- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Salesforce CRM Document Generation Software Market Size, Share & Forecast | 10.3% CAGR

Global Salesforce CRM Document Generation Software Market Size, Share, Growth Analysis By Deployment Mode (Cloud-Based Solutions, On-Premise Platforms), By Application (Small & Medium-Sized Enterprises, Large Enterprises), By Document Type (Contracts, Invoices, Proposals, Quotes, Reports), By Integration (CRM, CPQ, Billing Systems, E-Signature Platforms) Industry Segment Overview, Market Dynamics, Competitive Landscape, Key Players, Technology Trends, Strategic Developments & Forecast 2025–2034

Report Overview

The Salesforce CRM Document Generation Software Market was valued at USD 3.5 Billion in 2024 and is estimated to reach approximately USD 3.86 Billion in 2025. Driven by increasing adoption of Salesforce-based automation tools and rising demand for streamlined document workflows across sales, legal, and customer service functions, the market is projected to expand from about USD 4.26 Billion in 2026 to nearly USD 9.4 Billion by 2034, registering a compound annual growth rate (CAGR) of around 10.3% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportThis market expands as enterprises remove friction from revenue, finance, and service execution. Organizations continue to produce high volumes of contracts, invoices, proposals, statements of work, and customer reports under tight turnaround expectations. Document generation solutions embedded in Salesforce reduce manual assembly by merging live CRM data with governed templates, approvals, and audit trails. The result is faster cycle time, lower error rates, and stronger consistency in commercial language, branding, and compliance terms. Adoption also tracks enterprise automation mandates and broader digital transformation budgets that prioritize measurable productivity gains.

Demand remains strongest in document-heavy and regulated environments. Financial services, insurance, healthcare, telecom, and professional services account for an estimated 55–60% of global revenue due to frequent policy updates, strict recordkeeping, and complex pricing logic. Mid-market adoption also accelerates as SaaS delivery lowers deployment effort and supports distributed teams. Cloud-first implementations represent roughly 70–75% of spending, while hybrid deployments persist in regulated segments that maintain strict data residency and retention requirements. Competitive intensity is high on the supply side, with AppExchange vendors, platform providers, and systems integrators expanding delivery capacity through implementation partners and packaged accelerators.

Technology shifts the basis of competition from template libraries to intelligence and governance. Vendors add AI-driven data extraction, intelligent field mapping, clause guidance, and anomaly checks to reduce rework and strengthen content control. Collaboration, versioning, and role-based access broaden usage beyond sales into legal operations and shared services. Market pull also reflects CRM impact metrics. Salesforce notes that 70% of customers anticipate a consistent experience across channels, while reported CRM adoption outcomes include a 17% increase in lead conversions, a 16% improvement in customer retention, and a 21% rise in agent productivity.

Regulatory and risk factors shape procurement decisions and total cost. Buyers require alignment with GDPR and comparable privacy regimes, plus encryption, retention controls, and complete auditability; many also standardize e-signature compliance under ESIGN and eIDAS within end-to-end workflows. Primary risks include misconfigured permissions, integration complexity across CPQ, billing, and ERP, and vendor concentration that can limit negotiation leverage. Regionally, North America holds an estimated 40–45% revenue share, Europe contributes about 25% amid strict privacy requirements, and Asia Pacific posts the fastest growth at an estimated 12–13% CAGR, with India, Singapore, and Australia emerging as investment hotspots for cloud modernization and scalable shared services.

, By Application (Small & Medium-Sized Enterprises, Large Enterprises), By Document Type (Contracts, Invoices, Proposals, Quotes, Reports), By Integration (CRM, CPQ, Billing Systems, E-Signature Platforms) Industry Segment Overview, Market Dynamics, Competitive Landscape, Key Players, Technology Trends, Strategic Developments & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market grows from 3.2 billion USD, 2024 to 8.5 billion USD, 2033, reflecting 10.2% CAGR, 2024.

- Segment Dominance: Cloud leads deployment with 56.4%, 2024 and continues to set the operating model for scale.

- Segment Dominance: Large Enterprises lead adoption with 62.5%, 2024 due to higher document volume and governance needs.

