- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Semi-Trailer Dealership Market Size, Share & CAGR 9.7% Forecast 2034

Global Semi-Trailer Dealership Market Size, Share, Analysis By Product Type (New Semi-Trailers, Used Semi-Trailers), By Application (Freight Transportation, Logistics Services, Construction and Heavy Haul, Specialized Transport), By End-Use (Fleet Operators, Owner-Operators, Leasing Companies) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Fleet Modernization Trends, Logistics Infrastructure Investments & Forecast 2026–2034

Report Overview

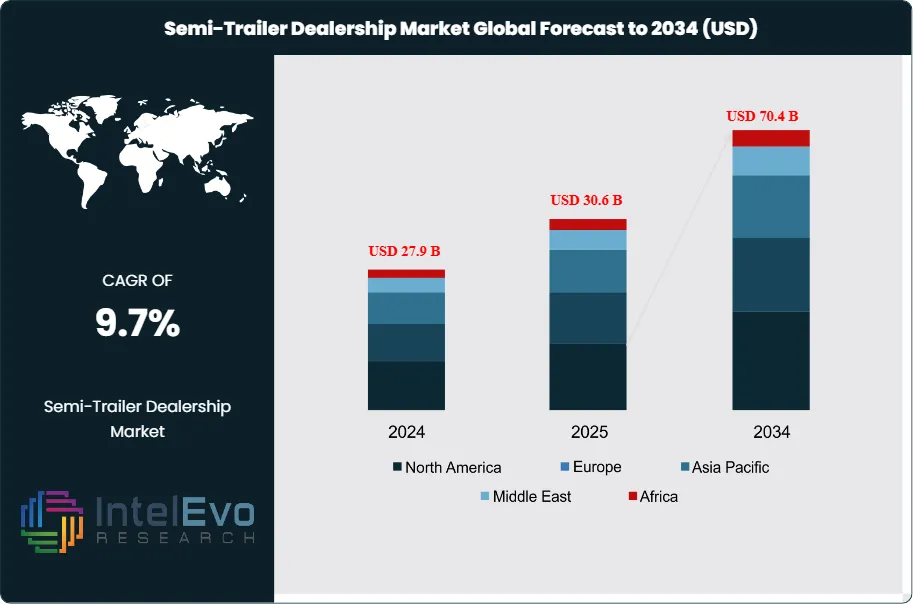

The Semi-Trailer Dealership Market was valued at USD 27.9 billion in 2024 and is projected to reach approximately USD 30.6 billion in 2025. The market is further expected to expand to nearly USD 70.4 billion by 2034, registering a compound annual growth rate (CAGR) of about 9.7% during the forecast period from 2026 to 2034. Growth in the market is driven by the rising demand for freight transportation, expanding e-commerce logistics networks, and increasing cross-border trade activities. Semi-trailer dealerships play a critical role in providing fleets with access to new and used trailers, financing solutions, and aftermarket services.

Get More Information about this report -

Request Free Sample ReportAdditionally, the ongoing modernization of commercial vehicle fleets, adoption of advanced trailer technologies, and growing investments in logistics infrastructure are expected to further support the expansion of semi-trailer dealership networks worldwide.

Dealerships serve as the interface between trailer OEMs and freight operators. They earn from new and used unit sales, leasing and financing facilitation, parts distribution, and workshop labor. The channel is consolidating as multi-location groups standardize inventory and expand service coverage, while independents compete on proximity and faster cycle times. Service and parts contribute an estimated 35%–45% of dealer gross profit, raising emphasis on contract maintenance and parts availability.

Demand growth follows freight volumes and replacement cycles. E-commerce supports dry-van and regional distribution demand, while cold-chain expansion sustains utilization of temperature-controlled equipment. Fleet buyers prioritize payload efficiency, aerodynamic performance, and uptime, and they require advisory support on specifications and total cost of ownership. Dealerships that bundle maintenance, mobile service, and telematics onboarding tend to secure higher share of wallet and steadier revenue.

Supply conditions remain a constraint. OEM allocation discipline, lead times for axles, tires, and refrigeration components, and parts availability influence delivery schedules and used-trailer turnover. Financing also shapes mix. When rates rise, fleets shift toward leasing and deferred replacement, which increases the value of remarketing expertise and residual-value governance.

Regulation shapes inventory and service strategy. Emissions and fuel-efficiency mandates, safety compliance, and evolving weight rules increase demand for lightweight materials, aerodynamic kits, electronic braking diagnostics, and condition monitoring. Dealers also manage technician shortages, warranty complexity, and cybersecurity exposure as connected service tools link to fleet systems.

Technology is moving the model from transactional selling to fleet enablement. AI supports demand forecasting, dynamic pricing for used inventory, and predictive maintenance scheduling from workshop and telematics data. Automation improves parts picking and bay utilization. E-trailer pilots reinforce the efficiency thesis: BMW Group testing reported up to 250 kilometres per day and an average diesel reduction of 46.59% with loads exceeding 16 tonnes, plus CO2 reduction near 120 tonnes annually per unit.

