- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Shape Memory Polymer Market Size, Share & Forecast | CAGR 11.9%

Global Shape Memory Polymer Market Size, Share, Growth Analysis By Material Type (Polyurethane SMP, Polyurethane-Urea SMP, Epoxy-Based SMP, Polyethylene SMP, Styrene-Based SMP), By Form (Films & Sheets, Foams, Fibers & Textiles, Molded Parts), By Application (Biomedical, Aerospace, Automotive, Smart Textiles, Robotics, Consumer Electronics), By End-Use Industry, Manufacturing Process & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 2.14 Billion | USD 5.87 Billion | 11.9% | Asia Pacific, 38.4% |

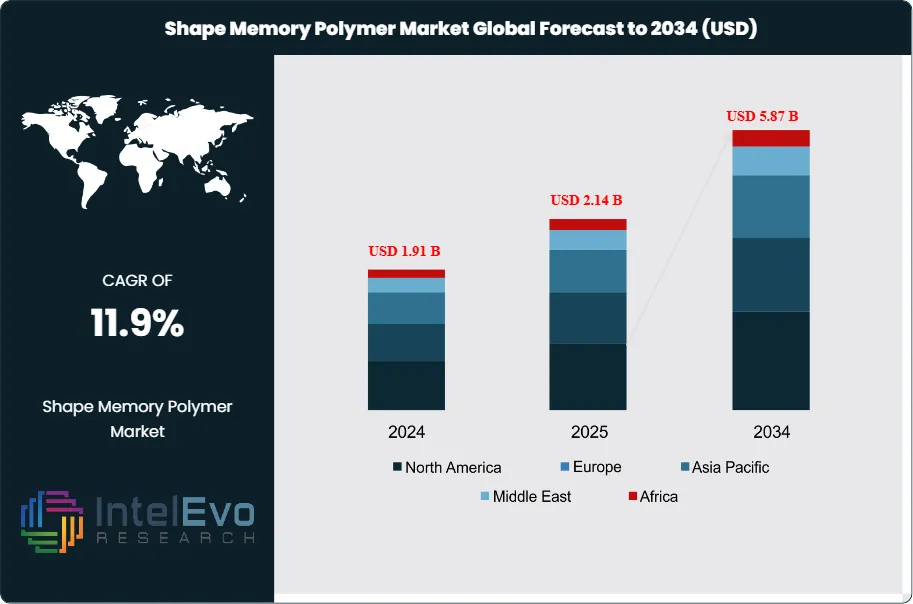

The Shape Memory Polymer Market was valued at approximately USD 1.91 Billion in 2024 and reached USD 2.14 Billion in 2025. The market is projected to grow to USD 5.87 Billion by 2034, expanding at a CAGR of 11.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.73 Billion over the analysis period, underpinned by accelerating adoption of stimuli-responsive smart materials across biomedical devices, aerospace structures, automotive systems, and advanced textile applications.

Get More Information about this report -

Request Free Sample ReportShape memory polymers are a class of stimuli-responsive advanced materials capable of fixing a temporary shape and recovering a programmed permanent shape upon exposure to thermal, photic, chemical, or electromagnetic triggers. Unlike metallic shape memory alloys, SMPs offer significantly lower density (0.9–1.3 g/cm3 versus 6.4–6.5 g/cm3 for Nitinol), design flexibility across a wide actuation temperature range (typically -10°C to 120°C), biocompatibility potential, and lower raw material cost — characteristics driving substitution across precision engineering sectors. Industry analysis confirms that polyurethane-based SMPs represent the dominant material type, accounting for 38.6% of global revenue in 2025, due to their well-established synthesis routes, broad transition temperature programmability, and commercial availability from major European chemical producers including Covestro and Evonik.

