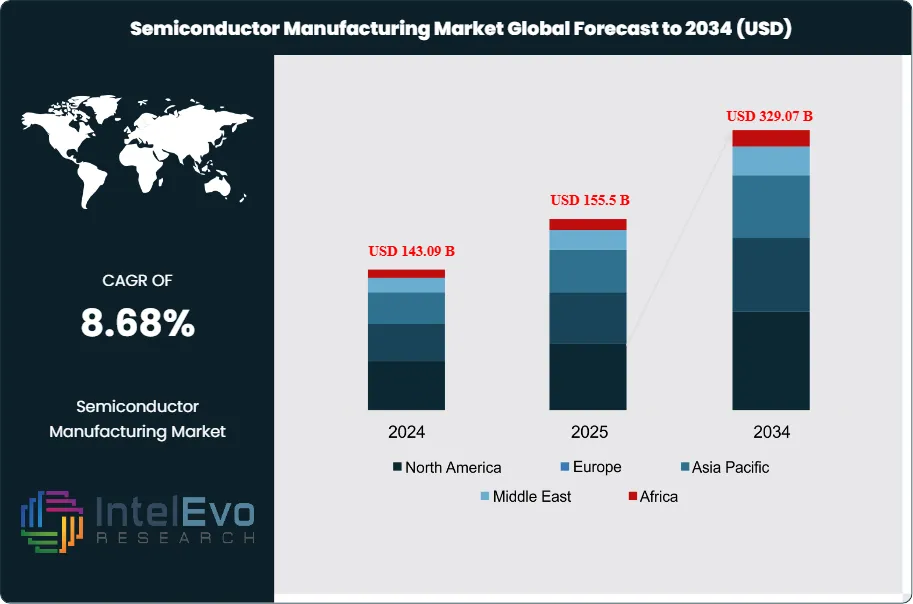

The Semiconductor Manufacturing Market size is expected to be worth around USD 329.07 Billion by 2034, from USD 143.09 Billion in 2024, growing at a CAGR of 8.68% during the forecast period from 2024 to 2034. The Semiconductor Manufacturing Market encompasses the global ecosystem of companies and technologies involved in designing, fabricating, assembling, and testing semiconductor devices and integrated circuits. This market includes foundry services, integrated device manufacturers (IDMs), fabless companies, and outsourced assembly and test (OSAT) providers. The scope extends across various product categories including logic processors, memory devices, analog circuits, discrete components, and specialized semiconductors serving diverse end markets from consumer electronics to automotive, industrial, and communications infrastructure.

The market is experiencing unprecedented growth driven by artificial intelligence adoption, 5G network expansion, automotive electrification, and the continued digitization of global industries. Advanced computing requirements, including high-performance computing (HPC), data centers, and edge computing applications, are creating substantial demand for cutting-edge semiconductor technologies. The transition to smaller process nodes, three-dimensional chip architectures, and specialized processors for AI workloads represents a fundamental shift in manufacturing complexity and value creation within the semiconductor ecosystem.

