- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Robotic Surgery System Market Size, Share & Forecast | CAGR 11.9%

Global Robotic Surgery System Market Size, Share, Growth Analysis By System Type (Multi-Arm Surgical Robotic Platforms, Single-Arm Robotic Systems, Orthopedic Robotic Systems), By Application (Urology, Gynecology, Orthopedics, General Surgery, Thoracic & Cardiac), By End-User (Hospitals, Ambulatory Surgery Centers, Specialty Clinics), By Technology, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

| USD 6.84 Billion | USD 18.92 Billion | 11.9% | North America, 41.3% |

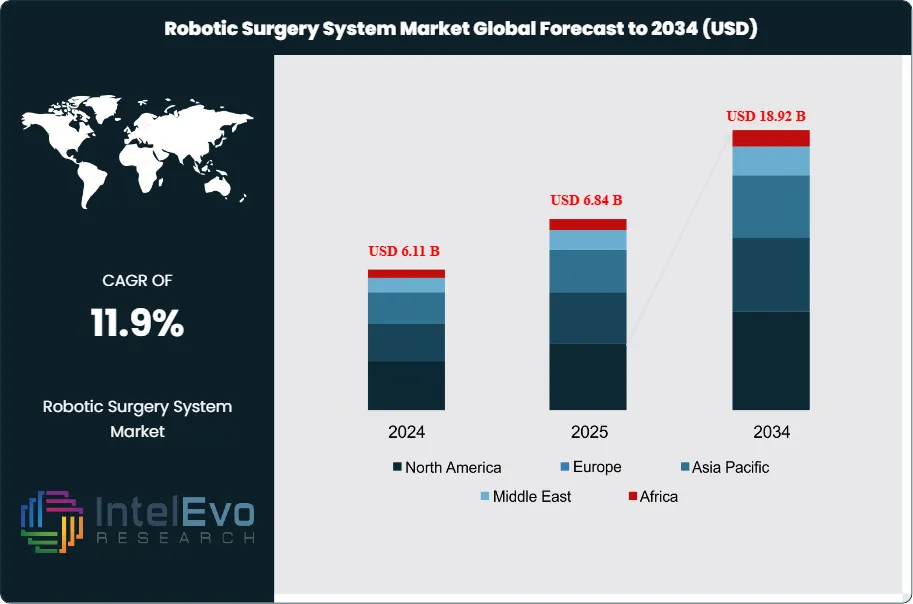

The Robotic Surgery System Market was valued at approximately USD 6.11 Billion in 2024 and reached USD 6.84 Billion in 2025. The market is projected to grow to USD 18.92 Billion by 2034, expanding at a CAGR of 11.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 12.08 Billion over the analysis period, reflecting sustained capital investment from hospital systems, accelerating surgical robot adoption across high-volume procedure categories, and expanding access in emerging healthcare markets.

Get More Information about this report -

Request Free Sample ReportRobotic surgery systems have moved well beyond early adoption in urology and gynecology. As of 2025, general surgery, colorectal, thoracic, and orthopedic indications collectively account for a growing share of robotic-assisted procedure volume. Hospitals are investing in multi-arm, multi-specialty platforms to maximize return on capital equipment investment and reduce dependence on any single vendor. Industry analysis indicates that annual robotic-assisted procedure volume exceeded 1.9 million globally in 2025, with a trajectory pointing toward 4.7 million procedures by 2034.

Regulatory tailwinds continue to support market expansion. The U.S. Food and Drug Administration has cleared a rising number of robotic surgery indications under 510(k) and de novo pathways, while the European Medicines Agency’s Medical Device Regulation (MDR) framework has established clearer standards for software-driven surgical tools. These regulatory signals reduce commercialization risk for device manufacturers and provide procurement confidence for hospital systems.

Technology integration is reshaping the competitive dynamics of the robotic surgery system market. Artificial intelligence-assisted surgical planning, real-time haptic feedback, augmented reality overlays, and machine learning-based tissue differentiation have moved from research settings to commercial deployment. These capabilities are shortening operative times, reducing complication rates, and generating procedure outcome data that supports reimbursement negotiations with payers.

