- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Silicone Rubber Market Size Growth Forecast, Trends & 8.6% CAGR

Global Silicone Rubber Market Size, Share & Analysis By Product Type (Room Temperature Vulcanized (RTV), High Temperature Vulcanized (HTV), Liquid Silicone Rubber (LSR)), Applications (Automotive & Transportation, Electrical & Electronics, Industrial Machinery, Consumer Goods, Construction, Healthcare, Others), By End-User Industry, Performance Advantages, Competitive Landscape & Forecast 2025–2034

Report Overview

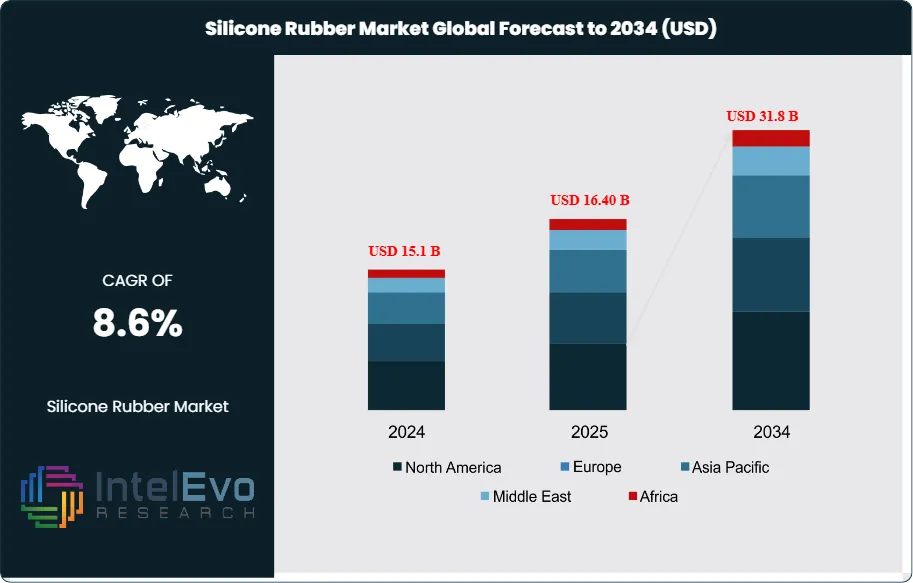

The Silicone Rubber Market is valued at USD 15.1 billion in 2024 and is projected to reach approximately USD 31.8 billion by 2034, expanding at a CAGR of around 8.6% during 2025–2034. Continuous demand from automotive, electronics, healthcare, and renewable energy applications is accelerating global adoption of high-performance silicone elastomers. As industries shift toward heat-resistant, durable, and biocompatible materials, silicone rubber is becoming a cornerstone for next-generation manufacturing. With rising EV production, medical device innovation, and industrial automation, the market is expected to witness strong momentum across all major regions through the next decade.

Get More Information about this report -

Request Free Sample ReportThis steady expansion reflects silicone rubber’s differentiated performance profile—thermal stability from −50°C to >200°C, electrical insulation, UV/weathering resistance, and biocompatibility—that entrenches demand across automotive, electronics, construction, healthcare, and consumer goods. After a pandemic-era dip, volumes rebounded through 2021–2023 alongside vehicle production and electronics output; value growth outpaced volume on premiumization toward liquid silicone rubber (LSR), high-consistency rubber (HCR), and specialty grades. The decade ahead adds an incremental c. USD 9.8 billion, underpinned by three structural themes: electrification, miniaturization, and medical device penetration.

On the demand side, EV adoption accelerates usage in thermal interface materials, high-voltage cable insulation, gasketing, and sensor encapsulation; in many platforms, silicone rubber content per vehicle is rising mid-single digits annually. Electronics requires heat-resistant, low-outgassing elastomers for 5G infrastructure, wearables, and power modules. Healthcare continues to mix-shift toward implantables and drug-delivery components, where medical-grade silicone’s regulatory pedigree (USP Class VI, ISO 10993) supports above-market growth. Supply-side dynamics remain shaped by upstream siloxane/MDM availability and energy costs—particularly in China, which dominates monomer capacity—creating margin cyclicality and pricing pass-through risk. Tighter environmental regulations (e.g., VOC limits, REACH-related scrutiny of cyclic siloxanes in adjacent chemistries) and end-of-life considerations require investment in cleaner curing systems and take-back/regrind programs.

