- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Rotational Molding Materials Market Size, Trends Forecast | CAGR 5.7%

Global Rotational Molding Materials Market Size, Share & Industry Analysis By Material Type (Polyethylene – LLDPE, HDPE, XLPE, MDPE, LDPE; Polypropylene; PVC; Nylon; Polycarbonate; Polyesters), By Type (Virgin, Recycled), By Form (Powder, Granules), By Application (Storage Tanks, Automotive Components, Containers, Toys & Leisure, Materials Handling, Industrial), By End-Use (Construction, Automotive, Agriculture, Consumer Goods, Chemical, Food & Beverage) – Trends & Forecast 2025–2034

Report Overview

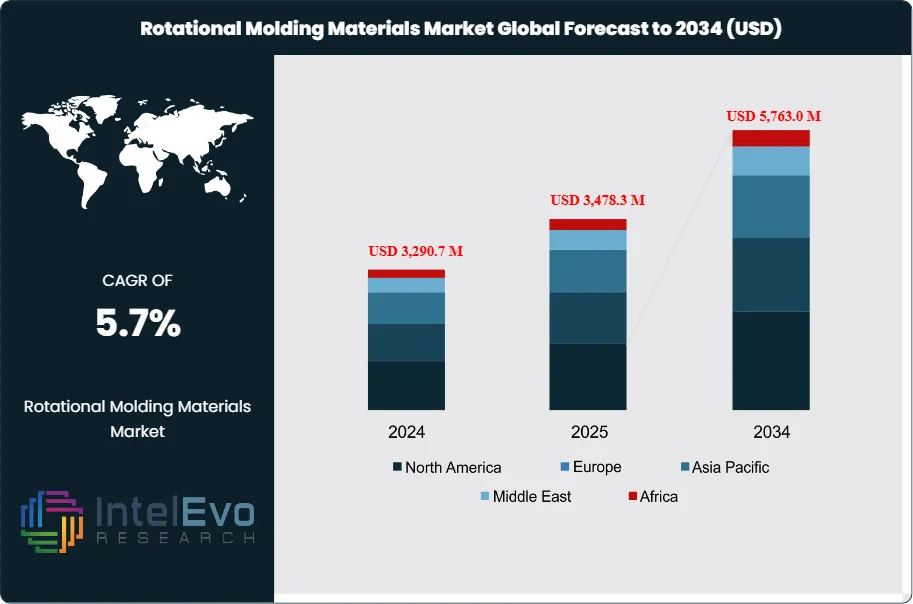

The Rotational Molding Materials Market was valued at approximately USD 3,290.7 million in 2024 and is projected to reach nearly USD 5,763.0 million by 2034, reflecting steady industry expansion over the forecast horizon. Based on the projected growth trajectory, the market size for 2025 is estimated at around USD 3,478.3 million. Beginning in 2026, the market is expected to grow at a compound annual growth rate (CAGR) of about 5.7% from 2026 to 2034, ultimately reaching an estimated valuation of approximately USD 5,763.0 million by 2034. This expansion reflects sustained demand for seamless, hollow plastic components across multiple industrial applications, driven by the inherent advantages of rotomolding processes in delivering uniform wall thickness, design flexibility, and cost efficiency at scale.

Get More Information about this report -

Request Free Sample ReportMarket dynamics are shaped by accelerating adoption in automotive manufacturing, industrial storage, agricultural equipment, and consumer goods sectors. Rotomolded tanks, containers, and playground structures benefit from superior durability and lower production costs compared to alternative manufacturing techniques. Supply-side factors include polyethylene resin availability, raw material price volatility, and capacity expansions by key material suppliers in established and emerging markets. Demand-side forces center on infrastructure modernization, urbanization trends, and the ongoing shift toward lightweight materials that reduce transportation costs and enhance fuel efficiency in automotive applications.

Regulatory frameworks governing plastic waste management and circular economy initiatives are reshaping production strategies. Manufacturers face mounting pressure to integrate recycled content and develop bio-based rotomolding resins, particularly in jurisdictions with stringent environmental mandates. Compliance requirements related to chemical safety and product lifecycle assessments introduce operational complexity but also create differentiation opportunities for companies that advance sustainable material formulations.

