- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Sand Control Systems Market Size, Share & Forecast 2034 | CAGR 5.8%

Global Sand Control Systems Market Size, Share, Analysis By Type (Gravel Pack Systems, Premium Screen Systems, Frac-Pack Systems, Expandable and Conformable Sand Management Systems), By Location (Onshore Sand Control Systems, Offshore Sand Control Systems), By Well Type (Horizontal Wells, Vertical Wells, Deviated and Multilateral Wells), By Application (Oil Wells, Gas Wells, Water Injection and Injector Wells) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Drilling Technology Trends & Forecast 2026–2034

Report Overview

| Market Size, 2025 | Forecast Value, 2034 | CAGR, 2026-2034 | Leading Region, 2025 |

| USD 3.5 Billion | USD 5.8 Billion | 5.8% | North America, 30.0% |

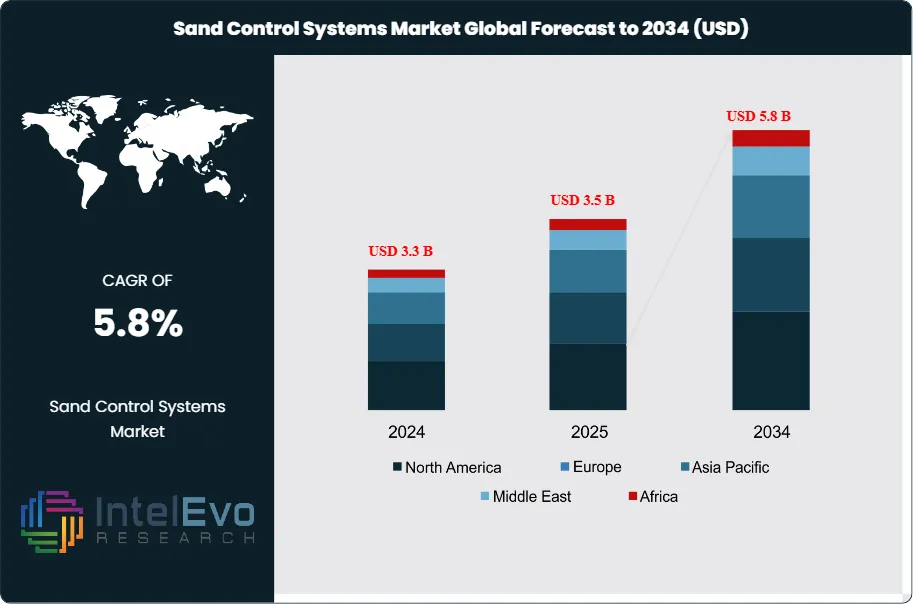

The Sand Control Systems Market was valued at USD 3.3 billion in 2024 and is projected to reach approximately USD 3.5 billion in 2025. The market is further expected to expand to nearly USD 5.8 billion by 2034, registering a compound annual growth rate (CAGR) of about 5.8% during the forecast period from 2026 to 2034. The Sand Control Systems Market is expanding because operators continue to drill longer horizontals, deepen offshore developments, and extend production from weakly consolidated reservoirs where sand influx can damage pumps, chokes, flowlines, and separators. Current public market references broadly support a 2025 market in the mid-USD 3 billion range, and this report uses a balanced midpoint with a CAGR that is mathematically consistent with the 2025 base and 2034 forecast.

Get More Information about this report -

Request Free Sample ReportThe Sand Control Systems Market remains tied to one simple operating fact. Sand production cuts well life and raises field cost. That is why the market stays relevant across offshore Brazil, the Gulf of America, the Middle East, Southeast Asia, and mature land fields where reservoir strength is weak and drawdown is high. Gravel packs, frac packs, premium screens, inflow control devices, and expandable screens remain the main technical choices. Market demand is strongest in offshore and deepwater developments, where the cost of intervention is high and where screen failure or pack failure can shut in major production volumes. In North America, horizontal shale and artificial-lift heavy fields also support demand for surface and downhole sand-management systems, including pump-intake protection and remedial sand-control work.

The Sand Control Systems Market is also shaped by standards and environmental controls. API Spec 19SS remains the key screen-equipment standard, covering design, validation, manufacturing, quality, storage, and transport of sand screens. In offshore environments, OSPAR measures continue to reduce discharges of hazardous chemicals and drilling fluids, which reinforces demand for reliable completions that minimize failure risk and repeat intervention. These regulatory and technical filters favor suppliers with validated hardware, testing capability, and strong offshore field records.

