- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Saudi Arabia Remotely Operated Vehicle (ROV) Market Size & Forecast 2034 | CAGR 10.2%

Saudi Arabia Remotely Operated Vehicle (ROV) Market Size, Share & Industry Analysis By Type (Work-Class ROVs, Inspection-Class ROVs, Observation-Class ROVs), By Depth Rating (Shallow Water, Midwater, Deepwater), By Power (Up to 100 HP, 100–200 HP, Above 200 HP), By Application (Oil & Gas, Offshore Construction, Scientific Research, Defense & Security) – Industry Trends, Competitive Landscape & Forecast 2025–2034

Report Overview

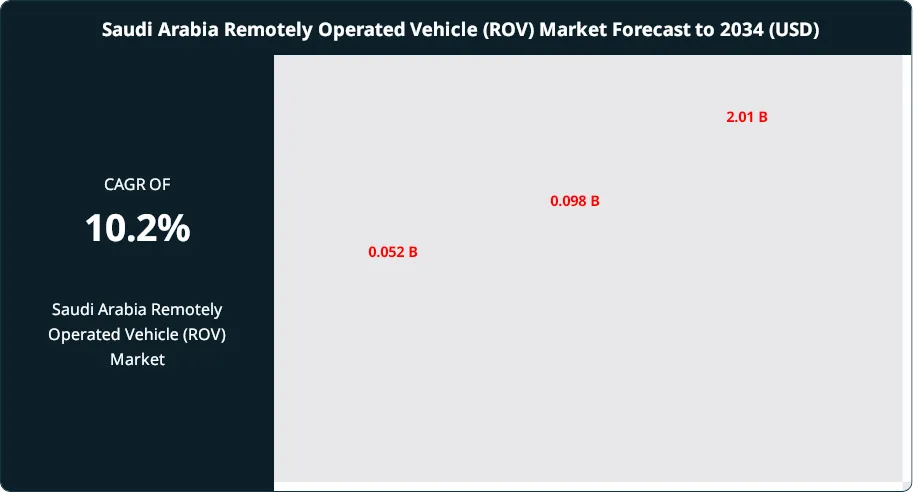

The Saudi Arabia Remotely Operated Vehicle (ROV) Market was valued at approximately USD 0.052 billion in 2024 and is projected to reach nearly USD 2.01 billion by 2034, reflecting strong expansion driven by offshore energy exploration, subsea infrastructure inspection, and defense applications. Based on the projected growth trajectory, the market size for 2025 is estimated at around USD 0.098 billion. Beginning in 2026, the market is expected to grow at a compound annual growth rate (CAGR) of about 10.2% from 2026 to 2034, ultimately reaching an estimated valuation of approximately USD 2.01 billion by 2034. This growth trajectory reflects the increasing dependence on highly capable subsea robotics for operations in deep-water and hazardous environments where human intervention is limited or impractical.

Get More Information about this report -

Request Free Sample ReportROVs form a critical component of the broader underwater robotics ecosystem, supporting a wide spectrum of applications across commercial, military, scientific, and renewable energy domains. These systems, typically outfitted with high-resolution imaging, advanced sensors, and manipulator arms, enable operators to conduct precise underwater inspection, maintenance, repair, and data-gathering missions. Their role has become particularly essential as industries shift toward more complex subsea infrastructure and deeper offshore operations.

The oil and gas sector continues to represent the largest demand center for ROVs, deploying them extensively for subsea pipeline inspection, rig installation, asset integrity management, and decommissioning. Meanwhile, defense organizations leverage ROV platforms for mine detection, explosive ordnance disposal, reconnaissance, and salvage operations, driven by rising maritime security requirements. Scientific and environmental agencies also depend on ROVs for oceanographic studies, ecosystem monitoring, and deep-sea exploration, expanding their relevance in research and conservation initiatives.

Market expansion is underpinned by several structural drivers. Continued investment in offshore oil and gas exploration, along with the accelerated rollout of offshore wind farms, is significantly increasing the need for versatile subsea robotic systems. In parallel, global defense modernization programs are amplifying procurement of advanced unmanned underwater systems. Growing awareness of environmental risks and the need for real-time subsea data further reinforces market demand.

Rapid technological progress remains a defining catalyst for market growth. Innovations in autonomous navigation, machine vision, real-time data analytics, lightweight material engineering, and power management are enhancing the operational range, precision, and efficiency of modern ROVs. As these platforms continue to integrate greater automation and AI-enabled capabilities, they are expected to play an increasingly strategic role across mission-critical underwater operations.

Overall, the ROV market is positioned for strong and sustained expansion as industries worldwide adopt more sophisticated subsea technologies to support energy transition, security imperatives, and scientific discovery.