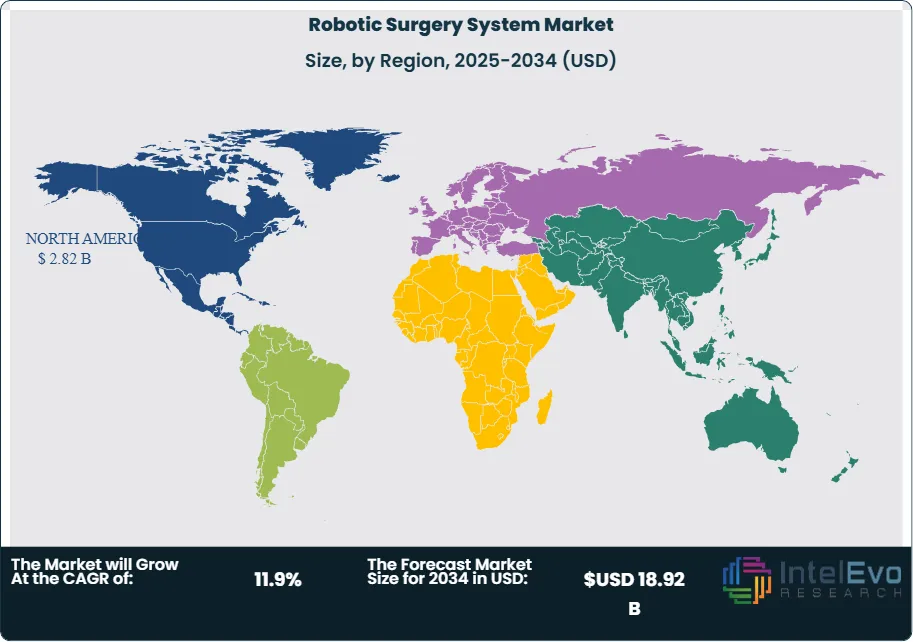

Asia Pacific represents the fastest-growing regional market, driven by China’s national healthcare infrastructure expansion, India’s medical tourism growth, and Japan’s aging population requiring higher volumes of minimally invasive procedures. Meanwhile, North America retains the largest market share at 41.3% in 2025, anchored by concentrated procedure volumes at academic medical centers and favorable reimbursement structures for robot-assisted surgery. Europe holds 27.1% of the global market, supported by Germany, France, and the United Kingdom’s health system procurement programs. Middle East and Africa is emerging as a credible growth corridor as sovereign wealth-funded hospital construction projects incorporate robotic surgical infrastructure from inception.

, By Application (Urology, Gynecology, Orthopedics, General Surgery, Thoracic & Cardiac), By End-User (Hospitals, Ambulatory Surgery Centers, Specialty Clinics), By Technology, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global robotic surgery system market was valued at USD 6.84 Billion in 2025 and is forecast to reach USD 18.92 Billion by 2034, expanding at a CAGR of 11.9% over the 2026–2034 period.

- Segment Dominance: By system type, surgical robotic platforms (multi-arm systems) hold the largest share at 58.4% of the market in 2025, driven by high procedure volumes and ongoing system placements at tertiary care hospitals.

- Segment Dominance: By application, urology and gynecology combined represent the largest application segment at 44.7% in 2025, reflecting the longest tenure of robotic adoption and established reimbursement coverage in these specialties.

- Driver: Rising demand for minimally invasive surgery, with robotic-assisted procedures demonstrating up to 30% shorter hospital stays compared to open surgery, is accelerating capital equipment acquisition by hospital networks.

- Restraint: High acquisition costs, with capital outlays for a fully equipped robotic surgery platform averaging USD 1.5 Million to USD 2.5 Million per unit in 2025, constrain adoption at community hospitals and in lower-income markets.

- Opportunity: The orthopedic robotic surgery segment, valued at approximately USD 780 Million in 2025, is projected to grow at a CAGR exceeding 14.5% through 2034 as knee and hip replacement volumes increase with aging global demographics.

- Trend: Subscription-based and procedure-based pricing models for robotic surgery systems are gaining traction, with 18% of new platform contracts in 2025 structured as usage-based agreements rather than outright capital purchases.

- Regional Analysis: North America leads the global robotic surgery system market with a 41.3% share in 2025, representing USD 2.82 Billion, supported by high surgical volumes at academic medical centers and strong reimbursement coverage.

Competitive Landscape Overview

The robotic surgery system market remains moderately consolidated at the platform level, with the top four players accounting for approximately 67% of global market share in 2025. Competition centers on procedure portfolio breadth, software capability, consumable attachment rates, and service contract economics rather than hardware cost alone. Intuitive Surgical maintains a dominant installed base advantage built over more than two decades, while a wave of well-funded challengers has introduced competitive multi-arm platforms since 2020. Merger and acquisition activity has intensified, with medical device conglomerates acquiring specialized robotic component and software companies to accelerate platform roadmaps and lock in hospital relationships.

