- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Rigid Plastic Packaging Market Size, Share 2034 | 5.8% CAGR

Global Rigid Plastic Packaging Market Size, Share, Growth Analysis By Type (Bottles, Caps & Closures, Containers, Others), By Material (Polyethylene Terephthalate PET, High Density Polyethylene HDPE, Polypropylene PP, Others), By Production Process (Extrusion, Blow Molding, Thermoforming, Injection Molding, Others), By End-User (Food & Beverage, Household, Healthcare, Personal Care, Others) Industry Global Demand, Strategic Insights, Competitive Landscape, Emerging Technologies, Sustainability Trends, Market Dynamics, Investment Opportunities & Forecast 2025–2034

Report Overview

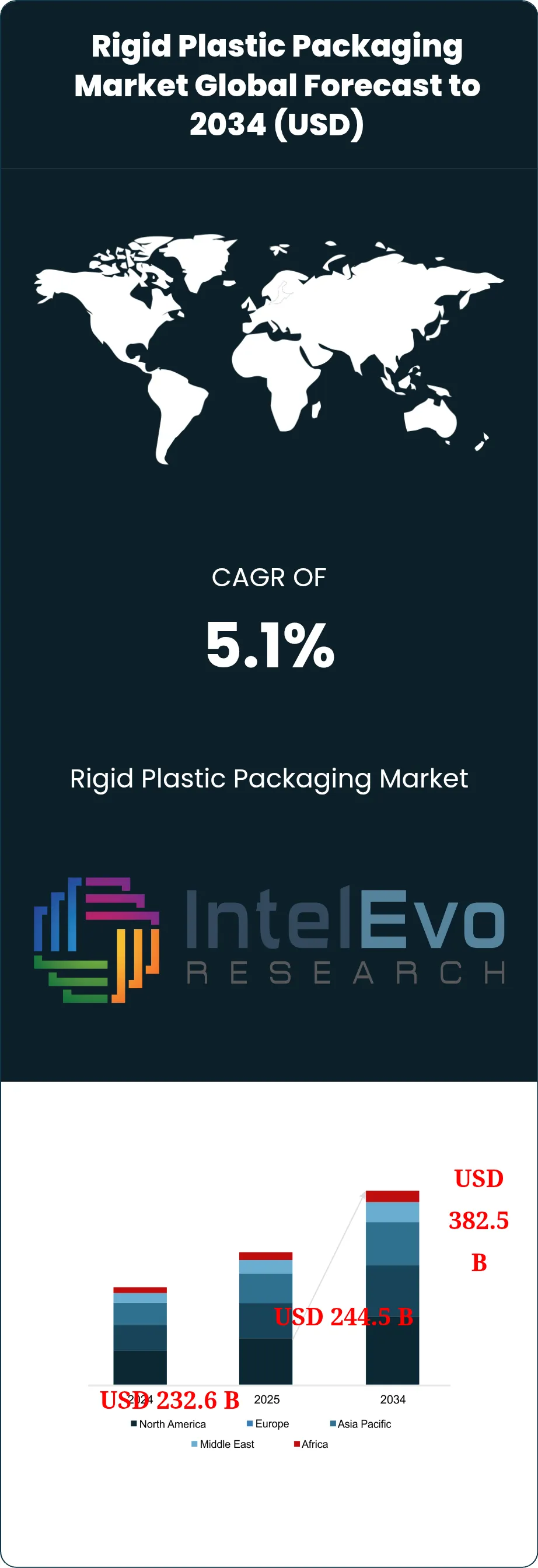

The Rigid Plastic Packaging Market was valued at USD 232.6 billion in 2024 and is projected to reach approximately USD 244.5 billion in 2025. The market is further expected to expand to nearly USD 382.5 billion by 2034, registering a compound annual growth rate (CAGR) of about 5.1% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportGrowth reflects resilient demand for durable, lightweight formats across high-volume consumer and healthcare categories. Bottles, jars, tubs, trays, and closures made from PET, HDPE, PP, PVC, and polystyrene remain central to modern distribution because they protect product integrity, reduce transport weight versus glass, and support high-speed filling lines.

Demand fundamentals stay anchored in food and beverage, which accounts for an estimated 50–55% of rigid plastic packaging revenue, supported by ready-to-eat meals, dairy, beverages, and convenience formats. Pharmaceuticals and medical supplies contribute roughly 10–12%, driven by compliance needs, dosing accuracy, and barrier performance. E-commerce and foodservice expand use of rigid protective packs and tamper-evident closures, with shipment growth and last-mile handling raising the value of impact resistance and leak prevention. On the supply side, converters face margin pressure from resin price volatility, energy costs, and tight capacity for food-grade recycled polymers, which can constrain near-term output.

