- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Rotary Steerable System Market Size, Share & Forecast 2034 | CAGR 7.0%

Global Rotary Steerable System Market Size, Share, Analysis By Type (Push-the-Bit Systems, Point-the-Bit Systems), By Hole Size (Below 6¾ Inch, 6¾–8¼ Inch, 8½–9⅞ Inch, Above 9⅞ Inch), By Application (Onshore, Offshore), By End Use (Conventional Development Wells, Extended-Reach and Horizontal Wells, HPHT and Deepwater Wells) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Drilling Technology Trends & Forecast 2026–2034

Report Overview

| Market Size, 2025 | Forecast Value, 2034 | CAGR, 2025-2034 | Leading Region, 2025 |

| USD 5.1 Billion | USD 9.4 Billion | 7.0% | North America, 31.5% |

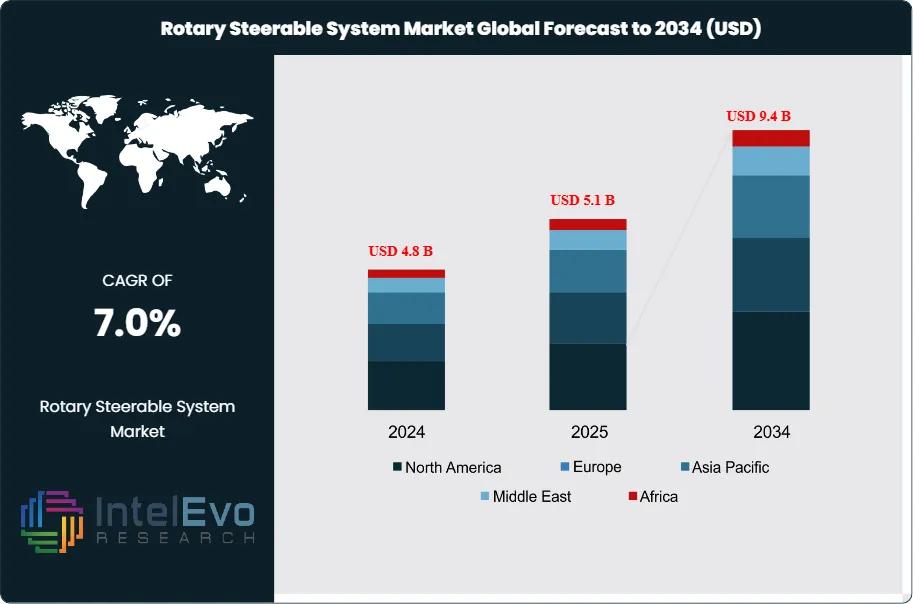

The Rotary Steerable System Market was valued at USD 4.8 billion in 2024 and is projected to reach approximately USD 5.1 billion in 2025. The market is further expected to expand to nearly USD 9.4 billion by 2034, registering a compound annual growth rate (CAGR) of about 7.0% during the forecast period from 2026 to 2034. Growth in the market is driven by increasing demand for advanced directional drilling technologies in complex oil and gas reservoirs, including deepwater and unconventional shale formations. Rotary steerable systems help operators achieve higher drilling accuracy, improved wellbore quality, and reduced non-productive time, making them essential tools for modern drilling operations.

Get More Information about this report -

Request Free Sample ReportAdditionally, rising investments in exploration and production activities, offshore drilling projects, and high-efficiency drilling solutions are expected to further accelerate the adoption of rotary steerable systems across global energy markets.

The rotary steerable system market sits at the premium end of directional drilling. Demand comes from operators that need faster penetration, smoother wellbores, lower tortuosity, and tighter well placement in complex wells. Adoption remains strongest in U.S. shale, Middle East development drilling, Brazil deepwater, the North Sea, and selected Asia Pacific offshore projects. The market is shaped by longer laterals, extended-reach wells, tighter in-zone drilling, and the shift toward automation-linked drilling workflows.

Supply remains concentrated among a small number of large oilfield service companies because RSS failures are expensive and operators prefer proven fleets in technically demanding wells. The market also faces a restraint from upstream capital discipline. Softness in some land drilling programs slows fleet additions and stretches procurement cycles. Even so, deepwater and national oil company development programs continue to support premium drilling tools, especially where continuous rotation lowers well time and improves borehole quality.