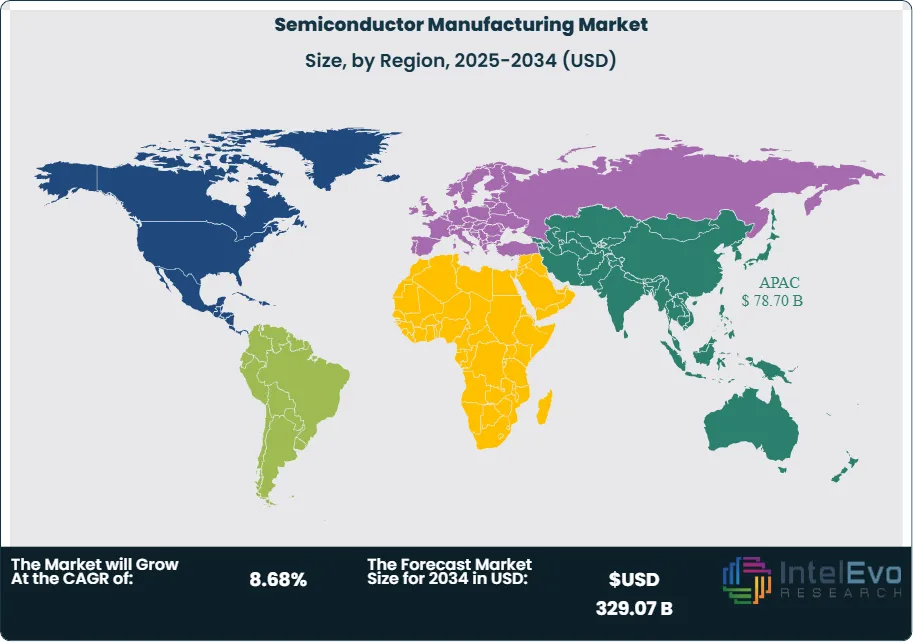

Asia-Pacific dominates the global semiconductor manufacturing landscape, with Taiwan leading through TSMC's foundry leadership, followed by significant manufacturing capacity in South Korea, China, and Japan. Taiwan alone accounts for the majority of advanced semiconductor manufacturing capacity, while China represents the fastest-growing market through substantial government investments and domestic demand growth. North America maintains leadership in semiconductor design and emerging manufacturing initiatives, while Europe focuses on specialized applications and strategic technology sovereignty.

The pandemic initially disrupted semiconductor supply chains and manufacturing operations, leading to global chip shortages that highlighted the critical importance of semiconductor supply chain resilience. However, accelerated digitization, remote work adoption, and increased electronics consumption drove unprecedented demand for semiconductors across all categories. The crisis prompted governments worldwide to recognize semiconductors as strategic assets, leading to massive investment programs and initiatives to build domestic manufacturing capabilities and reduce supply chain dependencies.

Escalating trade tensions, technology export controls, and geopolitical competition have fundamentally reshaped the semiconductor manufacturing landscape. Technology restrictions on advanced semiconductor equipment and materials have accelerated regional diversification of manufacturing capabilities and supply chains. These dynamics have created opportunities for domestic manufacturers while challenging established global supply chain models, driving increased investment in regional manufacturing capacity and technology development across multiple geographic regions.

Key Takeaways

Market Growth: The Semiconductor Manufacturing Market is expected to reach USD 329.07 Billion by 2034, fueled by advances in artificial intelligence, 5G networks, electric vehicles, and digital transformation across industries.

Technology Node: The 3nm technology node represents the cutting-edge of chip fabrication, enabling greater performance and energy efficiency for advanced applications.

End-User: Consumer electronics dominate semiconductor demand, pushing advancements in miniaturization, efficiency, and integration across devices.

Drivers: Key drivers accelerating growth include artificial intelligence adoption and 5G infrastructure deployment, which boost market expansion through increased processing requirements and network equipment demand.

Restraints: Growth is hindered by high capital requirements and geopolitical trade restrictions, which create challenges such as massive facility investment needs and technology access limitations.

Opportunities: The market is poised for expansion due to opportunities like automotive electrification and edge computing growth, which enable new semiconductor applications and processing architectures.

Trends: Emerging trends including advanced packaging technologies and chiplet architectures are reshaping the market by enabling system integration and performance optimization.

Regional Leader: Asia-Pacific leads owing to manufacturing capacity concentration and foundry leadership. North America and Europe show high promise due to government investment programs and strategic manufacturing initiatives.

Technology Node Analysis:

3nm semiconductors are considered the forefront of process technology, offering substantial improvements in transistor density, speed, and power consumption over previous generations. This node is mainly driven by high-end markets such as flagship smartphones, AI accelerators, and data center processors, where performance and energy efficiency are paramount. Foundries investing in 3nm capabilities often lead the market, attracting premium clients eager for the latest technology. The complexity of manufacturing at this scale presents challenges in yield and equipment cost, but leaders in this segment establish a technological and competitive advantage.

