- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Semiconductor Photoresist Stripping Market Growth Outlook, 2025 to 2034

Global Semiconductor Photoresist Stripping Market Size, Share, Forecast& Analysis Report by Product Type (Positive Photoresist Stripper, Negative Photoresist Stripper), (Application, Integrated Circuit Manufacturing, Wafer Level Packaging), Technology (Wet Stripping, Dry Stripping), End User (Foundries, IDMs (Integrated Device Manufacturers), Other Facilities ) Industry Region & Key Players – Segment Overview, Dynamics, Strategies, Trends & Forecast 2025–2034

Report Overview

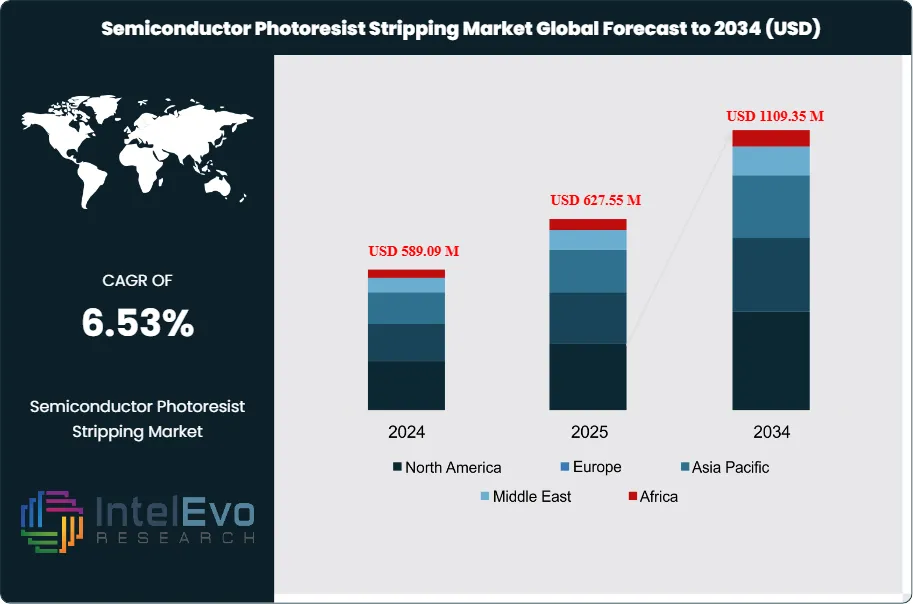

The Semiconductor Photoresist Stripping Market size is expected to be worth around USD 1109.35 Million by 2034, from USD 589.09 Million in 2024, growing at a CAGR of 6.53% during the forecast period from 2024 to 2034. The semiconductor photoresist stripping market is a critical component of the semiconductor manufacturing process. Photoresist stripping involves removing photoresist layers applied during lithography to create intricate patterns on silicon wafers.

Get More Information about this report -

Request Free Sample ReportThis step is vital to ensure clean, defect-free surfaces for subsequent fabrication stages and is integral to producing high-quality integrated circuits (ICs). As semiconductor devices continually downscale in size and complexity, the demand for advanced photoresist stripping solutions grows, driven by the need for precision, efficiency, and environmental compliance.

Several factors influence the growth and evolution of the photoresist stripping market. One major factor is the rapid miniaturization of semiconductor devices. As chip manufacturers push for smaller feature sizes and higher transistor densities, the stripping process must become more selective and less damaging to delicate wafer surfaces. Advanced chemical formulations and plasma-based stripping techniques are increasingly favored to meet these stringent requirements. Additionally, the escalating adoption of emerging semiconductor applications, such as 5G communications, artificial intelligence (AI), and automotive electronics, further fuels market demand. Another significant market driver is the rising emphasis on eco-friendly manufacturing. Stricter environmental regulations worldwide are prompting semiconductor fabs to adopt greener, more sustainable photoresist stripping technologies which reduce hazardous waste and energy consumption without compromising stripping performance or yield.