Competitive Landscape Matrix

| Company | HQ (Country) | Market Position | Key Product | Geographic Strength | Recent Strategic Move (2024–2026) |

|---|---|---|---|---|---|

| Intuitive Surgical | USA | Leader | da Vinci 5 System | North America | Launched da Vinci 5 with force feedback and AI-assisted analytics in early 2024; expanded multi-year service agreements globally. |

| Medtronic | Ireland/USA | Challenger | Hugo RAS System | Europe, APAC | Received additional FDA clearances for Hugo in 2025; expanded commercial rollout to 14 new countries. |

| Johnson & Johnson (Ethicon) | USA | Challenger | Ottava Robotic Platform | North America, Europe | Completed Ottava clinical trial sites across 20 U.S. hospitals in 2025; regulatory submission filing progressed to FDA review stage. |

| Stryker | USA | Leader (Ortho) | MAKO SmartRobotics | North America, Europe | Acquired OrthoSoft navigation assets in 2025 to deepen MAKO software intelligence; expanded MAKO to 600+ global sites. |

| Zimmer Biomet | USA | Niche Player | ROSA Robotic System | North America, Europe | Signed a partnership with a major U.S. health system in 2025 to deploy ROSA across 25 facilities under a subscription model. |

| Smith+Nephew | UK | Niche Player | CORI Surgical System | Europe, North America | Launched CORI 2.0 with enhanced ML-based bone mapping in 2025; added shoulder arthroplasty to CORI’s indication portfolio. |

| CMR Surgical | UK | Niche Player | Versius Surgical System | Europe, Middle East | Secured USD 165 Million Series D funding in 2024; expanded Versius to 12 new countries by 2025. |

| Asensus Surgical | USA | Niche Player | LUNA System | North America, Europe | Received FDA clearance for LUNA general surgery indication in early 2025; entered into first commercial hospital contracts. |

By System Type

The robotic surgery system market by system type is led by multi-arm surgical robotic platforms, which captured 58.4% of global revenue in 2025, equivalent to approximately USD 3.99 Billion. These systems, exemplified by da Vinci 5 and Hugo, offer a full suite of surgical instrument wristed movement, high-definition 3D visualization, and integrated digital workflow tools. Their dominance reflects the broadest clinical indication coverage and the depth of peer-reviewed evidence supporting robotic-assisted outcomes in soft tissue procedures. Hospitals view multi-arm platforms as multi-specialty assets capable of generating utilization across urology, gynecology, general surgery, and thoracic departments. Single-arm robotic systems represent 22.1% of the market, valued at USD 1.51 Billion in 2025, and are growing as lower-cost entry points for community hospitals entering robotic surgery for the first time. Orthopedic robotic systems account for 19.5% of the market at USD 1.33 Billion in 2025, a segment growing above the overall market average due to the volume trajectory of total knee and hip replacement surgeries.

By Application

The robotic surgery system market by application is dominated by urological procedures, which accounted for 26.8% of market revenue in 2025, or USD 1.83 Billion. Robotic-assisted radical prostatectomy has achieved near-universal adoption at high-volume prostate cancer centers in North America and Europe, and growing adoption in Asia Pacific reflects the expansion of prostate cancer screening programs. Gynecological applications represent 17.9% of the market at USD 1.22 Billion in 2025, driven by hysterectomy, myomectomy, and endometriosis excision procedures. General surgery, including colorectal resection and hernia repair, accounts for 16.4% at USD 1.12 Billion and is the fastest-growing application category within soft tissue robotics, as evidence for robotic colorectal surgery outcomes continues to strengthen. Orthopedic applications represent 14.8% at USD 1.01 Billion, while thoracic, cardiac, and other emerging indications account for the remaining 24.1%.

By End-User

The robotic surgery system market by end-user is primarily served by hospitals and health systems, which represent 73.6% of global revenue in 2025 at USD 5.03 Billion. Academic medical centers and large tertiary hospitals account for the bulk of installed base, given their procedure volumes, residency training programs, and capital budget scale. Ambulatory surgery centers (ASCs) represent 14.3% of the market at USD 978 Million in 2025, a share growing rapidly as platform miniaturization and procedure clearances expand the range of robotic cases suitable for outpatient settings. Specialty surgical clinics and military healthcare facilities collectively account for 12.1% of the market.

By Technology

The robotic surgery system market by technology is bifurcated between laparoscopic robotic systems and open robotic systems, with hybrid and specialized platforms emerging as a distinct third tier. Laparoscopic robotic systems dominate with 64.2% of market share at USD 4.39 Billion in 2025, as minimally invasive soft tissue surgery represents the largest volume of robot-assisted procedures globally. Open robotic systems, primarily applicable in orthopedic reconstruction and neurosurgery, hold 28.9% of the market at USD 1.98 Billion. Emerging autonomous and semi-autonomous surgical robotic platforms represent 6.9% of the market as of 2025, with regulatory and clinical validation activity expected to drive this segment’s share above 12% by 2034.