Technology is now shifting competitive advantage. Premium mesh screens, autonomous inflow control integration, modular gravel-pack systems, and electric and digital completions are pushing sand control toward smarter, lower-intervention designs. SLB won an offshore Brazil completions contract in September 2025 that will use advanced completion technologies in deepwater wells. Halliburton secured Petrobras deepwater completion contracts in October 2025. Weatherford won a multi-year integrated completions contract in Denmark in February 2026. These moves show that sand control is becoming a core part of integrated completion design in high-value wells.

Regional investment also supports the outlook. The Middle East is expected to invest about USD 130 Billion in oil and gas supply in 2025, while Petrobras’ 2025–2029 strategic plan earmarks USD 77 Billion for exploration and production. Those capital flows support higher use of sand control systems in both new wells and brownfield redevelopment. The main risks remain oil-price volatility, project deferrals, and supply-chain pressure on completion hardware. Even so, the Sand Control Systems Market should maintain steady growth because sand exclusion remains essential to production continuity in both offshore and onshore assets.

, By Location (Onshore Sand Control Systems, Offshore Sand Control Systems), By Well Type (Horizontal Wells, Vertical Wells, Deviated and Multilateral Wells), By Application (Oil Wells, Gas Wells, Water Injection and Injector Wells) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Drilling Technology Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Sand Control Systems Market was valued at USD 3.5 Billion in 2025 and is projected to reach USD 5.8 Billion by 2034, at a CAGR of 5.8% during 2026–2034.

- Segment Dominance: By type, gravel pack systems led with 34.0% share in 2025, equal to USD 1.2 Billion.

- Segment Dominance: By location, onshore sand control systems held 57.0% share in 2025, equal to USD 2.0 Billion.

- Driver: The main driver is rising high-value completions activity in deepwater and mature reservoirs. Petrobras awarded SLB an USD 800 million offshore services contract in December 2024 tied to more than 100 deepwater wells.

- Restraint: The main restraint is hardware cost and procurement pressure. Baker Hughes said in April 2025 that tariffs could cut full-year core profit by USD 100 million to USD 200 million.

- Opportunity: The biggest opportunity is integration of screens, ICDs, and intelligent completion tools in deepwater wells, highlighted by SLB’s September 2025 Brazil contract and Weatherford’s February 2026 Denmark award.

- Trend: The clearest trend is premium screen and digital completion integration. SLB’s PumpGuard systems helped a Permian operator increase ESP run life by 400% and reach 96% uptime.

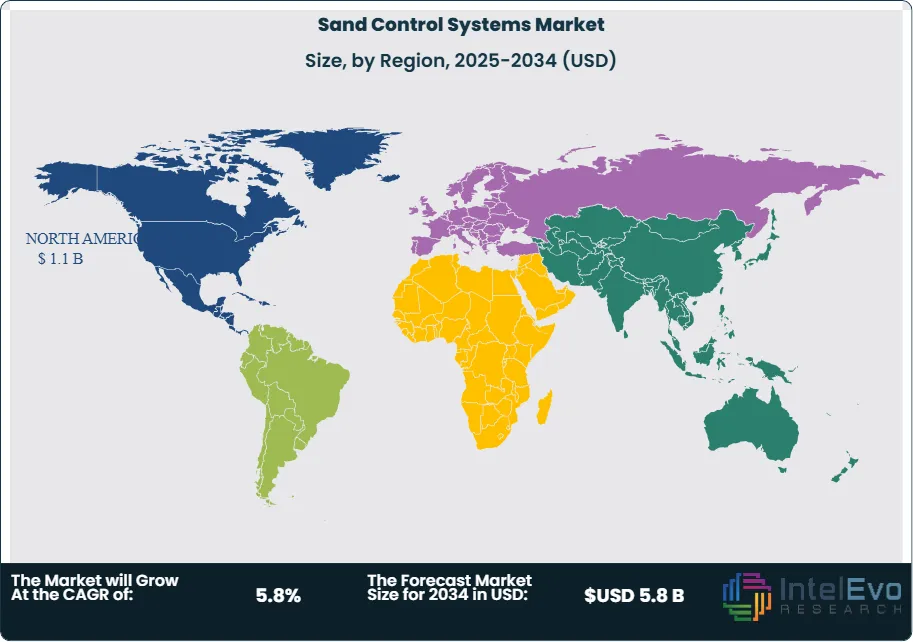

- Regional Analysis: North America led the Sand Control Systems Market with 30.0% share in 2025, equal to USD 1.1 Billion, supported by shale activity, remedial work, and a large installed base.