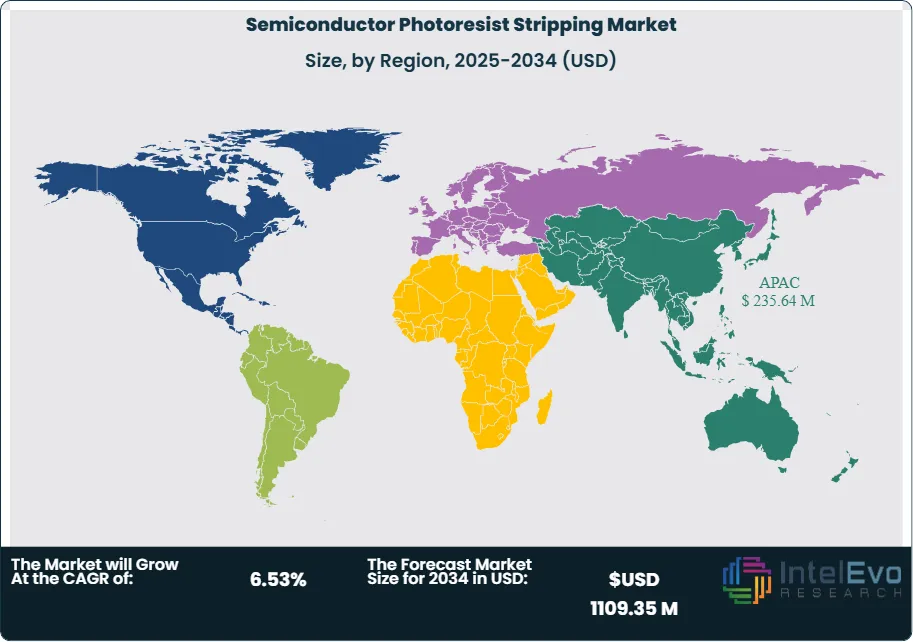

Geographically, the semiconductor photoresist stripping market is strongly influenced by regional manufacturing hubs. The Asia-Pacific region dominates, accounting for almost half of the market revenue. This leadership is due to major semiconductor production centers in China, South Korea, Taiwan, and Japan, supported by substantial capital investments in fabs and aggressive policy initiatives like China’s “Made in China 2025.” North America—especially the United States—maintains a considerable share thanks to its technological expertise, robust innovation ecosystem, and presence of leading equipment and chemical suppliers. Europe also contributes to the market, driven by a focus on environmental regulations and ongoing investments in advanced manufacturing technologies.

The COVID-19 pandemic had a notable impact on the photoresist stripping market. Early in the crisis, semiconductor supply chains experienced disruptions from factory shutdowns, logistics restrictions, and material shortages, slowing production and investment in new stripping technologies. However, the pandemic also accelerated digital transformation trends and demand for electronic devices, creating a surge in chip consumption. This led to a rapid market recovery and intensified efforts toward automation and more resilient supply chains. The push for sustainability and efficiency in fabs also gained momentum as companies adapted to the new normal.

Regional conflicts and trade tensions between major economic players—most prominently between the United States and China—have introduced complex challenges for the semiconductor photoresist stripping market. Tariffs on semiconductor materials and equipment have increased operational costs and created uncertainties in sourcing critical chemicals and tools. Export controls on cutting-edge semiconductor technologies restrict technology flow and collaboration, forcing countries to localize parts of their supply chains. These geopolitical frictions contribute to market fragmentation, impact pricing strategies, and influence investment decisions, driving some manufacturers to diversify or onshore their fabrication capabilities to mitigate risk.

Nevertheless, international trade agreements continue to play a crucial role in shaping the global market landscape. Multilateral trade pacts such as the Regional Comprehensive Economic Partnership (RCEP) in Asia enhance trade and supply chain integration among member countries. The United States-Mexico-Canada Agreement (USMCA) facilitates semiconductor equipment movement and supports North American supply chains. Additionally, ongoing negotiations for technology cooperation and regulatory harmonization between regions help reduce tariff barriers and foster the development and distribution of advanced photoresist stripping technologies. These agreements support more stable and collaborative market growth despite geopolitical uncertainties.

