- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Seismic Data Acquisition Equipment Market Forecast | CAGR 6.8%

Global Seismic Data Acquisition Equipment Market Size, Share, Analysis By Equipment Type (Land Seismic Recording Systems, Marine Seismic Acquisition Systems, Seismic Sensors Including Geophones, Hydrophones, Accelerometers, MEMS, Auxiliary Equipment), By Technology (3D Seismic, 4D Time-Lapse Seismic, 2D Seismic, VSP & Transition Zone), By Application (Oil & Gas Exploration, Mining, Civil Engineering, Environmental Monitoring), By Deployment (Land, Marine, Airborne) Industry Region & Key Players – Market Dynamics, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 4.1 Billion, 2025 | USD 7.4 Billion, 2034 | 6.8%, 2026–2034 | North America, 36.2%, 2025 |

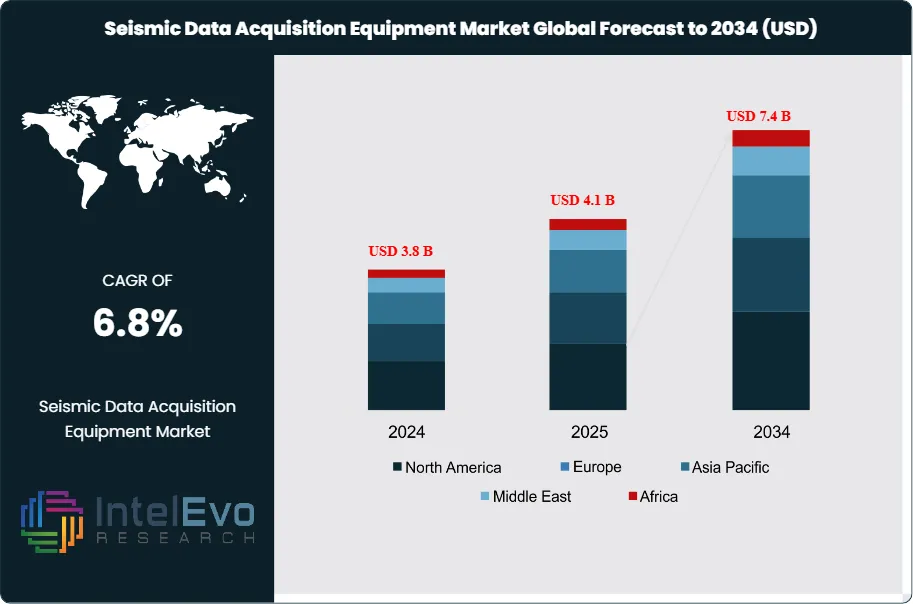

The Seismic Data Acquisition Equipment Market was valued at approximately USD 3.8 Billion in 2024 and increased to USD 4.1 Billion in 2025. The market is projected to reach nearly USD 7.4 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 6.8% during the forecast period from 2026 to 2034. Market growth is primarily driven by increasing exploration and production activities in oil and gas, particularly in deepwater and unconventional reservoirs, along with rising demand for advanced seismic imaging technologies. Additionally, expanding applications in mining, geothermal exploration, and infrastructure development, combined with advancements in nodal systems, wireless acquisition, and AI-enabled seismic technologies, are expected to further accelerate market expansion globally.

Get More Information about this report -

Request Free Sample ReportThe seismic data acquisition equipment market occupies a critical position within the global geophysical services industry, providing the instrumentation, sensors, and recording systems essential for subsurface imaging across oil and gas exploration, mining, civil engineering, and environmental monitoring. Market participants range from vertically integrated oilfield service multinationals to specialized hardware manufacturers, creating a moderately consolidated competitive structure where the top four players collectively account for approximately 58% of total revenue in 2025. Demand is primarily driven by sustained upstream capital expenditure cycles, the depletion of existing hydrocarbon reserves, and expanding exploration programs in frontier basins across the Middle East, Africa, and the Asia Pacific region.