Regulation reshapes material choices and procurement standards. Packaging represents about 31% of global plastic use, and in Europe the packaging sector consumes close to 40% of plastics, which keeps policy attention high. Recycled-content mandates and extended producer responsibility fees accelerate redesign toward mono-material structures, downgauging, tethered caps, and higher recycled input. The EU’s recycling rate of roughly 41% for plastic packaging waste provides a reference point for performance targets and investment priorities. Compliance risk rises for complex, multi-layer structures that struggle in mechanical recycling streams.

Technology adoption strengthens cost control and quality outcomes. AI-enabled demand planning improves inventory turns and reduces changeover waste. Automated vision inspection and robotics raise throughput, lower defect rates, and support traceability in regulated end markets. Digitalization also improves life-cycle accounting, enabling brand owners to compare carbon and recycled-content performance at SKU level. Regionally, Asia-Pacific leads with an estimated 40–45% share, supported by India, Vietnam, and Indonesia as high-growth manufacturing and consumption centers. North America remains a scale market focused on rPET capacity buildouts, while Europe concentrates capital in recycling infrastructure and compliant design. Mexico, Poland, and Southeast Asia stand out as near-term capacity and logistics hubs for multinational packaging supply chains.

, By Material (Polyethylene Terephthalate PET, High Density Polyethylene HDPE, Polypropylene PP, Others), By Production Process (Extrusion, Blow Molding, Thermoforming, Injection Molding, Others), By End-User (Food & Beverage, Household, Healthcare, Personal Care, Others) Industry Global Demand, Strategic Insights, Competitive Landscape, Emerging Technologies, Sustainability Trends, Market Dynamics, Investment Opportunities & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands from 221.3 billion USD, 2023 to 363.9 billion USD, 2033 and delivers 5.1% CAGR, 2026-2034. It maintains scale at estimated: 232.6 billion USD, 2024.

- Segment Dominance: Bottles lead by type at 40.0% share, 2023, supported by high-volume adoption. They sustain demand at estimated: 5.1% CAGR, 2024-2034.

- Segment Dominance: PET dominates materials at estimated: 45.0% share, 2023, driven by barrier performance and recyclability. It supports cost-efficient conversion at estimated: 1.0% yield loss, 2024.

- Driver: Food and beverage leads end use at 28.2% share, 2023, and pulls volumes through safety and shelf-life needs. Packaged consumption growth supports estimated: 3.0% volume growth, 2024.

- Restraint: Policy pressure intensifies as packaging represents 31.0% of global plastic use, 2024. Virgin resin reliance remains high at estimated: 60.0% share, 2024, and raises compliance and cost risk.

- Opportunity: Recycled-content mandates expand investment in rPET and closed-loop systems at estimated: 15.0% recycled-content requirement, 2024. Capacity additions target estimated: 2.0 billion USD, 2026 in recycling and food-grade resin upgrades.

- Trend: Extrusion leads production at estimated: 35.0% share, 2023, and enables consistent, high-throughput rigid formats. Automation and AI lift efficiency at estimated: 8.0% OEE improvement, 2025.

