- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Robot Simulation Software Market Size, Share & Forecast | CAGR 20.7%

Global Robot Simulation Software Market Size, Share, Analysis By Software Type (Industrial Robots, Service Robotics, Collaborative Cobots, Autonomous Mobile Robots [AMRs]), By Component (Software Licences, Maintenance Services), By Deployment Mode (Cloud-Based SaaS, On-Premises Systems), By Enterprise Size (SMEs, Large Industrial Plants) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 4.5 Billion | USD 24.5 Billion | 20.7% | North America, 36.0% |

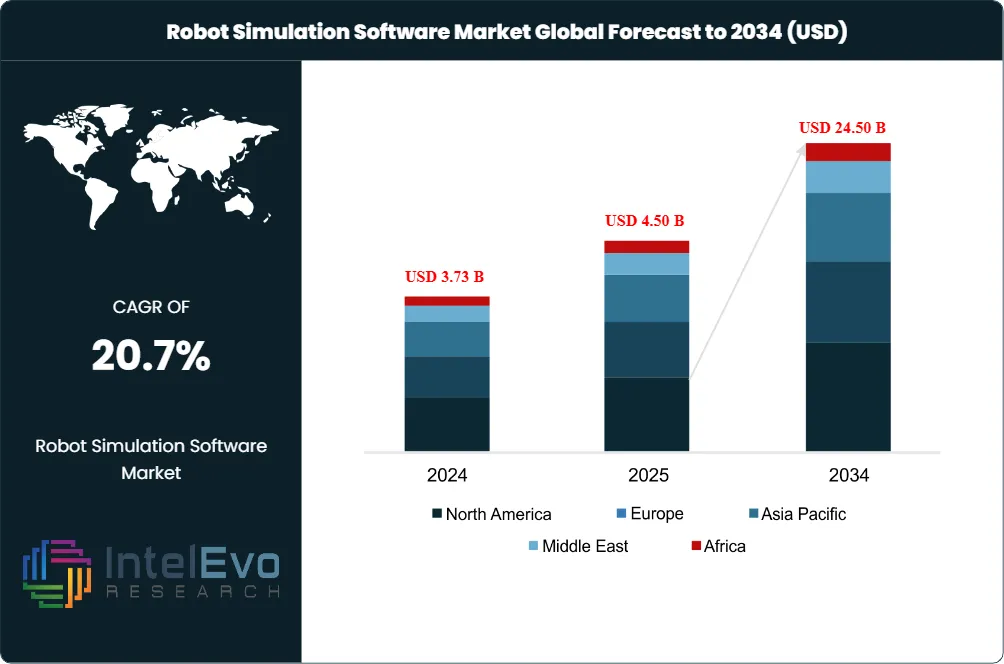

The Robot Simulation Software Market was valued at USD 3.73 Billion in 2024 and USD 4.50 Billion in 2025. The market is projected to reach USD 24.50 Billion by 2034, expanding at a CAGR of 20.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 20.0 Billion over the analysis period, more than five times the 2025 base. The Robot Simulation Software Market is being driven by the simulation-first deployment doctrine adopted by humanoid, industrial, and autonomous-vehicle programs, where teams build digital twins of factories or warehouses and train robot policies in physics-accurate virtual environments before any hardware leaves the lab.

Get More Information about this report -

Request Free Sample ReportThree structural drivers anchor Robot Simulation Software Market expansion through 2034. First, NVIDIA released general availability for Isaac Sim 5.0 and Isaac Lab 2.2 at SIGGRAPH 2025 on GitHub under Apache 2.0, lowering the barrier for synthetic data generation and reinforcement learning across humanoid, mobile, and manipulator programs. Second, the International Federation of Robotics reported China at 470 robots per 10,000 manufacturing employees in 2023, up from 402 in 2022, with 51% global share of industrial robot installations and 276,288 units deployed, sustaining demand for offline programming and simulation across automotive, electronics, and metalworking lines. Third, humanoid commercialization went from prototype to production in January 2026 when Boston Dynamics unveiled the production Atlas at CES 2026 with all 2026 capacity committed to Hyundai's Robotics Metaplant Application Center (RMAC) and Google DeepMind.

Simulation-first deployment is the methodology underlying every leading humanoid program. Figure AI trains Figure 02 in physics-accurate environments before deploying at BMW's Spartanburg plant; Hyundai data feeds the RMAC for Atlas training; and the Newton physics engine, co-developed by Google DeepMind, Disney Research, and NVIDIA and managed by the Linux Foundation, is now available in beta as an open-source GPU-accelerated foundation. NVIDIA Cosmos generates synthetic 3D data, NVIDIA Omniverse Replicator handles randomization, and Isaac Lab handles reinforcement learning, creating a layered open stack that competes against proprietary suites from Siemens, ABB, and FANUC.

