- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Road Safety Market Size & Forecast 2025–2034 | 16.2% CAGR

Global Road Safety Market Size, Share & Strategic Outlook – By Solution Type (Red Light Enforcement Systems, Speed Enforcement Systems, Incident Detection & Monitoring Systems, Automatic License Plate Recognition (ALPR), Traffic Management Systems, Surveillance Systems), By Service Type (Professional, Consulting & Advisory, Implementation, Managed Services), By End-User (Government & Municipalities, Construction & Infrastructure, Transportation & Logistics), Regional Analysis, Competitive Landscape & Forecast 2025–2034

Report Overview

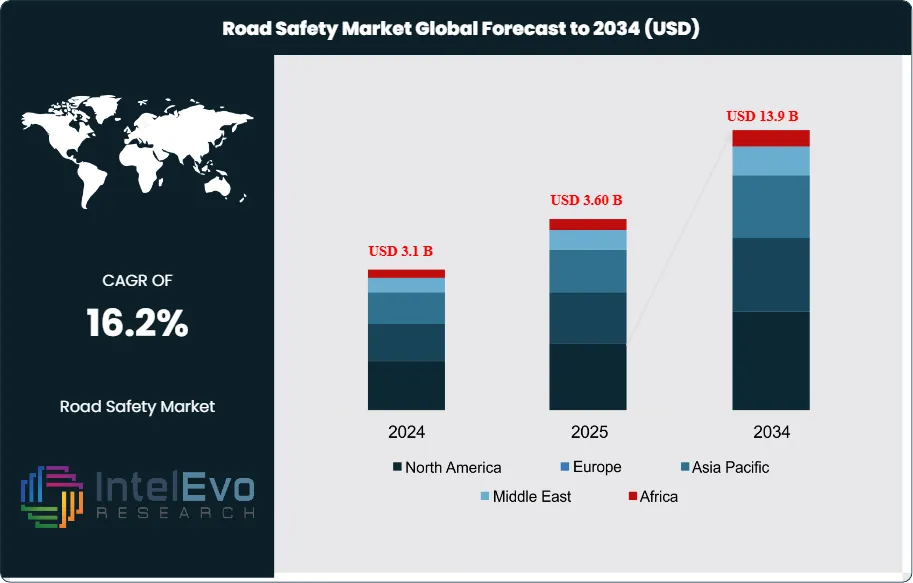

The Global Road Safety Market was valued at approximately USD 3.1 billion in 2024 and is projected to reach nearly USD 13.9 billion by 2034, driven by increasing government investments in smart transportation infrastructure, traffic monitoring systems, and advanced driver safety technologies. Based on the stated growth trajectory, the market size for 2025 is estimated at approximately USD 3.60 billion. From 2026 onward, the market is expected to expand at a compound annual growth rate (CAGR) of approximately 16.2% during 2026–2034, ultimately reaching around USD 13.9 billion by 2034. This growth reflects the mounting urgency to reduce road fatalities and manage rising traffic densities through a combination of regulation, advanced technology, and infrastructure modernization. Demand accelerates as governments, municipalities, and fleet operators prioritize safety outcomes, compliance, and operational efficiency over purely cost-based decision-making.

Get More Information about this report -

Request Free Sample ReportRising vehicle ownership forms a structural demand driver. As of the second quarter of 2024, the United States had approximately 291.1 million vehicles in operation, while the global vehicle fleet is projected to approach 2 billion units by 2035. This expansion strains existing road networks and intensifies the need for intelligent enforcement, adaptive signaling, and real-time monitoring. At the same time, the social and economic cost of accidents remains high. In 2022, the U.S. recorded 42,795 traffic fatalities, corresponding to 1.35 deaths per 100 million vehicle miles traveled, which keeps safety firmly on the policy agenda.