The seismic data acquisition equipment market landscape is actively shaped by the transition from conventional wire-line recording systems toward wireless and autonomous nodal acquisition architectures. Wireless seismic data acquisition systems, which eliminate the need for physical cabling across survey arrays, accounted for approximately 34% of new equipment deployments in 2025 and are gaining share at an accelerated pace. This technological shift reduces operational costs, improves crew safety in remote terrain, and enables higher-density sensor grids that enhance subsurface imaging resolution. Equipment manufacturers are embedding real-time data telemetry, edge computing, and machine learning-assisted quality control into acquisition hardware, fundamentally altering the economics of large-scale land and marine survey programs.

Regulatory forces exert a dual influence on the seismic data acquisition equipment market. Environmental legislation governing seismic operations in marine and ecologically sensitive onshore environments has increased compliance costs for equipment operators, particularly in North America and Western Europe. At the same time, government-backed exploration mandates across national oil companies in Saudi Arabia, Iraq, China, and Brazil are generating predictable long-term procurement pipelines for acquisition hardware and sensor arrays. The International Energy Agency projected in its most recent outlook that upstream oil and gas investment will remain above USD 500 billion annually through 2027, providing a stable foundation for seismic survey equipment spending.

From a risk perspective, the seismic data acquisition equipment market faces cyclical exposure to oil price volatility. When Brent crude trades below USD 60 per barrel for extended periods, exploration budgets contract sharply, reducing equipment utilization rates and deferring capital upgrades. Conversely, the current energy security imperative, amplified by geopolitical disruptions and the structural underinvestment of 2020-2022, has restored E&P confidence and driven multi-year seismic campaign commitments across several major producing regions. Asia Pacific represents the fastest-growing investment hotspot for this market, with China's National Energy Administration targeting a 12% increase in domestic hydrocarbon exploration expenditure by 2027, directly benefiting seismic data acquisition equipment suppliers with established in-country manufacturing and service networks.

, By Technology (3D Seismic, 4D Time-Lapse Seismic, 2D Seismic, VSP & Transition Zone), By Application (Oil & Gas Exploration, Mining, Civil Engineering, Environmental Monitoring), By Deployment (Land, Marine, Airborne) Industry Region & Key Players – Market Dynamics, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Global Seismic Data Acquisition Equipment Market was valued at USD 4.1 Billion in 2025 and is projected to reach USD 7.4 Billion by 2034, expanding at a CAGR of 6.8% over the forecast period 2025–2034.

- Segment Dominance (By Equipment Type): Land-based seismic recording systems held the dominant share at approximately 42.3% of total seismic data acquisition equipment market revenue in 2025, underpinned by extensive shale and tight-formation exploration programs in North America and the Middle East.

- Segment Dominance (By Application): The oil and gas exploration segment accounted for the largest application share at approximately 67.4% of the seismic data acquisition equipment market in 2025, driven by persistent upstream capital spending and hydrocarbon reserve replenishment demands.

- Driver: Rising global upstream oil and gas capital expenditure, estimated at over USD 520 Billion in 2025, is the primary growth driver, directly funding new seismic survey campaigns and equipment procurement cycles.

- Restraint: Fluctuating crude oil prices and E&P budget volatility constrain equipment demand; a sustained price decline below USD 60 per barrel historically reduces exploration spending by 15–25%, creating cyclical headwinds for seismic data acquisition equipment manufacturers.

- Opportunity: The integration of autonomous nodal seismic acquisition systems in ultra-deepwater and remote frontier basins represents an addressable equipment opportunity exceeding USD 1.2 Billion by 2034, with early-mover vendors positioned to secure long-term service contracts.

- Trend: Wireless and nodal seismic data acquisition systems accounted for 34% of new equipment deployments in 2025 and are expected to surpass 55% by 2034, reflecting a structural shift away from conventional cable-based recording technologies.

- Regional Analysis: North America led the seismic data acquisition equipment market with a 36.2% share and USD 1.48 Billion in revenue in 2025, supported by high-density shale exploration programs across the Permian Basin, Marcellus, and Gulf of Mexico.