Regionally, North America remains the largest profit pool at roughly 30%–35% share, while Asia-Pacific posts the fastest expansion as India and Southeast Asia scale logistics-park and corridor investment. Mexico nearshoring lanes and Gulf intermodal corridors are emerging growth hotspots.

, By Application (Freight Transportation, Logistics Services, Construction and Heavy Haul, Specialized Transport), By End-Use (Fleet Operators, Owner-Operators, Leasing Companies) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Fleet Modernization Trends, Logistics Infrastructure Investments & Forecast 2026–2034")

Key Takeaways

- Market Growth: The market expands from 27.9 billion USD, 2024 to 70.4 billion USD, 2034 across 2026-2034. It delivers a 9.7% CAGR, 2026-2034.

- Segment Dominance: New Semi-Trailers lead by product type at 67.2%, 2024. Dealer revenue concentrates in new-unit programs worth 18.8 billion USD, 2024.

- Segment Dominance: Freight Transportation leads by application at 49.4%, 2024. Freight-linked dealership turnover reaches 13.8 billion USD, 2024.

- Driver: Fleet operators accelerate modernization to meet compliance and uptime targets, sustaining 56.8%, 2024 demand share. Replacement-led purchasing cycles support estimated: 2.0% annual unit refresh, 2024.

- Restraint: Higher financing costs and rate volatility suppress discretionary upgrades, creating estimated: 9.0% deal deferrals, 2024. Supply lead-times constrain availability and reduce inventory turns to estimate: 3.0 turns per year, 2024.

- Opportunity: Electrified e-trailer deployments open attach revenue in charging coordination and technical service, estimated: 0.6 billion USD, 2030. Efficiency gains of 46.6%, 2024 strengthen the value case for advanced trailers.

- Trend: Dealerships embed AI and digital tools to raise conversion and optimize service scheduling, estimated: 35.0% dealer adoption, 2024. Digital aftermarket and telematics pull-through lift service revenue to estimate: 40.0% of gross profit, 2024.

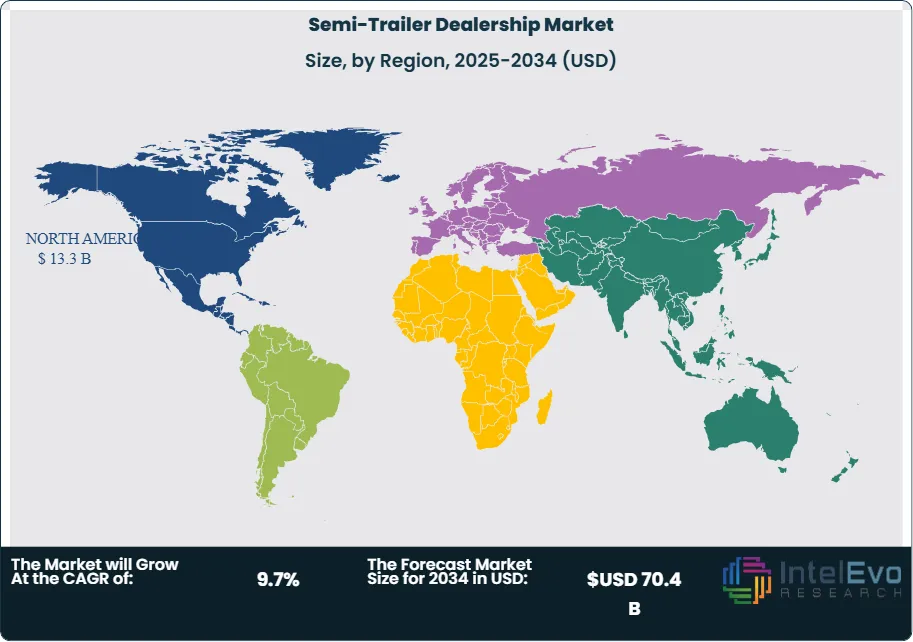

- Regional Analysis: North America leads with 47.9%, 2024 share and 13.3 billion USD, 2024 value. Growth shifts to cross-border and intermodal corridors, estimated: 2.5 billion USD, 2034.

By Type

New semi-trailers account for the majority of dealership revenue as fleets prioritize regulatory compliance and operating efficiency. In 2025, new units continue to represent about 67% of total volume, supported by replacement demand across long-haul and regional freight fleets. Buyers favor factory-built trailers equipped with advanced braking systems, aerodynamic features, and telematics-ready architecture to meet tightening safety and emissions requirements in North America and Europe.

Fleet renewal cycles remain a core demand driver. Large operators typically replace trailers every seven to ten years, which sustains baseline dealership volumes even during softer freight cycles. Warranty coverage and predictable lifecycle costs further support preference for new equipment, particularly among fleets managing several thousand assets.