On the supply side, vendors broaden portfolios from traditional signage and barriers to integrated solutions that combine sensors, cameras, connectivity, and analytics. Intelligent transportation systems capable of reducing crashes by up to 80% are gaining traction, supported by advances in artificial intelligence, automation, and digitalization. AI-driven video analytics, automated incident detection, and predictive maintenance reshape how agencies manage risk and allocate resources. Software and analytics are expected to account for roughly 35% of market revenues by 2034, while hardware remains the largest segment at close to 45%, with services such as consulting, training, and managed operations contributing the balance.

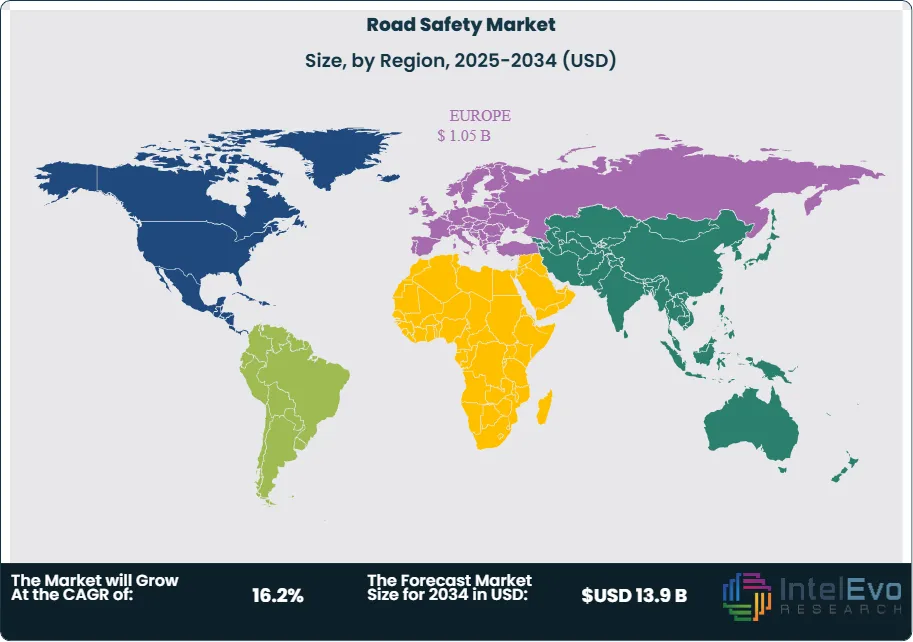

Regulation and public investment anchor the market. Stricter vehicle safety norms, mandatory speed and red-light enforcement, and national road safety strategies stimulate steady funding pipelines. Government and public-sector entities represent more than 70% of spending, complemented by growing participation from logistics firms, ride-hailing platforms, and insurance companies that seek data-driven risk reduction. North America currently contributes an estimated 32% of global revenues, followed by Europe at about 28%, while Asia Pacific is the fastest-growing region, supported by urbanization and large-scale infrastructure programs. Emerging hotspots in South and Southeast Asia, Latin America, and the Middle East offer increasing opportunities for public–private partnerships and scalable technology platforms focused on measurable safety outcomes.

, Traffic Management Systems, Surveillance Systems), By Service Type (Professional, Consulting & Advisory, Implementation, Managed Services), By End-User (Government & Municipalities, Construction & Infrastructure, Transportation & Logistics), Regional Analysis, Competitive Landscape & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Road Safety Market records 3.1 billion USD, 2024 in revenues. It is projected to reach 13.9 billion USD, 2034, representing a CAGR of 16.2%, 2024-2034.

- Segment Dominance: Red Light & Speed Enforcement Systems lead the solution type segment with a 58.3%, 2024 revenue share. This dominance underscores their central role in curbing traffic violations.

- Segment Dominance: Professional Services command an 82.5%, 2024 share of the service type segment. This leadership position highlights the critical importance of expert implementation and integration support for road safety solutions.