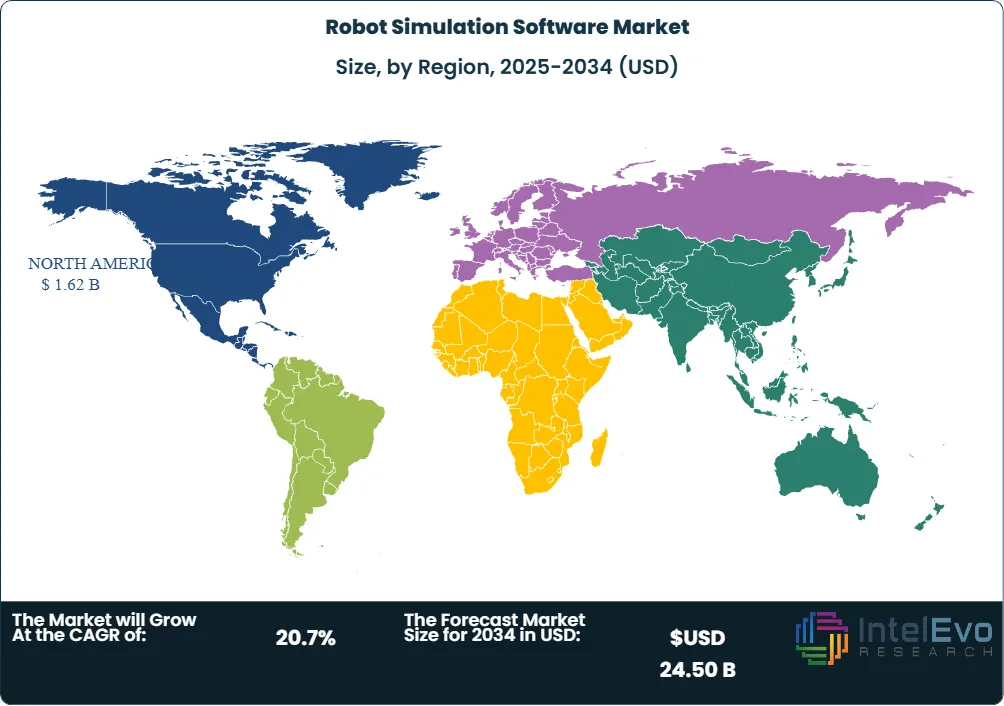

North America led the Robot Simulation Software Market with 36.0% revenue share in 2025, anchored by NVIDIA, Boston Dynamics, Microsoft, Autodesk, Rockwell Automation, and the Open Source Robotics Foundation. Europe sustains durable growth because Siemens AG, ABB Ltd., KUKA AG, Dassault Systèmes, and Wandelbots concentrate R&D in Germany, Switzerland, France, and Sweden. Asia Pacific is the fastest-growing region because China's industrial robot software market reached USD 5.26 Billion in 2025, supported by 190,000 industrial robot deployments with AI-driven software per industry analysis, and Japan and South Korea anchor FANUC, Yaskawa, Mitsubishi Electric, and Hyundai-affiliated programs. The forward outlook through 2034 favors physics-accurate platforms that combine GPU acceleration, OpenUSD scene description, and ROS 2 integration.

Market Definition & Scope

The Robot Simulation Software Market is defined as software platforms, frameworks, and cloud services that model, simulate, train, validate, and deploy industrial, mobile, humanoid, and service robots in physics-accurate virtual environments. The market encompasses offline programming software, digital twin platforms, reinforcement-learning frameworks, synthetic data generation tools, and ROS-integrated simulation packages, plus the services that customize, integrate, and maintain these platforms across automotive, logistics, electronics, healthcare, and aerospace customers.

This analysis includes brand-specific platforms such as ABB RobotStudio, FANUC ROBOGUIDE, KUKA Sim Pro, and Yaskawa MotoSim alongside vendor-neutral platforms including NVIDIA Isaac Sim, Siemens Process Simulate, Dassault Systèmes DELMIA, Visual Components, RoboDK, and Coppelia Robotics CoppeliaSim. The scope explicitly excludes general-purpose CAD systems unrelated to robot kinematics, video-game physics engines without robotics SDKs, and pure analytical mechanical-design tools. The Robot Simulation Software Market sits within the broader robot software category, accounting for an estimated 18-22% of global robot software spend in 2025.

