- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

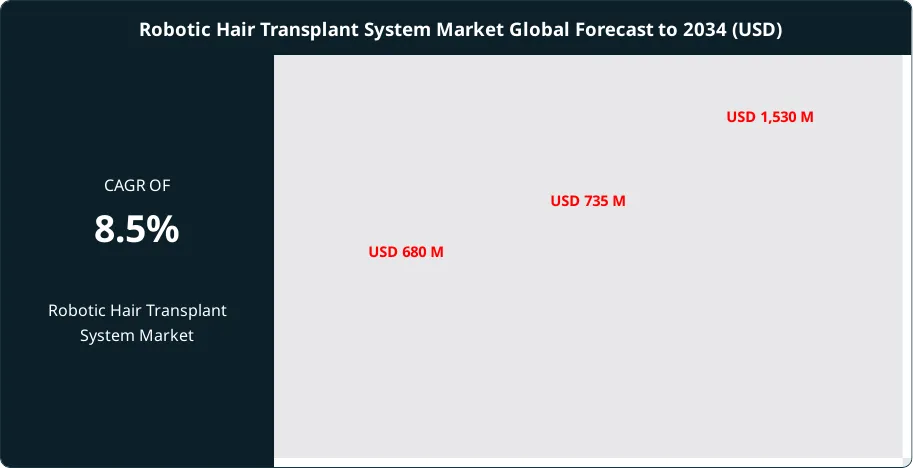

Global Robotic Hair Transplant System Market Size, Share | CAGR 8.5%

Global Robotic Hair Transplant System Market Size, Share, Analysis By Product Type (FUE-Based Robotic Systems, Hybrid Harvest and Implantation Systems, Manual-Assist Robotic Systems), By Application (Androgenetic Alopecia, Female Pattern Hair Loss, Scarring Alopecia Repair, Eyebrow and Beard Restoration), By End User (Specialty Dermatology Clinics, Hair Restoration Centers, Hospitals, Ambulatory Surgical Centers, Research Institutes), By Procedure Type (Graft Harvesting, Integrated Harvest & Implantation, Recipient Site Creation) Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 735 Million | USD 1,530 Million | 8.5% | North America, 33.3% |

The Robotic Hair Transplant System Market was valued at approximately USD 680 Million in 2024 and reached USD 735 Million in 2025. The market is projected to grow to USD 1,530 Million by 2034, expanding at a CAGR of 8.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 795 Million over the analysis period. The robotic hair transplant system market is defined as the industry producing image-guided, AI-enabled robotic platforms that automate follicular unit extraction, recipient site creation, and graft implantation during surgical hair restoration, excluding purely manual handheld devices and non-surgical therapeutics such as minoxidil or finasteride.

Get More Information about this report -

Request Free Sample ReportMarket scope covers capital equipment sales, procedure kits, warranty and service contracts, software upgrades, and consumables tied to FDA-cleared and CE-marked robotic platforms including ARTAS iX, ARTAS iXi, and successor hybrid systems. The scope extends upstream to precision optics, seven-axis robotic arms supplied by KUKA AG, and proprietary machine-vision subsystems, and downstream to dermatology clinics, ambulatory surgical centers, and hospital-based hair restoration units.

Primary demand drivers include rising prevalence of androgenetic alopecia affecting an estimated 35 million men and 21 million women in the United States per International Society of Hair Restoration Surgery data, increasing social acceptance of aesthetic procedures, and a demographic shift toward first-time patients aged 20 to 35, who represented 95% of initial surgical cases in 2024 according to the ISHRS 2025 Practice Census. Demand is further strengthened by a 16.5% rise in female surgical patients treated between 2021 and 2024, reported by the same census.

The regulatory environment centers on FDA 510(k) clearance pathways governing ARTAS iX and NeoGraft systems, CE marking under EU Medical Device Regulation (MDR) 2017/745, and national medical device registrations administered by the NMPA in China, PMDA in Japan, and CDSCO in India. Regulatory tightening on unlicensed clinics across Europe and the United Kingdom has pushed volume toward accredited providers that typically operate robotic systems, reinforcing equipment demand.