Technology is a clear catalyst. Advancements in LSR micro-molding and multi-shot over-molding shorten cycle times and reduce scrap; AI-enabled process controls and machine-vision inspection improve first-pass yield in high-precision parts. Formulation innovation is broadening addressable use cases: halogen-free flame-retardant grades for rail/building, high-thermal-conductivity compounds (~1–4 W/m·K) for power electronics, and low-volatile, low-compression-set elastomers for autonomy-ready sensors. Early additive manufacturing pathways for silicone elastomers are emerging for rapid prototypes and patient-specific medical devices.

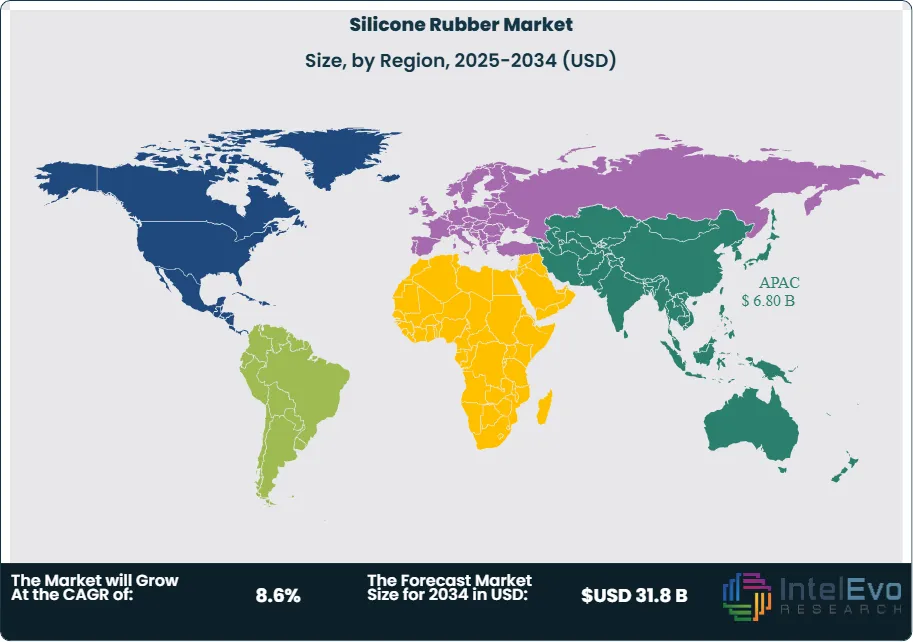

Regionally, Asia–Pacific accounts for an estimated >45% of revenue, led by China’s integrated supply chains and expanding Southeast Asian manufacturing. North America benefits from onshoring in medical devices and grid/EV infrastructure, while Europe’s renovation wave and rail standards favor premium, compliant grades. Investment hot spots include EV battery plants, advanced packaging and power-semiconductor hubs, and medtech clusters in the United States, Germany, Ireland, China’s coastal provinces, India, and Vietnam—locations where demand density, regulatory clarity, and skilled labor tilt the risk-reward balance toward capacity additions and specialty product lines.

, High Temperature Vulcanized (HTV), Liquid Silicone Rubber (LSR)), Applications (Automotive & Transportation, Electrical & Electronics, Industrial Machinery, Consumer Goods, Construction, Healthcare, Others), By End-User Industry, Performance Advantages, Competitive Landscape & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Silicone Rubber market was USD 15.1 billion in 2024 and is projected to reach USD 31.8 billion by 2034, reflecting a 8.6% CAGR driven by electrification (EV/charging), miniaturized electronics, and medical devices requiring biocompatible elastomers.

- Product Type: HTV/HCR led in 2023 with ~48.5% share, favored for superior heat/chemical resistance in under-hood, wire & cable, and industrial sealing; LSR is the fastest-growing sub-segment (~7–8% CAGR) on the back of injection molding for precision medical and electronics parts.