Demand-side dynamics reflect two distinct growth vectors. First, the biomedical sector is deploying shape memory polymers in minimally invasive devices including self-expanding vascular stents, intracranial aneurysm occlusion systems, and drug-eluting implants where the SMP actuates from a compressed delivery profile to a deployed therapeutic geometry upon reaching body temperature. The U.S. FDA has cleared 14 SMP-based device submissions under 510(k) and De Novo pathways between 2022 and 2025, validating clinical translation momentum. Second, the aerospace and defense sector is utilizing SMP composites for deployable satellite structures, morphing aerosurfaces, and low-observable antenna panels, areas prioritized under NASA's Space Technology Mission Directorate and DARPA's Advanced Materials programs.

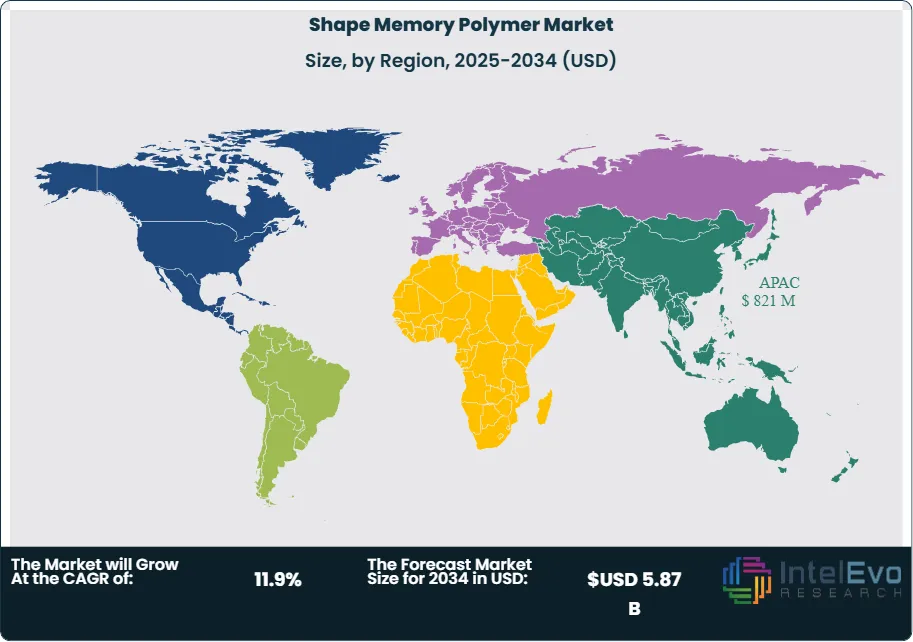

Asia Pacific leads global shape memory polymer demand with a 38.4% share at USD 821 Million in 2025, driven by China's dominant role in polymer feedstock production, Japan's advanced materials research base, and South Korea's electronics and semiconductor material supply chains. North America is the second-largest region at 28.7%, with aerospace and defense applications anchoring demand. Europe accounts for 21.4%, supported by the region's concentration of SMP material producers in Germany and the Netherlands and growing automotive lightweighting requirements under EU CO2 fleet emission regulations. The 4D printing segment — where SMPs serve as the active material in time-evolving three-dimensional printed structures — is the fastest-growing application, expanding at a 19.3% CAGR and drawing USD 186 Million in revenue in 2025.

Regulatory frameworks across end-use sectors are shaping SMP market trajectories meaningfully. In medical devices, ISO 10993 biocompatibility testing and ASTM F3355 shape memory test standards define the qualification pathway. In aerospace, FAA AC 20-107B and EASA CS-25 impose structural material certification requirements that SMP composite systems must satisfy before entering primary structures. REACH regulation in the EU governs the chemical composition of SMP formulations containing diisocyanate precursors, with updated REACH restrictions on MDI and TDI-based systems effective 2024 compelling manufacturers to reformulate toward aliphatic isocyanate chemistries — a shift adding 8–14% to raw material costs but opening new EU market access.

, By Form (Films & Sheets, Foams, Fibers & Textiles, Molded Parts), By Application (Biomedical, Aerospace, Automotive, Smart Textiles, Robotics, Consumer Electronics), By End-Use Industry, Manufacturing Process & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global shape memory polymer market was valued at USD 2.14 Billion in 2025 and is projected to reach USD 5.87 Billion by 2034, advancing at a CAGR of 11.9% across the 2026–2034 forecast period.