Technology dynamics are dominated by ARTAS iXi's seven-axis KUKA robotic arm delivering 0.1 mm repeatability, 44-micron stereoscopic vision, and AI tracking of follicle position, angle, and orientation 60 times per second. Recent engineering focus has shifted toward integrated implantation modules that reduce graft out-of-body time and improve survival rates above 90% in clinical practice.

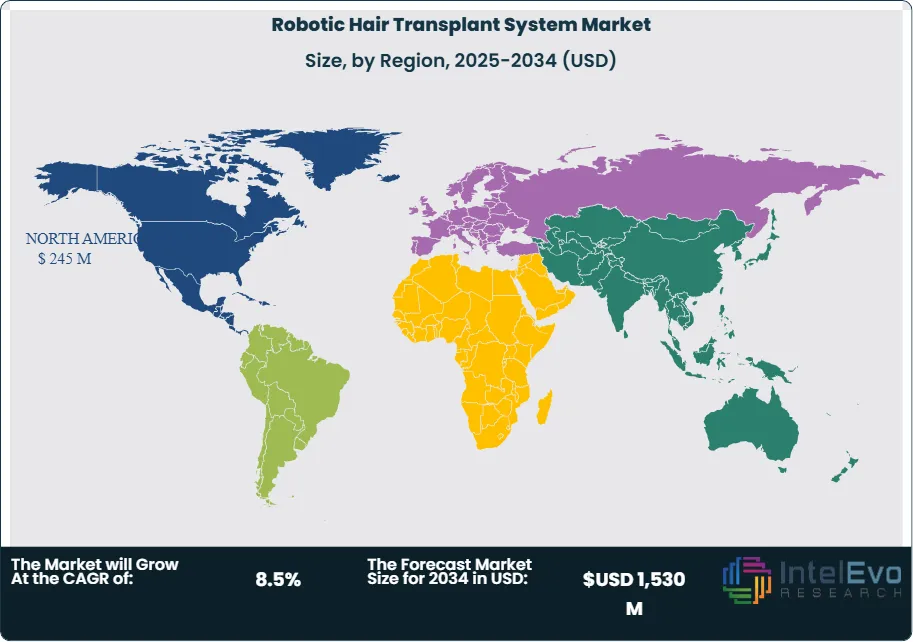

Regionally, North America held 33.3% revenue share in 2025 driven by high disposable income and early adoption; Asia Pacific is the fastest-growing region, propelled by medical tourism hubs in Turkey, India, and South Korea. Turkish hair transplant tourism alone generates approximately USD 1 billion annually, per a 2025 Mayo Clinic peer-reviewed analysis published in Aesthetic Plastic Surgery.

Supply chain consolidation accelerated in June 2025 when Venus Concept Inc. entered a definitive USD 20 Million agreement to divest its ARTAS and NeoGraft assets to MHG Co. Ltd., trading as Meta Healthcare Group. The transaction consolidates manufacturing at the San Jose, California facility under a new owner and reshapes the competitive landscape for the forecast period. The outlook through 2034 is anchored on expanded FDA indications, broader hair-type compatibility beyond black and brown straight hair, and deeper integration of regenerative adjuncts such as platelet-rich plasma and exosome therapy into robotic workflows.

, By Application (Androgenetic Alopecia, Female Pattern Hair Loss, Scarring Alopecia Repair, Eyebrow and Beard Restoration), By End User (Specialty Dermatology Clinics, Hair Restoration Centers, Hospitals, Ambulatory Surgical Centers, Research Institutes), By Procedure Type (Graft Harvesting, Integrated Harvest & Implantation, Recipient Site Creation) Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The robotic hair transplant system market is projected to expand from USD 735 Million in 2025 to USD 1,530 Million by 2034, growing at a CAGR of 8.5% over the nine-year forecast horizon.

- Segment Dominance: FUE-based robotic systems captured 78.2% of product-type revenue in 2025, driven by the ARTAS platform's dominance and ISHRS data showing 85.4% of male hair transplant procedures use FUE harvesting.