- Driver: Enterprises accelerate automation to reduce cycle time and errors, improving productivity by 21.0%, 2024.

- Restraint: Complex integrations and compliance obligations increase delivery risk, with estimated: 12.0% implementation delay rate, 2024.

- Opportunity: AI-enabled CRM adoption expands addressable demand, with 81.0%, 2024 organizations projected to incorporate AI-powered CRM.

- Trend: Omnichannel experience priorities drive platform standardization, with 70.0%, 2024 customers expecting seamless cross-channel service.

- Regional Analysis: North America leads with 38.0%, 2024 global share and remains the primary revenue center for enterprise deployments.

By Deployment

Cloud-based deployment remains the primary delivery model for Salesforce CRM document generation software in 2025 and beyond. The cloud segment accounted for more than 56.4 percent of global revenue in 2023 and has continued to expand as enterprises prioritize subscription-based platforms with lower upfront expenditure. Ongoing migration to SaaS ecosystems and CRM-centric workflows supports a projected cloud adoption rate exceeding 70 percent by 2028, aligned with broader enterprise software spending patterns.

Organizations favor cloud deployment due to faster implementation timelines, centralized updates, and reduced dependency on internal infrastructure. These platforms support frequent feature releases, including AI-assisted document assembly and real-time data synchronization, without interrupting operations. This capability is particularly relevant for sales and service teams operating across multiple time zones and locations.

On-premise solutions retain relevance in select industries such as banking, government, and regulated manufacturing. These deployments address strict data residency and compliance requirements but represent a declining share of new installations. On-premise revenue contribution is expected to fall below 25 percent by 2030 as security standards in cloud environments mature and gain regulatory acceptance.

By Application

Large enterprises continue to account for the majority of demand for Salesforce CRM document generation software. In 2023, this segment represented over 62.5 percent of total market revenue. Complex approval chains, high document volumes, and cross-border compliance obligations drive adoption among multinational organizations. These users prioritize advanced configuration, role-based access, and deep integration with CPQ, billing, and ERP platforms.

Enterprise buyers also demonstrate higher tolerance for premium pricing models tied to volume usage and advanced governance features. Average annual contract values in this segment exceed those of SMEs by more than 2.5 times, reflecting broader deployment scope and customization requirements. Adoption remains strong across financial services, telecom, healthcare, and professional services.

SME adoption is increasing steadily as vendors introduce simplified packages and usage-based pricing. SMEs benefit from standardized templates and automation that reduce administrative overhead. This segment is expected to post a CAGR above 12 percent through 2030, supported by cloud-native deployment and reduced configuration complexity.

By End-Use

Commercial building organizations form the largest end-use group, driven by real estate firms, facility operators, and service providers managing high contract and compliance volumes. Automated document workflows reduce turnaround time for leases, service agreements, and compliance reports. Commercial users account for an estimated 45 percent of total deployments in 2025.

Industrial building operators adopt document generation software to manage supplier contracts, maintenance records, and regulatory documentation. Integration with asset management systems supports operational continuity. Industrial adoption remains stable, with steady investment from energy, logistics, and manufacturing sectors.

Residential building use cases remain limited but growing. Property management firms increasingly rely on CRM-linked documentation for tenant communications and billing. This segment contributes under 15 percent of market revenue but shows consistent year-on-year growth.