Technology adoption is accelerating through automation, digital process monitoring, and predictive maintenance systems that enhance production throughput and quality control. Advanced simulation software reduces prototype cycles, while machine learning algorithms optimize heating and cooling parameters to minimize defects. These innovations lower per-unit costs and improve competitiveness for rotomolders serving high-volume segments.

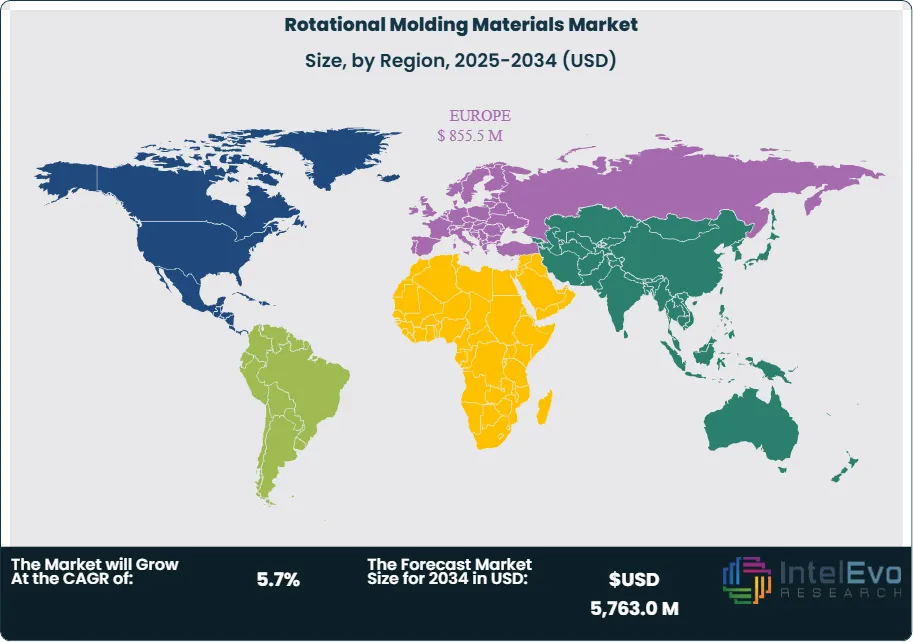

Europe commanded a 29.6% market share in 2024, generating USD 855.5 million in revenue, supported by mature automotive and industrial sectors and robust regulatory frameworks promoting recycled plastics. North America maintains strong demand driven by agriculture, water management, and recreational equipment industries. Asia-Pacific represents the fastest-growing region, propelled by industrial expansion in China, India, and Southeast Asia, where infrastructure investment and rising disposable incomes fuel demand for rotomolded products. Emerging markets in Latin America and the Middle East present untapped opportunities as local manufacturing capabilities expand and import dependencies decline.

, By Type (Virgin, Recycled), By Form (Powder, Granules), By Application (Storage Tanks, Automotive Components, Containers, Toys & Leisure, Materials Handling, Industrial), By End-Use (Construction, Automotive, Agriculture, Consumer Goods, Chemical, Food & Beverage) – Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global rotational molding materials market expands from 3,290.7 million USD in 2024 to 5,763.0 million USD by 2034, registering a compound annual growth rate of 5.7% over 2024-2034.

- Segment Dominance : Polyethylene dominates the material type category with an 80.0% market share in 2024. Virgin materials command 82.0% of the type segment during the same period.

- Segment Dominance: Powder form holds 80.4% of revenue share in 2024, while storage tanks lead applications with 38.6% and construction accounts for 24.3% of end-use revenue.

- Driver: Rising demand for lightweight, durable components across automotive, agriculture, and industrial sectors accelerates market expansion, representing estimated: 38.0% of total applications, 2024.

- Restraint: Raw material price volatility and polyethylene resin cost fluctuations constrain profit margins, with estimated: 14.0% annual price variance, 2024.

- Opportunity: Regulatory mandates for recycled content and circular economy compliance create differentiation avenues, with estimated: 18.0% growth potential in bio-based formulations, 2024-2034.

- Trend: Automation and digital process monitoring systems enhance production efficiency and quality control, reducing manufacturing defects by estimated: 22.0%, 2024.

- Regional Analysis: Europe commands 29.6% of the global market in 2024, generating 974.1 million USD in revenue, driven by mature industrial sectors and stringent environmental frameworks.