- Segment Dominance: Androgenetic alopecia treatment accounted for 74.8% of robotic procedure volume in 2025, reflecting the FDA indication for male pattern hair loss under which ARTAS iX remains cleared.

- Driver: Patients aged 20 to 35 represented 95% of first-time hair restoration surgery cases in 2024 according to the ISHRS 2025 Practice Census, materially enlarging the addressable patient base and extending revenue tails per procedure.

- Restraint: Capital system cost of USD 200,000 to USD 300,000 and per-procedure pricing of USD 10,000 to USD 20,000 limit penetration among independent dermatology practices, with only larger clinics able to absorb payback horizons exceeding 24 months.

- Opportunity: Female hair restoration patients increased 16.5% between 2021 and 2024 per the ISHRS census, creating an addressable niche estimated at USD 155 Million by 2030 as systems expand indication labels beyond male pattern baldness.

- Trend: Integrated harvest-plus-implantation robotic workflows accounted for 38.2% of 2025 procedure volume and are forecast to exceed 55% by 2030 as ARTAS iXi and successor competitors reduce graft out-of-body time below 30 minutes.

- Regional Analysis: North America led with 33.3% share and approximately USD 245 Million in revenue during 2025, anchored by United States clinic demand and early robotic adoption.

Key Insights Summary

- ARTAS iXi delivers 0.1 mm robotic arm repeatability through a seven-axis KUKA arm combined with a 44-micron resolution stereoscopic vision system that tracks follicle position, angle, and orientation 60 times per second, per Venus Concept product specifications.

- ISHRS 2025 Practice Census data shows the average ISHRS member performed 178 hair restoration procedures in 2024, with 15 surgeries per month and a 20% increase in average patients per physician compared to the 2021 cycle.

- Female hair restoration surgical patients rose 16.5% between 2021 and 2024 according to ISHRS, expanding an historically male-skewed customer base that previously accounted for 78.74% of procedure revenue.

- First-time hair restoration surgery patients aged 20 to 35 represented 95% of new cases in 2024 per the ISHRS census, a demographic shift that extends patient lifetime value and repeat-visit potential.

- Hair transplant medical tourism generates approximately USD 1 billion annually in Turkey, with Istanbul serving as the global epicenter per peer-reviewed analysis published in Aesthetic Plastic Surgery in September 2025.

- Venus Concept reported USD 12.5 Million in FY2024 revenue from ARTAS and NeoGraft systems, procedure kits, and warranty services, disclosed in its June 2025 definitive agreement filing with MHG Co. Ltd.

- FUE harvesting accounted for 85.4% of male hair transplant procedures and 68.2% of female procedures in 2024 according to ISHRS, establishing the methodology ceiling robotic systems address.

Competitive Landscape Overview

The robotic hair transplant system market is moderately consolidated, with the top four players commanding approximately 72% of global revenue in 2025. Meta Healthcare Group holds the leading position following its June 2025 acquisition of ARTAS and NeoGraft assets from Venus Concept, consolidating the only FDA-cleared integrated harvest-plus-implantation robotic platform under single ownership. Competition is primarily technology-based, differentiating on imaging resolution, robotic arm precision, implantation integration, and AI-enabled follicle tracking rather than on price alone.

Competitive evolution has accelerated through 2024-2025 as the ARTAS and NeoGraft divestiture restructured incumbent economics, while Asian challengers including HARRTS World and regional motorized FUE specialists have expanded geographic footprint. Price competition remains contained within the handheld and motorized-assist segments, where SmartGraft and HARRTS X2 compete against manual alternatives at 50-60% below full robotic platform pricing. The next competitive phase through 2028 will center on FDA indication expansion, particularly for female pattern hair loss and non-black-or-brown hair types, as first movers in indication broadening will capture 30% of currently excluded patient volume.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Meta Healthcare Group (MHG Co. Ltd.) | South Korea | Leader | ARTAS iX / iXi Robotic Hair Restoration System | Asia, North America, Europe | Announced USD 20 Million acquisition of ARTAS and NeoGraft portfolio from Venus Concept in June 2025 |