, (Application, Integrated Circuit Manufacturing, Wafer Level Packaging), Technology (Wet Stripping, Dry Stripping), End User (Foundries, IDMs (Integrated Device Manufacturers), Other Facilities ) Industry Region & Key Players – Segment Overview, Dynamics, Strategies, Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Semiconductor Photoresist Stripping Market is expected to reach USD 1109.35 Million by 2034, propelled by technology advances, shifts in regional manufacturing power, and evolving global trade dynamics.

- Product Type Dominance: Positive photoresist stripper leads the market due to wider applicability and superior performance in standard processes.

- Application Dominance: Integrated circuit manufacturing dominates the market, driven by continuous demand for advanced chip fabrication.

- Technology Dominance: Wet stripping holds larger market share currently, owing to established infrastructure and cost-effectiveness.

- End User Dominance: Foundries represent the fastest-growing segment, primarily due to increased fabless semiconductor design adoption.

- Drivers: Key drivers accelerating growth include increasing complexity in semiconductor designs and rising demand for miniaturization, which boost market expansion through advanced fabrication requirements.

- Restraints: Growth is hindered by high cost of advanced stripping technologies and stringent environmental regulations, which create challenges such as increased operational expenses and compliance requirements.

- Opportunities: The market is poised for expansion due to opportunities like development of eco-friendly stripping solutions and adoption of advanced packaging technologies, which enable sustainable manufacturing and enhanced device performance.

- Trends: Emerging trends including plasma-based dry stripping and automation in manufacturing are reshaping the market by improving precision and reducing environmental impact.

- Regional Analysis: Asia-Pacific leads owing to concentrated semiconductor manufacturing and government support. North America and Europe show high promise due to technological innovation and sustainability focus.

Product Type Analysis:

The positive photoresist stripper segment maintains market leadership through its superior versatility and performance characteristics. This dominance stems from the segment's ability to handle diverse photoresist formulations used in modern semiconductor manufacturing. The positive stripping process offers advantages in processing speed and pattern resolution, critical factors as device geometries continue shrinking. Environmental considerations are driving development of aqueous-based positive strippers, aligning with sustainability trends while maintaining performance standards. The segment benefits from established supply chains and manufacturing expertise, creating barriers for alternative technologies. Market maturity in this segment provides stability but also intensifies competition on cost and performance optimization.

Application-Based Analysis:

Integrated Circuit Manufacturing Leads With over 65% Market Share In Semiconductor Photoresist Stripping Market. Integrated circuit manufacturing represents the cornerstone application driving market demand, benefiting from continuous expansion in consumer electronics, automotive semiconductors, and emerging technologies. This segment's leadership reflects the central role of photoresist stripping in IC fabrication processes, where precision and yield optimization directly impact profitability. The complexity of modern IC designs necessitates advanced stripping solutions capable of handling multiple photoresist layers and intricate pattern geometries. Wafer-level packaging applications, while smaller in current market share, demonstrate strong growth potential as advanced packaging techniques gain adoption. The IC manufacturing segment drives technological innovation through demanding requirements for selectivity, uniformity, and process control.

Technology-Based Analysis:

Wet stripping technology maintains market leadership through its proven reliability and cost-effectiveness in high-volume manufacturing environments. The established infrastructure supporting wet stripping processes provides significant competitive advantages, including mature process knowledge and optimized equipment designs. However, environmental regulations and sustainability concerns are gradually shifting preference toward dry stripping methods. Plasma-based dry stripping offers superior precision and reduced chemical waste, making it attractive for advanced node manufacturing. The technology transition reflects broader industry trends toward environmentally sustainable manufacturing practices while meeting increasingly stringent performance requirements for next-generation semiconductor devices.

End-User Analysis:

The foundry segment demonstrates the strongest growth momentum, driven by the continued expansion of fabless semiconductor business models and specialized manufacturing requirements. Foundries benefit from economies of scale and process specialization, enabling optimization of photoresist stripping operations across diverse customer requirements. IDMs maintain significant market presence through integrated manufacturing strategies, though many are transitioning toward hybrid models incorporating foundry partnerships. The competitive dynamics in this segment reflect broader semiconductor industry consolidation and specialization trends, with leading foundries investing heavily in advanced process capabilities to maintain technological leadership and customer relationships.