- Segment Dominance: By material type, polyurethane SMPs hold the largest share at 38.6% of global market revenue in 2025, favored for their broad transition temperature programmability, commercial scalability, and established supply chains among European specialty chemical producers.

- Segment Dominance: By application, biomedical and healthcare is the leading segment at 31.2% of global SMP market revenue in 2025, driven by FDA-cleared SMP vascular and neurovascular device approvals and increasing clinical preference for body-temperature-actuated minimally invasive implants.

- Driver: Rapid expansion of minimally invasive surgery and interventional cardiology — a combined global procedure volume exceeding 28 million annually in 2025 — is creating direct pull-through demand for SMP-based self-expanding devices, stents, and deployment systems that eliminate mechanical actuation mechanisms.

- Restraint: High shape-recovery precision requirements and long qualification timescales — averaging 24–36 months for aerospace-grade SMP composites and 36–48 months for FDA-cleared SMP medical devices — constrain revenue conversion of SMP pipeline applications and limit market growth velocity by an estimated 1.8–2.4 CAGR percentage points.

- Opportunity: The 4D printing application segment represents an addressable incremental market of USD 1.2 Billion by 2034, growing at 19.3% CAGR, as additive manufacturing platforms integrate SMP filament and resin systems for soft robotics, deployable space structures, and programmable biomedical scaffolds.

- Trend: Multi-stimuli-responsive SMP systems capable of actuation via combinations of heat, light, moisture, and magnetic fields are reaching commercial readiness, with 23 new multi-trigger SMP formulations registered under ASTM and ISO standards between 2023 and 2025, opening automotive and soft robotics end-uses previously inaccessible to single-trigger systems.

- Regional Analysis: Asia Pacific is the dominant region with a 38.4% share, equivalent to USD 821 Million in 2025 revenue, with China, Japan, and South Korea collectively representing 81.3% of regional demand across electronics, automotive, and biomedical SMP applications.

Competitive Landscape Overview

The shape memory polymer market is moderately fragmented, with the top four players — Covestro, Evonik Industries, BASF, and Mitsubishi Chemical Group — collectively accounting for approximately 44.8% of global revenue in 2025. Competition is primarily technology-driven, centered on polymer architecture innovation, transition temperature precision, and end-use sector application development support. The market has experienced a notable increase in strategic partnerships between material producers and device manufacturers, particularly in the biomedical and aerospace segments, as customers require co-development commitments to reduce application qualification risk. New entrants with expertise in 4D printing-compatible SMP formulations are intensifying competition in the research and prototyping segment, where IP position rather than scale is the primary competitive currency.

Competitive Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Move (2024–2026) |

| Covestro AG | Germany | Leader | Desmopan SMP Polyurethane | Europe / Asia Pacific | Launched bio-based SMP series for automotive OEMs, Feb 2025 |

| Evonik Industries | Germany | Leader | VESTAMID SMP Polyamide | Europe / North America | Expanded SMP compounding capacity in Marl, Germany by 18,000 MT, Apr 2025 |

| BASF SE | Germany | Challenger | Elastollan SMP TPU Grade | Europe / North America | Partnered with Airbus for aerospace SMP actuator qualification, Jul 2025 |

| Mitsubishi Chemical Group | Japan | Challenger | DiARY SMP Film | Asia Pacific | Acquired SMP startup Toki Corp. for USD 88M to expand medical SMP portfolio, Oct 2025 |

| Cornerstone Research Group | USA | Niche Player | SMP Structural Epoxy Systems | North America | Received USD 34M DARPA contract for deployable SMP space structures, Jan 2026 |

| SMP Technologies (Spinoff) | USA | Niche Player | MemShape SMP Blend | North America | Entered licensing agreement with Medtronic for vascular SMP stent applications, Mar 2025 |

| Toray Industries | Japan | Niche Player | Torayfan SMP Film | Asia Pacific | Commenced pilot production of SMP composite pre-preg for drone fuselage, Aug 2025 |

| Asahi Kasei | Japan | Niche Player | Tenac SMP Engineering Resin | Asia Pacific | Deployed SMP textile fiber line for smart garment applications, Nov 2025 |