| Venus Concept Inc. | Toronto, Canada | Incumbent Divesting | NeoGraft Automated FUE; ARTAS iX (pre-transfer) | North America, EMEA | Entered definitive agreement to divest hair business; announced Nasdaq delisting intention in January 2026 |

| HARRTS World (SMC Robotics) | India | Challenger | HARRTS X2 Hair Robotic Transplant System | Asia Pacific, Middle East | Expanded HARRTS X2 rollout to Gulf Cooperation Council hair clinics during 2024-2025 |

| Vision Medical Systems | United States | Niche Player | SmartGraft Automated FUE Device | North America, Latin America | Continued distribution expansion through aesthetic surgeons in 2025 |

| Cole Instruments Inc. | Georgia, United States | Niche Player | Cole Isolation Technique (CIT) Device | North America, Europe | Ongoing refinement of hand-controlled follicular isolation tools |

| Medicamat (Moria Group) | France | Niche Player | Mamba Motorized FUE System | Europe, Middle East | Continued supply to European hair clinics in 2025 |

| Trivellini Tech | Argentina | Niche Player | Mamba System motorized device | Latin America, Europe | Expanded distribution network across Spanish-speaking markets in 2024 |

| Devroye Instruments | Belgium | Niche Player | WAW FUE System | Europe, select global clinics | Continued manual/hybrid precision tool refinement |

| Ellis Instruments | New Jersey, United States | Niche Player | Ellis motorized FUE punches | North America | Ongoing sales through surgeon-led distribution |

| FUE Systems Ltd. | United Kingdom | Niche Player | Trivellini Mamba handpieces | United Kingdom, Europe | Expanded UK clinic installations through 2025 |

By Product Type

The robotic hair transplant system market by product type is led by FUE-based robotic systems, which held 78.2% revenue share in 2025 and remain the category's anchor due to ARTAS iX and ARTAS iXi deployment in more than 37 countries. Demand centers on fully image-guided harvesting systems cleared by the FDA for follicular unit extraction in patients with androgenetic alopecia.

Hybrid systems combining harvest and implantation accounted for approximately 15.4% of 2025 revenue. These platforms, typified by the ARTAS iXi with its implantation module, reduce graft out-of-body time and enable single-session workflows that address surgeon fatigue. Uptake is strongest in United States and South Korean clinics equipped to absorb the USD 250,000-plus capital cost.

Manual-assist robotic systems, including motorized handpiece platforms such as HARRTS X2 and specialty punches from Cole Instruments, held 6.4% share in 2025. This category competes on price against full-scale robotic installations and serves mid-tier clinics in emerging markets, particularly India and Turkey, where per-procedure economics compress capital-heavy platforms. By comparison, FUE-based robotic systems outsold hybrid configurations by a ratio of approximately 5 to 1 during 2025.

By Application

By application, androgenetic alopecia treatment accounted for 74.8% of robotic procedure revenue in 2025, reflecting the FDA indication under which ARTAS iX is cleared for male pattern hair loss in patients with black or brown straight hair. Clinical demand concentrates on Norwood Stage III to V patients seeking donor preservation and minimal linear scarring.

Female pattern hair loss applications captured 13.2% share in 2025, a segment expanding faster than the overall market at an estimated 10.7% CAGR through 2034 per patient-mix data from ISHRS. Growth follows the 16.5% rise in female surgical patients reported between 2021 and 2024, and is driven by broader clinic willingness to perform non-scalp procedures such as eyebrow restoration, which rose to 12% of female cases.

Scarring alopecia and repair procedures held 7.5% share and address patients requiring correction after black-market hair transplants. The ISHRS 2025 Practice Census found that 6.9% of patients sought treatment specifically for repair of previous surgery, and 59% of ISHRS members reported black-market clinics operating in their cities, up from 51% in 2021. Eyebrow and beard restoration rounded out the segment at 4.5%, with moustache and beard transplants representing 5% of male recipient-area procedures per ISHRS 2024 data.