![Global Robot Simulation Software Market Size, Share, Analysis By Software Type (Industrial Robots, Service Robotics, Collaborative Cobots, Autonomous Mobile Robots [AMRs]), By Component (Software Licences, Maintenance Services), By Deployment Mode (Cloud-Based SaaS, On-Premises Systems), By Enterprise Size (SMEs, Large Industrial Plants) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034](storage/Key-takeaway.webp "Global Robot Simulation Software Market Size, Share, Analysis By Software Type (Industrial Robots, Service Robotics, Collaborative Cobots, Autonomous Mobile Robots [AMRs]), By Component (Software Licences, Maintenance Services), By Deployment Mode (Cloud-Based SaaS, On-Premises Systems), By Enterprise Size (SMEs, Large Industrial Plants) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Robot Simulation Software Market grows from USD 4.5 Billion in 2025 to USD 24.5 Billion by 2034 at a CAGR of 20.7%, generating USD 20.0 Billion in absolute new revenue.

- Segment Dominance: Solutions captured 71.0% of the Robot Simulation Software Market in 2025, equivalent to USD 3.20 Billion, as buyers prioritize integrated software over standalone advisory services.

- Segment Dominance: Industrial Robotics led applications with 45.0% share in 2025 per industry analysis, anchored by automotive, electronics, and metalworking customers using ABB RobotStudio, FANUC ROBOGUIDE, and Siemens Process Simulate.

- Driver: NVIDIA released general availability for Isaac Sim 5.0 and Isaac Lab 2.2 at SIGGRAPH 2025, with Isaac Sim now licensed under Apache 2.0 on GitHub, opening physics-accurate simulation to the entire ROS 2 developer base.

- Restraint: Initial license costs of USD 5,000 to USD 30,000 per seat for proprietary suites and steep learning curves on Universal Scene Description (USD), URDF, and ROS 2 limit adoption among small and medium manufacturers.

- Opportunity: Humanoid robot training represents a USD 6 Billion forecast opportunity by 2034, illustrated by Boston Dynamics-DeepMind's Atlas program, Figure AI's BMW Spartanburg deployment, and Hyundai's planned 30,000 humanoids per year capacity by 2028.

- Trend: Generative-AI-powered synthetic data generation is replacing manual scene creation; NVIDIA Cosmos, Omniverse Replicator, and the Newton open-source physics engine collectively shrink data-collection cycles from weeks to hours.

- Regional: North America held 36.0% Robot Simulation Software Market share in 2025 at USD 1.62 Billion, with the United States contributing approximately USD 1.30 Billion or roughly 80% of the regional total.

Key Insights Summary

- Boston Dynamics unveiled the production Atlas humanoid at CES 2026 on 5 January 2026, with the entire 2026 production capacity committed to Hyundai's Robotics Metaplant Application Center (RMAC) and Google DeepMind, validating simulation-first humanoid deployment doctrine.

- NVIDIA released general availability for Isaac Sim 5.0 and Isaac Lab 2.2 at SIGGRAPH 2025 on GitHub under Apache 2.0, with Isaac Sim built on NVIDIA Omniverse and supporting URDF, MJCF, and CAD-based robot import.

- China deployed 276,288 industrial robots in 2023, holding 51% of global industrial robotic software installations and reaching 470 robots per 10,000 employees, per the International Federation of Robotics World Robotics 2024 report.

- Newton, an open-source GPU-accelerated physics engine co-developed by Google DeepMind, Disney Research, and NVIDIA and managed by the Linux Foundation, entered beta in 2025, providing a vendor-neutral foundation for robot learning platforms including MuJoCo Playground and Isaac Lab.

- Hyundai disclosed a USD 26 Billion US manufacturing investment supporting Boston Dynamics, with a planned annual production capacity of 30,000 Atlas humanoids per year from a single factory by 2028, lifting downstream simulation-software demand.

- Microsoft and Hexagon Robotics announced a strategic partnership at CES 2026 on 6 January 2026 combining Microsoft Azure cloud and AI capabilities with Hexagon's spatial intelligence to scale industrial humanoid robots, including Hexagon's AEON platform.

- NEURA Robotics introduced the third-generation 4NE1 Gen 3 humanoid robot in January 2026 with full digital twin integration via the Neuraverse ecosystem, advancing skill transfer and multi-task learning across cooperating units.

Competitive Landscape Overview

The Robot Simulation Software Market is moderately consolidated, with the top four vendors NVIDIA Corporation, Siemens AG, ABB Ltd., and Dassault Systèmes estimated to hold a combined 38-44% share of disclosed enterprise simulation revenue in 2025. Competition is bifurcating between two patterns: brand-specific suites (FANUC ROBOGUIDE, ABB RobotStudio, KUKA Sim Pro, Yaskawa MotoSim) that deliver highest fidelity for one robot family, and vendor-neutral platforms (NVIDIA Isaac Sim, Siemens Process Simulate, Dassault DELMIA, Visual Components, RoboDK) that simulate multiple robot brands inside a unified scene.