By Material Type

The shape memory polymer market by material type is led by polyurethane SMPs, which account for 38.6% of global revenue at USD 826 Million in 2025. Polyurethane SMPs are synthesized through reaction of polyols, chain extenders, and diisocyanate hard segments, enabling precise programming of transition temperatures (Ttrans) across a -20°C to 90°C range by adjusting hard-to-soft segment ratios. Their commercial advantage lies in scalable manufacturing using standard polyurethane processing equipment, broad biocompatibility profiles confirming ISO 10993 compliance, and well-characterized mechanical performance including tensile strengths of 25–60 MPa and shape recovery ratios exceeding 96% under optimized formulations. Covestro's Desmopan and Evonik's VESTAMID SMP grades are benchmark products in this sub-segment, widely deployed in medical device prototyping and automotive component applications.

Epoxy-based SMPs represent 21.4% of the market at USD 458 Million in 2025, with applications concentrated in aerospace structural components and electronic packaging where thermoset rigidity, high shape fixity ratios above 99%, and Ttrans values in the 80°C–150°C range are required. Cross-linked polyethylene SMPs account for 14.2% at USD 304 Million, primarily used in heat-shrink tubing, pipe repair sleeves, and packaging applications where radiation-induced crosslinking provides stable shape memory behavior. Styrene-based and copolymer SMPs hold 12.8% at USD 274 Million, valued for transparency and UV-trigger compatibility. Other SMP formulations — including polyamide, polynorbornene, polylactic acid, and multi-block copolymer systems — collectively represent the remaining 13.0% at USD 278 Million in 2025, with polylactic acid SMPs growing at the fastest sub-segment rate of 17.8% CAGR through 2034 due to biodegradable implant applications.

By Form

Films and sheets constitute the largest form segment in the shape memory polymer market at 29.3% of revenue, equivalent to USD 627 Million in 2025. SMP films serve critical functions in self-healing automotive paint protection layers, shape-morphing packaging, and deployable membrane structures in space applications. Film production via solvent casting and melt extrusion allows tight control over film thickness (5–500 microns) and transition temperature uniformity across web widths. Foams represent 24.1% of the market at USD 516 Million, with applications in self-deploying space insulation panels, adaptive cushioning systems, and thermal energy storage media for building envelopes. SMP foams can achieve volumetric expansion ratios of 2:1 to 8:1 upon thermal actuation, enabling compact storage and deployment in inaccessible environments.

Fibers and textiles account for 19.6% of SMP revenue at USD 420 Million in 2025, with growth driven by smart garment applications in athletic wear, medical compression therapy, and protective equipment that adapts fit geometry to body temperature changes. SMP fiber spinning via electrospinning and melt spinning produces filaments with diameters of 10–500 microns and programmable crimp-recovery behaviors. Bulk and molded parts represent the remaining 27.0% at USD 578 Million, the dominant form for automotive, aerospace structural, and biomedical device end-uses where three-dimensional geometry and load-bearing requirements drive production via injection molding and compression molding processes.

By Application

Biomedical and healthcare is the leading application segment of the shape memory polymer market, capturing 31.2% of global revenue at USD 668 Million in 2025 and growing at 13.7% CAGR through 2034. SMP devices leverage body temperature (37°C) as the thermal trigger, enabling self-expanding stents, intracranial flow diverters, spinal fixation components, and drug-eluting scaffolds to deploy from a compressed catheter-deliverable profile to a therapeutic expanded geometry without external actuation mechanisms. The FDA's De Novo pathway has cleared SMP neurovascular implants from three manufacturers since 2023, establishing clinical precedent that is accelerating physician adoption. Drug-device combination products incorporating SMP matrices for controlled-release applications are advancing through IND filings under 21 CFR Part 3 combination product regulations, representing a high-value sub-segment.