By End User

Specialty dermatology and hair restoration clinics held 55.3% of end-user revenue in 2025, mirroring the broader hair transplant market where dermatology clinics control 54.93% of service revenue. These accounts absorb the majority of new ARTAS iX and NeoGraft placements because procedure throughput supports capital equipment amortization.

Hospitals contributed 22.6% share in 2025, with academic medical centers in Germany, South Korea, and the United States leading adoption. Hospital purchases cluster around integrated plastic surgery and aesthetic medicine departments where robotic systems complement broader surgical capital investments.

Ambulatory surgical centers represented 14.8% of revenue in 2025, a category growing alongside outpatient aesthetic procedure expansion in the United States under CMS ambulatory surgery payment policies. Academic and research centers accounted for the remaining 7.3%, driven by clinical trials evaluating integration of platelet-rich plasma, exosomes, and stem cell adjuncts with robotic harvest. Specialty clinics outsold hospitals by a ratio of approximately 2.4 to 1 during 2025.

By Procedure Type

Integrated harvest plus implantation procedures held 38.2% of procedure-type revenue in 2025 and are projected to exceed 55% by 2030 as ARTAS iXi and successor platforms close the manual-implantation gap. These workflows reduce graft out-of-body time to under 30 minutes in clinical practice and support graft survival above 90%.

Graft harvesting-only procedures accounted for 48.6% of 2025 revenue, reflecting the installed base of ARTAS iX units placed prior to implantation-module upgrades. This segment remains the revenue backbone for clinics using robotic harvesting followed by manual implantation by technicians.

Harvest plus recipient site creation procedures held 13.2% share in 2025, typically chosen when operator preference favors manual graft placement while leveraging robotic consistency for site making. Compared to integrated workflows, harvesting-only procedures generated 27% higher single-session revenue per clinic in 2025 due to shorter session times.

Regional Analysis

North America

North America held 33.3% of the robotic hair transplant system market in 2025, generating approximately USD 245 Million in revenue. The United States contributed over 80% of regional revenue, supported by early adoption of ARTAS iX across specialty clinics in California, Florida, New York, and Texas. Canadian demand centers in Toronto and Vancouver, where accredited providers operate ARTAS iX platforms under Health Canada medical device licensing.

Regional expansion reflects high disposable income, strong cultural emphasis on aesthetic outcomes, and FDA-cleared deuruxolitinib approval in 2024, which broadened the alopecia therapeutics market and funneled inquiry volume into surgical clinics. Private equity investment in hair restoration chains accelerated in 2024 and 2025, consolidating regional operators and standardizing robotic system deployment.

In November 2024, Venus Concept expanded its international distributor network including Index International Ltd., a subsidiary of Paragon Meditech, strengthening ARTAS distribution infrastructure. The Mexican market grew from medical tourism crossover, with Mexico City and Guadalajara clinics positioning lower-cost robotic procedures for United States patients seeking cross-border treatment.

Europe

Europe held 24.6% share of the robotic hair transplant system market in 2025, with Germany, the United Kingdom, Spain, and Italy leading equipment deployment. European demand splits between established high-end providers in Germany and Spain and low-cost operators in Eastern Europe serving price-sensitive United Kingdom and Scandinavian patients.

CE marking under EU Medical Device Regulation 2017/745 governs all robotic systems on the continent, with national competent authorities such as BfArM in Germany and AEMPS in Spain administering clinical post-market surveillance. Regulatory scrutiny intensified in 2024-2025 as several member states tightened oversight of non-physician-operated hair clinics.

Italy is projected to grow at 17.4% CAGR through 2030 per broader hair restoration market analysis, driven by the country's established cosmetic surgery industry and luxury aesthetic tourism. French clinics anchor domestic demand while Medicamat, a Moria Group subsidiary, supplies motorized FUE devices primarily into European markets, providing the region a domestically manufactured alternative to imported robotic platforms.

Asia Pacific

Asia Pacific held 28.4% share of the robotic hair transplant system market in 2025 and is the fastest-growing region, expanding above 12% CAGR through 2034. Turkey, India, South Korea, and China anchor demand. Turkish hair transplant tourism alone generated approximately USD 1 billion in 2024 according to peer-reviewed Mayo Clinic analysis, with Istanbul clinics performing over 1.2 million procedures in recent years.