Competitive evolution is moving toward open standards, with Universal Scene Description (OpenUSD) emerging as the lingua franca for robot scene exchange and ROS 2 acting as the runtime backbone. NVIDIA Isaac Sim is now licensed open-source under Apache 2.0 and hosted on GitHub, pressuring proprietary suites to expose APIs and asset libraries. Specialist challengers Wandelbots (NOVA), Coppelia Robotics, RoboDK, and Open Robotics (Gazebo) are gaining traction in research and integrator workflows.

The competitive matrix below summarizes leading players in the Robot Simulation Software Market, their headquarters, market position, primary product offering, geographic strength, and the most recent strategic move verified through public disclosures during the trailing 18 months.

Competitive Landscape Matrix

| Company | HQ Country | Position | Key Product | Geographic Strength | Recent Strategic Move (Trailing 18 Months) |

|---|---|---|---|---|---|

| NVIDIA Corporation | USA | Leader | Isaac Sim, Isaac Lab, Omniverse, Cosmos | Global | GA of Isaac Sim 5.0 and Isaac Lab 2.2 at SIGGRAPH 2025 under Apache 2.0 |

| Siemens AG | Germany | Leader | Process Simulate, Tecnomatix, NX MCD | EU, North America, APAC | Expanded Process Simulate to integrate FANUC RCS and CAD-to-Path workflows (2025) |

| ABB Ltd. | Switzerland | Leader | RobotStudio with Virtual Controller | Global | Continued RobotStudio updates with Augmented Reality and Stop Position Simulation (2025) |

| Dassault Systèmes | France | Leader | DELMIA Robot Programmer, 3DEXPERIENCE | EU, North America | Integrated DELMIA with 3DEXPERIENCE cloud workflows (2025) |

| FANUC Corporation | Japan | Challenger | ROBOGUIDE with HandlingPRO, WeldPRO, PaintPRO | Japan, North America, EU | Launched ROBOGUIDE v10 enhancements covering virtual reality (2025) |

| KUKA AG | Germany | Challenger | KUKA Sim Pro, KUKA.OfficeLite | EU, North America, China | Continued KUKA Sim Pro updates with KRL editor (2025) |

| Yaskawa Electric | Japan | Challenger | MotoSim EG-VRC | APAC, North America | Integrated MotoSim with new MotoCom programming SDK (2025) |

| Microsoft Corporation | USA | Challenger | Azure cloud + Hexagon partnership | Global cloud | Strategic partnership with Hexagon Robotics for AEON industrial humanoids (Jan 2026) |

| Autodesk Inc. | USA | Niche Player | Fusion 360, Inventor with simulation | North America, EU | Continued Fusion 360 robotics extensions for SMEs (2025) |

| RoboDK | Canada | Niche Player | RoboDK with 70+ post-processors | Global, integrators | Expanded support to over 40 robot brands and CAD-to-path workflows (2025) |

Segmentation Analysis

The Robot Simulation Software Market segments along five primary axes: by component, by deployment mode, by application, by end-user vertical, and by robot type. Segment shares below are aggregated from disclosed company filings, regulator submissions, and trade body data, then normalized to sum to 100% within each category.

By Component

Solutions captured 71.0% of the Robot Simulation Software Market in 2025, equivalent to USD 3.20 Billion, while Services held 29.0% or USD 1.31 Billion. Solutions dominate because integrators and end users prioritize integrated software platforms that combine kinematics solvers, physics engines, sensor models, and post-processors for multiple robot brands. NVIDIA Isaac Sim, Siemens Process Simulate, ABB RobotStudio, and Dassault DELMIA are bought primarily as software licenses with optional services attach.

The Services segment grows at approximately 22% CAGR because customers increasingly outsource scene authoring, sim-to-real calibration, and digital twin maintenance to system integrators and consulting firms. Robot simulation software ROI calculation typically requires 3-6 months of configuration before commissioning gains materialize, sustaining services attach above 0.40 of total contract value. Solution buyers prioritize OpenUSD compatibility, ROS 2 bridges, and CAD-to-path workflows; service buyers prioritize sim-to-real transfer expertise and SI partnerships.

By Deployment Mode

On-premises deployments held 60.0% of Robot Simulation Software Market revenue in 2025, totaling USD 2.70 Billion, while Cloud-based deployments held 40.0% or USD 1.80 Billion. On-premises retains majority share because automotive OEMs and aerospace primes require local control over CAD assets, factory layouts, and proprietary robot programs. ABB RobotStudio, FANUC ROBOGUIDE, and KUKA Sim Pro continue to ship as workstation installs.

