- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Security Service Edge (SSE) Market Size, Trends 2034 | 21.6% CAGR

Global Security Service Edge (SSE) Market Size, Share, Analysis By Component (Solutions, Services), By Organization Size (SMEs, Large Enterprises), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By End User (BFSI, IT & Telecom, Healthcare, Government & Public Sector, Manufacturing, Retail & E-commerce, Energy & Utilities), Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034

Report Overview

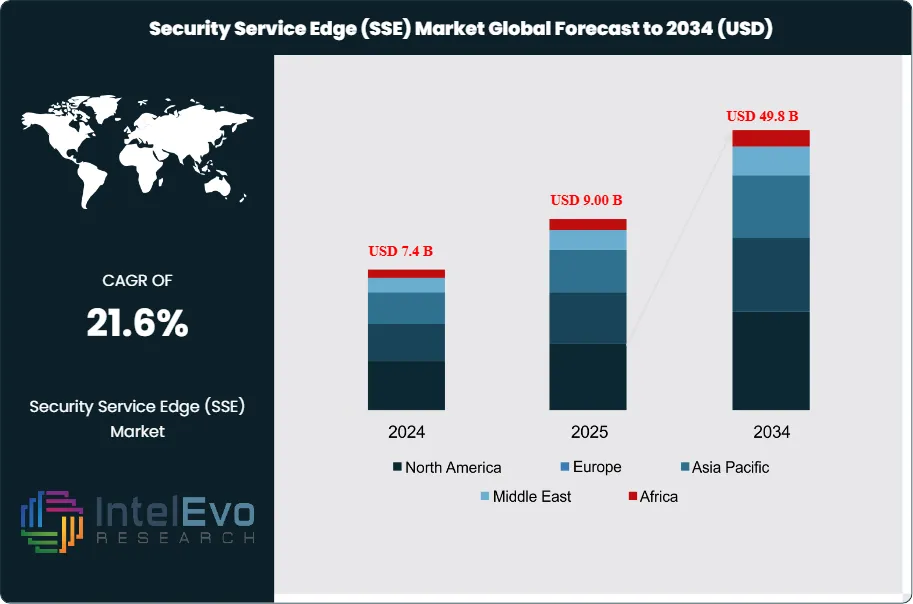

The Global Security Service Edge (SSE) Market size is expected to be worth around USD 49.8 billion by 2034, up from USD 7.4 billion in 2024, growing at a CAGR of 21.6% during the forecast period from 2025 to 2034. The market’s rapid growth is driven by the surge in remote work adoption, cloud migration, and increasing cybersecurity threats that demand integrated cloud-based security frameworks. SSE solutions combining Secure Web Gateway (SWG), Cloud Access Security Broker (CASB), and Zero Trust Network Access (ZTNA) are becoming essential for modern enterprises. As organizations embrace hybrid IT infrastructures, the demand for scalable and unified security services will continue to accelerate globally.

Get More Information about this report -

Request Free Sample ReportA rapidly changing sector of the cybersecurity landscape, the Security Service Edge (SSE) industry is characterized by the incorporation of security features into cloud-based infrastructure. SSE solutions give companies a complete architecture that lets them instantly secure their networks, data, and apps. These solutions, which are designed to meet the growing need for security in distributed contexts, include tools like zero-trust network access (ZTNA), cloud access security brokers, and secure web gateways. As businesses move more and more to remote work models and hybrid cloud architectures, the necessity to protect data and the growing acceptance of cloud technologies are driving the SSE market.