- Application: Automotive & Transportation accounted for ~36.7% of demand in 2023 as OEMs adopt silicone gaskets, thermal interface compounds, and sensor encapsulants; EV platforms are lifting per-vehicle silicone content and mix-shifting toward higher-value thermal and high-voltage insulation grades.

- Driver: Rapid EV and power-electronics penetration is expanding use in thermal management (1–4 W/m·K compounds), HV cable insulation, and ADAS sensor sealing; alongside 5G/IoT, this is sustaining mid-single-digit volume growth with above-inflation pricing in specialty grades.

- Restraint: Upstream siloxane/MDM price volatility and energy-linked costs (notably in China) can swing input prices ±20–30% YoY, compressing converter margins by 150–250 bps and complicating long-term supply contracts.

- Opportunity: Medical-grade silicone (ISO 10993/USP Class VI) for implants, wound care, and drug-delivery components is poised to outpace the market (~8–9% CAGR), potentially exceeding USD 5–6 billion by 2033 as OEMs reshore sterile, LSR micro-molded production.

- Trend: Process intensification—multi-shot over-molding, LSR micro-molding, and AI-enabled vision/closed-loop controls—is raising first-pass yield and shortening cycle times; additive manufacturing of silicones is emerging for patient-specific devices and rapid prototyping.

- Regional Analysis: Asia–Pacific commands ~45–50% of revenue, anchored by China’s integrated monomer-to-compounding footprint and rising ASEAN manufacturing; North America benefits from EV/battery and medtech investments (CAGR ~6–7%), while Europe grows ~5–6% supported by rail/building fire-safety standards and renovation demand.

- Competitive Landscape: Leading players—Dow, Wacker Chemie, Shin-Etsu, Momentive, Elkem, and KCC—are reallocating capacity toward high-purity LSR, flame-retardant, and high-thermal-conductivity lines; differentiated application support and security of MDM supply are key to share gains.

Type Analysis

In 2025, High-Temperature Vulcanized (HTV/HCR) grades remain the anchor of the silicone rubber portfolio, sustaining an estimated 47–49% revenue share on the strength of superior heat, tear, and chemical resistance. Demand concentrates in under-hood components, high-voltage wire & cable, and industrial sealing where peroxide- and platinum-cured HTV maintains performance from −50°C to >200°C. Growth is steady rather than breakaway (≈4–5% CAGR to 2033) as customers prioritize durability, flame-retardancy, and compliance for rail/building applications.

Room Temperature Vulcanized (RTV) systems—both one-part moisture-cure and two-part addition-cure—hold a solid mid-20s share, benefitting from ease of use at ambient conditions and broad compatibility with substrates. Uptake in construction glazing, façade sealing, and electronics potting tracks retrofit cycles and infrastructure programs, with low-VOC, low-migrating formulations gaining share in regulated markets.

Liquid Silicone Rubber (LSR) is the clear out-performer, expanding at ~7–9% CAGR through 2033 as precision injection-molding, multi-shot over-molding, and micro-molding enable tight-tolerance parts. LSR’s biocompatibility (ISO 10993/USP Class VI) and low compression set underpin rapid adoption in medical devices, infant care, and wearables; by 2030, LSR’s mix could approach a quarter of sector revenues as suppliers (e.g., Wacker, Shin-Etsu, Dow, Momentive, Elkem) scale high-purity lines and high-thermal-conductivity variants.

Application Analysis

Sealing & gasketing remains the largest functional use, representing roughly 35–40% of 2025 demand as OEMs specify long-life elastomers for dynamic seals, profiles, and O-rings exposed to fuels, oils, and thermal cycling. Cycle-time reductions from cold-runner and hot-deck LSR systems enhance cost competitiveness versus alternative elastomers.

Electrical insulation & encapsulation accounts for ~25–28% of consumption, lifted by power electronics, 5G infrastructure, and sensor packaging that require low-outgassing, arc-resistant materials. Potting and conformal coatings using RTV/LSR are displacing epoxies in high-reliability modules due to improved flexibility and thermal shock resistance.

Thermal management is the fastest-rising niche, with gap fillers, pads, and adhesives delivering 1–4 W/m·K conductivity for EV batteries, inverters, and data-center power supplies. This slice is poised to climb toward 10–12% of the market by 2030 (from high-single-digits in 2024), supported by increasing watt densities and stricter reliability standards.

