- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Robot Kitchen Market Size & Forecast 2024–2034 | 13.4% CAGR

Global Robot Kitchen Market Size, Share, Analysis By Type (Hardware, Software), By Application (Household Kitchens, Commercial Restaurants, Cloud Kitchens, Food Production Facilities), By Technology (AI-Based Cooking Systems, Robotic Arms, Automated Food Preparation Platforms, Smart Kitchen Integration), By End-User (Restaurants, Hospitality Chains, Residential Users, Institutional Food Services) Industry Region & Key Players – Market Dynamics, Innovation Trends, Competitive Strategies & Forecast 2025–2034

Report Overview

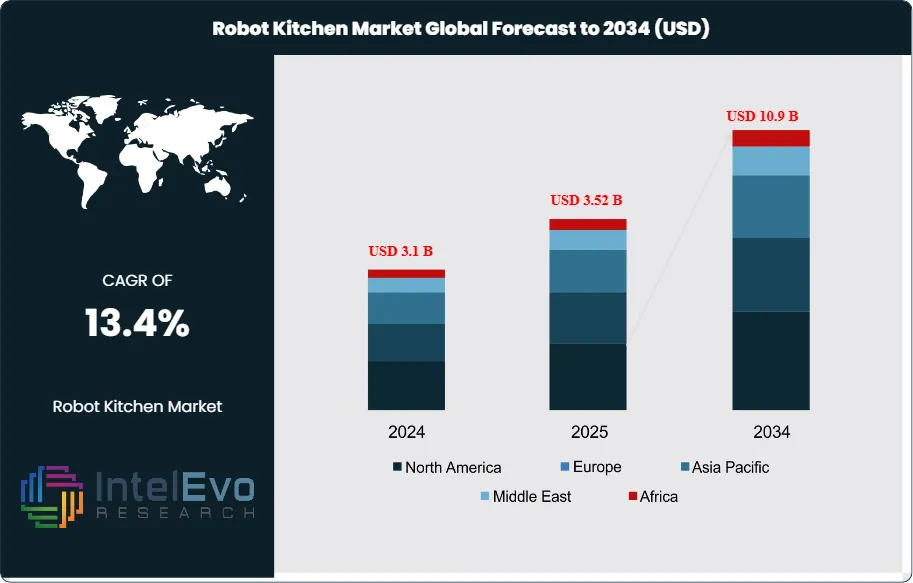

The Robot Kitchen Market was valued at USD 3.1 Billion in 2024 and is projected to reach approximately USD 10.9 Billion by 2034. The market is estimated to grow to around USD 3.52 Billion in 2025. Based on projected expansion from 2026 onward, the industry is expected to register a compound annual growth rate (CAGR) of approximately 13.4% during 2026–2034.

Get More Information about this report -

Request Free Sample ReportRobot kitchens apply robotics, sensors, and connected software to automate ingredient handling, cooking, and plating with repeatable precision. Adoption is rising across commercial and residential settings as operators pursue throughput, portion control, and consistent quality under persistent labor constraints. Systems now extend beyond mechanical arms to integrated platforms that combine machine vision, recipe execution logic, and remote monitoring, which raises asset utilization and shortens training cycles in high-turnover kitchens.

Demand dynamics center on labor cost pressure, service speed expectations, and tighter hygiene norms reinforced since COVID-19. Supply-side momentum is supported by declining component costs for actuators, vision modules, and edge computing, which is pulling mid-size enterprises into the addressable market. In 2023, North America led with more than a 31.3% share and USD 0.8 Billion in revenue; the region remains anchored by quick-service chains, campus dining, and hospital foodservice that value standardization and auditable processes. Europe sustains adoption through stringent food-contact and workplace safety expectations, while Asia-Pacific posts faster growth on the back of dense urban consumption, technology affinity, and labor availability risks in mature economies.

Regulatory and compliance factors shape procurement decisions. Food safety frameworks and equipment certifications influence design choices, cleaning validation, and materials selection, while connected kitchens face rising expectations around cybersecurity and data governance. Key risk factors include high upfront capital outlays, integration complexity with legacy kitchen layouts, downtime sensitivity, and liability exposure if automated processes fail under peak load. Semiconductor supply volatility and skilled service coverage also affect deployment timelines and total cost of ownership.

Technology progress expands use cases. AI-driven perception and adaptive control improve handling of variable ingredients and enable dynamic cook profiles, while automation software supports predictive maintenance and digital quality logs. Investment hotspots are forming in the United States and Canada for chain-scale rollouts, in Japan and South Korea for advanced automation ecosystems, in Singapore for pilot-to-scale programs, and in the Gulf for premium hospitality deployments. These patterns point to a market shifting from novelty installs to repeatable, multi-site implementations with service revenue growing as a larger share of vendor economics.