One of the main factors propelling the SSE market's growth is the adoption of Zero Trust security methods. In order to secure digital assets even in a setting without a perimeter, zero trust principles emphasize confirming each user and device trying to access network resources. This concept is in line with the increasing requirement for businesses to safeguard confidential information, particularly as remote and hybrid workforces become more common. SSE solutions are increasingly essential in a number of areas, such as government, manufacturing, healthcare, and finance. For instance, SSE is being used by financial institutions to protect sensitive financial data and guarantee adherence to strict laws like GDPR and PCI DSS. SSE aids in the protection of patient data in the healthcare industry, particularly as the use of electronic health records (EHR) grows. SSE tackles the hazards associated with industrial systems and connected devices in manufacturing. Strong security frameworks offered by SSE solutions are in high demand due to the expanding requirement for remote access, secure cloud collaboration, and compliance across industries.

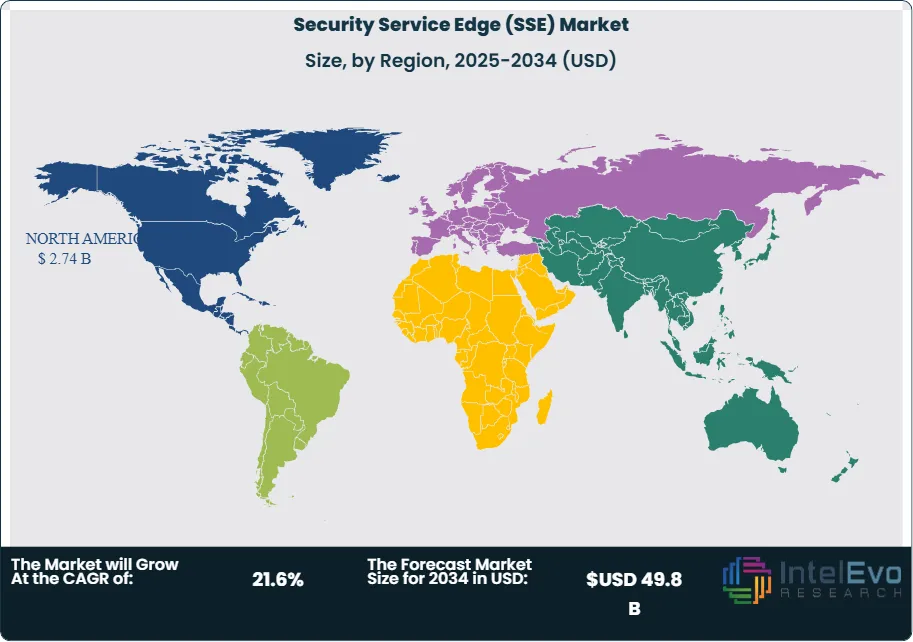

North America is considered to have the highest growth market for Security Service Edge (SSE) mainly due to high regulatory concerns and increasing demand for safety and security towards data. Furthermore, the need for sophisticated security solutions has increased due to a high degree of digitization. The capacity of SSE to safeguard edge settings becomes increasingly important as more and more companies embrace remote and hybrid work practices. Additionally, a strong ecosystem of cybersecurity providers and the region's established technology infrastructure support the expansion of SSE services. Adoption of SSE solutions is further accelerated by the focus on data protection and compliance, which makes North America a vital hub for the thriving SSE sector.

COVID 19 has had a mixed effect on the market size of Security Service Edge (SSE). Businesses' approaches to cybersecurity were profoundly impacted by the COVID-19 epidemic, which sped up the adoption of new security concepts and technology. The growing use of remote work during this period was one of the most significant changes, forcing businesses to reevaluate their security protocols. One important way to address these changing demands is using Security Service Edge (SSE).

Market Size, Share, Analysis By Component (Solutions, Services), By Organization Size (SMEs, Large Enterprises), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By End User (BFSI, IT & Telecom, Healthcare, Government & Public Sector, Manufacturing, Retail & E-commerce, Energy & Utilities), Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Key Takeaways

- Market Growth: The Security Service Edge (SSE) market is expected to reach USD 49.8 billion by 2034, growing at a robust CAGR of 21.6%, indicating strong market expansion.

