Valley’s infrastructure innovation.

Competitive Landscape Overview

The Global Retrieval Augmented Generation Platform Market is currently moderately consolidated, with the top four players commanding a combined market share of approximately 48.2% in 2025. Competition is platform-based, with hyperscalers integrating RAG capabilities into their existing cloud AI stacks while pure-play vector database and orchestration firms focus on modular flexibility. Current market assessment shows that the nature of competition is shifting toward proprietary embedding quality and "time-to-retrieval" efficiency. Recent competitive intensity shifts indicate a surge in M&A activity as traditional data warehouse providers acquire AI startups to bridge the gap between structured records and unstructured semantic search.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| MICROSOFT | USA | Leader | Azure AI Search (RAG) | Global | Integrated automated chunking in Dec 2024 |

| PINECONE | USA | Leader | Pinecone Serverless | Global | Launched hybrid search optimization in 2025 |

| OPENAI | USA | Leader | Assistants API (RAG) | Global | Upgraded file search retrieval logic in 2025 |

| AMAZON AWS | USA | Leader | Amazon Bedrock RAG | Global | Partnered with Anthropic for industry RAG |

| MONGODB | USA | Challenger | MongoDB Atlas Vector Search | North America | Released integrated AI orchestrator in 2025 |

| DATASTAX | USA | Challenger | Astra DB (Vector) | Global | Acquired a specialized RAG startup in 2025 |

| COHERE | Canada | Challenger | Cohere Rerank | Europe/NA | Optimized multi-step retrieval for SMEs |

| ELASTIC | USA | Challenger | Elasticsearch Relevance Engine | Global | Launched automated embedding updates 2025 |

| WEAVIATE | Netherlands | Niche Player | Weaviate Cloud | Europe | Focused on multi-modal vector search |

| LANGCHAIN | USA | Niche Player | LangGraph | Global | Introduced agentic RAG frameworks in 2026 |

By Offering

Based on supply-chain and demand-side evaluation, the market is divided into Software/Platforms and Services. The Software/Platform segment dominated the Global Retrieval Augmented Generation Platform Market in 2025 with a 68.2% share, valued at USD 3.68 Billion. This dominance is attributed to the critical need for unified infrastructures that handle the entire RAG pipeline, including document parsing, embedding generation, vector storage, and prompt engineering. Enterprises are prioritizing platforms that offer low-code interfaces to reduce the technical debt associated with building custom retrieval layers. The rise of cloud-native, serverless vector platforms has further accelerated software revenue, as companies shift from high-CAPEX infrastructure to scalable SaaS models. Current market assessment shows that the integration of automated "reranking" modules within software platforms is becoming a standard requirement for ensuring high precision in document retrieval.

The Services segment, including consulting, integration, and managed services, accounted for 31.8% of the market in 2025, worth USD 1.72 Billion. While the platforms provide the tools, the complexity of aligning RAG with legacy enterprise data silos requires significant professional expertise. Industry analysis indicates that the demand for services is particularly high among mid-market firms that lack in-house AI research teams. These firms seek third-party integrators to optimize embedding models and fine-tune retrieval thresholds to ensure high model accuracy. Managed RAG services are also gaining traction, where vendors handle the continuous update of vector indexes and embedding maintenance, allowing enterprises to focus on application development.

By Deployment Mode

The deployment segmentation includes Cloud, On-Premise, and Hybrid models. Cloud-based deployment held a significant 72.4% share in 2025, valued at USD 3.91 Billion. The inherent scalability of cloud environments is essential for managing the high-memory requirements of vector indexing and the inference demands of LLMs. Hyperscalers are leading this segment by offering managed RAG services that integrate directly with existing data lakes. Current market assessment shows that the elasticity of cloud RAG platforms allows enterprises to scale their knowledge bases from thousands to millions of documents without manual hardware adjustments. The proliferation of serverless vector search models has further reduced the entry barrier for startups and SMEs, driving a 38.0% growth in cloud-native AI deployments.