South Korea leads robotic platform density per capita, reflecting its dominance in aesthetic medicine and strong domestic research investment from Meta Healthcare Group. India's market expanded through DHI International's network of 16 clinics and competing chain operators; national regulation under CDSCO registers ARTAS iX as an imported Class C medical device.

China's market operates under NMPA approval pathways and shows rising domestic clinic adoption in Tier 1 cities. Japan's PMDA has cleared ARTAS for use since 2014, with Tokyo and Osaka dermatology groups driving installed base growth. Regional growth is reinforced by the April 2024 announcement that DHI International received European Medical Tourism & Wellness Awards recognition, elevating Asian clinic credibility for inbound tourism.

Latin America

Latin America held 4.9% share of the robotic hair transplant system market in 2025, led by Brazil and Mexico. Brazil's ANVISA regulates medical device imports, with São Paulo and Rio de Janeiro anchoring the country's substantial cosmetic surgery sector. Brazilian clinics increasingly adopt ARTAS and HARRTS platforms to compete with Colombian and Argentine operators in regional medical tourism.

Mexican demand is propelled by cross-border medical tourism from the United States, with Tijuana, Guadalajara, and Mexico City clinics offering robotic procedures at 40-50% below United States pricing. Argentine manufacturer Trivellini Tech supplies regional clinics with motorized Mamba FUE handpieces, providing a domestic supply alternative to imported robotic systems.

Regional growth is constrained by currency volatility affecting capital equipment imports and uneven regulatory enforcement that permits under-trained operators in several markets. In 2025, Colombian authorities expanded medical device surveillance under INVIMA, signaling broader regional tightening that favors accredited clinics running verified robotic platforms.

Middle East & Africa

Middle East & Africa held 8.8% share of the robotic hair transplant system market in 2025, dominated by Turkey and the United Arab Emirates. Dubai Healthcare City anchors UAE demand, with multiple clinics operating ARTAS iX platforms targeting Gulf Cooperation Council and South Asian patients. Saudi Arabia's Vision 2030 medical tourism investment expanded hair restoration clinic openings in Riyadh and Jeddah through 2024-2025.

Turkey's role is central, serving as the largest single-country hub for hair transplant procedures globally, with Istanbul handling the majority of cross-border volume. Turkish clinics predominantly run manual and motorized FUE protocols but high-end providers have deployed ARTAS iX to differentiate from commodity operators offering USD 1,700-3,800 package procedures.

South Africa anchors Sub-Saharan Africa demand with Johannesburg and Cape Town clinics. Regional growth is tempered by limited reimbursement and concentrated wealth, though North African markets including Egypt and Morocco are adopting robotic systems through 2025 to attract European medical tourists seeking lower prices than Turkey.

Country Analysis

United States

The United States robotic hair transplant system market reached approximately USD 210 Million in 2025 and is projected to grow at a CAGR of 8.2% through 2034. ARTAS iX commands the dominant installed base, cleared by the FDA since 2011 for follicular unit harvesting in men with androgenetic alopecia and black or brown straight hair. FDA 510(k) pathways govern system modifications, with recent clearances addressing the implantation module in ARTAS iXi.

Demand concentrates in California, Florida, and Texas, where private equity-backed hair restoration chains expanded footprint through 2024 and 2025. The Inflation Reduction Act did not directly affect elective aesthetic procedures, but broader healthcare consumer financing options from firms such as CareCredit and Alphaeon have improved patient access to USD 10,000-20,000 procedure pricing.

Deuruxolitinib FDA approval in 2024 amplified consumer awareness of alopecia treatments, funneling inquiry volume to surgical clinics. Venus Concept's announced divestiture of its ARTAS business to Meta Healthcare Group in June 2025 restructures domestic distribution, with the San Jose, California facility transferring to the new owner and influencing service continuity for installed United States accounts.