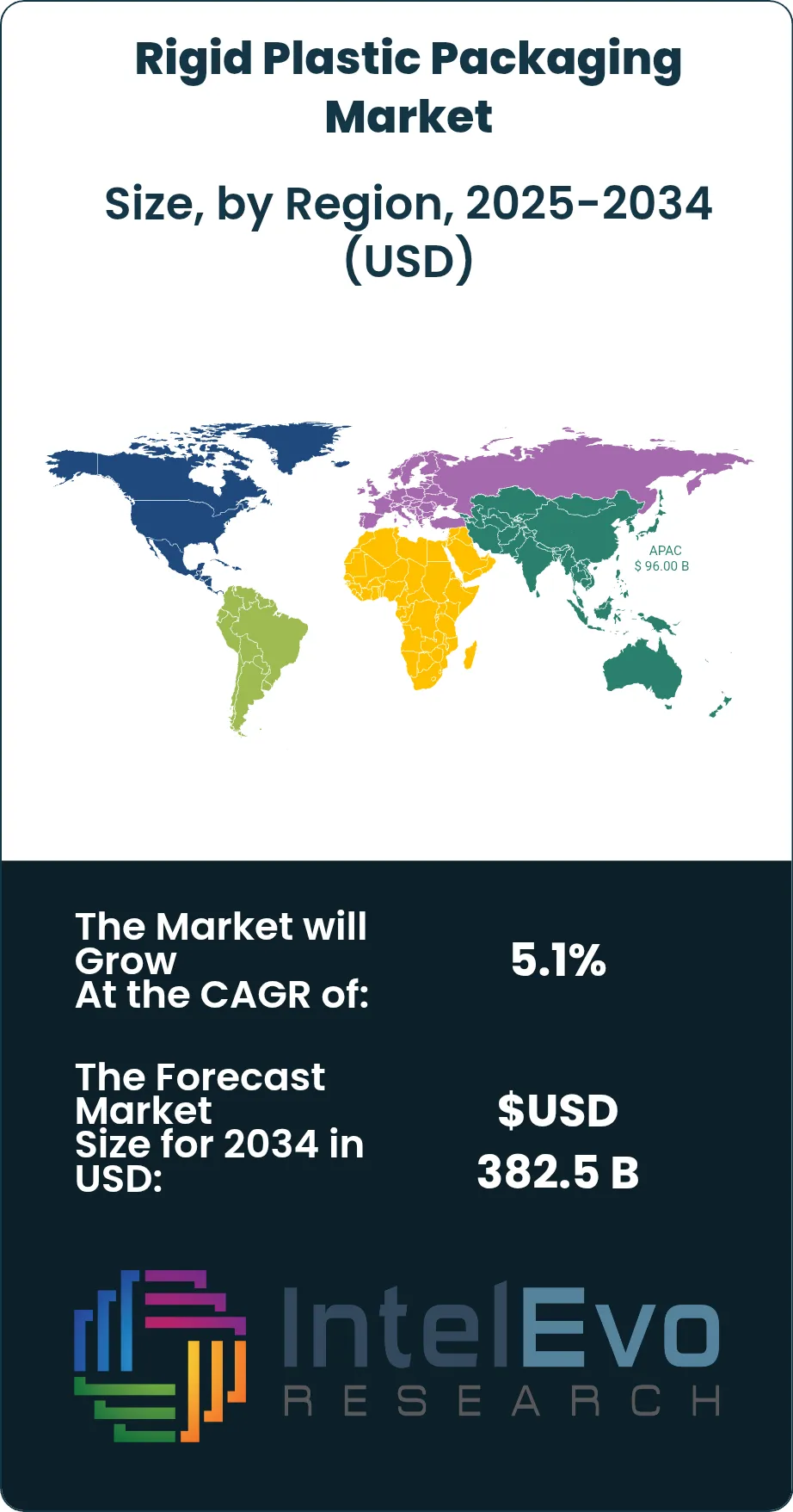

- Regional Analysis: Asia Pacific leads at 43.5% share, 2023, equal to 96.2 billion USD, 2023. Regional growth sustains momentum at estimated: 5.6% CAGR, 2024-2034.

By Type

Bottles remain the largest rigid plastic packaging format as the market moves through 2025, accounting for roughly 40 percent of global demand based on recent industry estimates. Their dominance reflects sustained volume growth in beverages, pharmaceuticals, and personal care products, where high throughput filling lines and standardized shapes favor bottle formats. PET and HDPE bottles continue to replace glass and metal in mass-market applications due to lower transport weight and reduced breakage rates.

Caps and closures form the second largest type segment and play a direct role in product safety and shelf integrity. Demand growth tracks bottled beverage volumes and pharmaceutical packaging output, with tamper-evident and child-resistant designs gaining wider adoption. Containers, including tubs and jars, maintain steady use in food, household chemicals, and industrial goods, supported by their stackability and impact resistance. Other formats such as trays and blister packs serve niche requirements in fresh food, medical devices, and consumer electronics, contributing incremental volume and supporting portfolio diversification.

By Material

Polyethylene terephthalate continues to lead material demand in rigid plastic packaging in 2025, supported by its barrier performance, clarity, and recycling compatibility. PET accounts for an estimated 45 percent of total material consumption, driven primarily by beverages and personal care. Food-grade recycled PET adoption continues to increase, with recycled content levels commonly ranging between 25 and 50 percent in regulated markets.

High-density polyethylene remains critical for applications requiring chemical resistance and durability, including household products and healthcare containers. Polypropylene holds a stable position due to its heat tolerance and suitability for microwave and hot-fill applications. Other materials, including polystyrene and PVC, retain limited but stable demand in applications where rigidity, clarity, or cost considerations outweigh recycling constraints. Material selection increasingly reflects regulatory compliance and lifecycle performance rather than unit cost alone.

By Production Process

Extrusion remains the most widely used production process in rigid plastic packaging, accounting for an estimated one-third of global output in 2025. The process supports continuous production of uniform profiles and sheets used in containers, trays, and closures, which aligns with high-volume manufacturing requirements.

Blow molding continues to underpin bottle and hollow container production, particularly in beverages and healthcare. Thermoforming gains traction in food packaging due to shorter tooling lead times and lower upfront costs, which suit private label and regional brands. Injection molding maintains steady demand for closures and precision components, where dimensional accuracy and repeatability remain critical. Process selection increasingly reflects energy efficiency and scrap reduction targets.

By End-user

Food and beverage remains the largest end-use sector, representing just over 28 percent of rigid plastic packaging demand as of the mid-decade outlook. Growth is supported by packaged food consumption, ready-to-drink beverages, and extended shelf-life requirements. Rigid formats continue to support product safety and logistics efficiency across cold and ambient supply chains.