Competitive Summary

The seismic data acquisition equipment market is moderately consolidated. The top four players, Sercel (CGG), SLB (formerly Schlumberger), INOVA Geophysical, and Geospace Technologies, collectively held approximately 58% of total market revenue in 2025. Competition is primarily technology-driven, with differentiation based on sensor sensitivity, wireless node architecture, and integrated data management platforms. Competitive intensity increased materially during 2024–2026, with Sercel and SLB both expanding product portfolios through targeted acquisitions and next-generation node launches.

Competitive Landscape Matrix

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Sercel (CGG Group) | France | Leader | UNITE Wireless Node System | Europe, Global | Launched STRYDE Lite compact node platform (Feb 2025) |

| SLB (Schlumberger) | USA | Leader | WesternGeco IsoMetrix Marine System | North America, Global | Expanded partnership with Saudi Aramco for 3D land survey fleet (Apr 2025) |

| INOVA Geophysical | USA | Challenger | HAWK Full-Wave Seismic Recorder | North America | Secured multi-year contract with BGP Inc. for wireless nodes (Jan 2025) |

| Geospace Technologies | USA | Challenger | OBX Ocean-Bottom Node | North America, Asia Pacific | Announced USD 48M capacity expansion at Houston facility (Mar 2025) |

| BGP Inc. | China | Challenger | GeoEast Seismic Acquisition System | Asia Pacific, Middle East | Extended seismic survey fleet deployment across Iraq and Central Asia (Jun 2025) |

| Kinemetrics Inc. | USA | Niche Player | Episensor ES-T Accelerometer | North America, Europe | Partnered with USGS for national seismic monitoring network upgrade (Sep 2025) |

| Nanometrics Inc. | Canada | Niche Player | Centaur Digital Field System | North America | Integrated cloud-based data telemetry into Centaur platform (Nov 2025) |

| Geometrics Inc. | USA | Niche Player | Geode Seismic Recorder | North America, Latin America | Released Geode 3.0 with AI-assisted noise filtering (Jan 2026) |

| OYO Corporation | Japan | Niche Player | McSEIS-AT Shallow Seismic System | Asia Pacific | Expanded distribution with Indian geological survey agencies (Dec 2024) |

| Güralp Systems | UK | Niche Player | Certimus Broadband Seismometer | Europe, MEA | Delivered seismometer arrays for UAE national hazard monitoring (Feb 2026) |

By Equipment Type

The equipment type segmentation reveals that land-based seismic recording systems command the dominant position within the seismic data acquisition equipment market, accounting for approximately 42.3% of total market revenue, or USD 1.74 Billion in 2025. Land recording systems encompass multi-channel seismographs, shot-point controllers, field data recorders, and nodal acquisition units deployed across onshore survey programs in oil and gas, mining, and civil engineering. North American shale plays and Middle Eastern carbonate exploration programs drive the bulk of land equipment procurement. The performance advantage of modern land recorders, capable of managing thousands of simultaneous channels at sampling rates exceeding 2,000 samples per second, continues to attract capital investment from national oil companies seeking high-resolution reservoir models. Key manufacturers competing for land system contracts include Sercel, INOVA Geophysical, and Geospace Technologies.

Marine seismic equipment, including streamer arrays, ocean-bottom nodes, hydrophone cables, and air-gun sources, represented 31.6% of the seismic data acquisition equipment market, or approximately USD 1.30 Billion in 2025. Marine acquisition is strategically important for deepwater and ultra-deepwater exploration programs in the Gulf of Mexico, the pre-salt basins of Brazil, and the emerging offshore West African blocks. SLB's IsoMetrix system and Geospace Technologies' OBX ocean-bottom nodes hold leading positions in this sub-segment, with towed streamer configurations remaining cost-effective for regional 2D surveys and ocean-bottom systems preferred for high-resolution 3D imaging in complex subsalt geology. Regulatory constraints on marine seismic operations near protected marine areas in North America and Europe add compliance layers but have not materially suppressed equipment demand given the geographic concentration of marine programs in less regulated offshore zones.