- Driver: Government and Municipalities act as the primary demand catalyst, holding a 47.6%, 2024 end-user share. This concentration signals sustained public-sector investment in comprehensive road safety programs.

- Restraint: Budget pressures and slow procurement cycles continue to limit large-scale rollouts. As a result, estimated: 20.0% of planned road safety projects face delays, 2024.

- Opportunity: Vendors can expand by addressing underpenetrated private fleets and smart-city initiatives. These segments represent estimated: 1.5 billion USD, 2034 in additional addressable spending, 2024-2034.

- Trend: Digital enforcement, analytics, and automation increasingly shape road safety deployments. Estimated: 65.0% of new road safety investments, 2028 are expected to embed AI-enabled monitoring and decision support, 2024-2034.

- Regional Analysis: Europe leads the regional landscape with a 29.1%, 2024 market share and 0.9 billion USD, 2024 in revenues. Faster-growing regions outside Europe are projected to contribute estimated: 40.0% of incremental global market expansion, 2024-2034.

By Solution Type

Red light and speed enforcement systems hold a significant position in the 2025 market, accounting for 58.3 percent of global revenues. Their scale reflects continued investment from agencies seeking to reduce violations and improve compliance. Adoption rises as cities upgrade intersections with automated detection tools and as insurance programs tie compliance scores to risk evaluations. The segment is expected to expand steadily through 2030 as governments prioritize measurable outcomes in road safety programs.

Other system categories show meaningful traction. Incident detection and monitoring systems support faster response times and help reduce secondary accidents. Automatic license plate recognition systems record strong demand from tolling authorities and border agencies that require automated identification capabilities. Traffic management systems form the backbone of large urban programs that aim to improve flow and reduce queuing. Surveillance systems continue to scale as operators require wider visibility into traffic patterns and safety events. Together these categories contribute a growing share of investment as cities modernize core infrastructure and shift toward integrated digital monitoring.

Growth across solution types aligns with rising vehicle volumes and higher expectations for reliability. Vendors continue to enhance system accuracy and interoperability to support larger deployments. The combined shift toward automated enforcement and continuous monitoring strengthens the position of these solution types as core components of road safety strategies.

By Service Type

Professional services represent 82.5 percent of service-related revenue in 2025. Agencies depend on advisory, engineering, system design, and integration support to ensure that deployments comply with national safety standards and operate at full capacity. Implementation cycles remain complex, which drives continued demand for specialized expertise and structured project delivery.

Managed services form a smaller but expanding segment. Operators adopt subscription-based monitoring, maintenance, and analytics as a way to reduce operational burdens and maintain system readiness. This approach supports continuous updates to software, sensors, and analytics tools. It also helps agencies manage long-term performance without major capital outlays.

Both service types play a central role as deployments scale. Large programs require structured governance, cybersecurity oversight, and real-time operational support. As a result, service providers remain essential partners in the lifecycle of road safety systems.

By End-Use

Government and municipal agencies represent 47.6 percent of total demand in 2025. Their mandate to manage public safety and reduce crash rates drives recurring investment in enforcement, monitoring, and traffic management platforms. National strategies that target reduced fatalities by 2030 further support the segment.

Construction and infrastructure firms form the next major group of end users. They deploy temporary and permanent safety systems to protect workers, guide traffic around work zones, and comply with regulatory requirements. Demand rises as large transportation programs move forward in North America, Europe, and Asia.

Transportation and logistics companies adopt enforcement and monitoring tools to reduce fleet risk and improve delivery performance. Rising insurance scrutiny and higher claims costs strengthen the business case for in-cab monitoring, automated violation reporting, and route safety analytics. The segment is expected to expand as global freight volumes increase.

By Region

Europe holds 29.1 percent of the market in 2025 with a value of 0.90 billion USD. The region enforces strict compliance standards and invests consistently in roadway modernization. Programs that focus on lowering crash rates and expanding automated enforcement sustain Europe’s leadership. Countries in Western Europe deploy advanced systems at scale, while Eastern Europe shows rising adoption driven by cross-border freight flows.