Competitive Landscape

The Sand Control Systems Market is moderately consolidated. The top four companies, SLB, Halliburton, Baker Hughes, and Weatherford, controlled an estimated 49.0% of global revenue in 2025. Competition is technology-driven in offshore and deepwater projects, but it is service-plus-price driven in land markets. Competitive intensity increased in 2025–2026 as SLB expanded deepwater completions in Brazil, Halliburton won Petrobras completion work, and Weatherford added a Denmark integrated completions contract. The market still leaves room for niche challengers because operators often buy around specific screen, packer, or gravel-placement performance rather than only global brand scale.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| SLB | US | Leader | MeshRite / PumpGuard / sand control screens | Latin America, Middle East, North America | Won a major Petrobras completions contract in Sep 2025 for ultra-deepwater Brazil wells. |

| HALLIBURTON | US | Leader | Sand Control portfolio / FlexRite completion system | Latin America, Middle East, North America | Won Petrobras deepwater completion and stimulation contracts in Oct 2025 for Brazil. |

| BAKER HUGHES | US | Leader | EXCELLPAK gravel-pack screen / GeoFORM conformable sand management | North America, offshore global, Middle East | Announced a mature-fields redevelopment framework with Hunt in Dec 2025, supporting higher-value completion and sand-management work. |

| WEATHERFORD | US | Leader | ESS expandable sand screens / FloReg ICDs / Maxflo screens | Europe, Middle East, Latin America | Won a multi-year integrated completions contract in Denmark in Feb 2026. |

| NOV | US | Challenger | Completion and screen-adjacent downhole portfolio | North America, Middle East | Maintained offshore and completion equipment momentum through 2025 across adjacent well-construction systems. |

| TAM INTERNATIONAL | US | Challenger | Swellable packers and completion isolation tools | North America, Middle East | Continued positioning in openhole completions and sand-control-adjacent isolation systems through 2025. |

| INNOVEX | US | Challenger | RLDe subsea wellhead and completion-adjacent systems | North America, offshore global | Became OneSubsea’s exclusive wellhead partner in Sep 2025, strengthening offshore completion supply-chain relevance. |

| PACKERS PLUS | Canada | Niche Player | Openhole completion and packer systems | North America, Middle East | Continued deployment of openhole completion tools into 2025 and early 2026 basin programs. |

| JEREH | China | Niche Player | Completion tools and regional well service systems | Asia Pacific, Middle East | Expanded regional oilfield technology visibility in 2025 through stronger ADNOC-linked initiatives. |

| DUNEFRONT | US | Niche Player | Sand-control design and modeling services | North America, offshore Latin America | Reported 2025 project work involving openhole horizontal gravel-pack design with AICD-equipped screens. |

By Type

Gravel pack systems held the largest share of the Sand Control Systems Market at 34.0% in 2025, equal to USD 1.2 Billion. They lead because they remain the most broadly accepted method for unconsolidated formations, offshore wells, and long laterals where screen-only solutions may not provide enough protection. Premium screen systems accounted for 27.0% in 2025, or USD 0.9 Billion. This segment includes wire-wrap, mesh, pre-pack, and erosion-resistant screen configurations. Frac-pack systems represented 21.0% in 2025, equal to USD 0.7 Billion, driven mainly by high-rate offshore and cased-hole completions. Expandable and conformable sand-management systems made up the remaining 18.0% in 2025, or USD 0.6 Billion. These products remain smaller in revenue but are growing in remedial and complex-well applications where adaptability is worth a price premium. Competitive strength is concentrated among vendors that combine screen design, packer integration, pumping execution, and completion modeling rather than those selling screens alone.