Turkey

Turkey's robotic hair transplant system market reached approximately USD 38 Million in 2025, with a country-level CAGR of 9.1% projected through 2034. Istanbul concentrates over 80% of national robotic system installations, operating under the Turkish Medicines and Medical Devices Agency, known as TITCK. The country performed approximately 1.2 million hair transplant procedures in recent years according to ISHRS-cited data.

Hair transplant tourism generates approximately USD 1 billion annually per a September 2025 peer-reviewed Mayo Clinic analysis published in Aesthetic Plastic Surgery. Turkish clinics typically price packages between USD 1,700 and USD 3,800, bundling hotel accommodation, transfers, and aftercare. Premium providers deploy ARTAS iX to differentiate against manual FUE commodity operators.

Turkish regulatory authorities tightened oversight in 2024-2025 following ISHRS campaigns against unlicensed clinics, with approximately 59% of ISHRS members globally reporting black-market activity in their cities. Accredited Turkish providers increasingly deploy robotic systems to signal clinical quality and capture high-value European and Gulf patients.

India

India's robotic hair transplant system market reached approximately USD 32 Million in 2025, with a country-level CAGR of 12.4% projected through 2034, the fastest among major markets. CDSCO regulates imports as Class C medical devices, while domestic innovation is led by HARRTS World, whose HARRTS X2 platform competes directly with imported ARTAS systems.

Delhi, Bangalore, Mumbai, and Chennai host the largest hair restoration clinic clusters, including DHI International's network of 16 domestic clinics recognized at the 2024 European Medical Tourism & Wellness Awards. Indian FUE packages range from USD 1,200 to USD 2,500, meaningfully lower than Turkey, creating a growing inbound tourism base for South Asian and African patients.

The Indian government's Ayushman Bharat framework does not cover elective hair restoration, keeping procedure financing dependent on private pay. Domestic equipment supply is strengthened by HARRTS World deployment across Gulf and African markets during 2024-2025, positioning India as both a tourism destination and an emerging robotic system exporter.

Germany

Germany's robotic hair transplant system market reached approximately USD 48 Million in 2025, with a country-level CAGR of 7.2% projected through 2034. BfArM administers medical device oversight under EU Medical Device Regulation 2017/745, with ARTAS iX operating under CE marking across all member states. Berlin, Munich, and Frankfurt clinics anchor national installed base.

German hospital-based aesthetic surgery departments drive a disproportionate share of ARTAS iX installations compared to standalone clinics elsewhere in Europe. The country serves as a price anchor for Western European medical tourism, with packages typically priced above USD 5,000, positioning Germany as the premium alternative to Turkish commodity providers.

Research partnerships with Fraunhofer institutes and German university hospitals have accelerated protocol standardization for robotic harvesting, contributing to the country's reputation for procedural consistency. In 2025, regulatory guidance from the German Federal Joint Committee, known as G-BA, maintained elective-procedure status for hair restoration, preserving private-pay economics for premium clinics operating ARTAS iX platforms.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- FUE-Based Robotic Systems

- Hybrid Systems (Harvest + Implantation)

- Manual-Assist Robotic Systems

By Application

- Androgenetic Alopecia (Male Pattern)