End-Use Analysis

Automotive & Transportation leads with ~35–37% of 2025 volume; EV platforms lift per-vehicle silicone content by ~8–12% versus ICE due to battery sealing, HV insulation, and thermal interface materials. Content growth offsets cyclical builds, supporting ~6–7% value CAGR through 2033.

Electrical & Electronics represents ~22–24% share, propelled by power semiconductors, wearables, and smart-home devices that require low-volatile, high-purity elastomers. Industrial machinery holds ~12–14%, leveraging HTV’s resilience for compressors, pumps, and processing equipment.

Consumer goods (~9–11%) continue migrating to food-contact-safe LSR for bakeware and infant care; Construction (~10–12%) benefits from glazing and weatherproofing in renovation-heavy markets. Healthcare is the fastest-growing end-use (~8–9% CAGR), with implantables, wound-care, and drug-delivery devices positioning medical-grade silicone to exceed USD 5–6 billion by 2033; others remain niche but strategic in aerospace and energy.

Regional Analysis

Asia Pacific remains the demand and supply fulcrum with >45% of 2025 revenues, expanding at ~6.5–7% CAGR as China sustains monomer-to-compounding integration and ASEAN/India scale automotive, electronics, and medical manufacturing. Policy-driven localization and rising mid-income consumption accelerate adoption across transportation and consumer health.

North America benefits from EV/battery and medtech capex, onshoring of precision molding, and grid modernization, supporting ~6–7% CAGR. Europe grows at ~5–6% amid higher energy costs but strong pull for premium, low-VOC, and flame-retardant grades aligned with REACH and building/rail safety standards.

Smaller in absolute terms but accelerating, Latin America and the Middle East & Africa post ~7–8% CAGR through 2033 on industrialization, infrastructure, and energy investments. Nearshoring (Mexico, Brazil) and petrochemical integration (GCC) are creating localized opportunities in wire & cable, construction sealants, and industrial components.

Get More Information about this report -

Request Free Sample ReportKey Маrkеt Ѕеgmеntѕ

By Product Type

- Room Temperature Vulcanized (RTV)

- High Temperature Vulcanized (HTV)

- Liquid Silicone Rubber (LSR)

By Applications

- Automotive & Transportation

- Electrical & Electronics

- Industrial Machinery

- Consumer Goods

- Construction

- Healthcare

- Others

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 15.1 B |

| Forecast Revenue (2034) | USD 31.8 B |

| CAGR (2024-2034) | 8.6% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Room Temperature Vulcanized (RTV), High Temperature Vulcanized (HTV), Liquid Silicone Rubber (LSR)), Applications (Automotive & Transportation, Electrical & Electronics, Industrial Machinery, Consumer Goods, Construction, Healthcare, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Evonik Industries AG, Wacker Chemie AG, Shin-Etsu Chemical Co. Ltd., CHT Group, BRB International, Jiangsu Mingzhu Silicone Rubber Material Co. Ltd, Wynca Group, Elkem ASA, Hoshine Silicon Industry Co. Ltd, DyStar Singapore Pte Ltd, Dow, Kaneka Corporation, Mitsubishi Chemical Holdings Corporation, Momentive Silicone |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, High Temperature Vulcanized (HTV), Liquid Silicone Rubber (LSR)), Applications (Automotive & Transportation, Electrical & Electronics, Industrial Machinery, Consumer Goods, Construction, Healthcare, Others), By End-User Industry, Performance Advantages, Competitive Landscape & Forecast 2025–2034")

, High Temperature Vulcanized (HTV), Liquid Silicone Rubber (LSR)), Applications (Automotive & Transportation, Electrical & Electronics, Industrial Machinery, Consumer Goods, Construction, Healthcare, Others), By End-User Industry, Performance Advantages, Competitive Landscape & Forecast 2025–2034")

, High Temperature Vulcanized (HTV), Liquid Silicone Rubber (LSR)), Applications (Automotive & Transportation, Electrical & Electronics, Industrial Machinery, Consumer Goods, Construction, Healthcare, Others), By End-User Industry, Performance Advantages, Competitive Landscape & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date