Seismic sensors, including geophones, hydrophones, accelerometers, and MEMS-based sensors, represented approximately 14.8% of seismic data acquisition equipment market revenue, equating to USD 607 Million in 2025. Sensor performance directly determines the frequency bandwidth and amplitude fidelity of acquired seismic data, making sensor technology a primary competitive differentiator. MEMS accelerometers are progressively displacing conventional moving-coil geophones in high-frequency land applications due to their lower self-noise, broader frequency response, and ability to function correctly on uneven terrain. Kinemetrics and Güralp Systems lead the broadband sensor segment, while Sercel dominates the high-channel-count geophone market.

Auxiliary equipment, including seismic cables, connectors, power systems, positioning equipment, and vibroseis vehicles, accounted for the remaining 11.3% of the seismic data acquisition equipment market at approximately USD 463 Million in 2025. While individually lower in unit value, auxiliary components represent recurring replacement and consumable revenue that stabilizes supplier income through survey campaign cycles. Cable and connector demand is closely linked to land recording system deployments but is gradually declining as nodal wireless architectures reduce cabling requirements.

By Technology

The 3D seismic survey technology segment is the largest by application technology, holding a 47.2% share of the seismic data acquisition equipment market, valued at approximately USD 1.94 Billion in 2025. Three-dimensional surveys deliver volumetric subsurface imaging that enables accurate reservoir boundary mapping, well placement optimization, and structural interpretation. The rapid adoption of broadband 3D acquisition techniques, which extend usable frequency ranges both above and below conventional limits, has driven equipment upgrades across both land and marine segments. National oil companies in Saudi Arabia, Abu Dhabi, and Iraq have committed to large-scale 3D re-surveys of mature fields, generating sustained equipment demand.

The 4D seismic survey technology segment, also termed time-lapse seismic, captured approximately 19.6% of the seismic data acquisition equipment market in 2025, representing USD 804 Million. 4D surveys monitor fluid movement and pressure changes within producing reservoirs over time, improving enhanced oil recovery decisions and reducing unnecessary drilling. Adoption is concentrated in the North Sea, Gulf of Mexico, and Brazilian pre-salt assets where field life extension economics justify the additional acquisition cost. Technavio projected a 30% market share contribution from 4D seismic survey technology by 2025, consistent with the growing installed base of permanent monitoring systems.

The 2D seismic survey technology segment maintained a 23.8% share at USD 976 Million in 2025. Despite lower resolution compared to 3D methods, 2D surveys remain the standard for initial basin reconnaissance, cost-sensitive frontier exploration, and academic geological research. Demand concentrates in Latin America, Africa, and Southeast Asia where exploration programs prioritize cost efficiency over imaging resolution. The remaining 9.4% of the technology segment encompasses transition zone and vertical seismic profiling (VSP) systems.

By Application

The oil and gas exploration application segment accounted for 67.4% of the seismic data acquisition equipment market in 2025, representing USD 2.76 Billion. Oil and gas E&P companies represent the dominant customer base for seismic equipment manufacturers, with procurement directly tied to exploration and appraisal budgets. The persistent need to replace aging reserves, combined with growing deepwater and unconventional resource programs, ensures that oil and gas will remain the primary application through 2034.

Mining exploration represented 14.3% of the seismic data acquisition equipment market at USD 587 Million in 2025. The use of seismic reflection and refraction techniques to identify metalliferous ore bodies and map geological structures for mine planning has expanded significantly over the past decade. Copper, lithium, and gold exploration programs in Australia, Chile, and Canada are leading adopters. Civil engineering and infrastructure applications accounted for 10.2% at USD 418 Million, covering tunnel surveys, foundation assessment, and fault mapping for large construction projects. Environmental monitoring and academic research comprised the remaining 8.1% at USD 332 Million.

By Deployment

Land deployment commanded 58.7% of total seismic data acquisition equipment market revenue at USD 2.41 Billion in 2025. Land-based operations benefit from lower mobilization costs and the availability of established service infrastructure across North America, the Middle East, and Central Asia. Marine deployment captured 36.8% at USD 1.51 Billion, reflecting the higher per-unit equipment value associated with offshore streamer and ocean-bottom node systems. Airborne and transition zone deployments comprised the remaining 4.5% at USD 185 Million.