Aerospace and defense accounts for 22.8% of SMP revenue at USD 488 Million in 2025. SMP composites serve morphing wing skins, deployable antenna booms, satellite solar array hinges, and low-observable radar-absorbing panels. The segment is growing at 14.1% CAGR, supported by NASA, ESA, JAXA, and DARPA investment in deployable space structures where SMP actuators reduce mass versus motor-driven mechanisms by 35–55%. Automotive represents 18.4% at USD 394 Million, with applications in self-healing clearcoat systems (exploiting photo-triggered SMP recovery), morphing air dam components for aerodynamic efficiency, and smart joining systems. Textiles and smart fabrics hold 12.6% at USD 270 Million, robotics and actuators 9.2% at USD 197 Million, and consumer electronics the remaining 5.8% at USD 124 Million.

By End-Use Industry

Healthcare and life sciences is the dominant end-use industry in the shape memory polymer market, representing 33.8% of global revenue at USD 723 Million in 2025. This segment encompasses medical device OEMs, surgical instrument manufacturers, and biopharmaceutical drug delivery companies investing in SMP-based therapeutic systems. The concentration of SMP-active device development programs at Medtronic, Boston Scientific, Abbott, and Stryker validates the industrial commitment to SMP adoption. Aerospace and defense follows at 22.8% as analyzed above. Automotive and transportation accounts for 18.4%, with Europe's fleet CO2 emission targets under EU Regulation 2019/631 and lightweighting mandates driving substitution of metal actuators with SMP analogs where mass reduction exceeds 40%.

Electronics and semiconductors represent 10.7% of SMP end-use revenue at USD 229 Million in 2025, with applications in self-healing protective films for flexible OLED displays, SMP encapsulants for semiconductor packaging capable of stress relief at reflow temperatures, and smart connector components. The textile and apparel industry accounts for 8.3% at USD 178 Million. Industrial and other end-uses — including oil and gas pipeline repair sleeves, SMP-based fasteners, and environmental sensing applications — represent the remaining 6.0% at USD 128 Million in 2025.

By Manufacturing Process

Injection molding is the dominant manufacturing process in the shape memory polymer market, holding 34.7% of production volume in 2025. The process is favored for net-shape production of complex three-dimensional SMP components in automotive and medical device applications, where tolerances of plus or minus 0.05 mm are achievable with optimized tooling. Extrusion accounts for 28.4%, primarily serving film, sheet, and fiber production. Additive manufacturing — encompassing FDM with SMP filaments, DLP with SMP resins, and multi-material jetting — represents 17.6% of process share in 2025 and is the fastest-growing process at 22.1% CAGR, driven by 4D printing research programs and the ability to produce personalized SMP medical implants with patient-specific transition temperature profiles. Electrospinning accounts for 11.8% and serves SMP fiber and scaffold production for biomedical applications, while other processes (compression molding, solvent casting) constitute the remaining 7.5%.

Regional Analysis

Asia Pacific Shape Memory Polymer Market

Asia Pacific leads the global shape memory polymer market with a 38.4% share at USD 821 Million in 2025, growing at a 13.4% CAGR through 2034 — the fastest regional growth rate globally. China is the dominant country, representing 44.2% of Asia Pacific SMP revenue at USD 363 Million in 2025. Chinese demand is driven by the country's position as the world's largest automotive manufacturer (producing 30.2 million vehicles in 2024), its expanding medical device manufacturing sector operating under NMPA reforms, and state investment in aerospace materials under the C919 and COMAC programs. Japan contributes 28.6% of APAC revenue at USD 235 Million, anchored by precision applications in electronics (semiconductor packaging, flexible display films), robotics, and medical devices at Toray, Asahi Kasei, and Mitsubishi Chemical. South Korea represents 10.4% at USD 85 Million, with Samsung Display and LG Chem driving SMP adoption in flexible electronics. India accounts for 8.1% at USD 66 Million, with growth accelerating in automotive and healthcare sectors under Make in India manufacturing incentives.