Used semi-trailers serve budget-conscious operators and short-term capacity needs. Demand concentrates on younger assets with documented service history. While compliance concerns limit broader uptake, used units deliver faster inventory turnover and flexible pricing. Small carriers and owner-operators rely on this segment to manage capital constraints, keeping used trailers relevant in dealership portfolios.

By Application

Freight transportation remains the largest application segment, contributing close to 49% of dealership demand in 2025. Long-haul and cross-border trade flows support consistent purchases of dry vans, flatbeds, and refrigerated trailers. Retail distribution, manufacturing output, and agricultural exports anchor baseline volumes across developed markets.

Logistics services continue to expand as third-party providers invest in regional hubs and spoke networks. Rising e-commerce penetration supports demand for standardized trailer configurations designed for high utilization and rapid loading cycles. This segment favors volume orders and service contracts, strengthening dealership recurring revenue.

Construction and heavy haul applications provide steady but cyclical demand tied to infrastructure spending. Specialized transport remains smaller in volume but delivers higher margins through customization for temperature-controlled, hazardous, and oversized cargo.

By End-Use

Fleet operators represent the largest end-use group, accounting for nearly 57% of dealership sales in 2025. Bulk procurement, structured replacement planning, and centralized maintenance strategies reinforce long-term dealership relationships. Financing packages and service agreements remain key differentiators.

Owner-operators form a stable secondary segment. Purchasing decisions emphasize affordability and flexibility. Trade-in programs and deferred payment structures influence dealer selection.

Leasing companies maintain a growing presence as fleets shift toward asset-light models. Their focus on residual value and durability increases demand for standardized trailer specifications.

By Region

North America leads the market with about 48% share, valued near USD 13 billion, driven by dense highway networks and high freight intensity. Europe shows stable demand supported by cross-border trade and regulatory alignment. Asia Pacific posts the fastest growth, led by China and India, as highway investment and organized logistics expand. Latin America and the Middle East and Africa show moderate growth tied to trade corridors, mining, energy logistics, and gradual infrastructure upgrades.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- New Semi-Trailers

- Used Semi-Trailers

By Application

- Freight Transportation

- Logistics Services

- Construction and Heavy Haul

- Specialized Transport

By End-Use

- Fleet Operators

- Owner-Operators

- Leasing Companies

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 30.6 B |

| Forecast Revenue (2034) | USD 70.4 B |

| CAGR (2025-2034) | 9.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (New Semi-Trailers, Used Semi-Trailers), By Application (Freight Transportation, Logistics Services, Construction and Heavy Haul, Specialized Transport), By End-Use (Fleet Operators, Owner-Operators, Leasing Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Velocity Vehicle Group, Ryder System, Inc., Premier Truck Group, Penske Truck Leasing, Arrow Truck Sales, MHC Kenworth, TransWest Truck Trailer RV, Rush Enterprises, Inc., Idealease, Inc., TEC Equipment, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Freight Transportation, Logistics Services, Construction and Heavy Haul, Specialized Transport), By End-Use (Fleet Operators, Owner-Operators, Leasing Companies) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Fleet Modernization Trends, Logistics Infrastructure Investments & Forecast 2026–2034")

, By Application (Freight Transportation, Logistics Services, Construction and Heavy Haul, Specialized Transport), By End-Use (Fleet Operators, Owner-Operators, Leasing Companies) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Fleet Modernization Trends, Logistics Infrastructure Investments & Forecast 2026–2034")

, By Application (Freight Transportation, Logistics Services, Construction and Heavy Haul, Specialized Transport), By End-Use (Fleet Operators, Owner-Operators, Leasing Companies) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Fleet Modernization Trends, Logistics Infrastructure Investments & Forecast 2026–2034")

Frequently Asked Questions

How big is the Semi-Trailer Dealership Market?

Global Semi-Trailer Dealership Market was valued at USD 27.9 billion in 2024 and is projected to reach USD 70.4 billion by 2034, growing at a CAGR of 9.7%. Explore market trends, logistics demand, and growth opportunities.

Who are the major players in the Semi-Trailer Dealership Market?

Velocity Vehicle Group, Ryder System, Inc., Premier Truck Group, Penske Truck Leasing, Arrow Truck Sales, MHC Kenworth, TransWest Truck Trailer RV, Rush Enterprises, Inc., Idealease, Inc., TEC Equipment, Inc.

Which segments covered the Semi-Trailer Dealership Market?

By Product Type (New Semi-Trailers, Used Semi-Trailers), By Application (Freight Transportation, Logistics Services, Construction and Heavy Haul, Specialized Transport), By End-Use (Fleet Operators, Owner-Operators, Leasing Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Semi-Trailer Dealership Market

Published Date : 10 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date