- Component Segment Dominance: The component segment is dominated by solutions, accounting for over 58% of the market share. The need to strengthen cybersecurity in ever-changing digital environments is driving the growing use of Security Service Edge (SSE) solutions, which include technologies such as FWaaS (Firewall as a Service), ZTNA (Zero Trust Network Access), SWG (Secure Web Gateways), CASB (Cloud Access Security Broker), and others.

- Industry Vertical Segment Insights: BFSI is anticipated to hold the largest market share, reflecting the sector’s need for robust security measures. Because of the high value of the data involved and the growing sophistication of cyber threats, the BFSI sector confronts many cybersecurity challenges.

- Driver: The significance of putting strong security measures in place at the edge to identify and stop threats before they reach vital assets is becoming more widely recognized as a result of the rise in cyberattacks that target businesses. Advanced threat detection and response capabilities are frequently included in SSE solutions, which support market growth dynamics by fostering a more proactive and efficient security posture.

- Restraint: Concerns about data privacy and compliance are serious obstacles for the SSE industry. Concerns about maintaining regulatory compliance and safeguarding user privacy grew as businesses processed and stored sensitive data at the edge more and more. It may be difficult to adopt SSE solutions while adhering to various industry standards and data protection rules, especially in highly regulated industries like healthcare and banking.

- Opportunity: Significant prospects exist in the Security Service Edge market due to the growing demand for hybrid cloud solutions, the need for improved compliance management, the development of AI-powered security, and the growth of small and mid-sized enterprises.

- Trend: It is anticipated that the use of AI and ML technology in SSE solutions would increase. These tools can improve threat detection, automate security incident response, and offer predictive analytics to spot possible dangers. SSE platforms may become more flexible and able to respond to new cyberthreats instantly by utilizing AI and ML.

- Regional Analysis: The market for security services is expanding in North America. The region's high degree of digitization and proactive commitment to cybersecurity have increased demand for cutting-edge security solutions. The capacity of SSE to safeguard edge settings becomes increasingly important as more and more companies embrace remote and hybrid work practices.

Component Analysis:

Security Service Edge (SSE) market can be categorized by material. These include solutions and services. The SSE framework's solutions comprise a range of hardware and software for controlling and safeguarding network access to data and apps. Secure online gateways, cloud access security brokers, and zero-trust security network access are just a few of the integrated security features that these systems are intended to provide. In the SSE market, services are just as important as solutions, which have the largest market share. The deployment, operation, and maintenance of SSE systems are supported by professional and managed services. These services are crucial for businesses who want to improve their security measures without making large upfront costs or that lack the internal knowledge to handle complicated security environments.

End User Industry Analysis:

There are three categories for industry verticals: the Banking, Financial Services, and Insurance (BFSI) sector. The BFSI sector holds the largest market share during the forecast period. The sector's stringent legal requirements and the vital necessity for strong data protection procedures to safeguard sensitive financial data are the main causes of this dominance.

Because of the high value of the data involved and the growing sophistication of cyber threats, the BFSI sector confronts many cybersecurity challenges. In order to provide safe data access, guard against data breaches, and adhere to national and international laws like GDPR, PCI-DSS, and others that need stringent data security protocols, financial institutions are thus major users of SSE solutions.

Region Analysis:

North America Leads With 37% Market Share in the Security Service Edge (SSE) Market. North America and Asia-Pacific are the regions with the highest market shares for Security Service Edge (SSE), driven by increased need for cloud security solutions and advanced cybersecurity infrastructure. North America holds approximately 37% of the market share, owing to the increasing cyberthreats and stringent data protection laws in sectors like government, healthcare, and finance. North America's early adoption of cloud technology, the abundance of cybersecurity providers, and sophisticated regulatory frameworks like HIPAA and GDPR are important reasons contributing to its substantial market dominance. The region's focus on safeguarding cloud environments and remote workers also makes a substantial contribution to the Security Service Edge (SSE) market's expansion.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Component

- Solutions

- Secure Web Gateway (SWG)

- Cloud Access Security Broker (CASB)

- Zero Trust Network Access (ZTNA)

- Firewall as a Service (FWaaS)

- Data Loss Prevention (DLP)

- Services

- Professional Services

- Managed Services

By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

By Deployment Mode

- Cloud-Based Deployment

- On-Premises Deployment

- Hybrid Deployment

By End User Industry

- BFSI

- IT & Telecommunications

- Healthcare

- Government & Public Sector

- Manufacturing

- Retail & E-commerce

- Energy & Utilities

- Others (Education, Transportation, etc.)