North America Shape Memory Polymer Market

North America accounts for 28.7% of global SMP revenue at USD 614 Million in 2025. The United States drives 87.4% of regional demand at USD 537 Million, with the biomedical application and aerospace and defense segments collectively accounting for 68.3% of US SMP consumption. Defense spending on SMP research through DARPA, AFRL, and NASA has exceeded USD 180 Million cumulatively since 2020, establishing a strong pull-through effect on commercial SMP adoption. The country hosts the highest concentration of SMP-focused startups globally, supported by NIH SBIR grants and DoD CRADA agreements that facilitate technology transfer from university research to commercial production. Canada represents 8.4% of North American SMP revenue, primarily in automotive applications tied to Tier 1 suppliers in Ontario. Mexico contributes 4.2%, with demand growing from cross-border automotive manufacturing operations.

Europe Shape Memory Polymer Market

Europe holds 21.4% of global SMP revenue at USD 458 Million in 2025. Germany is the dominant European market at 31.2% of regional revenue, reflecting its leadership in advanced polymer chemistry and automotive engineering. Covestro and Evonik — both headquartered in Germany — account for a combined 58.4% of European SMP production capacity. France contributes 16.8% of European SMP revenue, supported by Airbus Groupe's aerospace materials programs and Solvay's specialty polymer operations. The United Kingdom represents 14.6%, with SMP medical device development concentrated in the UK MedTech cluster around London and Cambridge. The Netherlands holds 11.4% of European SMP revenue, driven by DSM (now Firmenich-DSM) and Shell Chemicals' specialty polymer operations. EU CO2 fleet emission regulations and the European Green Deal are compelling automotive OEMs to accelerate SMP adoption for lightweight actuator components, adding an estimated EUR 340 Million in incremental SMP demand through 2030.

Latin America Shape Memory Polymer Market

Latin America accounts for 7.1% of global SMP revenue at USD 152 Million in 2025. Brazil leads the region at 49.3% of LATAM SMP revenue, with demand concentrated in automotive, oil and gas pipeline rehabilitation (where SMP heat-shrink sleeves serve as corrosion protection systems), and growing medical device manufacturing under ANVISA's regulatory framework. Mexico represents 29.4% of regional revenue, benefiting from its deep integration with North American automotive supply chains. Colombia contributes 8.6%, with nascent medical device and agricultural packaging SMP applications expanding under free trade agreements with the United States and EU. Regional growth is constrained by limited domestic SMP production capacity, which creates import dependency and subjects the market to currency volatility risk against USD-denominated material contracts.

Middle East & Africa Shape Memory Polymer Market

The Middle East and Africa region holds 4.4% of global SMP revenue at USD 94 Million in 2025. The UAE leads regional demand at 32.8% of MEA SMP revenue, driven by aerospace MRO activity at Dubai Aerospace Enterprise and growing advanced manufacturing investment under the UAE National Advanced Technology Strategy. Saudi Arabia represents 27.6% of MEA revenue, with ARAMCO's upstream pipeline integrity programs deploying SMP-based pipe repair composite sleeves and Vision 2030 diversification driving healthcare device manufacturing investment. South Africa accounts for 19.2% of MEA SMP revenue, representing the primary gateway for Sub-Saharan African industrial SMP adoption. Regional SMP market development is at an early stage, and multinational material producers are beginning to establish technical sales infrastructure in the Gulf Cooperation Council countries to support qualification programs at local manufacturing operations.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Material Type