Market Size, Share & Industry Analysis By Type (Work-Class ROVs, Inspection-Class ROVs, Observation-Class ROVs), By Depth Rating (Shallow Water, Midwater, Deepwater), By Power (Up to 100 HP, 100–200 HP, Above 200 HP), By Application (Oil & Gas, Offshore Construction, Scientific Research, Defense & Security) – Industry Trends, Competitive Landscape & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global ROV market grows from 2.2 billion USD, 2023 to 8.2 billion USD, 2034, reflecting a robust 11.3% CAGR, 2026-2034.

- Segment Dominance : Offshore oil and gas applications lead overall demand, contributing estimated: 40.0% revenue share, 2024. These operations deploy ROVs intensively for subsea pipeline inspection, infrastructure installation, and maintenance to safeguard production continuity.

- Segment Dominance: Defense, scientific research, and offshore wind collectively form the next wave of demand, accounting for estimated: 60.0% deployment share, 2024 beyond the core oil and gas base. These segments require high-specification ROVs with advanced sensors, cameras, and manipulators for complex underwater missions.

- Driver: Accelerating offshore exploration and production and rising investment in renewable energy assets drive ROV adoption, supported by an 11.0% market CAGR, 2023-2033. Advancements in robotics, sensing, and real-time data analytics further justify capital spending that exceeds estimated: 1.0 billion USD, 2024 across major operators.

- Restraint: High acquisition and operating costs, complex subsea logistics, and stringent regulatory requirements restrain broader ROV penetration, with sophisticated work-class units reaching estimated: 15.0 million USD per unit, 2024. Limited availability of skilled pilots and maintenance specialists further constrains deployment scale and project throughput.

- Opportunity: Expanding offshore wind farms and deep-sea environmental monitoring programs create new revenue streams, potentially adding estimated: 1.5 billion USD in incremental ROV-related spending, 2030. Vendors that align offerings with these high-growth use cases can capture significant share via specialized tooling, data services, and lifecycle support.

- Trend: Technology roadmaps emphasize greater autonomy, AI-enabled navigation, and enhanced data analytics, with next-generation systems expected to represent estimated: 50.0% of new ROV deliveries, 2030. Operators increasingly integrate ROV platforms into digital twins and remote operation centers to optimize subsea asset performance and reduce human exposure.

- Regional Analysis: North America and Europe currently lead ROV adoption, jointly contributing estimated: 55.0% revenue share, 2024 driven by mature offshore energy and defense programs. Asia-Pacific is poised to close the gap as offshore development and naval modernization accelerate toward an estimated: 2.0 billion USD market size, 2033.

By Type

Work-class ROVs continue to lead the market in 2025 as operators rely on their strength, stability, and tool-carrying capacity for high-risk offshore tasks. These systems account for the largest share of global deployments due to their role in drilling support, subsea construction, and complex intervention projects. Rising offshore activity in deep and ultra-deepwater fields reinforces demand as energy producers focus on asset reliability and operational safety.

Inspection-class ROVs hold a strong position as operators increase their use of compact, maneuverable vehicles for routine structural assessments. You will see sustained adoption as offshore platforms age and pipeline networks expand. The segment benefits from a steady shift toward planned inspection cycles and standardized maintenance protocols across major operators in North America, Europe, and Asia.

Observation-class ROVs attract interest from scientific agencies, universities, and environmental groups. Their lower acquisition costs and simple deployment procedures make them suitable for marine biology research, reef mapping, and coastal surveillance. Adoption expands further as governments increase funding for environmental monitoring and climate-impact studies.

Specialized ROVs fill niche requirements in defense, subsea mining, and advanced research. These vehicles often carry custom sensor packages or mission-specific tooling. Although they represent a smaller portion of global demand, they remain central to programs that require specialized underwater capabilities.

By Depth Rating

Shallow-water ROVs maintain broad usage as governments and commercial entities prioritize nearshore inspections and environmental assessments. You will find these units widely used in coastal infrastructure surveys, archaeological work, and habitat monitoring. Their lower cost of ownership appeals to small and mid-size service providers seeking reliable equipment for recurring nearshore assignments.

Midwater ROVs serve a balanced role for operators that require more capability than shallow-water systems but do not need the full specifications of deepwater vehicles. These units remain essential for pipeline inspections, asset integrity checks, and infrastructure repairs at intermediate depths. Their capacity to operate in variable current and pressure conditions keeps them relevant for diversified offshore portfolios.