Regional Analysis

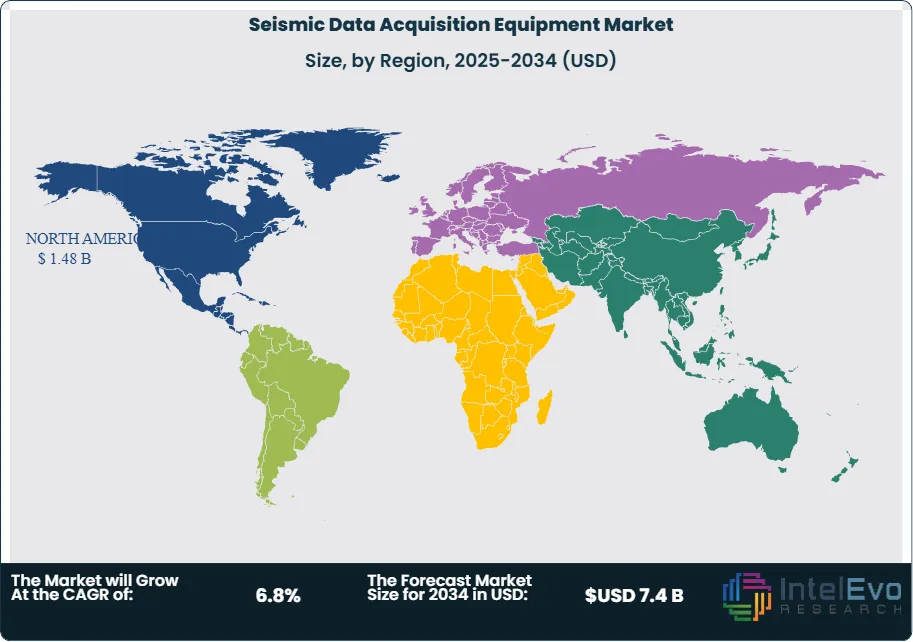

North America Seismic Data Acquisition Equipment Market

North America held the largest share of the global seismic data acquisition equipment market at 36.2%, equating to USD 1.48 Billion in 2025. The United States is the primary driver, accounting for approximately 82% of regional revenue through active shale exploration across the Permian Basin, Eagle Ford, and Marcellus formations. The Gulf of Mexico deepwater segment generates additional demand for marine seismic acquisition systems, with major operators investing in 3D ocean-bottom node surveys to optimize reservoir drainage patterns. Canada contributes approximately 13% of North American market revenue, driven by oil sands characterization projects in Alberta and offshore exploration off the Atlantic seaboard. Mexico's national energy company, Pemex, has increased seismic survey budgets following regulatory reforms that encourage renewed exploration in the Sureste Basin and shallow-water Gulf of Mexico blocks. The competitive environment in North America is the most intense globally, with all major seismic data acquisition equipment manufacturers maintaining regional offices, rental fleets, and technical service centers. U.S. government agencies, including the USGS, also drive demand for broadband seismometer arrays and permanent monitoring networks.

Europe Seismic Data Acquisition Equipment Market

Europe represented 21.4% of the seismic data acquisition equipment market at USD 877 Million in 2025. The United Kingdom remains Europe's largest single market, driven by North Sea basin monitoring, decommissioning-related subsurface characterization, and offshore carbon storage site assessment. Norway is the second-largest European market, where Equinor and its partners continue to invest in high-resolution 4D seismic acquisition across the Norwegian Continental Shelf to support mature field management. Germany contributes through industrial seismic monitoring, academic geophysical research, and geothermal exploration programs that require precision sensor arrays. France houses the global headquarters of Sercel and CGG, positioning it as the primary R&D and manufacturing hub for seismic data acquisition equipment in the region. EU carbon reduction policies have introduced a new application demand pathway: seismic imaging of geological carbon storage formations, which is expected to generate equipment procurement budgets of USD 180 Million by 2030 across the European carbon capture, utilization, and storage sector.