Regional Analysis

North America

North America accounts for 41.3% of the global robotic surgery system market in 2025, representing USD 2.82 Billion. The United States is the dominant market, home to more than 4,200 installed da Vinci systems and the largest concentration of high-volume robotic surgery centers globally. Centers for Medicare and Medicaid Services (CMS) reimbursement coverage for robotic-assisted procedures in prostatectomy, hysterectomy, and colorectal resection provides a stable revenue foundation for hospital capital investment. Canada represents approximately 8% of the regional market, with provincial health systems progressively expanding robotic surgery capacity at urban academic centers. Mexico holds growing appeal as a medical tourism destination, with private hospitals investing in robotic platforms to attract cross-border patients. The competitive environment is intensive, with Intuitive Surgical’s installed base facing direct commercial pressure from Medtronic Hugo and J&J Ottava platforms targeting greenfield hospital accounts. The FDA’s Digital Health Center of Excellence is establishing frameworks for AI-integrated surgical platforms that are expected to clarify the regulatory pathway for next-generation robotic systems by 2026.

Europe

Europe represents 27.1% of the global robotic surgery system market in 2025, equivalent to USD 1.85 Billion. Germany is the largest European market, with its statutory health insurance system covering an expanding list of robotic-assisted indications and its university hospital network operating some of the highest-volume robotic surgical programs outside the United States. France’s Health Technology Assessment authority has approved reimbursement pathways for robotic colorectal surgery, stimulating investment from regional hospital groups. The United Kingdom’s National Health Service has committed to a multi-system procurement strategy that has increased installed base by approximately 22% between 2023 and 2025. Italy and Spain represent additional growth opportunities as public health systems balance budget constraints with the long-term cost efficiency of reduced postoperative complications. The EU MDR framework’s stringent post-market surveillance requirements have raised the clinical evidence bar for new robotic entrants, which is a barrier to short-cycle competition but benefits established platforms with long-term data records.

Asia Pacific

Asia Pacific accounts for 21.4% of the global robotic surgery system market in 2025 at USD 1.46 Billion and represents the fastest-growing regional market, projected to expand at a CAGR exceeding 15% through 2034. China is the fastest-growing national market, propelled by the 14th Five-Year Plan’s healthcare modernization targets, which prioritize robotic surgery deployment at Tier-3 hospitals across major provincial capitals. The National Medical Products Administration (NMPA) has streamlined Class III medical device approval timelines for robotic surgical systems, reducing average market entry lag from 36 months to approximately 18 months. Japan represents a mature but stable segment, with robotic surgery integrated into national health insurance coverage across 12 approved indications. India’s market is growing rapidly, driven by private hospital group expansion and medical tourism. South Korea’s health ministry has approved reimbursement for robotic colorectal and thyroid surgery, supporting volume growth at specialized cancer centers. Domestic robotic surgery manufacturers in China, including Tinavi Medical and others, are beginning to compete with international platforms at the price-sensitive tier of the market.

Latin America

Latin America represents 6.1% of the global robotic surgery system market in 2025 at USD 417 Million. Brazil is the dominant market, with a network of large private hospital operators and academic medical centers maintaining growing robotic surgery programs in oncology, urology, and general surgery. The Brazilian Health Surveillance Agency (ANVISA) registration processes have become more streamlined for internationally approved robotic platforms, reducing market entry timelines. Mexico’s market growth is linked to increasing investment by major private hospital chains catering to insured and medical tourism populations. Colombia and Chile are emerging markets where private-sector hospital investment is driving initial robotic platform acquisitions. A primary constraint across the region is currency risk and import duties on capital medical equipment, which inflate total acquisition costs. The International Finance Corporation and Inter-American Development Bank have both initiated health infrastructure financing programs that include provisions for advanced surgical technology, providing an indirect demand catalyst.