End-User Analysis:

Consumer Electronics Leads With over 50% Market Share In Semiconductor Manufacturing Market: Driven by the proliferation of smartphones, tablets, smart TVs, and wearable technology, the consumer electronics sector consistently demands leading-edge semiconductor manufacturing. As consumer preferences evolve rapidly, this segment sets the pace for innovation, compelling manufacturers to move to new nodes for better functionality, longer battery life, and improved form factors. The sector’s scale encourages volume production, helping to amortize R&D costs and accelerate the adoption of advanced manufacturing processes industry-wide. As a result, consumer electronics act as the primary test bed for new semiconductor technologies.

Regional Analysis

Asia-Pacific Leads With more than 55% Market Share In Semiconductor Manufacturing Market: Asia-Pacific commands the global semiconductor manufacturing market through its comprehensive ecosystem encompassing advanced foundry capabilities, established supply chains, and substantial government support for technology development. Taiwan leads the region and global market through TSMC's foundry dominance, which captures over sixty percent of global foundry revenue and maintains technological leadership in advanced node manufacturing. South Korea contributes significant capacity through Samsung's foundry operations and memory manufacturing leadership, while also hosting SK Hynix's memory production capabilities. China represents the fastest-growing regional market through substantial government investments in domestic semiconductor capabilities, growing design expertise, and massive domestic demand for semiconductor products across consumer electronics, automotive, and industrial applications.

North America demonstrates strong growth potential driven by major government investment programs, including the CHIPS and Science Act, which aims to rebuild domestic semiconductor manufacturing capabilities and reduce supply chain dependencies. The region maintains leadership in semiconductor design through major companies like Intel, AMD, Nvidia, and Qualcomm, while also hosting significant manufacturing capacity expansion projects from global foundry leaders. Advanced research and development capabilities, combined with substantial venture capital investment in semiconductor startups, position North America as a key innovation center for next-generation semiconductor technologies.

Europe focuses on strategic technology development and specialized semiconductor applications, particularly in automotive, industrial, and power electronics markets. The European Union's semiconductor strategy emphasizes technology sovereignty, advanced research capabilities, and specialized manufacturing for critical applications. The region's strength lies in automotive semiconductor expertise, advanced materials research, and sophisticated equipment manufacturing that supports global semiconductor production. Government initiatives and industrial partnerships are driving increased investment in domestic manufacturing capabilities and advanced packaging technologies.

Technology Node (3nm, 4-10nm, 14-28nm, 28-130nm); Industry Vertical (Consumer Electronics, Automotive, IT & Telecom, Computing, Industrial, Others)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

Samsung, Semiconductor Manufacturing International Corporation, ASML Holding N.V., GlobalFoundries Inc., Vanguard International Semiconductor Corporation, United Microelectronics Corporation, Intel Corporation, Taiwan Semiconductor Manufacturing Co., Ltd., PSMC Co., Ltd., Hua Hong Semiconductor Limited, Applied Materials Inc., Nexchip Semiconductor Corp., Tower Semiconductor Ltd.

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

FIGURE 19 NORTH AMERICA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 20 NORTH AMERICA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 21 U.S. SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 22 U.S. SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 23 CANADA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 24 CANADA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 25 MEXICO SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 26 MEXICO SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 27 MARKET SHARE BY COUNTRY

FIGURE 28 APAC SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 29 APAC SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 30 CHINA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 31 CHINA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 32 JAPAN SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 33 JAPAN SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 34 KOREA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 35 KOREA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 36 INDIA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 37 INDIA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 38 SOUTHEAST ASIA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 39 SOUTHEAST ASIA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 40 MARKET SHARE BY COUNTRY