- Polyurethane (PU) SMP

- Polyurethane-Urea (PUU) SMP

- Epoxy-Based SMP

- Polyethylene (Cross-linked) SMP

- Styrene-Based SMP

- Other SMP Formulations

By Form

- Films & Sheets

- Foams

- Fibers & Textiles

- Bulk/Molded Parts

By Application

- Biomedical & Healthcare

- Aerospace & Defense

- Automotive

- Textiles & Smart Fabrics

- Robotics & Actuators

- Consumer Electronics

By End-Use Industry

- Healthcare & Life Sciences

- Aerospace & Defense

- Automotive & Transportation

- Electronics & Semiconductors

- Textile & Apparel

- Industrial & Others

By Manufacturing Process

- Injection Molding

- Extrusion

- 3D Printing / Additive Manufacturing

- Electrospinning

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.14 B |

| Forecast Revenue (2034) | USD 5.87 B |

| CAGR (2025-2034) | 11.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material Type, (Polyurethane (PU) SMP, Polyurethane-Urea (PUU) SMP, Epoxy-Based SMP, Polyethylene (Cross-linked) SMP, Styrene-Based SMP, Other SMP Formulations), By Form, (Films & Sheets, Foams, Fibers & Textiles, Bulk/Molded Parts), By Application, (Biomedical & Healthcare, Aerospace & Defense, Automotive, Textiles & Smart Fabrics, Robotics & Actuators, Consumer Electronics), By End-Use Industry, (Healthcare & Life Sciences, Aerospace & Defense, Automotive & Transportation, Electronics & Semiconductors, Textile & Apparel, Industrial & Others), By Manufacturing Process, (Injection Molding, Extrusion, 3D Printing / Additive Manufacturing, Electrospinning) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | COVESTRO AG, EVONIK INDUSTRIES, BASF SE, MITSUBISHI CHEMICAL GROUP, CORNERSTONE RESEARCH GROUP, SMP TECHNOLOGIES INC., TORAY INDUSTRIES, ASAHI KASEI CORPORATION, HUNTSMAN CORPORATION, SOLVAY SA, LUBRIZOL CORPORATION, DUPONT DE NEMOURS, DSM-FIRMENICH, LANXESS AG, KURARAY CO. LTD., NIPPON STEEL CHEMICAL & MATERIAL, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Form (Films & Sheets, Foams, Fibers & Textiles, Molded Parts), By Application (Biomedical, Aerospace, Automotive, Smart Textiles, Robotics, Consumer Electronics), By End-Use Industry, Manufacturing Process & Forecast 2026-2034")

, By Form (Films & Sheets, Foams, Fibers & Textiles, Molded Parts), By Application (Biomedical, Aerospace, Automotive, Smart Textiles, Robotics, Consumer Electronics), By End-Use Industry, Manufacturing Process & Forecast 2026-2034")

, By Form (Films & Sheets, Foams, Fibers & Textiles, Molded Parts), By Application (Biomedical, Aerospace, Automotive, Smart Textiles, Robotics, Consumer Electronics), By End-Use Industry, Manufacturing Process & Forecast 2026-2034")

Frequently Asked Questions

How big is the Shape Memory Polymer Market?

The Global Shape Memory Polymer Market was valued at USD 1.91 Billion in 2024 and is projected to reach USD 5.87 Billion by 2034, growing at a CAGR of 11.9% from 2026 to 2034, driven by increasing demand for smart materials in biomedical devices, aerospace, automotive, electronics, and advanced 4D printing applications.

Who are the major players in the Shape Memory Polymer Market?

COVESTRO AG, EVONIK INDUSTRIES, BASF SE, MITSUBISHI CHEMICAL GROUP, CORNERSTONE RESEARCH GROUP, SMP TECHNOLOGIES INC., TORAY INDUSTRIES, ASAHI KASEI CORPORATION, HUNTSMAN CORPORATION, SOLVAY SA, LUBRIZOL CORPORATION, DUPONT DE NEMOURS, DSM-FIRMENICH, LANXESS AG, KURARAY CO. LTD., NIPPON STEEL CHEMICAL & MATERIAL, OTHERS

Which segments covered the Shape Memory Polymer Market?

By Material Type, (Polyurethane (PU) SMP, Polyurethane-Urea (PUU) SMP, Epoxy-Based SMP, Polyethylene (Cross-linked) SMP, Styrene-Based SMP, Other SMP Formulations), By Form, (Films & Sheets, Foams, Fibers & Textiles, Bulk/Molded Parts), By Application, (Biomedical & Healthcare, Aerospace & Defense, Automotive, Textiles & Smart Fabrics, Robotics & Actuators, Consumer Electronics), By End-Use Industry, (Healthcare & Life Sciences, Aerospace & Defense, Automotive & Transportation, Electronics & Semiconductors, Textile & Apparel, Industrial & Others), By Manufacturing Process, (Injection Molding, Extrusion, 3D Printing / Additive Manufacturing, Electrospinning)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date