Middle East & Africa

Middle East & Africa accounts for 4.1% of the global robotic surgery system market in 2025, representing USD 280 Million, and is evolving as a credible long-term growth market. The United Arab Emirates leads regional adoption, with Cleveland Clinic Abu Dhabi, Mediclinic, and government health authority hospitals operating multiple robotic surgery systems across urology, gynecology, and bariatric specialties. Saudi Arabia’s Vision 2030 healthcare transformation program has allocated capital investment for advanced surgical technology deployment at both public and private hospitals. South Africa represents the most developed sub-Saharan market, centered on Johannesburg and Cape Town private hospital networks. Infrastructure limitations and surgeon training gaps restrict broader African adoption, but targeted programs by device manufacturers and the African Society of Urological Surgeons are addressing workforce development. The Gulf Cooperation Council’s harmonized medical device regulatory framework is simplifying multi-country commercial launches, reducing per-country approval burden for international robotic system manufacturers.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By System Type

- Multi-Arm Surgical Robotic Platforms

- Single-Arm Robotic Systems

- Orthopedic Robotic Systems

By Application

- Urology

- Gynecology

- General Surgery

- Orthopedics

- Thoracic & Cardiac

- Other Applications

By End-User

- Hospitals & Health Systems

- Ambulatory Surgery Centers

- Specialty Surgical Clinics

- Military & Government Healthcare Facilities

By Technology

- Laparoscopic Robotic Systems

- Open Robotic Systems

- Autonomous & Semi-Autonomous Platforms

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.84 B |

| Forecast Revenue (2034) | USD 18.92 B |

| CAGR (2025-2034) | 11.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By System Type, (Multi-Arm Surgical Robotic Platforms, Single-Arm Robotic Systems, Orthopedic Robotic Systems), By Application, (Urology, Gynecology, General Surgery, Orthopedics, Thoracic & Cardiac, Other Applications), By End-User, (Hospitals & Health Systems, Ambulatory Surgery Centers, Specialty Surgical Clinics, Military & Government Healthcare Facilities), By Technology, (Laparoscopic Robotic Systems, Open Robotic Systems, Autonomous & Semi-Autonomous Platforms) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | INTUITIVE SURGICAL, MEDTRONIC, STRYKER, JOHNSON & JOHNSON (ETHICON/OTTAVA), ZIMMER BIOMET, SMITH+NEPHEW, CMR SURGICAL, ASENSUS SURGICAL, GLOBUS MEDICAL, BRAINLAB, ACCURAY, TINAVI MEDICAL TECHNOLOGIES, MICROBOT MEDICAL, AVATERA MEDICAL, VERB SURGICAL (ALPHABET), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Urology, Gynecology, Orthopedics, General Surgery, Thoracic & Cardiac), By End-User (Hospitals, Ambulatory Surgery Centers, Specialty Clinics), By Technology, Industry Trends & Forecast 2026-2034")

, By Application (Urology, Gynecology, Orthopedics, General Surgery, Thoracic & Cardiac), By End-User (Hospitals, Ambulatory Surgery Centers, Specialty Clinics), By Technology, Industry Trends & Forecast 2026-2034")

, By Application (Urology, Gynecology, Orthopedics, General Surgery, Thoracic & Cardiac), By End-User (Hospitals, Ambulatory Surgery Centers, Specialty Clinics), By Technology, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Robotic Surgery System Market?

The Global Robotic Surgery System Market was valued at USD 6.11 Billion in 2024 and is projected to reach USD 18.92 Billion by 2034, growing at a CAGR of 11.9% from 2026 to 2034, driven by rising adoption of minimally invasive surgical procedures, increasing demand for robotic-assisted precision surgeries, advancements in AI-integrated surgical robotics, and expanding applications across orthopedic, cardiovascular, gynecological, and urological surgeries worldwide.

Who are the major players in the Robotic Surgery System Market?

INTUITIVE SURGICAL, MEDTRONIC, STRYKER, JOHNSON & JOHNSON (ETHICON/OTTAVA), ZIMMER BIOMET, SMITH+NEPHEW, CMR SURGICAL, ASENSUS SURGICAL, GLOBUS MEDICAL, BRAINLAB, ACCURAY, TINAVI MEDICAL TECHNOLOGIES, MICROBOT MEDICAL, AVATERA MEDICAL, VERB SURGICAL (ALPHABET), Others

Which segments covered the Robotic Surgery System Market?

By System Type, (Multi-Arm Surgical Robotic Platforms, Single-Arm Robotic Systems, Orthopedic Robotic Systems), By Application, (Urology, Gynecology, General Surgery, Orthopedics, Thoracic & Cardiac, Other Applications), By End-User, (Hospitals & Health Systems, Ambulatory Surgery Centers, Specialty Surgical Clinics, Military & Government Healthcare Facilities), By Technology, (Laparoscopic Robotic Systems, Open Robotic Systems, Autonomous & Semi-Autonomous Platforms)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Robotic Surgery System Market

Published Date : 21 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date