By Material Type

Polyethylene continues to anchor the rotational molding materials market in 2025. It accounted for close to 80 percent of global revenue in 2024 and is expected to retain a dominant position over the next five to seven years. Its combination of low density, chemical resistance, and favorable processing characteristics gives manufacturers a cost-effective solution for large hollow parts such as tanks, containers, and material handling products. Linear low-density polyethylene (LLDPE) and cross-linked polyethylene grades, in particular, see strong demand in storage, agriculture, and infrastructure applications where long service life and impact strength are essential.

Other materials, including polycarbonate, nylon, PVC, polyesters, and polypropylene, together form a smaller but strategically important share. These polymers serve applications that require higher temperature resistance, improved dimensional stability, or specific regulatory compliance, such as food contact or medical uses. For example, nylon-based rotomolded components are gaining traction in automotive and industrial environments that require enhanced wear resistance, while polypropylene finds use in chemical handling and technical parts. Although their combined share remains well below polyethylene, these materials benefit from rising demand for higher-value, application-specific solutions, which supports above-average growth within their niches through 2030.

The “others” category, which includes specialty resins and bio-based or partially bio-based materials, remains nascent but attracts growing interest as sustainability and producer responsibility regulations tighten in Europe and parts of North America. While current volumes are modest, pilot projects in compost bins, consumer products, and non-pressure liquid storage are creating reference use cases. This area is likely to expand at a faster CAGR than conventional grades, even if from a small base, as brand owners and regulators increasingly require lower carbon footprints and improved recyclability.

By Type

Virgin materials remain the primary feedstock in rotational molding. In 2024 they represented about 80 to 82 percent of total consumption and are projected to maintain a clear lead through at least 2028. Users in construction, chemicals, automotive, and industrial storage continue to specify virgin polyethylene, polypropylene, and PVC to meet stringent requirements for mechanical strength, stress cracking resistance, and long-term performance. The consistency of melt flow, color, and contamination levels also supports efficient processing and predictable part quality, which is critical for large parts where scrap or failure carries high cost.

Recycled materials, while still a minority share, are registering one of the fastest growth rates in the value chain. Regulatory pressure in Europe, EPR schemes, and brand-led sustainability commitments in consumer goods and agriculture are pushing adoption of high-quality recycled polyethylene in non-critical applications such as refuse containers, playground equipment, and some agricultural products. Between 2024 and 2030, several industry analysts expect recycled content in rotational molding to grow from low single digits to the 10 to 15 percent range in developed markets, provided supply of clean, traceable feedstock continues to improve.

However, quality variation, material contamination, and the limited availability of food-grade or pressure-rated recycled resins still constrain broader use. You see this particularly in applications such as potable water tanks, chemical storage, and safety-critical automotive components, where regulatory standards remain strict and testing costs are high. Over the medium term, investments in advanced sorting, mechanical recycling, and chemical recycling technologies should gradually improve the reliability of recycled grades and support their adoption in more demanding segments, but virgin materials will remain the reference standard in most high-performance uses.

By Form

Powder form remains the preferred feedstock for rotational molding, accounting for more than 80 percent of market volume in 2024 and expected to grow in line with overall market CAGR through 2030. Powdered resins provide better flow, faster sintering, and more uniform heat distribution inside the mold, which is critical for achieving even wall thickness on large parts and complex geometries. This advantage supports their use in storage tanks, material handling bins, playground equipment, and industrial housings, where dimensional stability and surface finish influence both performance and aesthetics.

The cost structure of powders also favors their continued use. Although grinding adds a processing step, the improved cycle times, lower defect rates, and reduced scrap can offset the additional cost in many applications. Powder allows tight control over particle size distribution, which directly affects fusion and mechanical properties; this gives manufacturers greater control over part performance and supports repeatable production at scale. As demand for custom colors, UV-stabilized grades, and functional additives grows, powder form offers a flexible platform for tailored formulations.

Granules hold a smaller share and are used mainly where in-house grinding capabilities or specialized processing systems are in place. Some producers adopt granules to reduce logistics costs or to feed integrated compounding and grinding operations, giving them control over formulation and quality. Over the forecast period, you can expect incremental growth in granules for vertically integrated players, but powder will remain the reference form for most third-party compounders and molders worldwide.