Asia Pacific Seismic Data Acquisition Equipment Market

Asia Pacific accounted for 26.8% of the seismic data acquisition equipment market at USD 1.10 Billion in 2025, positioning it as the fastest-growing region through the forecast period. China is the dominant country market, with BGP Inc. operating the world's largest fleet of land seismic acquisition crews. China National Petroleum Corporation and CNOOC drive domestic equipment demand through exploration programs in the Sichuan Basin, Tarim Basin, and South China Sea. India represents the fastest-growing single country within the region; the Directorate General of Hydrocarbons has mandated accelerated seismic coverage of under-explored sedimentary basins, and ONGC has committed to multi-year equipment upgrade cycles. Australia's mining sector, particularly iron ore and gold exploration in Western Australia, generates independent demand for seismic survey equipment outside the oil and gas segment. Japan's OYO Corporation serves domestic infrastructure and disaster-risk monitoring markets, providing a stable non-oil-and-gas demand baseline. Government subsidies for domestic energy security and significant capital flows from state-owned enterprises ensure that Asia Pacific will sustain a CAGR above the global market average through 2034.

Latin America Seismic Data Acquisition Equipment Market

Latin America captured 9.1% of the global seismic data acquisition equipment market at USD 373 Million in 2025. Brazil is the region's dominant market, with Petrobras executing large-scale 3D and 4D seismic acquisition programs across its pre-salt offshore blocks in the Santos and Campos Basins. These deepwater programs require advanced marine seismic acquisition systems, including autonomous ocean-bottom nodes and high-capacity streamer vessels, generating premium equipment procurement activity. Mexico occupies the second position in the region, with ongoing deepwater Gulf of Mexico exploration and shallow-water appraisal programs requiring both land and marine acquisition systems. Colombia is emerging as a growth market for land-based seismic equipment, particularly as the government promotes exploration in underexplored Llanos and Putumayo Basin acreage. Infrastructure constraints, currency volatility, and regulatory uncertainty in Argentina temper equipment investment despite significant shale resource potential in the Vaca Muerta formation. Latin America's overall contribution to the global seismic data acquisition equipment market is projected to expand, supported by Brazil's continued pre-salt investment program and growing mining exploration activity across the Andean nations.

Middle East and Africa Seismic Data Acquisition Equipment Market

The Middle East and Africa region represented 6.5% of the seismic data acquisition equipment market at USD 267 Million in 2025. Saudi Arabia is the largest individual market within the region, with Saudi Aramco operating one of the world's most extensive land seismic acquisition programs to map complex carbonate reservoirs in the Ghawar, Shaybah, and Marjan fields. The UAE's ADNOC is investing in 3D seismic re-surveys across its onshore and offshore concessions, generating procurement demand for both sensor arrays and data management systems. South Africa hosts southern Africa's primary seismic equipment service infrastructure and serves as a regional hub for sub-Saharan survey operations. Iraq and Kuwait are expanding their national seismic programs to support field development planning in prolific Mesopotamian Basin structures. Africa's frontier exploration activity, concentrated offshore East Africa and in the West African Transform Margin, adds incremental marine equipment demand. Geopolitical risk and project financing constraints periodically defer equipment purchases, but the region's long-term strategic importance to global oil supply ensures sustained seismic data acquisition equipment market participation through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Equipment Type

- Land Seismic Recording Systems

- Marine Seismic Acquisition Systems

- Seismic Sensors (Geophones, Hydrophones, Accelerometers, MEMS)

- Auxiliary Equipment (Cables, Connectors, Power Systems, Vibroseis Units)

By Technology

- 3D Seismic Survey

- 4D Seismic Survey (Time-Lapse)