North America records strong spending as agencies replace legacy systems and adopt automated detection technologies. Investments in federal infrastructure programs support wider deployment across highways and metropolitan corridors. Asia Pacific experiences the fastest growth due to rapid urban expansion, higher traffic density, and national programs aimed at reducing fatalities.

Latin America and the Middle East and Africa gain momentum as funding programs mature and authorities invest in structured enforcement models. Rising urbanization and increased commercial traffic create long-term opportunities for solution and service providers across these regions.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Solution Type

- Red Light Enforcement Systems

- Speed Enforcement Systems

- Incident Detection and Monitoring Systems

- Automatic License Plate Recognition (ALPR) Systems

- Traffic Management Systems

- Surveillance Systems

By Service Type

- Professional Services

- Consulting and Advisory Services

- Implementation Services

- Managed Services

By End-User

- Government and Municipalities

- Construction and Infrastructure Companies

- Transportation and Logistics Companies

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.60 B |

| Forecast Revenue (2034) | USD 13.9 B |

| CAGR (2025-2034) | 16.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Solution Type (Red Light Enforcement Systems, Speed Enforcement Systems, Incident Detection and Monitoring Systems, Automatic License Plate Recognition (ALPR) Systems, Traffic Management Systems, Surveillance Systems), By Service Type (Professional Services, Managed Services), By End-User (Government and Municipalities, Construction and Infrastructure Companies, Transportation and Logistics Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | IDEMIA, Redflex Holdings, Cubic Corporation, FLIR Systems, Inc., Verra Mobility Corporation, SWARCO AG, Motorola Solutions, Inc., Conduent, Inc., Kapsch TrafficCom AG, Jenoptik AG, Siemens Mobility, Sensys Gatso Group AB, Thales Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Traffic Management Systems, Surveillance Systems), By Service Type (Professional, Consulting & Advisory, Implementation, Managed Services), By End-User (Government & Municipalities, Construction & Infrastructure, Transportation & Logistics), Regional Analysis, Competitive Landscape & Forecast 2025–2034")

, Traffic Management Systems, Surveillance Systems), By Service Type (Professional, Consulting & Advisory, Implementation, Managed Services), By End-User (Government & Municipalities, Construction & Infrastructure, Transportation & Logistics), Regional Analysis, Competitive Landscape & Forecast 2025–2034")

, Traffic Management Systems, Surveillance Systems), By Service Type (Professional, Consulting & Advisory, Implementation, Managed Services), By End-User (Government & Municipalities, Construction & Infrastructure, Transportation & Logistics), Regional Analysis, Competitive Landscape & Forecast 2025–2034")

Frequently Asked Questions

How big is the Road Safety Market?

The Global Road Safety Market was valued at USD 3.1 Billion in 2024 and is projected to reach USD 13.9 Billion by 2034, expanding at a CAGR of 16.2% from 2026–2034. Explore key trends in smart traffic management, road monitoring systems, government safety initiatives, and advanced driver safety technologies.

Who are the major players in the Road Safety Market?

IDEMIA, Redflex Holdings, Cubic Corporation, FLIR Systems, Inc., Verra Mobility Corporation, SWARCO AG, Motorola Solutions, Inc., Conduent, Inc., Kapsch TrafficCom AG, Jenoptik AG, Siemens Mobility, Sensys Gatso Group AB, Thales Group

Which segments covered the Road Safety Market?

By Solution Type (Red Light Enforcement Systems, Speed Enforcement Systems, Incident Detection and Monitoring Systems, Automatic License Plate Recognition (ALPR) Systems, Traffic Management Systems, Surveillance Systems), By Service Type (Professional Services, Managed Services), By End-User (Government and Municipalities, Construction and Infrastructure Companies, Transportation and Logistics Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date