FIGURE 41 MIDDLE EAST AND AFRICA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 42 MIDDLE EAST AND AFRICA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 43 SAUDI ARABIA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 44 SAUDI ARABIA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 45 UAE SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 46 UAE SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 47 EGYPT SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 48 EGYPT SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 49 NIGERIA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 50 NIGERIA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 51 SOUTH AFRICA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 52 SOUTH AFRICA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 53 MARKET SHARE BY COUNTRY

FIGURE 54 EUROPE SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 55 EUROPE SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 56 GERMANY SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 57 GERMANY SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 58 FRANCE SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 59 FRANCE SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 60 UK SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 61 UK SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 62 SPAIN SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 63 SPAIN SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 64 ITALY SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 65 ITALY SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 66 MARKET SHARE BY COUNTRY

FIGURE 67 SOUTH AMERICA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 68 SOUTH AMERICA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 69 BRAZIL SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 70 BRAZIL SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 71 ARGENTINA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 72 ARGENTINA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 73 COLUMBIA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE TECHNOLOGY NODE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 74 COLUMBIA SEMICONDUCTOR MANUFACTURING CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 75 FINANCIAL OVERVIEW:

Key Players Analysis

Taiwan Semiconductor Manufacturing Company (TSMC): TSMC maintains its position as the undisputed global foundry leader, commanding over sixty percent of the worldwide foundry market through technological excellence, manufacturing scale, and comprehensive customer service capabilities. The company's competitive edge stems from continuous investment in leading-edge process technologies, advanced packaging capabilities, and strong customer relationships built through decades of reliable manufacturing service delivery. TSMC's strategic advantages include first-to-market introduction of new process nodes, comprehensive intellectual property portfolio, and extensive global manufacturing footprint that serves diverse customer requirements. The company's expansion strategy focuses on advanced technology development including 2nm process technology, advanced packaging solutions, and specialty technologies for automotive and high-performance computing applications while expanding manufacturing capacity in Taiwan and internationally.

Samsung Electronics Co., Ltd.: Samsung leverages its position as a diversified technology conglomerate to compete in both foundry services and memory manufacturing markets, utilizing vertical integration advantages and substantial research and development capabilities. The company's competitive differentiators include advanced memory technologies, comprehensive semiconductor product portfolio, and strong relationships with major technology companies across multiple market segments. Samsung's strategic initiatives emphasize expanding foundry customer base, developing advanced process technologies competitive with TSMC, and creating integrated solutions that combine memory, logic, and system technologies. The company's expansion plans include significant capital investment in manufacturing capacity, advanced packaging capabilities, and strategic partnerships with major customers seeking alternative foundry sources.

Intel Corporation: Intel combines its traditional strength in processor design with ambitious plans to become a major foundry service provider, leveraging decades of manufacturing expertise and substantial financial resources to compete in global semiconductor markets. The company's competitive strengths include advanced process technology development, comprehensive manufacturing capabilities, and strong relationships with enterprise and data center customers. Intel's strategic direction emphasizes foundry service expansion through Intel Foundry Services, advanced packaging technology development, and strategic partnerships that leverage government investment programs for domestic manufacturing capacity expansion. The company's transformation includes substantial investment in new manufacturing facilities, advanced technology development, and customer acquisition programs designed to compete with established foundry leaders.

Applied Materials Inc.: Applied Materials maintains leadership in semiconductor manufacturing equipment through comprehensive product portfolios, technological innovation, and strong customer relationships across the global semiconductor ecosystem. The company's market advantages include critical process equipment for advanced node manufacturing, materials engineering expertise, and comprehensive service capabilities that support customer manufacturing operations. Applied Materials' strategic focus involves developing next-generation manufacturing equipment for advanced process nodes, expanding into new application areas including advanced packaging and display technologies, and strengthening partnerships with leading semiconductor manufacturers worldwide. The company benefits from increasing semiconductor manufacturing capacity investments and the transition to more sophisticated manufacturing processes that require advanced equipment solutions.