- 2D Seismic Survey

- Vertical Seismic Profiling (VSP) and Transition Zone

By Application

- Oil and Gas Exploration

- Mining Exploration

- Civil Engineering and Infrastructure

- Environmental Monitoring and Academic Research

By Deployment

- Land

- Marine

- Airborne and Transition Zone

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.1 B |

| Forecast Revenue (2034) | USD 7.4 B |

| CAGR (2025-2034) | 6.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Equipment Type (Land Seismic Recording Systems, Marine Seismic Acquisition Systems, Seismic Sensors (Geophones, Hydrophones, Accelerometers, MEMS), Auxiliary Equipment (Cables, Connectors, Power Systems, Vibroseis Units)), By Technology (3D Seismic Survey, 4D Seismic Survey (Time-Lapse), 2D Seismic Survey, Vertical Seismic Profiling (VSP) and Transition Zone), By Application (Oil and Gas Exploration, Mining Exploration, Civil Engineering and Infrastructure, Environmental Monitoring and Academic Research), By Deployment (Land, Marine, Airborne and Transition Zone) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SERCEL (CGG GROUP), SLB (SCHLUMBERGER / WESTERNGECO), INOVA GEOPHYSICAL, GEOSPACE TECHNOLOGIES CORPORATION, BGP INC. (CHINA NATIONAL PETROLEUM CORPORATION), ION GEOPHYSICAL CORPORATION, KINEMETRICS INC., NANOMETRICS INC., GEOMETRICS INC., OYO CORPORATION, GÜRALP SYSTEMS LTD, GEOSENSE LTD, WIRELESS SEISMIC INC., TERREX SEISMIC, PARAGON GEOPHYSICAL SERVICES, DAWSON GEOPHYSICAL COMPANY, FUGRO N.V., TRIMBLE INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (3D Seismic, 4D Time-Lapse Seismic, 2D Seismic, VSP & Transition Zone), By Application (Oil & Gas Exploration, Mining, Civil Engineering, Environmental Monitoring), By Deployment (Land, Marine, Airborne) Industry Region & Key Players – Market Dynamics, Competitive Landscape & Forecast 2026–2034")

, By Technology (3D Seismic, 4D Time-Lapse Seismic, 2D Seismic, VSP & Transition Zone), By Application (Oil & Gas Exploration, Mining, Civil Engineering, Environmental Monitoring), By Deployment (Land, Marine, Airborne) Industry Region & Key Players – Market Dynamics, Competitive Landscape & Forecast 2026–2034")

, By Technology (3D Seismic, 4D Time-Lapse Seismic, 2D Seismic, VSP & Transition Zone), By Application (Oil & Gas Exploration, Mining, Civil Engineering, Environmental Monitoring), By Deployment (Land, Marine, Airborne) Industry Region & Key Players – Market Dynamics, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Seismic Data Acquisition Equipment Market?

Seismic data acquisition equipment market valued at USD 3.8B in 2024, reaching USD 7.4B by 2034, growing at a CAGR of 6.8% driven by E&P and AI-enabled seismic tech.

Who are the major players in the Seismic Data Acquisition Equipment Market?

SERCEL (CGG GROUP), SLB (SCHLUMBERGER / WESTERNGECO), INOVA GEOPHYSICAL, GEOSPACE TECHNOLOGIES CORPORATION, BGP INC. (CHINA NATIONAL PETROLEUM CORPORATION), ION GEOPHYSICAL CORPORATION, KINEMETRICS INC., NANOMETRICS INC., GEOMETRICS INC., OYO CORPORATION, GÜRALP SYSTEMS LTD, GEOSENSE LTD, WIRELESS SEISMIC INC., TERREX SEISMIC, PARAGON GEOPHYSICAL SERVICES, DAWSON GEOPHYSICAL COMPANY, FUGRO N.V., TRIMBLE INC., Others

Which segments covered the Seismic Data Acquisition Equipment Market?

By Equipment Type (Land Seismic Recording Systems, Marine Seismic Acquisition Systems, Seismic Sensors (Geophones, Hydrophones, Accelerometers, MEMS), Auxiliary Equipment (Cables, Connectors, Power Systems, Vibroseis Units)), By Technology (3D Seismic Survey, 4D Seismic Survey (Time-Lapse), 2D Seismic Survey, Vertical Seismic Profiling (VSP) and Transition Zone), By Application (Oil and Gas Exploration, Mining Exploration, Civil Engineering and Infrastructure, Environmental Monitoring and Academic Research), By Deployment (Land, Marine, Airborne and Transition Zone)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Seismic Data Acquisition Equipment Market

Published Date : 18 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date