Household and personal care segments show stable growth, driven by refill-resistant containers and premium packaging designs. Healthcare demand expands at a faster pace due to rising pharmaceutical output and stricter packaging standards. Other end users, including automotive, electronics, and industrial chemicals, rely on rigid plastics for protection during transport and storage, supporting baseline demand.

By Region

Asia Pacific remains the largest regional market, accounting for approximately 43.5 percent of global revenue, equivalent to about USD 96 billion in recent estimates. Growth is supported by population scale, expanding packaged food consumption, and ongoing capacity additions across China, India, and Southeast Asia.

North America and Europe maintain mature but stable demand profiles, shaped by recycling mandates and investments in circular materials. Europe continues to set benchmarks in recycled content usage and waste collection rates, influencing packaging design decisions. Latin America records moderate growth linked to food and beverage expansion and urban retail development. The Middle East and Africa show gradual demand increases, supported by rising packaged goods consumption and investment in modern manufacturing and distribution infrastructure.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Bottles

- Caps and closures

- Containers

- Others

By Material

- Polyethylene terephthalate (PET)

- High density polypropylene (HDPE)

- Polypropylene (PP)

- Others

By Production Process

- Extrusion

- Blow Molding

- Thermoforming

- Injection Molding

- Others

By End-user

- Food and Beverage

- Household

- Healthcare

- Personal Care

- Others

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 244.5 B |

| Forecast Revenue (2034) | USD 382.5 B |

| CAGR (2025-2034) | 5.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Bottles, Caps and closures, Containers, Others), By Material (Polyethylene terephthalate (PET), High density polypropylene (HDPE), Polypropylene (PP), Others), By Production Process (Extrusion, Blow Molding, Thermoforming, Injection Molding, Others), By End-user, Food and Beverage, Household, Healthcare, Personal Care, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Berry Global Inc., ALPLA Werke Alwin Lehner GmbH & Co KG, Sealed Air Corporation, DS Smith Plc, Plastipak Holdings Inc., Sonoco Products Company, Amcor PLC, Silgan Holdings Inc., Klockner Pentaplast Group GmbH & Co. KG, Pactiv Evergreen Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Material (Polyethylene Terephthalate PET, High Density Polyethylene HDPE, Polypropylene PP, Others), By Production Process (Extrusion, Blow Molding, Thermoforming, Injection Molding, Others), By End-User (Food & Beverage, Household, Healthcare, Personal Care, Others) Industry Global Demand, Strategic Insights, Competitive Landscape, Emerging Technologies, Sustainability Trends, Market Dynamics, Investment Opportunities & Forecast 2025–2034")

, By Material (Polyethylene Terephthalate PET, High Density Polyethylene HDPE, Polypropylene PP, Others), By Production Process (Extrusion, Blow Molding, Thermoforming, Injection Molding, Others), By End-User (Food & Beverage, Household, Healthcare, Personal Care, Others) Industry Global Demand, Strategic Insights, Competitive Landscape, Emerging Technologies, Sustainability Trends, Market Dynamics, Investment Opportunities & Forecast 2025–2034")

, By Material (Polyethylene Terephthalate PET, High Density Polyethylene HDPE, Polypropylene PP, Others), By Production Process (Extrusion, Blow Molding, Thermoforming, Injection Molding, Others), By End-User (Food & Beverage, Household, Healthcare, Personal Care, Others) Industry Global Demand, Strategic Insights, Competitive Landscape, Emerging Technologies, Sustainability Trends, Market Dynamics, Investment Opportunities & Forecast 2025–2034")

Frequently Asked Questions

How big is the Rigid Plastic Packaging Market?

Global Rigid Plastic Packaging Market was valued at USD 232.6 billion in 2024 and is projected to reach USD 382.5 billion by 2034, expanding at a CAGR of 5.1%. Explore key trends, drivers, challenges, and future growth outlook.

Who are the major players in the Rigid Plastic Packaging Market?

Berry Global Inc., ALPLA Werke Alwin Lehner GmbH & Co KG, Sealed Air Corporation, DS Smith Plc, Plastipak Holdings Inc., Sonoco Products Company, Amcor PLC, Silgan Holdings Inc., Klockner Pentaplast Group GmbH & Co. KG, Pactiv Evergreen Inc.

Which segments covered the Rigid Plastic Packaging Market?

By Type (Bottles, Caps and closures, Containers, Others), By Material (Polyethylene terephthalate (PET), High density polypropylene (HDPE), Polypropylene (PP), Others), By Production Process (Extrusion, Blow Molding, Thermoforming, Injection Molding, Others), By End-user, Food and Beverage, Household, Healthcare, Personal Care, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Rigid Plastic Packaging Market

Published Date : 07 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date