ASML Holding N.V.: ASML holds a unique position as the sole supplier of extreme ultraviolet lithography systems essential for advanced semiconductor manufacturing, creating substantial competitive advantages and customer dependency relationships. The company's competitive edge stems from decades of optical technology development, comprehensive intellectual property protection, and strong partnerships with leading semiconductor manufacturers and research institutions. ASML's strategic advantages include technological monopoly in critical manufacturing equipment, strong customer relationships built through collaborative technology development, and substantial barriers to entry that protect market position. The company's expansion strategy focuses on increasing extreme ultraviolet system production capacity, developing next-generation lithography technologies, and expanding service capabilities that support customer manufacturing operations and technology transitions.

Market Key Players

Samsung

Semiconductor Manufacturing International Corporation

ASML Holding N.V.

GlobalFoundries Inc.

Vanguard International Semiconductor Corporation

United Microelectronics Corporation

Intel Corporation

Taiwan Semiconductor Manufacturing Co., Ltd.

PSMC Co., Ltd.

Hua Hong Semiconductor Limited

Applied Materials Inc.

Nexchip Semiconductor Corp.

Tower Semiconductor Ltd.

Drivers:

Artificial Intelligence and Machine Learning Revolution:

The explosive growth of artificial intelligence applications across industries is driving unprecedented demand for specialized semiconductor devices including AI accelerators, graphics processing units, and high-bandwidth memory systems. Machine learning workloads require massive computational power, parallel processing capabilities, and high-speed memory access that push the boundaries of semiconductor performance and efficiency. This driver manifests through increasing investments in data center infrastructure, edge computing devices, and AI-enabled consumer electronics that require cutting-edge semiconductor technologies. The AI revolution spans multiple market segments including autonomous vehicles, natural language processing, computer vision, and predictive analytics, each creating specific semiconductor requirements and driving innovation in processor architectures. The timeline for AI-driven growth extends throughout the forecast period as organizations across industries integrate artificial intelligence capabilities into their operations and products. Strategic outcomes include development of specialized AI processors, advanced packaging technologies for system integration, and new memory architectures optimized for machine learning workloads.

5G Network Infrastructure and Connectivity Expansion:

The global deployment of 5G networks and the evolution toward advanced wireless connectivity standards are creating substantial demand for sophisticated semiconductor devices including radio frequency components, baseband processors, and network infrastructure chips. 5G technology requires significantly more complex signal processing, higher frequency operations, and enhanced power efficiency compared to previous wireless generations, driving innovation in semiconductor design and manufacturing technologies. This driver encompasses both network equipment requirements for cellular base stations and infrastructure, as well as consumer device needs for 5G-enabled smartphones, tablets, and connected devices. The influence extends beyond traditional communications applications to enable Internet of Things deployment, industrial automation, and real-time applications that require low-latency, high-bandwidth connectivity. Implementation timelines span multiple years as network operators upgrade infrastructure and consumers adopt 5G-enabled devices. Strategic outcomes include development of advanced RF semiconductor technologies, integration of multiple wireless standards in single devices, and creation of specialized processors for network edge computing applications.

Restraints:

Massive Capital Investment Requirements and Technology Complexity:

The semiconductor manufacturing industry requires unprecedented capital investments for advanced manufacturing facilities, with leading-edge fabs costing tens of billions of dollars and requiring continuous technology upgrades to maintain competitiveness. These enormous financial requirements create significant barriers to entry and limit the number of companies capable of competing in advanced technology nodes. The complexity extends beyond initial capital investment to include ongoing research and development expenses, equipment maintenance costs, and continuous workforce training requirements needed to operate sophisticated manufacturing processes. Technology complexity increases exponentially with each new process node generation, requiring specialized expertise in areas including extreme ultraviolet lithography, advanced materials science, and precision process control that few organizations can master. The financial impact affects not only manufacturing companies but also their suppliers, customers, and entire regional economies that depend on semiconductor industry success. Mitigation strategies include government investment programs, international partnerships for technology development, and innovative financing models that spread capital requirements across multiple stakeholders and timeframes.