Deepwater ROVs remain a high-value segment driven by continued activity in ultra-deepwater developments. These systems support drilling, completions, and production operations at depths beyond 2,000 meters. You will see rising demand as exploration programs return in Brazil, the Gulf of Mexico, and West Africa. High technical standards and advanced materials extend their operating limits, making them central to deep-sea research and commercial missions.

By Power

ROVs in the 100 to 200 HP range dominate global demand due to their balanced performance profile. These vehicles deliver enough thrust for moderate construction work, material handling, and salvage operations while maintaining maneuverability suitable for precision tasks. Offshore contractors favor this range as it supports a wide set of intervention requirements without significantly increasing operational costs.

ROVs up to 100 HP remain important for inspection work, environmental studies, and scientific missions. Their compact size supports entry into confined spaces and sensitive habitats. You will find these systems used by research organizations and smaller commercial fleets that prioritize accuracy and low operating expenses.

ROVs above 200 HP serve heavy-duty industrial needs, including drill support, high-load lifting, and construction at extreme depths. This category represents a critical asset for major offshore operators that require powerful equipment capable of managing difficult terrain and demanding tool packages. Rising investment in deepwater energy projects continues to support adoption.

By Application

The oil and gas industry continues to hold the largest share of ROV demand in 2025 as operators rely on subsea systems for inspection, drilling support, and pipeline integrity tasks. High levels of deepwater activity and strict safety compliance requirements reinforce the need for reliable robotic intervention. You will see sustained procurement as companies extend the life of aging fields and expand into frontier basins.

Offshore construction uses ROVs for cable laying, foundation installation, and seabed preparation. Growth in offshore wind projects in Europe, China, and the United States increases the number of construction missions that require reliable subsea robotics. Contractors depend on ROVs to verify installation accuracy and ensure compliance with engineering plans.

Scientific research programs rely on ROVs for sampling, quantitative habitat surveys, and long-term ecosystem monitoring. As governments increase ocean observation budgets, research groups expand their use of robotics to reach depths inaccessible to divers.

Defense and security agencies deploy ROVs for mine clearance, port surveillance, and underwater recovery. Rising maritime security concerns and modernization programs in Asia and Europe support stronger adoption. Other sectors, including aquaculture and water infrastructure, continue to expand their use of ROVs for routine inspection and maintenance.

By Region

North America remains the largest regional market in 2025 due to its strong offshore energy base, mature defense sector, and extensive research activities. The United States accounts for most of the regional demand as operators maintain a large fleet of work-class ROVs for deepwater operations in the Gulf of Mexico. Canada contributes additional growth driven by Arctic research and coastal inspection programs.

Europe maintains a significant share supported by offshore wind expansion, subsea engineering expertise, and robust inspection requirements. The United Kingdom, Norway, and the Netherlands remain central hubs for ROV manufacturing and deployment. You will see consistent procurement tied to renewable energy development and subsea service contracts.

Asia Pacific emerges as the fastest-growing market. China, Japan, and South Korea expand R&D spending and increase maritime security investments. Offshore exploration in India and Southeast Asia adds further demand for work-class and inspection-class systems.

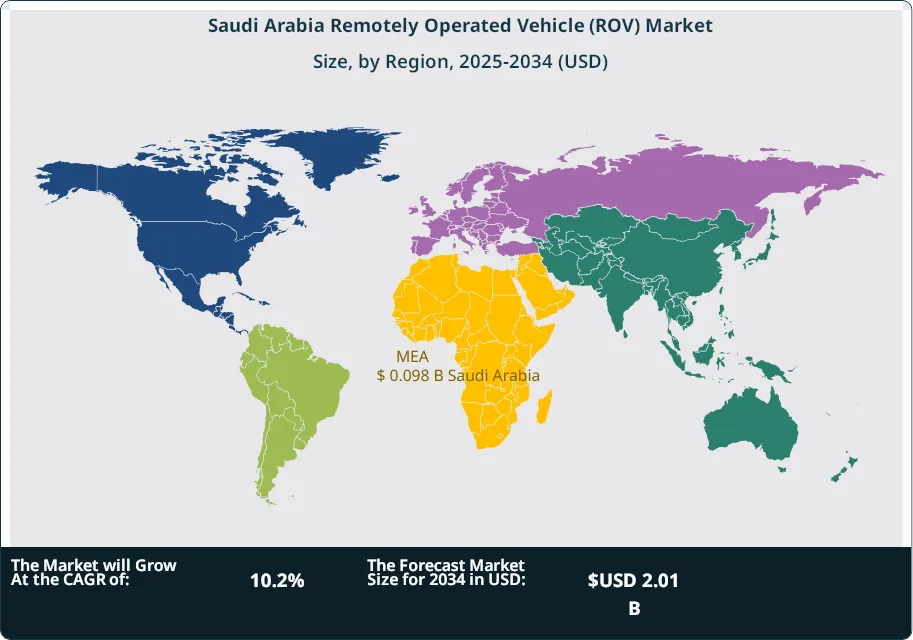

Latin America and the Middle East & Africa show steady adoption driven by offshore oil and gas projects in Brazil, Mexico, Saudi Arabia, and the UAE. Deepwater fields in Brazil and West Africa sustain long-term requirements for high-capacity ROV fleets.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Work-Class ROVs