, By Application (Household Kitchens, Commercial Restaurants, Cloud Kitchens, Food Production Facilities), By Technology (AI-Based Cooking Systems, Robotic Arms, Automated Food Preparation Platforms, Smart Kitchen Integration), By End-User (Restaurants, Hospitality Chains, Residential Users, Institutional Food Services) Industry Region & Key Players – Market Dynamics, Innovation Trends, Competitive Strategies & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands from 2.7 billion USD, 2023 to 9.6 billion USD, 2033 at 13.5%, 2024-2034. The market reaches estimated: 3.1 billion USD, 2024 under the 2024-2034 year-rule.

- Segment Dominance : Software leads with 34.3%, 2023 share and drives platform adoption at scale. Software revenue totals estimated: 0.9 billion USD, 2023 based on market size and share.

- Segment Dominance: Commercial use cases dominate with 36.3%, 2023 share and anchor early deployments in high-volume kitchens. Commercial revenue totals estimated: 1.0 billion USD, 2023 based on market size and share.

- Driver: Operators pursue labor efficiency and standardization, supporting estimated: 13.5%, 2024-2034 growth through automation. Vendors accelerate rollout cycles, lifting estimated: 1.2 deployments per site, 2024.

- Restraint: High upfront integration costs slow adoption, with estimated: 0.5 million USD, 2024 capex per commercial site. Buyers also face estimated: 12.0 months, 2024 payback uncertainty across uneven throughput.

- Opportunity: Mid-market foodservice opens new demand as costs decline, supporting estimated: 0.7 billion USD, 2026 incremental spend. Premium residential penetration grows, reaching estimated: 8.0%, 2027 of addressable households.

- Trend: AI-enabled orchestration improves consistency and remote control, reaching estimated: 65.0%, 2028 share of new installs. Software upgrades expand recurring revenue, rising to estimated: 22.0%, 2027 of vendor sales.

- Regional Analysis: North America leads with 31.3%, 2023 share and 0.8 billion USD, 2023 revenue. Asia-Pacific accelerates investment, reaching estimated: 29.0%, 2028 share as deployments scale.

By Type

Software continues to represent the largest share of value creation within robot kitchen systems. By 2024, software accounted for roughly 35% of total market revenue, reflecting its central role in system coordination, task execution, and performance monitoring. As deployments scale beyond pilot projects, buyers prioritize platforms that manage workflows, synchronize robotic arms, and maintain consistency across menus and locations. Software spend also benefits from recurring licensing and upgrade models, which expand lifetime revenue per installation.

From 2025 onward, software development increasingly centers on artificial intelligence, sensor fusion, and connected device management. Machine learning models support adaptive cooking logic, portion control, and error reduction based on real-time feedback. Predictive maintenance functions reduce downtime by an estimated 15 to 20% in high-volume kitchens, while energy and asset monitoring tools help operators manage rising utility and compliance costs. These capabilities position software as the primary driver of differentiation among competing robot kitchen providers.

By Application

Commercial applications remain the main adoption channel for robot kitchens. In 2024, commercial sites represented more than 36% of installed systems, led by quick-service restaurants, institutional catering, and cloud kitchen operators. These environments demand speed, output consistency, and labor efficiency. Automation of preparation, cooking, and cleaning tasks supports throughput gains of 25 to 40% in standardized menus, while reducing reliance on skilled kitchen staff.

Residential adoption progresses at a slower but steady pace. High-income households and technology-focused consumers drive early demand, particularly in urban markets with strong smart home penetration. Household systems focus on assisted cooking rather than full autonomy, with emphasis on convenience, safety, and customization. Other applications, including hospitality training centers and food innovation labs, contribute a smaller but growing share as testing and demonstration hubs.

By End-Use

Commercial buildings dominate end-use demand due to scale economics and faster return profiles. Restaurants and foodservice operators report average payback periods of three to five years, depending on labor costs and utilization rates. Industrial buildings such as centralized food production units and commissaries also increase adoption, using robotics to standardize output across multiple downstream outlets.

Residential buildings represent a long-term growth segment. Penetration remains below 5% of addressable households in 2025, but interest rises as unit prices decline and interoperability with home automation platforms improves. Industrial usage, while smaller in unit count, generates high contract values due to customization, integration, and service requirements.