Geopolitical Tensions and Trade Policy Uncertainty:

Escalating trade tensions, technology export controls, and geopolitical competition create significant uncertainty and operational challenges for semiconductor manufacturers operating in global markets. Technology restrictions limit access to critical manufacturing equipment, materials, and intellectual property that are essential for advanced semiconductor production, forcing companies to develop alternative supply chains and technologies. These restrictions disproportionately impact companies seeking to access the most advanced manufacturing technologies and materials, creating competitive disadvantages and limiting market opportunities. Historical patterns show that trade policy changes can rapidly reshape market dynamics, supply chain relationships, and technology transfer agreements, creating planning challenges for long-term investment decisions. Cross-regional impacts vary significantly based on political relationships, trade agreements, and technology dependencies, with some regions benefiting from restricted competition while others face limited access to critical technologies. The uncertainty affects strategic planning, investment decisions, and partnership development throughout the semiconductor ecosystem, requiring companies to develop more resilient and geographically diversified operations while potentially sacrificing efficiency and cost optimization.

Opportunities:

Automotive Electrification and Autonomous Vehicle Technologies:

The transformation of the automotive industry toward electric vehicles, advanced driver assistance systems, and autonomous driving capabilities creates enormous opportunities for semiconductor manufacturers to develop specialized products for automotive applications. Electric vehicles require sophisticated power management semiconductors, battery management systems, and motor control electronics that differ significantly from traditional automotive semiconductor requirements. Autonomous vehicle technologies demand high-performance processors for sensor fusion, real-time decision making, and machine learning inference that push the boundaries of automotive semiconductor performance and reliability. This opportunity encompasses developing automotive-qualified semiconductors that meet stringent reliability, temperature, and safety requirements while providing the computational power needed for advanced automotive applications. Market sectors affected include traditional automotive manufacturers, electric vehicle startups, autonomous vehicle developers, and automotive tier-one suppliers who require specialized semiconductor solutions. Growth potential extends to vehicle-to-everything communication systems, over-the-air update capabilities, and integrated automotive computing platforms that consolidate multiple vehicle functions into centralized processing systems.

Edge Computing and Internet of Things Expansion:

The proliferation of edge computing applications and Internet of Things deployments creates significant opportunities for specialized semiconductor devices that can process data locally, reduce latency, and operate efficiently in distributed computing environments. Edge computing requires processors that can perform artificial intelligence inference, real-time analytics, and decision making at the network edge while operating within power, thermal, and cost constraints that differ from traditional data center applications. Internet of Things applications span diverse markets including industrial automation, smart cities, healthcare monitoring, and agricultural technology, each requiring specialized semiconductor solutions optimized for specific application requirements. Success enablers include development of ultra-low-power processors, integrated wireless connectivity solutions, and security-focused semiconductor architectures that protect distributed computing systems from cyber threats. The opportunity extends to creating new semiconductor business models including software-defined hardware, edge computing platforms, and integrated sensor-to-cloud solutions that combine multiple semiconductor technologies into comprehensive system solutions for emerging applications.

Trends:

Advanced Packaging and Chiplet Architecture Integration:

The semiconductor industry is experiencing a fundamental transformation toward advanced packaging technologies and chiplet architectures that enable system-level integration and performance optimization beyond traditional scaling limitations. Advanced packaging techniques including 2.5D and 3D integration allow multiple semiconductor dies to be combined into single packages, enabling heterogeneous integration of different technologies and process nodes within unified systems. Chiplet architectures decompose traditional monolithic processors into smaller, specialized functional blocks that can be manufactured using optimal process technologies and combined through high-speed interconnect technologies. This trend addresses the increasing cost and complexity of large monolithic chips while enabling system architects to optimize each functional block independently. The transformation includes development of standardized chiplet interfaces, advanced thermal management solutions, and sophisticated electronic design automation tools that support chiplet-based system design. Implementation requires collaboration across the semiconductor ecosystem including foundries, packaging companies, electronic design automation providers, and system companies that integrate these technologies into their products.