By Application

Storage tanks remain the single largest application segment for rotational molding materials. They accounted for close to 40 percent of global consumption in 2024 and will likely maintain a high-30s share through 2030. Demand is driven by water storage infrastructure, chemical handling, fuel tanks, and agricultural liquids across both developed and emerging markets. Rotomolded tanks offer seamless construction, corrosion resistance, and lower installed cost compared with steel in many use cases, which is especially relevant for remote or rural locations where maintenance access is limited.

Water scarcity, urban expansion, and climate resilience agendas underpin steady tank demand. Countries in Asia Pacific, the Middle East, and parts of Africa are investing in rainwater harvesting, on-site wastewater systems, and decentralized storage for agriculture and households. In parallel, regulatory scrutiny on chemical storage in North America and Europe supports upgrades from older metal tanks to corrosion-resistant plastic solutions that meet modern safety standards. Global demand for water tanks and chemical tanks is projected to grow in the mid-single-digit range annually through 2030, providing a stable base for material suppliers.

Beyond tanks, applications such as automotive components, containers, toys and leisure, and material handling equipment contribute diversified growth. Automotive demand focuses on specialized parts like fuel and DEF tanks for off-road vehicles, construction machinery, and agricultural equipment rather than high-volume passenger car components. Containers and material handling products benefit from e-commerce, warehouse automation, and food distribution trends, while toys and leisure products remain a smaller but visible niche. Industrial housings, ducts, and technical parts within the “others” category are expanding as designers recognize the benefits of low tooling cost and design flexibility for short and medium production runs.

By End-Use

Construction is the leading end-use sector for rotational molding materials, with an estimated share of about 24 to 25 percent in 2024. The sector uses rotomolded products such as water and septic tanks, road and traffic barriers, drainage components, and rooftop storage systems. As governments in Asia Pacific, Latin America, and Africa continue to invest in basic infrastructure and urban services, demand for durable, low-maintenance plastic components is set to rise. Industry forecasters expect construction-related rotomolded applications to grow at a CAGR of around 5 to 6 percent to 2030, supported by housing expansion and infrastructure renewal.

Chemical and food and beverage industries also represent significant demand centers. Chemical producers and distributors require corrosion-resistant tanks and containers for acids, alkalis, and specialty chemicals, while food and beverage operations use hygiene-friendly bins, containers, and auxiliary equipment that must meet regulatory standards. In these sectors, polyethylene tanks often compete with stainless steel, but offer a more attractive cost profile and easier installation for many non-pressurized systems. As safety, traceability, and quality regulations continue to tighten, users will focus more on certified materials and documented performance, which favors established suppliers with robust testing and compliance capabilities.

Automotive, agriculture, and consumer goods collectively add scale and product diversity. Agriculture uses rotomolded tanks, feeders, and equipment for liquid fertilizers and animal husbandry, particularly in North America, Brazil, and Australia. Automotive and off-highway equipment manufacturers adopt rotational molding for complex-shaped tanks and covers where blow molding or metal fabrication is less economical at medium production volumes. Consumer goods, including outdoor furniture, playground systems, and leisure products, are sensitive to discretionary spending but benefit from design flexibility and color options offered by rotomolding. Over time, growth in these segments will track broader macro trends in consumer spending, farm investments, and equipment markets.

By Region

Europe held the largest share of the global rotational molding materials market in 2024, at close to 30 percent by revenue. The region has a well-established base of molders and compounders serving construction, chemicals, agriculture, and high-spec industrial applications. Strong regulatory frameworks on product safety, recyclability, and emissions encourage adoption of high-quality materials and support premium pricing. Western Europe, in particular Germany, Italy, the UK, and France, leads in value-added applications such as certified chemical tanks, advanced material handling systems, and specialized industrial components.

Asia Pacific, however, is the fastest-growing regional market and is expected to narrow the gap with Europe before 2030. China, India, and Southeast Asian countries are increasing consumption of water storage tanks, agricultural equipment, and building-related plastic products in line with urbanization and rising incomes. The region benefits from lower labor costs and proximity to resin production hubs, which supports competitive production of large-volume items. Analysts project mid to high single-digit CAGR for rotational molding materials in Asia Pacific over the forecast period, driven by infrastructure build-out, manufacturing growth, and expanding domestic consumption.