- Female Pattern Hair Loss

- Scarring Alopecia and Repair

- Eyebrow and Beard Restoration

By End User

- Specialty Dermatology and Hair Restoration Clinics

- Hospitals

- Ambulatory Surgical Centers

- Academic and Research Centers

By Procedure Type

- Graft Harvesting Only

- Integrated Harvest Plus Implantation

- Harvest Plus Recipient Site Creation

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 735 M |

| Forecast Revenue (2034) | USD 1,530 M |

| CAGR (2025-2034) | 8.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (FUE-Based Robotic Systems, Hybrid Systems (Harvest + Implantation), Manual-Assist Robotic Systems), By Application, (Androgenetic Alopecia (Male Pattern), Female Pattern Hair Loss, Scarring Alopecia and Repair, Eyebrow and Beard Restoration), By End User, (Specialty Dermatology and Hair Restoration Clinics, Hospitals, Ambulatory Surgical Centers, Academic and Research Centers), By Procedure Type, (Graft Harvesting Only, Integrated Harvest Plus Implantation, Harvest Plus Recipient Site Creation) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | META HEALTHCARE GROUP (MHG CO. LTD.), VENUS CONCEPT INC., HARRTS WORLD (SMC ROBOTICS), VISION MEDICAL SYSTEMS, COLE INSTRUMENTS INC., MEDICAMAT (MORIA GROUP), TRIVELLINI TECH, DEVROYE INSTRUMENTS, ELLIS INSTRUMENTS, FUE SYSTEMS LTD., BERNSTEIN MEDICAL, BOSLEY (AUSTRALIAN HEALTHCARE), DHI INTERNATIONAL MEDICAL GROUP, HAIR CLUB (ADERANS), HAIRLINE INTERNATIONAL, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Androgenetic Alopecia, Female Pattern Hair Loss, Scarring Alopecia Repair, Eyebrow and Beard Restoration), By End User (Specialty Dermatology Clinics, Hair Restoration Centers, Hospitals, Ambulatory Surgical Centers, Research Institutes), By Procedure Type (Graft Harvesting, Integrated Harvest & Implantation, Recipient Site Creation) Industry Trends & Forecast 2026-2034")

, By Application (Androgenetic Alopecia, Female Pattern Hair Loss, Scarring Alopecia Repair, Eyebrow and Beard Restoration), By End User (Specialty Dermatology Clinics, Hair Restoration Centers, Hospitals, Ambulatory Surgical Centers, Research Institutes), By Procedure Type (Graft Harvesting, Integrated Harvest & Implantation, Recipient Site Creation) Industry Trends & Forecast 2026-2034")

, By Application (Androgenetic Alopecia, Female Pattern Hair Loss, Scarring Alopecia Repair, Eyebrow and Beard Restoration), By End User (Specialty Dermatology Clinics, Hair Restoration Centers, Hospitals, Ambulatory Surgical Centers, Research Institutes), By Procedure Type (Graft Harvesting, Integrated Harvest & Implantation, Recipient Site Creation) Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Robotic Hair Transplant System Market?

The Global Robotic Hair Transplant System Market was valued at USD 680 Million in 2024 and is projected to reach USD 1,530 Million by 2034, growing at a CAGR of 8.5% from 2026 to 2034. Growth is driven by increasing prevalence of hair loss disorders, rising demand for minimally invasive hair restoration procedures, adoption of AI-powered robotic follicular unit extraction (FUE) systems, advancements in robotic imaging and graft harvesting technologies, and growing consumer interest in aesthetic and cosmetic treatments worldwide.

Who are the major players in the Robotic Hair Transplant System Market?

META HEALTHCARE GROUP (MHG CO. LTD.), VENUS CONCEPT INC., HARRTS WORLD (SMC ROBOTICS), VISION MEDICAL SYSTEMS, COLE INSTRUMENTS INC., MEDICAMAT (MORIA GROUP), TRIVELLINI TECH, DEVROYE INSTRUMENTS, ELLIS INSTRUMENTS, FUE SYSTEMS LTD., BERNSTEIN MEDICAL, BOSLEY (AUSTRALIAN HEALTHCARE), DHI INTERNATIONAL MEDICAL GROUP, HAIR CLUB (ADERANS), HAIRLINE INTERNATIONAL, OTHERS

Which segments covered the Robotic Hair Transplant System Market?

By Product Type, (FUE-Based Robotic Systems, Hybrid Systems (Harvest + Implantation), Manual-Assist Robotic Systems), By Application, (Androgenetic Alopecia (Male Pattern), Female Pattern Hair Loss, Scarring Alopecia and Repair, Eyebrow and Beard Restoration), By End User, (Specialty Dermatology and Hair Restoration Clinics, Hospitals, Ambulatory Surgical Centers, Academic and Research Centers), By Procedure Type, (Graft Harvesting Only, Integrated Harvest Plus Implantation, Harvest Plus Recipient Site Creation)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Robotic Hair Transplant System Market

Published Date : 01 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date