By Location

Onshore sand control systems accounted for 57.0% share in 2025, equal to USD 2.0 Billion. The segment leads because land well counts are much higher than offshore well counts, especially in North American shale, Middle East conventional drilling, and selective Latin American land programs. Onshore work also supports repeat demand for remedial sand-control systems, pump-intake protection, and thru-tubing solutions in fields where sand production appears after initial completion. Offshore sand control systems represented 43.0% in 2025, or USD 1.5 Billion. Offshore unit volumes are lower, but revenue per well is significantly higher because deepwater and platform environments require stricter hardware qualification, longer design cycles, and stronger placement reliability. The location split therefore reflects a classic volume-versus-value market. Land systems dominate by quantity and installed base, but offshore projects drive premium technology adoption, stronger margins, and faster uptake of AICD-linked and intelligent completion-compatible designs.

By Well Type

Horizontal wells formed the largest well-type segment with 46.0% share in 2025, equivalent to USD 1.6 Billion. This dominance reflects the way long reservoir contact increases both productivity and sanding risk. Horizontal wells often require more complex gravel placement, stronger inflow balancing, and better control of fines migration than vertical wells. Vertical wells accounted for 30.0% in 2025, or USD 1.1 Billion. They remain important in conventional fields, mature assets, and selected offshore completions where simpler architecture still supports strong economics. Deviated and multilateral wells made up 24.0% in 2025, equal to USD 0.8 Billion. These wells create more selective but higher-value demand because sand placement and flow distribution become harder as geometry grows more complex.

By Application

Oil wells accounted for 61.0% share in 2025, equal to USD 2.1 Billion. They lead because the broadest installed base of sand-control applications still sits in oil-producing reservoirs with unconsolidated formations, high drawdown, and artificial-lift exposure. Gas wells represented 24.0% in 2025, or USD 0.8 Billion. Gas completions can require high-integrity sand control in weak sandstone and offshore gas developments, but total market volume remains lower than oil. Water injection and injector wells accounted for 15.0% in 2025, equal to USD 0.5 Billion. This smaller segment still matters because injectors also require reliable screen and completion integrity to prevent solids movement and maintain sweep performance. The application mix matters strategically because oil wells drive broad recurring demand, gas wells drive higher-spec technical requirements, and injectors create a smaller but technically necessary market for premium reliability.

Regional Analysis

North America Sand Control Systems Market

North America held 30.0% share in 2025, equal to USD 1.1 Billion. The United States dominates the region, followed by Canada, Mexico, and the Rest of North America. The region leads because it combines high land-well volume, strong remedial work demand, and a large installed base of artificial lift and completion hardware vulnerable to sand-related failure. The U.S. market alone was valued at USD 1.01 Billion in 2023 and is projected to reach USD 1.43 Billion by 2029, which supports North America’s leading global position. Demand is strongest in shale and tight-oil areas where operators need screens, gravel packs, pump-intake protection, and thru-tubing remedial solutions. Canada adds demand through heavy oil, thermal wells, and mature assets, while Mexico contributes through offshore and selective land projects. The main challenge is price sensitivity in land markets. Even so, the region remains the largest market because of sheer well count, installed infrastructure, and recurring intervention needs.

Europe Sand Control Systems Market

Europe accounted for 16.0% share in 2025, equal to USD 0.6 Billion. The UK, Norway, Germany, and Denmark are the key countries, with the North Sea acting as the true commercial center. Europe remains a high-value region because offshore wells require high-integrity sand-control systems and strong environmental discipline. Norway and the UK dominate spending because of offshore field concentration and mature-asset redevelopment. Denmark has gained visibility through Weatherford’s February 2026 integrated completions contract supporting offshore operations for TotalEnergies. Europe’s competitive structure favors vendors with deep offshore track records and integrated completion capability. The main growth limit is lower well volume than North America or the Middle East. The main strength is high average revenue per well because offshore complexity and qualification standards remain demanding.

Asia Pacific Sand Control Systems Market

Asia Pacific captured 21.0% share in 2025, equal to USD 0.7 Billion. China, Japan, India, and Australia are the most relevant countries, followed by the Rest of Asia Pacific. China leads through broad upstream activity and a large regional oilfield-service base. India supports offshore and gas-field demand, while Australia contributes premium sand-control demand through offshore gas and technically complex wells. Asia Pacific benefits from a favorable mix of offshore gas, mature sandstone reservoirs, and rising completion complexity. Regional competition is split between global majors and a growing set of Asia-based equipment manufacturers. Asia Pacific should outgrow Europe through 2034 because it combines a broad project base with stronger long-term offshore gas potential.