Cloud-based deployment grows fastest at approximately 24% CAGR through 2034 because GPU-intensive workloads, including reinforcement learning at scale and large-batch synthetic data generation, are uneconomic on local hardware. NVIDIA Omniverse Cloud, Microsoft Azure (now reinforced by the Hexagon Robotics partnership announced 6 January 2026), and AWS RoboMaker support elastic compute. Cloud RBF buyers prioritize 99.9% API uptime, OpenUSD asset streaming, and tight integration with NVIDIA Cosmos for pre-trained world models.

By Application

Industrial Robotics led Robot Simulation Software Market applications with 45.0% share in 2025, equivalent to USD 2.03 Billion, followed by Research and Education at 22.0% (USD 0.99 Billion), Autonomous Vehicles and Drones at 15.0% (USD 0.68 Billion), Medical Robotics at 11.0% (USD 0.50 Billion), and Other applications including humanoids, agriculture, and inspection at 7.0% (USD 0.31 Billion). Industrial Robotics dominates because automotive welding, painting, and assembly cells generate the largest seat count for ABB RobotStudio, ROBOGUIDE, and Process Simulate.

Autonomous Vehicles and Drones is the fastest-growing application at approximately 24% CAGR because regulatory testing, sensor calibration, and edge-case scenario coverage require simulation at miles-driven scale. Cosmos pre-trained world models, NVIDIA DRIVE Sim, CARLA, and Microsoft AirSim anchor this segment. Medical Robotics adoption rises through digital twin training for surgical robots from Intuitive Surgical, Medtronic Hugo, and CMR Surgical Versius. Research and Education benefits from open-source platforms including Gazebo, MuJoCo, and the Newton physics engine.

By End-User Vertical

Manufacturing held approximately 38.0% of Robot Simulation Software Market end-user spend in 2025, totaling USD 1.71 Billion, followed by Automotive at 21.0% (USD 0.95 Billion), Aerospace and Defense at 14.0% (USD 0.63 Billion), Healthcare at 11.0% (USD 0.50 Billion), Education and Research at 9.0% (USD 0.41 Billion), and Logistics, agriculture, and other verticals at 7.0% (USD 0.31 Billion). Manufacturing dominates because Tier 1 suppliers including Foxconn, Magna International, and Siemens use simulation for line-balancing, virtual commissioning, and ROI calculation before capital release.

Aerospace and Defense is forecast to grow fastest among major verticals at approximately 23% CAGR because Boeing, Airbus, Lockheed Martin, and Raytheon expand robotic riveting, drilling, and inspection cells using ABB, KUKA, and FANUC robots. Healthcare RBF benefits from Intuitive Surgical's da Vinci 5, Medtronic Hugo, and CMR Surgical Versius programs that train clinicians inside simulation before live procedures. Logistics RBF expansion is anchored by Amazon Robotics, Symbotic, and AutoStore deploying mobile robots whose path planning is validated in simulation before warehouse rollout.

By Robot Type

Industrial robot simulation captured 65.0% of Robot Simulation Software Market spend in 2025 at USD 2.93 Billion, mobile and autonomous robots held 18.0% at USD 0.81 Billion, humanoid robots held 9.0% at USD 0.41 Billion, and surgical or service robots held 8.0% at USD 0.36 Billion. Humanoid simulation grows fastest at approximately 28% CAGR through 2034 because Boston Dynamics Atlas, Figure 02, Tesla Optimus, NEURA 4NE1, and AgiBot A2 programs all rely on simulation-first training methodology. Manufacturers use NVIDIA Isaac Sim, the Newton physics engine, and proprietary digital twins to accumulate millions of synthetic interaction hours before hardware deployment.

Regional Analysis

The Robot Simulation Software Market demonstrates sharp regional differentiation in 2025, anchored by North America at 36.0% share, Europe at 28.0%, Asia Pacific at 26.0%, Latin America at 5.0%, and Middle East and Africa at 5.0%. Regional shares sum to 100% of 2025 revenue.

North America

North America held 36.0% of the Robot Simulation Software Market in 2025, generating USD 1.62 Billion. The United States accounted for approximately 80% of the regional total at USD 1.30 Billion, anchored by NVIDIA, Boston Dynamics, Microsoft, Autodesk, Rockwell Automation, and the Open Source Robotics Foundation. Canada hosts Clearpath Robotics (now part of Rockwell Automation) and RoboDK at approximately USD 0.18 Billion. The Federal Aviation Administration's drone Beyond Visual Line of Sight rulemaking and the Department of Defense's Robotic and Autonomous Systems Strategy continue to anchor government-funded simulation contracts. NVIDIA's headquarters in Santa Clara, Boston Dynamics in Waltham, Massachusetts, and Microsoft in Redmond concentrate North American R&D investment.