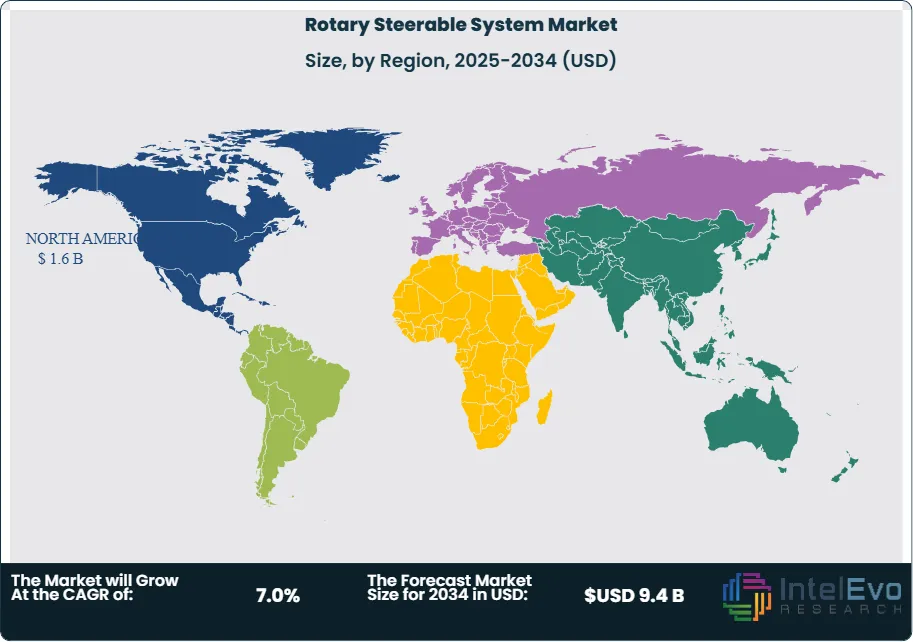

Technology remains the main competitive factor. Vendors now combine RSS tools with drilling automation, real-time downhole data, remote operations, and integrated formation evaluation. This lifts system value per well and moves competition beyond tool hardware alone. North America held the largest share of the rotary steerable system market in 2025 at 31.5%, equal to USD 1.6 Billion. The strongest medium-term investment momentum is moving toward the Middle East, Latin America deepwater, and selected Asia Pacific offshore corridors.

, By Hole Size (Below 6¾ Inch, 6¾–8¼ Inch, 8½–9⅞ Inch, Above 9⅞ Inch), By Application (Onshore, Offshore), By End Use (Conventional Development Wells, Extended-Reach and Horizontal Wells, HPHT and Deepwater Wells) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Drilling Technology Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The rotary steerable system market stood at USD 5.1 Billion in 2025 and is projected to reach USD 9.4 Billion by 2034, at a CAGR of 7.0% across 2025-2034.

- Segment Dominance: Push-the-bit systems led by type with a 57.0% share in 2025, equal to USD 2.9 Billion, supported by strong adoption in harsh formations and long-curve applications.

- Segment Dominance: Onshore applications led by application with a 61.0% share in 2025, or USD 3.1 Billion, driven by U.S. shale, Middle East land drilling, and Argentina development work.

- Driver: The main growth driver is the rise in complex well architecture, including long laterals, extended-reach wells, and exact reservoir targeting that reward continuous rotation and precise steering.

- Restraint: The main restraint is capital discipline in upstream drilling. Lower spending in some land markets slows premium tool deployment and extends replacement cycles.

- Opportunity: The largest opportunity sits in deepwater and national oil company drilling, especially in the Middle East and Brazil where premium well construction standards support higher RSS intensity.

- Trend: The strongest market trend is RSS integration with drilling automation, remote operations, and real-time subsurface decision support across multiwell and offshore programs.

- Regional Analysis: North America led the rotary steerable system market with 31.5% share in 2025, equivalent to USD 1.6 Billion, supported by horizontal shale drilling and dense service infrastructure.