Sustainable Manufacturing and Circular Economy Principles:

Growing environmental consciousness and regulatory pressure are driving the semiconductor industry toward more sustainable manufacturing practices, energy-efficient operations, and circular economy principles that minimize waste and environmental impact. Semiconductor manufacturing traditionally consumes substantial energy and water resources while generating chemical waste that requires careful management and disposal. This trend encompasses development of more energy-efficient manufacturing processes, renewable energy adoption for semiconductor facilities, and closed-loop water recycling systems that minimize environmental impact. Behavioral shifts include increasing customer demand for environmentally responsible semiconductor products, investor pressure for sustainable business practices, and regulatory requirements for environmental reporting and waste reduction. The transformation includes development of semiconductor recycling technologies, design for disassembly principles that facilitate component recovery, and life-cycle assessment methodologies that evaluate environmental impact throughout product lifecycles. Success requires collaboration between semiconductor manufacturers, equipment suppliers, chemical companies, and waste management specialists to develop comprehensive sustainable manufacturing ecosystems.

Recent Development

In March 2025: Pragmatic Semiconductor Ltd. has unveiled the FlexIC Platform Gen 3, setting a new benchmark in flexible semiconductor technology. This next-generation platform delivers a remarkable 10x improvement in digital power efficiency and a 3x reduction in digital area usage compared to its predecessor. The upgrade enables significant advancements in the design and manufacture of ultra-thin, physically flexible application-specific integrated circuits (ASICs), broadening the possibilities for new products in consumer, industrial, healthcare, and IoT markets.

In January 2025: Infineon Technologies has officially commenced the construction of its new semiconductor backend production facility in Samut Prakan, just south of Bangkok, Thailand. This strategic investment aims to broaden and strengthen the company’s global manufacturing operations by optimizing cost efficiency, bolstering supply chain resilience, and supporting the expansion of its frontend capacities. The new factory will focus on highly automated backend processes—crucial for power modules in applications ranging from industrial automation to renewables and electric vehicles—and is expected to be operational by early 2026, with potential for further expansion based on market needs.

Frequently Asked Questions

How big is the Semiconductor Manufacturing Market?

Global Semiconductor Manufacturing Market to grow from USD 143.09B in 2024 to USD 329.07B by 2034 at 8.68% CAGR, fueled by AI, IoT, and 5G demand.

Who are the major players in the Semiconductor Manufacturing Market?

Samsung, Semiconductor Manufacturing International Corporation, ASML Holding N.V., GlobalFoundries Inc., Vanguard International Semiconductor Corporation, United Microelectronics Corporation, Intel Corporation, Taiwan Semiconductor Manufacturing Co., Ltd., PSMC Co., Ltd., Hua Hong Semiconductor Limited, Applied Materials Inc., Nexchip Semiconductor Corp., Tower Semiconductor Ltd.

Which segments covered the Semiconductor Manufacturing Market?

Technology Node (3nm, 4-10nm, 14-28nm, 28-130nm); Industry Vertical (Consumer Electronics, Automotive, IT & Telecom, Computing, Industrial, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

Industry Vertical (Consumer Electronics, Automotive, IT & Telecom, Computing, Industrial, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Industry Vertical (Consumer Electronics, Automotive, IT & Telecom, Computing, Industrial, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Industry Vertical (Consumer Electronics, Automotive, IT & Telecom, Computing, Industrial, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Industry Vertical (Consumer Electronics, Automotive, IT & Telecom, Computing, Industrial, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")