Latin America Sand Control Systems Market

Latin America held 14.0% share in 2025, equal to USD 0.5 Billion. Brazil dominates the region, followed by Mexico, Argentina, and the Rest of Latin America. Brazil is the core market because offshore pre-salt and deepwater developments require premium sand-control systems inside larger completion scopes. Petrobras’ December 2024 award to SLB, valued at USD 800 million, covers integrated services across offshore fields and more than 100 deepwater wells. Halliburton added more deepwater completion contracts in October 2025, and SLB secured another major completions award in September 2025 for ultra-deepwater work. The region should remain one of the best markets for premium gravel-pack, frac-pack, and intelligent-completion-compatible sand-control systems through 2034.

Middle East & Africa Sand Control Systems Market

Middle East & Africa represented 19.0% share in 2025, equal to USD 0.7 Billion. Saudi Arabia, the UAE, South Africa, and the Rest of MEA define the region, though Gulf producers generate most revenue. The region remains one of the best long-term growth zones because the Middle East is expected to invest about USD 130 Billion in oil and gas supply in 2025. Saudi Arabia and the UAE lead due to large conventional fields, gas expansion, and strong use of completion technologies in sand-prone reservoirs. The region should remain one of the fastest-growing areas through 2034 because sustained upstream spending supports both new-well installations and sand-control retrofits in mature assets.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Gravel Pack Systems

- Premium Screen Systems

- Frac-Pack Systems

- Expandable and Conformable Sand Management Systems

By Location

- Onshore Sand Control Systems

- Offshore Sand Control Systems

By Well Type

- Horizontal Wells

- Vertical Wells

- Deviated and Multilateral Wells

By Application

- Oil Wells

- Gas Wells

- Water Injection and Injector Wells

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.5 B |

| Forecast Revenue (2034) | USD 5.8 B |

| CAGR (2025-2034) | 5.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Gravel Pack Systems, Premium Screen Systems, Frac-Pack Systems, Expandable and Conformable Sand Management Systems), By Location (Onshore Sand Control Systems, Offshore Sand Control Systems), By Well Type (Horizontal Wells, Vertical Wells, Deviated and Multilateral Wells), By Application (Oil Wells, Gas Wells, Water Injection and Injector Wells) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, NOV, TAM INTERNATIONAL, INNOVEX, PACKERS PLUS, JEREH, DUNEFRONT, JOHNSON SCREENS, OIL STATES, HUNTING, AXON PRESSURE PRODUCTS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Location (Onshore Sand Control Systems, Offshore Sand Control Systems), By Well Type (Horizontal Wells, Vertical Wells, Deviated and Multilateral Wells), By Application (Oil Wells, Gas Wells, Water Injection and Injector Wells) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Drilling Technology Trends & Forecast 2026–2034")

, By Location (Onshore Sand Control Systems, Offshore Sand Control Systems), By Well Type (Horizontal Wells, Vertical Wells, Deviated and Multilateral Wells), By Application (Oil Wells, Gas Wells, Water Injection and Injector Wells) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Drilling Technology Trends & Forecast 2026–2034")

, By Location (Onshore Sand Control Systems, Offshore Sand Control Systems), By Well Type (Horizontal Wells, Vertical Wells, Deviated and Multilateral Wells), By Application (Oil Wells, Gas Wells, Water Injection and Injector Wells) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Drilling Technology Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Sand Control Systems Market?

Global Sand Control Systems Market was valued at USD 3.3 billion in 2024 and is projected to reach USD 5.8 billion by 2034, growing at a CAGR of 5.8%. Explore key trends, offshore drilling demand, and advanced sand control technologies.

Who are the major players in the Sand Control Systems Market?

SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, NOV, TAM INTERNATIONAL, INNOVEX, PACKERS PLUS, JEREH, DUNEFRONT, JOHNSON SCREENS, OIL STATES, HUNTING, AXON PRESSURE PRODUCTS, Others

Which segments covered the Sand Control Systems Market?

By Type (Gravel Pack Systems, Premium Screen Systems, Frac-Pack Systems, Expandable and Conformable Sand Management Systems), By Location (Onshore Sand Control Systems, Offshore Sand Control Systems), By Well Type (Horizontal Wells, Vertical Wells, Deviated and Multilateral Wells), By Application (Oil Wells, Gas Wells, Water Injection and Injector Wells)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date