Competitive Landscape

The rotary steerable system market is moderately consolidated. The top four players held a combined 58.0% share in 2025. Competition is technology-driven and shaped by tool reliability, steering precision, automation integration, and regional service depth. Competitive intensity rose through 2025 and early 2026 as offshore and national oil company contracts increasingly bundled RSS with broader drilling and digital well construction services.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | US | Leader | PowerDrive Orbit / Archer | Middle East, offshore global | Expanded PowerDrive Archer-linked activity through ADNOC Drilling work in Kuwait and Oman during 2025. |

| Baker Hughes | US | Leader | AutoTrak / Lucida | North America, Latin America, Middle East | Reported strong Lucida and AutoTrak uptake with Pluspetrol in Argentina in January 2026. |

| Halliburton | US | Leader | iCruise intelligent RSS | North America, Brazil, Middle East | Won a three-year Petrobras offshore drilling contract in January 2025 using iCruise, LOGIX, and EarthStar. |

| Weatherford | US | Leader | Magnus Saker / Revolution | Middle East, North America | Highlighted Magnus Saker with 39 upgrades in September 2025. |

| NOV | US | Challenger | VectorZIEL RSS | Asia Pacific, Middle East | Continued positioning VectorZIEL for automated 3D drilling in international markets. |

| Scientific Drilling | US | Challenger | HALO RSS | US land | Maintained HALO deployment in complex North American lateral drilling. |

| Gyrodata | US | Niche Player | High-accuracy directional services | Middle East, North America | Expanded premium directional positioning work across complex drilling contracts. |

| APS Technology | US | Niche Player | SureSteer / steering electronics | North America | Continued supplying steering electronics and directional components into premium BHA systems. |

| COSL | China | Challenger | Rotary steerable drilling services | China, Asia Pacific offshore | Sustained offshore directional drilling build-out in Chinese offshore programs. |

By Type

Push-the-bit systems held 57.0% of market revenue in 2025, or USD 2.9 Billion. They lead because they deliver strong steering authority in harsh formations, long curves, and high dogleg sections. Point-the-bit systems accounted for 43.0%, or USD 2.2 Billion, and remain important where borehole smoothness, reduced drag, and precise trajectory control matter most. The gap between the two categories is narrowing as hybrid steering and better sensor packages improve both control and borehole quality.

By Hole Size,

The 6¾-8¼ inch range led with 34.0% share in 2025, equal to USD 1.7 Billion. This range covers a broad set of curve and lateral sections in onshore shale and standard development wells. The 8½-9⅞ inch range followed at 29.0%, or USD 1.5 Billion. Holes above 9⅞ inch accounted for 19.0%, or USD 1.0 Billion, while holes below 6¾ inch contributed 18.0%, or USD 0.9 Billion. Medium-hole sections dominate because they sit closest to the drilling intervals where removing sliding time creates the strongest cost benefit.

By Application

Onshore drilling held 61.0% of global revenue in 2025, or USD 3.1 Billion. High well counts in U.S. shale, Saudi land drilling, and Vaca Muerta development kept onshore demand ahead of offshore volumes. Offshore drilling represented 39.0%, or USD 2.0 Billion, but it carried higher revenue intensity per well due to deepwater complexity, stricter reliability requirements, and higher cost exposure from directional errors.

By End Use

Conventional development wells held 46.0% share in 2025, or USD 2.3 Billion. Extended-reach and horizontal wells followed at 34.0%, or USD 1.7 Billion, reflecting the strong technical fit between RSS tools and long lateral drilling. HPHT and deepwater wells accounted for 20.0%, or USD 1.0 Billion, but they generate outsized tool revenue because of premium pricing and low tolerance for tool failure. Over time, the share of extended-reach and deepwater wells is expected to rise as well design becomes more exact and offshore activity expands.

Regional Analysis

North America held 31.5% of the rotary steerable system market in 2025, equal to USD 1.6 Billion. The United States accounted for about USD 1.3 Billion, Canada for USD 0.2 Billion, Mexico for USD 0.1 Billion, and the rest of North America for USD 0.05 Billion. The region leads because horizontal shale drilling still demands premium directional performance, fast turnaround, and strong field support.

Europe represented 13.5% of the market in 2025, or USD 0.7 Billion. The UK and Norway remain the main offshore demand centers, while Germany and France contribute through selected gas and engineering-linked drilling activity. Europe stays smaller in volume terms, but technically demanding offshore wells support premium RSS pricing and strong quality requirements.