Europe

Europe held 28.0% Robot Simulation Software Market share in 2025 at USD 1.26 Billion, led by Germany, France, Switzerland, the United Kingdom, and Sweden. Germany hosts Siemens AG, KUKA AG, NEURA Robotics, and Wandelbots, while Switzerland anchors ABB Ltd. and France hosts Dassault Systèmes. The European Commission's Horizon Europe robotics calls and the EU Machinery Regulation (Regulation 2023/1230, applying from 14 January 2027) accelerate digital twin and risk-assessment workflows. Germany's industrial robot software market is forecast to reach USD 12.2 Billion by 2034 per industry analysis, anchored by automotive Tier 1 suppliers and Mittelstand machine builders. Wandelbots NOVA integration with NVIDIA Isaac Sim, announced at NVIDIA Omniverse 2025, illustrates the cross-Atlantic technology integration.

Asia Pacific

Asia Pacific held 26.0% Robot Simulation Software Market share in 2025 at USD 1.17 Billion, with China, Japan, South Korea, and India driving most regional spend. China deployed 276,288 industrial robots in 2023 (51% of global installations) per the International Federation of Robotics World Robotics 2024 report, with the China industrial robot software market reaching USD 5.26 Billion in 2025 per industry analysis. Japan anchors FANUC Corporation, Yaskawa Electric, Kawasaki Heavy Industries, and DENSO Robotics, all of which ship branded simulation suites bundled with their hardware. South Korea hosts Hyundai's Robotics Metaplant Application Center (RMAC) opening in 2026 to train Boston Dynamics Atlas. India is forecast to grow at over 22% country CAGR, supported by Make in India robotics manufacturing incentives.

Latin America

Latin America held 5.0% Robot Simulation Software Market share in 2025 at USD 0.23 Billion. Brazil leads regional demand because Volkswagen, Stellantis, and General Motors operate large welding, painting, and assembly lines around São Paulo, Curitiba, and Belo Horizonte using ABB and KUKA robots. Mexico hosts Tier 1 automotive suppliers including Magna International, Lear, and Yazaki across Monterrey, Saltillo, and Querétaro, all of which use simulation for cell design and offline programming. Argentina and Chile remain underpenetrated due to lower industrial robotics density, though aerospace and mining adopters are emerging.

Middle East and Africa

Middle East and Africa held 5.0% Robot Simulation Software Market share in 2025 at USD 0.23 Billion. The United Arab Emirates and Saudi Arabia push robotics adoption inside Vision 2030 manufacturing and logistics targets, with NEOM, ADNOC, and Saudi Aramco running pilots that include simulation-first design. Israel anchors Mobileye autonomous-driving simulation and Cogniteam mobile robot programming. South Africa's automotive plants for BMW Group, Toyota, and Ford in Rosslyn and Durban deploy ABB and KUKA robots whose offline programming uses RobotStudio and Sim Pro. Africa-wide adoption remains nascent but growing under Smart Africa digital transformation programs.

Country Analysis

Country-level dynamics in the Robot Simulation Software Market diverge sharply because each jurisdiction enforces distinct rule sets and houses different vendor concentrations.

United States

The United States Robot Simulation Software Market reached USD 1.30 Billion in 2025 and is projected to expand at a country-specific CAGR of 21.0% through 2034. Demand is anchored by NVIDIA Isaac Sim adoption across Boston Dynamics, Figure AI, Tesla Optimus, and 1X Technologies humanoid programs, plus Amazon Robotics, Symbotic, and Microsoft Hexagon partnerships in industrial logistics. The Federal Aviation Administration's drone simulation requirements and the Department of Defense's Robotic and Autonomous Systems Strategy continue to drive government-funded simulation contracts. NVIDIA disclosed the Newton open-source physics engine in 2025, co-developed with Google DeepMind and Disney Research and managed by the Linux Foundation.

Germany

The Germany Robot Simulation Software Market reached approximately USD 0.55 Billion in 2025 and is forecast at a 19.5% country CAGR through 2034. Germany hosts Siemens AG, KUKA AG, NEURA Robotics, Wandelbots, and Festo, all of which ship simulation suites used by Volkswagen Group, BMW Group, Mercedes-Benz Group, and Bosch. The Industrie 4.0 framework and the EU Machinery Regulation 2023/1230 (applying from 14 January 2027) require digital risk assessment that increasingly relies on simulation. NEURA Robotics introduced 4NE1 Gen 3 in January 2026 with Neuraverse digital twin integration.