On-premise and hybrid deployments accounted for the remaining 27.6% in 2025, valued at USD 1.49 Billion. These modes are preferred by government, defense, and national security agencies that require absolute data sovereignty. Many organizations in the financial sector are adopting hybrid RAG strategies, where highly sensitive records are retrieved from secure on-premise vector stores while general queries are processed in the cloud to balance performance and privacy. Current assessment suggests that "Private RAG" solutions are becoming a major sub-segment as regulated industries seek to deploy generative AI without exposing proprietary intellectual property to public cloud environments.

By Vertical

The BFSI vertical led the market in 2025 with a 26.4% share, worth USD 1.43 Billion. Financial institutions utilize RAG platforms to power sophisticated customer support bots and automated equity research tools that require citation-backed outputs. The need to mitigate financial risk caused by AI hallucinations is a primary driver for investment in this sector. Healthcare and Life Sciences represented 19.8% of the market in 2025, valued at USD 1.07 Billion. In this vertical, RAG platforms are used to ground medical AI in peer-reviewed journals and patient records, ensuring that clinical suggestions are based on verifiable data. Other significant verticals include IT & Telecommunications (18.2%), Government & Defense (14.5%), and Retail & E-commerce (12.6%), each driven by specific needs for factual automation and real-time knowledge retrieval.

Regional Analysis

North America

North America dominated the Global Retrieval Augmented Generation Platform Market in 2025, capturing a 41.5% share with revenue valued at USD 2.24 Billion. The region’s leadership is sustained by a robust ecosystem of technology pioneers in Silicon Valley and Seattle. Industry analysis indicates that North American enterprises are reallocating 35.0% of their total IT innovation budgets toward grounded AI systems to improve operational efficiency. The presence of major hyperscalers providing integrated cloud-RAG services ensures that the region remains at the forefront of the market. Regulatory filings suggest that the adoption of the NIST AI Risk Management Framework has encouraged U.S. firms to implement RAG as a safety standard for generative outputs. The high density of AI-native startups also fosters a rapid "fail-fast" culture that accelerates the development of advanced retrieval techniques like hybrid search and graph-based RAG.

Europe

Europe held a 24.2% market share in 2025, worth USD 1.31 Billion. The European market is heavily influenced by the EU AI Act and GDPR, which necessitate high levels of data transparency and sovereignty. Current market assessment shows that European firms are prioritizing hybrid RAG deployments to keep sensitive data within regional borders. Germany and France have emerged as significant hubs for AI development, with a strong focus on industrial RAG applications in manufacturing and automotive engineering. The UK also remains a critical market, particularly for legal-tech and fintech RAG applications that require high precision and verifiable citations. Industry analysis suggests that European investment is increasingly directed toward open-source RAG frameworks to avoid vendor lock-in with North American hyperscalers.

Asia Pacific

The Asia Pacific region accounted for 18.6% of the market in 2025, worth USD 1.00 Billion, and is projected to be the fastest-growing region through 2034. Rapid digitalization in China, India, and Japan is driving massive demand for automated customer support and localized knowledge management. Based on trade data and supply-chain evaluation, Asia Pacific enterprises are skipping unimodal LLM steps and moving directly to RAG-based systems to ensure accuracy in multi-lingual environments. Current market assessment shows that the region's massive manufacturing sector is adopting RAG for on-site technical manuals and supply-chain optimization, utilizing vector search to correlate complex logistics records. Government-led AI initiatives in India and Southeast Asia are also providing favorable conditions for platform providers to expand their footprint.

Latin America and Middle East & Africa

Latin America represented 7.5% of the market in 2025 (USD 0.41 Billion), with growth led by Brazil and Mexico’s expanding fintech sectors. The region is seeing a surge in RAG adoption for mobile-first customer engagement platforms. The Middle East & Africa held an 8.2% share in 2025 (USD 0.44 Billion). Growth is primarily driven by sovereign wealth fund investments in the UAE and Saudi Arabia, where national AI strategies focus on creating Arabic-centric RAG systems for government services and energy sector optimization. Both regions are expected to grow significantly as cloud providers expand their regional data center footprints through 2034, providing the localized low-latency infrastructure necessary for advanced semantic search.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software/Platforms