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 9.00 B |

| Forecast Revenue (2034) | USD 49.8 B |

| CAGR (2025-2034) | 21.6% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Solutions, (Secure Web Gateway (SWG), Cloud Access Security Broker (CASB), Zero Trust Network Access (ZTNA), Firewall as a Service (FWaaS), Data Loss Prevention (DLP)), Services, (Professional Services, Managed Services)), By Organization Size (Small and Medium Enterprises (SMEs), Large Enterprises), By Deployment Mode (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment), By End User Industry (BFSI, IT & Telecommunications, Healthcare, Government & Public Sector, Manufacturing, Retail & E-commerce, Energy & Utilities, Others (Education, Transportation, etc.)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Zscaler, Inc., Palo Alto Networks, Inc., Netskope, Inc., Cisco Systems, Inc., Cloudflare, Inc., Forcepoint LLC, McAfee Corp., Akamai Technologies, Fortinet, Inc., Broadcom Inc. (Symantec), Check Point Software Technologies Ltd., Versa Networks, Inc., Perimeter 81, Cato Networks, iboss, Inc., Proofpoint, Citrix, Kyndryl Inc., VMware, Aryaka |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Market Size, Share, Analysis By Component (Solutions, Services), By Organization Size (SMEs, Large Enterprises), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By End User (BFSI, IT & Telecom, Healthcare, Government & Public Sector, Manufacturing, Retail & E-commerce, Energy & Utilities), Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Market Size, Share, Analysis By Component (Solutions, Services), By Organization Size (SMEs, Large Enterprises), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By End User (BFSI, IT & Telecom, Healthcare, Government & Public Sector, Manufacturing, Retail & E-commerce, Energy & Utilities), Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Market Size, Share, Analysis By Component (Solutions, Services), By Organization Size (SMEs, Large Enterprises), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By End User (BFSI, IT & Telecom, Healthcare, Government & Public Sector, Manufacturing, Retail & E-commerce, Energy & Utilities), Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Frequently Asked Questions

How big is the Security Service Edge (SSE) Market?

Discover insights on the Global Security Service Edge (SSE) Market, projected to reach USD 49.8 billion by 2034 at a 21.6% CAGR. Explore key drivers and trends.

Who are the major players in the Security Service Edge (SSE) Market?

Zscaler, Inc., Palo Alto Networks, Inc., Netskope, Inc., Cisco Systems, Inc., Cloudflare, Inc., Forcepoint LLC, McAfee Corp., Akamai Technologies, Fortinet, Inc., Broadcom Inc. (Symantec), Check Point Software Technologies Ltd., Versa Networks, Inc., Perimeter 81, Cato Networks, iboss, Inc., Proofpoint, Citrix, Kyndryl Inc., VMware, Aryaka

Which segments covered the Security Service Edge (SSE) Market?

By Component (Solutions, (Secure Web Gateway (SWG), Cloud Access Security Broker (CASB), Zero Trust Network Access (ZTNA), Firewall as a Service (FWaaS), Data Loss Prevention (DLP)), Services, (Professional Services, Managed Services)), By Organization Size (Small and Medium Enterprises (SMEs), Large Enterprises), By Deployment Mode (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment), By End User Industry (BFSI, IT & Telecommunications, Healthcare, Government & Public Sector, Manufacturing, Retail & E-commerce, Energy & Utilities, Others (Education, Transportation, etc.))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Security Service Edge Market

Published Date : 17 Apr 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date