Regional Analysis

Asia-Pacific Leads With over 40% Market Share In Semiconductor Photoresist Stripping Market. Asia-Pacific maintains its position as the dominant regional market, driven by the concentration of major semiconductor manufacturing facilities in Taiwan, South Korea, and China. The region's leadership stems from substantial government investments in semiconductor infrastructure, favorable manufacturing costs, and proximity to major electronics markets. Taiwan's TSMC and South Korea's Samsung represent anchor customers driving significant demand for advanced photoresist stripping solutions. China's aggressive semiconductor development initiatives are creating new growth opportunities, though geopolitical considerations influence market dynamics.

North America holds approximately 30% market share, benefiting from technological innovation leadership and the presence of major equipment suppliers. The region's strength lies in R&D capabilities and early adoption of advanced manufacturing technologies. Environmental regulations in North America are driving development of sustainable stripping solutions, creating opportunities for companies focused on eco-friendly alternatives. Europe commands around 25% market share, with strong emphasis on environmental sustainability and regulatory compliance influencing technology adoption patterns. The region's focus on automotive semiconductors and industrial applications creates specialized demand for customized stripping solutions.

Get More Information about this report -

Request Free Sample ReportMarket Key Segment

Product Type

- Positive Photoresist Stripper

- Negative Photoresist Stripper

Application

- Integrated Circuit Manufacturing

- Wafer Level Packaging

Technology

- Wet Stripping

- Dry Stripping

End User

- Foundries

- IDMs (Integrated Device Manufacturers)

- Other Facilities

Region:

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 627.55 M |

| Forecast Revenue (2034) | USD 1109.35 M |

| CAGR (2025-2034) | 6.53% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Product Type (Positive Photoresist Stripper, Negative Photoresist Stripper), (Application, Integrated Circuit Manufacturing, Wafer Level Packaging), Technology (Wet Stripping, Dry Stripping), End User (Foundries, IDMs (Integrated Device Manufacturers), Other Facilities) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Applied Materials, Lam Research, Merck KGaA, Advanced Energy Industries, Brewer Science, EV Group, Screen Holdings Co. Ltd., Nordson Corp. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, (Application, Integrated Circuit Manufacturing, Wafer Level Packaging), Technology (Wet Stripping, Dry Stripping), End User (Foundries, IDMs (Integrated Device Manufacturers), Other Facilities ) Industry Region & Key Players – Segment Overview, Dynamics, Strategies, Trends & Forecast 2025–2034")

, (Application, Integrated Circuit Manufacturing, Wafer Level Packaging), Technology (Wet Stripping, Dry Stripping), End User (Foundries, IDMs (Integrated Device Manufacturers), Other Facilities ) Industry Region & Key Players – Segment Overview, Dynamics, Strategies, Trends & Forecast 2025–2034")

, (Application, Integrated Circuit Manufacturing, Wafer Level Packaging), Technology (Wet Stripping, Dry Stripping), End User (Foundries, IDMs (Integrated Device Manufacturers), Other Facilities ) Industry Region & Key Players – Segment Overview, Dynamics, Strategies, Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Semiconductor Photoresist Stripping Market?

The global Semiconductor Photoresist Stripping Market is projected to grow at a CAGR of 6.53%, rising from USD 589.09 Million in 2024 to USD 1109.35 Million by 2034.

Who are the major players in the Semiconductor Photoresist Stripping Market?

Applied Materials, Lam Research, Merck KGaA, Advanced Energy Industries, Brewer Science, EV Group, Screen Holdings Co. Ltd., Nordson Corp.

Which segments covered the Semiconductor Photoresist Stripping Market?

Product Type (Positive Photoresist Stripper, Negative Photoresist Stripper), (Application, Integrated Circuit Manufacturing, Wafer Level Packaging), Technology (Wet Stripping, Dry Stripping), End User (Foundries, IDMs (Integrated Device Manufacturers), Other Facilities)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Semiconductor Photoresist Stripping Market

Published Date : 04 Aug 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date