North America remains a mature but solid market, with strong participation in construction, agriculture, and off-road equipment. The United States and Canada see steady replacement demand for aging water and chemical tanks and continued investments in agriculture and energy infrastructure. Latin America and the Middle East & Africa are smaller in current revenue terms but show growing needs for water management, agriculture, and decentralized utilities. In these regions, rotomolded tanks, sanitation products, and agricultural solutions play a central role in improving basic services. Over the next decade, rising investment in water security and agricultural productivity in these emerging markets is likely to support above-average growth for rotational molding materials, albeit from a lower base.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Material Type

- Polyethylene

- LLDPE

- HDPE

- XLPE

- MDPE

- LDPE

- Polycarbonate

- Nylon

- Polyvinyl Chloride

- Polyesters

- Polypropylene

- Others

By Type

- Virgin

- Recycled

By Form

- Powder

- Granules

By Application

- Storage Tanks

- Automotive Components

- Containers

- Toys and Leisure

- Materials Handling

- Industrial

- Others

By End-Use

- Construction

- Automotive

- Agriculture

- Consumer Goods

- Chemical

- Food & Beverage

- Others

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3,478.3 M |

| Forecast Revenue (2034) | USD 5,763.0 M |

| CAGR (2025-2034) | 5.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material Type (Polyethylene, Polycarbonate, Nylon, Polyvinyl Chloride, Polyesters, Polypropylene, Others), By Type (Virgin, Recycled, By Form, Powder, Granules), By Application (Storage Tanks, Automotive Components, Containers, Toys and Leisure, Materials Handling, Industrial, Others), By End-Use (Construction, Automotive, Agriculture, Consumer Goods, Chemical, Food & Beverage, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Xiamen Keyuan Plastic Co., Ltd, Prisma Colour Limited, ExxonMobil, SCG Chemicals, DOMO Chemicals, Broadway Colours, PTT Global Chemical Public Company Limited, Kalpataru Polymer Private Limited, Pinaxis Polymer, Matrix Polymers Limited, OSWAL HITECH PVT. LTD., Roto Polymers, Petrotech Group, Reliance Industries Limited, GreenAge Industries, LyondellBasell Industries Holdings B.V., Mabaplast, Rototech Industries, SABIC, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Type (Virgin, Recycled), By Form (Powder, Granules), By Application (Storage Tanks, Automotive Components, Containers, Toys & Leisure, Materials Handling, Industrial), By End-Use (Construction, Automotive, Agriculture, Consumer Goods, Chemical, Food & Beverage) – Trends & Forecast 2025–2034")

, By Type (Virgin, Recycled), By Form (Powder, Granules), By Application (Storage Tanks, Automotive Components, Containers, Toys & Leisure, Materials Handling, Industrial), By End-Use (Construction, Automotive, Agriculture, Consumer Goods, Chemical, Food & Beverage) – Trends & Forecast 2025–2034")

, By Type (Virgin, Recycled), By Form (Powder, Granules), By Application (Storage Tanks, Automotive Components, Containers, Toys & Leisure, Materials Handling, Industrial), By End-Use (Construction, Automotive, Agriculture, Consumer Goods, Chemical, Food & Beverage) – Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Rotational Molding Materials Market?

The rotational molding materials market was valued at USD 3,290.7M in 2024 and is projected to reach USD 5,763.0M by 2034, growing at a CAGR of 5.7% from 2026–2034. Explore market trends and growth outlook.

Who are the major players in the Rotational Molding Materials Market?

Xiamen Keyuan Plastic Co., Ltd, Prisma Colour Limited, ExxonMobil, SCG Chemicals, DOMO Chemicals, Broadway Colours, PTT Global Chemical Public Company Limited, Kalpataru Polymer Private Limited, Pinaxis Polymer, Matrix Polymers Limited, OSWAL HITECH PVT. LTD., Roto Polymers, Petrotech Group, Reliance Industries Limited, GreenAge Industries, LyondellBasell Industries Holdings B.V., Mabaplast, Rototech Industries, SABIC, Other Key Players

Which segments covered the Rotational Molding Materials Market?

By Material Type (Polyethylene, Polycarbonate, Nylon, Polyvinyl Chloride, Polyesters, Polypropylene, Others), By Type (Virgin, Recycled, By Form, Powder, Granules), By Application (Storage Tanks, Automotive Components, Containers, Toys and Leisure, Materials Handling, Industrial, Others), By End-Use (Construction, Automotive, Agriculture, Consumer Goods, Chemical, Food & Beverage, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Rotational Molding Materials Market

Published Date : 27 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date