China

The China Robot Simulation Software Market reached approximately USD 0.42 Billion in 2025 and is forecast at a 23.3% country CAGR through 2034 per industry analysis, the fastest among major economies. China deployed 276,288 industrial robots in 2023 with 51% global share per IFR data, and the China industrial robot software market reached USD 5.26 Billion in 2025. Domestic players including AgiBot (Shanghai-based, unveiled A2 Series at CES 2026), Unitree Robotics, and EX-Robots compete alongside FANUC, ABB, and Yaskawa for simulation-software seats. The Made in China 2025 plan and the 14th Five-Year Plan robotics targets anchor government-supported demand.

Japan

The Japan Robot Simulation Software Market reached approximately USD 0.31 Billion in 2025 and is forecast at a 17.0% country CAGR through 2034. Japan hosts FANUC Corporation in Oshino, Yaskawa Electric in Kitakyushu, Kawasaki Heavy Industries, DENSO Robotics, and Mitsubishi Electric, all of which ship branded simulation suites including ROBOGUIDE, MotoSim, K-Roset, and ORiN. Japanese manufacturers including Toyota, Honda, and Toyota Industries use Process Simulate, ROBOGUIDE, and MotoSim across automotive, electronics, and material handling lines. The Society 5.0 framework and METI's robot strategy support continued simulation-software investment.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Component

- Software

- Simulation and Modeling Software

- Offline Programming Software

- Virtual Commissioning Software

- Digital Twin Software

- Robot Path Planning and Optimization Software

- Visualization and Analytics Software

- AI and Machine Learning-Based Simulation Software

- Others

- Services

- Consulting Services

- Integration and Deployment Services

- Training and Education Services

- Support and Maintenance Services

- Managed Services

By Deployment Model

- Cloud-Based Deployment

- On-Premises Deployment

- Hybrid Deployment

By Application

- Robot Design and Development

- Offline Programming

- Virtual Commissioning

- Digital Twin and Process Simulation

- Production Planning and Optimization

- Material Handling Simulation

- Welding Simulation

- Assembly Line Simulation

- Pick-and-Place Operations Simulation

- Inspection and Quality Control Simulation

- Training and Skill Development

- Research and Development

- Others

By End-User Vertical

- Automotive

- Electronics and Semiconductor

- Aerospace and Defense

- Healthcare and Medical Devices

- Food and Beverage

- Logistics and Warehousing

- Manufacturing

- Metals and Machinery

- Energy and Utilities

- Retail and E-commerce

- Education and Research

- Pharmaceuticals and Biotechnology

- Construction

- Others

By Robot Type

- Articulated Robots

- Collaborative Robots (Cobots)

- SCARA Robots

- Cartesian Robots

- Delta Robots

- Cylindrical Robots

- Autonomous Mobile Robots (AMRs)

- Automated Guided Vehicles (AGVs)

- Humanoid Robots

- Industrial Service Robots

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.50 B |

| Forecast Revenue (2034) | USD 24.50 B |

| CAGR (2025-2034) | 20.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Software, Services), By Deployment Model, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment), By Application, (Robot Design and Development, Offline Programming, Virtual Commissioning, Digital Twin and Process Simulation, Production Planning and Optimization, Material Handling Simulation, Welding Simulation, Assembly Line Simulation, Pick-and-Place Operations Simulation, Inspection and Quality Control Simulation, Training and Skill Development, Research and Development, Others), By End-User Vertical, (Automotive, Electronics and Semiconductor, Aerospace and Defense, Healthcare and Medical Devices, Food and Beverage, Logistics and Warehousing, Manufacturing, Metals and Machinery, Energy and Utilities, Retail and E-commerce, Education and Research, Pharmaceuticals and Biotechnology, Construction, Others), By Robot Type, (Articulated Robots, Collaborative Robots (Cobots), SCARA Robots, Cartesian Robots, Delta Robots, Cylindrical Robots, Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), Humanoid Robots, Industrial Service Robots, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NVIDIA CORPORATION, SIEMENS AG, ABB LTD., DASSAULT SYSTÈMES, FANUC CORPORATION, KUKA AG, YASKAWA ELECTRIC CORPORATION, MICROSOFT CORPORATION, AUTODESK INC., ROBODK, MITSUBISHI ELECTRIC CORPORATION, DENSO CORPORATION, OMRON CORPORATION, KAWASAKI HEAVY INDUSTRIES, ROCKWELL AUTOMATION INC., VISUAL COMPONENTS, COPPELIA ROBOTICS, OPEN ROBOTICS (OSRF), MATHWORKS, WANDELBOTS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