- Inspection-Class ROVs

- Observation-Class ROVs

- Others

By Depth Rating

- Shallow Water ROVs

- Midwater ROVs

- Deepwater ROVs

By Power

- Upto 100 HP

- 100 – 200 HP

- Above 200 HP

By Application

- Oil and Gas Industry

- Offshore Construction

- Scientific Research

- Defense and Security

- Others

By Regions

SAUDI ARABIA

| Report Attribute | Details |

| Market size (2025) | USD 0.098 B |

| Forecast Revenue (2034) | USD 2.01 B |

| CAGR (2025-2034) | 10.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Work-Class ROVs, Inspection-Class ROVs, Observation-Class ROVs, Others), By Depth Rating (Shallow Water ROVs, Midwater ROVs, Deepwater ROVs), By Power (Upto 100 HP, 100 – 200 HP, Above 200 HP), By Application (Oil and Gas Industry, Offshore Construction, Scientific Research, Defense and Security, Others) |

| Research Methodology |

|

| Regional scope | Saudi Arabia |

| Competitive Landscape | Oceaneering International, Inc., Deep Ocean Group, Aquabotix Technology Corporation, Forum Energy Technologies, Inc., Saab Seaeye Limited, Ocean Aero, Kongsberg Maritime AS, Ocean Infinity, Subsea 7 S.A., Atlas Elektronik GmbH, Blue Robotics, Inc., TechnipFMC plc, DOF Subsea AS, Fugro, ECA Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Market Size, Share & Industry Analysis By Type (Work-Class ROVs, Inspection-Class ROVs, Observation-Class ROVs), By Depth Rating (Shallow Water, Midwater, Deepwater), By Power (Up to 100 HP, 100–200 HP, Above 200 HP), By Application (Oil & Gas, Offshore Construction, Scientific Research, Defense & Security) – Industry Trends, Competitive Landscape & Forecast 2025–2034")

Market Size, Share & Industry Analysis By Type (Work-Class ROVs, Inspection-Class ROVs, Observation-Class ROVs), By Depth Rating (Shallow Water, Midwater, Deepwater), By Power (Up to 100 HP, 100–200 HP, Above 200 HP), By Application (Oil & Gas, Offshore Construction, Scientific Research, Defense & Security) – Industry Trends, Competitive Landscape & Forecast 2025–2034")

Market Size, Share & Industry Analysis By Type (Work-Class ROVs, Inspection-Class ROVs, Observation-Class ROVs), By Depth Rating (Shallow Water, Midwater, Deepwater), By Power (Up to 100 HP, 100–200 HP, Above 200 HP), By Application (Oil & Gas, Offshore Construction, Scientific Research, Defense & Security) – Industry Trends, Competitive Landscape & Forecast 2025–2034")

Frequently Asked Questions

How big is the Saudi Arabia Remotely Operated Vehicle (ROV) Market?

Saudi Arabia ROV Market valued at USD 0.052 Billion in 2024 is projected to reach USD 2.01 Billion by 2034, growing at a CAGR of 10.2%. Estimated at USD 0.098 Billion in 2025, driven by offshore energy, subsea inspection, and defense demand.

Who are the major players in the Saudi Arabia Remotely Operated Vehicle (ROV) Market?

Oceaneering International, Inc., Deep Ocean Group, Aquabotix Technology Corporation, Forum Energy Technologies, Inc., Saab Seaeye Limited, Ocean Aero, Kongsberg Maritime AS, Ocean Infinity, Subsea 7 S.A., Atlas Elektronik GmbH, Blue Robotics, Inc., TechnipFMC plc, DOF Subsea AS, Fugro, ECA Group

Which segments covered the Saudi Arabia Remotely Operated Vehicle (ROV) Market?

By Type (Work-Class ROVs, Inspection-Class ROVs, Observation-Class ROVs, Others), By Depth Rating (Shallow Water ROVs, Midwater ROVs, Deepwater ROVs), By Power (Upto 100 HP, 100 – 200 HP, Above 200 HP), By Application (Oil and Gas Industry, Offshore Construction, Scientific Research, Defense and Security, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Saudi Arabia Remotely Operated Vehicle (ROV) Market

Published Date : 27 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date