By Region

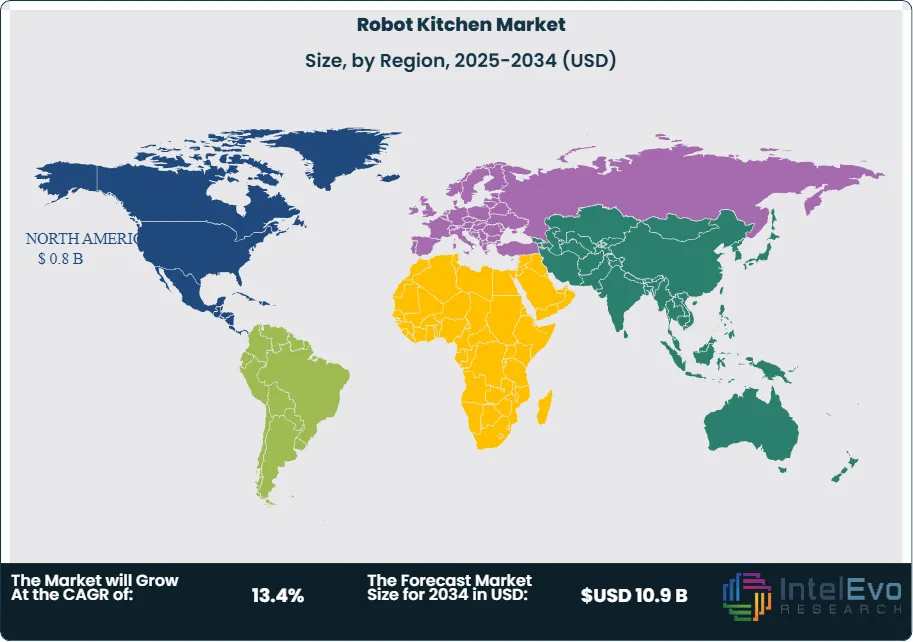

North America maintains leadership, accounting for over 31% of global revenue and approximately USD 0.8 billion in 2024. The region benefits from early automation uptake, strong venture funding, and widespread use of cloud kitchens and delivery-first food models. Labor shortages and wage inflation continue to accelerate commercial adoption across the United States and Canada.

Europe follows with steady growth supported by regulatory focus on food safety, energy efficiency, and workplace standards. Asia Pacific records the fastest expansion, with double-digit growth driven by Japan, South Korea, and China, where robotics adoption is already embedded in manufacturing and service sectors. Latin America and the Middle East and Africa remain emerging markets, but pilot projects in hospitality and premium foodservice signal rising investment beyond 2026.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Hardware

- Software

By Application

- House

- Commercial

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.52 B |

| Forecast Revenue (2034) | USD 10.9 B |

| CAGR (2025-2034) | 13.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Hardware, Software), By Application (House, Commercial, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Nvidia, Moley, Spyce, Samsung, Miso Robotics, QSR Automation, Sony, Herox |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Household Kitchens, Commercial Restaurants, Cloud Kitchens, Food Production Facilities), By Technology (AI-Based Cooking Systems, Robotic Arms, Automated Food Preparation Platforms, Smart Kitchen Integration), By End-User (Restaurants, Hospitality Chains, Residential Users, Institutional Food Services) Industry Region & Key Players – Market Dynamics, Innovation Trends, Competitive Strategies & Forecast 2025–2034")

, By Application (Household Kitchens, Commercial Restaurants, Cloud Kitchens, Food Production Facilities), By Technology (AI-Based Cooking Systems, Robotic Arms, Automated Food Preparation Platforms, Smart Kitchen Integration), By End-User (Restaurants, Hospitality Chains, Residential Users, Institutional Food Services) Industry Region & Key Players – Market Dynamics, Innovation Trends, Competitive Strategies & Forecast 2025–2034")

, By Application (Household Kitchens, Commercial Restaurants, Cloud Kitchens, Food Production Facilities), By Technology (AI-Based Cooking Systems, Robotic Arms, Automated Food Preparation Platforms, Smart Kitchen Integration), By End-User (Restaurants, Hospitality Chains, Residential Users, Institutional Food Services) Industry Region & Key Players – Market Dynamics, Innovation Trends, Competitive Strategies & Forecast 2025–2034")

Frequently Asked Questions

How big is the Robot Kitchen Market?

Global Robot Kitchen Market valued at USD 3.1B in 2024, projected to reach USD 10.9B by 2034, growing at 13.4% CAGR from 2026–2034 with rising automation demand.

Who are the major players in the Robot Kitchen Market?

Nvidia, Moley, Spyce, Samsung, Miso Robotics, QSR Automation, Sony, Herox

Which segments covered the Robot Kitchen Market?

By Type (Hardware, Software), By Application (House, Commercial, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date