- Services (Consulting, Integration, Support)

By Deployment Mode

- Cloud

- On-Premise

- Hybrid

By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

By Application

- Customer Support

- Content Generation

- Knowledge Management

- Legal and Compliance

- Data Research and Analytics

By Vertical

- BFSI

- Healthcare and Life Sciences

- IT and Telecommunications

- Government and Defense

- Retail and E-commerce

- Manufacturing

- Energy and Utilities

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.40 B |

| Forecast Revenue (2034) | USD 68.50 B |

| CAGR (2025-2034) | 32.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Software/Platforms, Services (Consulting, Integration, Support)), By Deployment Mode, (Cloud, On-Premise, Hybrid), By Organization Size, (Large Enterprises, Small and Medium Enterprises (SMEs)), By Application, (Customer Support, Content Generation, Knowledge Management, Legal and Compliance, Data Research and Analytics), By Vertical, (BFSI, Healthcare and Life Sciences, IT and Telecommunications, Government and Defense, Retail and E-commerce, Manufacturing, Energy and Utilities) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT, PINECONE, OPENAI, AMAZON AWS, GOOGLE, MONGODB, DATASTAX, COHERE, ELASTIC, WEAVIATE, LANGCHAIN, ANTHROPIC, QDRANT, ZILLIZ, NVIDIA, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Platform Market Size, Share, Growth & Industry Analysis By Offering (Software/Platforms, Services – Consulting, Integration, Support), By Deployment Mode (Cloud, On-Premise, Hybrid), By Organization Size (Large Enterprises, SMEs), By Application (Customer Support, Content Generation, Knowledge Management, Legal & Compliance, Data Research & Analytics), By Vertical (BFSI, Healthcare, IT & Telecom, Government, Retail, Manufacturing, Energy) Industry Trends & Forecast 2026–2034")

Platform Market Size, Share, Growth & Industry Analysis By Offering (Software/Platforms, Services – Consulting, Integration, Support), By Deployment Mode (Cloud, On-Premise, Hybrid), By Organization Size (Large Enterprises, SMEs), By Application (Customer Support, Content Generation, Knowledge Management, Legal & Compliance, Data Research & Analytics), By Vertical (BFSI, Healthcare, IT & Telecom, Government, Retail, Manufacturing, Energy) Industry Trends & Forecast 2026–2034")

Platform Market Size, Share, Growth & Industry Analysis By Offering (Software/Platforms, Services – Consulting, Integration, Support), By Deployment Mode (Cloud, On-Premise, Hybrid), By Organization Size (Large Enterprises, SMEs), By Application (Customer Support, Content Generation, Knowledge Management, Legal & Compliance, Data Research & Analytics), By Vertical (BFSI, Healthcare, IT & Telecom, Government, Retail, Manufacturing, Energy) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Retrieval Augmented Generation (RAG) Platform Market?

Global Retrieval augmented generation market valued at USD 4.07B in 2024, reaching USD 68.5B by 2034, growing at a CAGR of 32.6% from 2026–2034.

Who are the major players in the Retrieval Augmented Generation (RAG) Platform Market?

MICROSOFT, PINECONE, OPENAI, AMAZON AWS, GOOGLE, MONGODB, DATASTAX, COHERE, ELASTIC, WEAVIATE, LANGCHAIN, ANTHROPIC, QDRANT, ZILLIZ, NVIDIA, Others

Which segments covered the Retrieval Augmented Generation (RAG) Platform Market?

By Offering, (Software/Platforms, Services (Consulting, Integration, Support)), By Deployment Mode, (Cloud, On-Premise, Hybrid), By Organization Size, (Large Enterprises, Small and Medium Enterprises (SMEs)), By Application, (Customer Support, Content Generation, Knowledge Management, Legal and Compliance, Data Research and Analytics), By Vertical, (BFSI, Healthcare and Life Sciences, IT and Telecommunications, Government and Defense, Retail and E-commerce, Manufacturing, Energy and Utilities)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Retrieval Augmented Generation (RAG) Platform Market

Published Date : 09 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date