![Global Robot Simulation Software Market Size, Share, Analysis By Software Type (Industrial Robots, Service Robotics, Collaborative Cobots, Autonomous Mobile Robots [AMRs]), By Component (Software Licences, Maintenance Services), By Deployment Mode (Cloud-Based SaaS, On-Premises Systems), By Enterprise Size (SMEs, Large Industrial Plants) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034](storage/Major-Key-Players.webp "Global Robot Simulation Software Market Size, Share, Analysis By Software Type (Industrial Robots, Service Robotics, Collaborative Cobots, Autonomous Mobile Robots [AMRs]), By Component (Software Licences, Maintenance Services), By Deployment Mode (Cloud-Based SaaS, On-Premises Systems), By Enterprise Size (SMEs, Large Industrial Plants) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

![Global Robot Simulation Software Market Size, Share, Analysis By Software Type (Industrial Robots, Service Robotics, Collaborative Cobots, Autonomous Mobile Robots [AMRs]), By Component (Software Licences, Maintenance Services), By Deployment Mode (Cloud-Based SaaS, On-Premises Systems), By Enterprise Size (SMEs, Large Industrial Plants) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034](storage/DROT.webp "Global Robot Simulation Software Market Size, Share, Analysis By Software Type (Industrial Robots, Service Robotics, Collaborative Cobots, Autonomous Mobile Robots [AMRs]), By Component (Software Licences, Maintenance Services), By Deployment Mode (Cloud-Based SaaS, On-Premises Systems), By Enterprise Size (SMEs, Large Industrial Plants) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

![Global Robot Simulation Software Market Size, Share, Analysis By Software Type (Industrial Robots, Service Robotics, Collaborative Cobots, Autonomous Mobile Robots [AMRs]), By Component (Software Licences, Maintenance Services), By Deployment Mode (Cloud-Based SaaS, On-Premises Systems), By Enterprise Size (SMEs, Large Industrial Plants) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034](storage/Recent-Development.webp "Global Robot Simulation Software Market Size, Share, Analysis By Software Type (Industrial Robots, Service Robotics, Collaborative Cobots, Autonomous Mobile Robots [AMRs]), By Component (Software Licences, Maintenance Services), By Deployment Mode (Cloud-Based SaaS, On-Premises Systems), By Enterprise Size (SMEs, Large Industrial Plants) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Robot Simulation Software Market?

The Global Robot Simulation Software Market was valued at USD 3.73 Billion in 2024 and USD 4.50 Billion in 2025, and is projected to reach USD 24.50 Billion by 2034, growing at a CAGR of 20.7% from 2026 to 2034. Market growth is driven by increasing industrial automation, adoption of digital twins, and rising demand for virtual robot programming and optimization solutions.

Who are the major players in the Robot Simulation Software Market?

NVIDIA CORPORATION, SIEMENS AG, ABB LTD., DASSAULT SYSTÈMES, FANUC CORPORATION, KUKA AG, YASKAWA ELECTRIC CORPORATION, MICROSOFT CORPORATION, AUTODESK INC., ROBODK, MITSUBISHI ELECTRIC CORPORATION, DENSO CORPORATION, OMRON CORPORATION, KAWASAKI HEAVY INDUSTRIES, ROCKWELL AUTOMATION INC., VISUAL COMPONENTS, COPPELIA ROBOTICS, OPEN ROBOTICS (OSRF), MATHWORKS, WANDELBOTS, Others

Which segments covered the Robot Simulation Software Market?

By Component, (Software, Services), By Deployment Model, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment), By Application, (Robot Design and Development, Offline Programming, Virtual Commissioning, Digital Twin and Process Simulation, Production Planning and Optimization, Material Handling Simulation, Welding Simulation, Assembly Line Simulation, Pick-and-Place Operations Simulation, Inspection and Quality Control Simulation, Training and Skill Development, Research and Development, Others), By End-User Vertical, (Automotive, Electronics and Semiconductor, Aerospace and Defense, Healthcare and Medical Devices, Food and Beverage, Logistics and Warehousing, Manufacturing, Metals and Machinery, Energy and Utilities, Retail and E-commerce, Education and Research, Pharmaceuticals and Biotechnology, Construction, Others), By Robot Type, (Articulated Robots, Collaborative Robots (Cobots), SCARA Robots, Cartesian Robots, Delta Robots, Cylindrical Robots, Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), Humanoid Robots, Industrial Service Robots, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Robot Simulation Software Market

Published Date : 15 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date