Asia Pacific accounted for 21.0% of the market in 2025, equal to USD 1.1 Billion. China led regional demand, followed by Australia, India, and Japan. The region benefits from supply-security drilling, offshore gas programs, and technically tougher land wells. Asia Pacific is expected to grow above the global average through 2034 as offshore and redevelopment activity rises.

Latin America held 10.0% of the market in 2025, or USD 0.5 Billion. Brazil led through deepwater pre-salt activity, Mexico contributed a mix of offshore and selective land drilling, and Argentina remained the key unconventional growth market. The region combines premium offshore projects with rising long-lateral land development.

Middle East and Africa represented 24.0% of the market in 2025, equal to USD 1.2 Billion. Saudi Arabia and the UAE anchored regional demand, while the broader market benefited from national oil company spending, large development programs, and strong demand for exact well placement. This region is expected to be the main global growth engine for premium RSS deployments over the next decade.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Push-the-Bit Systems

- Point-the-Bit Systems

By Hole Size

- Below 6¾ Inch

- 6¾-8¼ Inch

- 8½-9⅞ Inch

- Above 9⅞ Inch

By Application

- Onshore

- Offshore

By End Use

- Conventional Development Wells

- Extended-Reach and Horizontal Wells

- HPHT and Deepwater Wells

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.1 B |

| Forecast Revenue (2034) | USD 9.4 B |

| CAGR (2025-2034) | 7.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Push-the-Bit Systems, Point-the-Bit Systems), By Hole Size (Below 6¾ Inch, 6¾-8¼ Inch, 8½-9⅞ Inch, Above 9⅞ Inch), By Application (Onshore, Offshore), By End Use (Conventional Development Wells, Extended-Reach and Horizontal Wells, HPHT and Deepwater Wells) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, BAKER HUGHES, HALLIBURTON, WEATHERFORD, NOV, SCIENTIFIC DRILLING, GYRODATA, APS TECHNOLOGY, COSL, JEREH, NABORS INDUSTRIES, OLIDEN TECHNOLOGY, GORDON TECHNOLOGIES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Hole Size (Below 6¾ Inch, 6¾–8¼ Inch, 8½–9⅞ Inch, Above 9⅞ Inch), By Application (Onshore, Offshore), By End Use (Conventional Development Wells, Extended-Reach and Horizontal Wells, HPHT and Deepwater Wells) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Drilling Technology Trends & Forecast 2026–2034")

, By Hole Size (Below 6¾ Inch, 6¾–8¼ Inch, 8½–9⅞ Inch, Above 9⅞ Inch), By Application (Onshore, Offshore), By End Use (Conventional Development Wells, Extended-Reach and Horizontal Wells, HPHT and Deepwater Wells) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Drilling Technology Trends & Forecast 2026–2034")

, By Hole Size (Below 6¾ Inch, 6¾–8¼ Inch, 8½–9⅞ Inch, Above 9⅞ Inch), By Application (Onshore, Offshore), By End Use (Conventional Development Wells, Extended-Reach and Horizontal Wells, HPHT and Deepwater Wells) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Drilling Technology Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Rotary Steerable System Market?

Global Rotary Steerable System Market was valued at USD 4.8 billion in 2024 and is projected to reach USD 9.4 billion by 2034, growing at a CAGR of 7.0%. Explore market trends, drilling technology demand, and growth opportunities.

Who are the major players in the Rotary Steerable System Market?

SLB, BAKER HUGHES, HALLIBURTON, WEATHERFORD, NOV, SCIENTIFIC DRILLING, GYRODATA, APS TECHNOLOGY, COSL, JEREH, NABORS INDUSTRIES, OLIDEN TECHNOLOGY, GORDON TECHNOLOGIES, Others

Which segments covered the Rotary Steerable System Market?

By Type (Push-the-Bit Systems, Point-the-Bit Systems), By Hole Size (Below 6¾ Inch, 6¾-8¼ Inch, 8½-9⅞ Inch, Above 9⅞ Inch), By Application (Onshore, Offshore), By End Use (Conventional Development Wells, Extended-Reach and Horizontal Wells, HPHT and Deepwater Wells)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Rotary Steerable System Market

Published Date : 11 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date