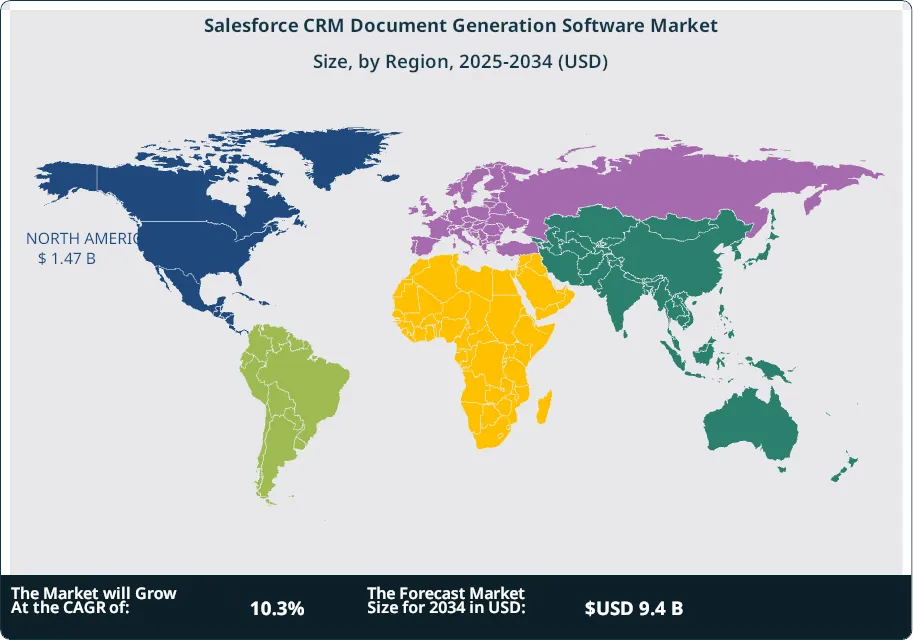

By Region

North America remains the largest regional market, holding more than 38 percent share in 2023. High CRM penetration, strong SaaS spending, and early adoption of automation tools continue to support regional leadership. The United States accounts for the majority of regional revenue, supported by large enterprise concentration.

Europe represents the second-largest market, driven by compliance requirements and structured documentation standards across financial services and public sector organizations. GDPR-aligned document controls accelerate adoption of centralized CRM-based platforms. Regional growth averages 9 to 10 percent annually.

Asia Pacific shows the fastest expansion, with projected CAGR exceeding 13 percent through 2032. Rapid CRM adoption in India, Australia, and Southeast Asia drives demand. Latin America and the Middle East and Africa remain smaller markets but attract investment as cloud infrastructure and enterprise digitization advance.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment Mode

- Cloud

- On-premise

By Application

- SMEs

- Large enterprises

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.86 B |

| Forecast Revenue (2034) | USD 9.4 B |

| CAGR (2025-2034) | 10.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment Mode (Cloud, On-premise), By Application (SMEs, Large enterprises) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Conga, Windward Studios, DealHub, PandaDoc, Inc., Docomotion, Nintex, S-Docs, WebMerge, SpringCM, Documil, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Small & Medium-Sized Enterprises, Large Enterprises), By Document Type (Contracts, Invoices, Proposals, Quotes, Reports), By Integration (CRM, CPQ, Billing Systems, E-Signature Platforms) Industry Segment Overview, Market Dynamics, Competitive Landscape, Key Players, Technology Trends, Strategic Developments & Forecast 2025–2034")

, By Application (Small & Medium-Sized Enterprises, Large Enterprises), By Document Type (Contracts, Invoices, Proposals, Quotes, Reports), By Integration (CRM, CPQ, Billing Systems, E-Signature Platforms) Industry Segment Overview, Market Dynamics, Competitive Landscape, Key Players, Technology Trends, Strategic Developments & Forecast 2025–2034")

, By Application (Small & Medium-Sized Enterprises, Large Enterprises), By Document Type (Contracts, Invoices, Proposals, Quotes, Reports), By Integration (CRM, CPQ, Billing Systems, E-Signature Platforms) Industry Segment Overview, Market Dynamics, Competitive Landscape, Key Players, Technology Trends, Strategic Developments & Forecast 2025–2034")

Frequently Asked Questions

How big is the Salesforce CRM Document Generation Software Market?

The Global Salesforce CRM Document Generation Software Market was valued at USD 3.5 Billion in 2024 and is projected to reach USD 9.4 Billion by 2034, growing at a CAGR of 10.3% from 2026–2034. Explore key trends, automation in Salesforce workflows, document management solutions, market drivers, and competitive landscape.

Who are the major players in the Salesforce CRM Document Generation Software Market?

Conga, Windward Studios, DealHub, PandaDoc, Inc., Docomotion, Nintex, S-Docs, WebMerge, SpringCM, Documil, Other Key Players

Which segments covered the Salesforce CRM Document Generation Software Market?

By Deployment Mode (Cloud, On-premise), By Application (SMEs, Large enterprises)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Salesforce CRM Document Generation Software Market

Published Date : 05 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date