- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Single-Use Bioprocessing Market Size & Forecast | CAGR 10.9%

Global Single-Use Bioprocessing Market Size, Share, Growth & Industry Analysis By Product Type (Single-Use Bioreactors, Filtration & Purification Systems, Fluid Management & Storage Bags, Sensors & Monitoring Equipment, Mixing Systems), By Application (mAb Production, Vaccine Manufacturing, Cell & Gene Therapy, Recombinant Proteins, Plasma Products), By End-User (Biopharma, CDMOs, CROs) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

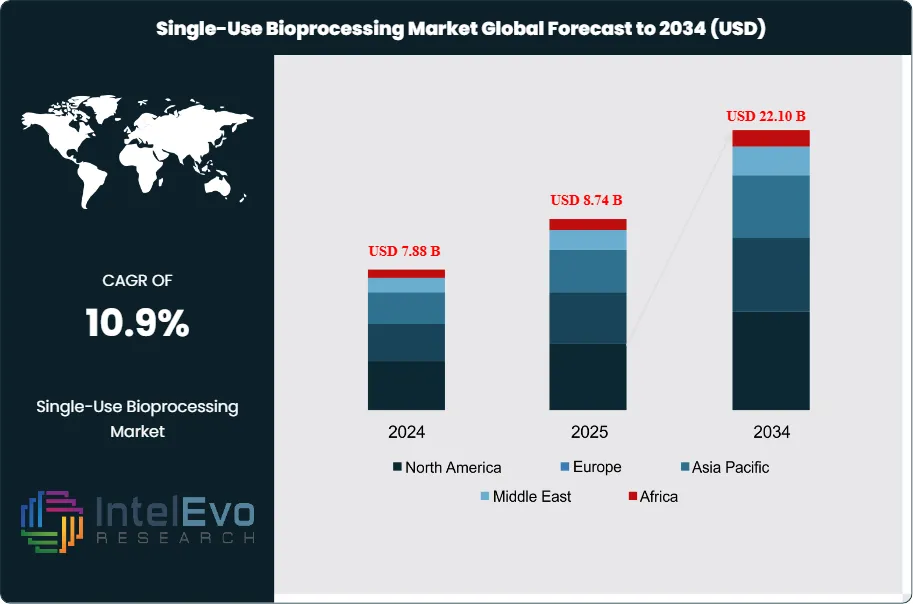

| USD 8.74 Billion | USD 22.10 Billion | 10.9% | North America, 41.3% |

The Single-Use Bioprocessing Market was valued at approximately USD 7.88 Billion in 2024 and reached USD 8.74 Billion in 2025. The market is projected to grow to USD 22.10 Billion by 2034, expanding at a CAGR of 10.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 13.36 Billion over the analysis period, underscoring the accelerating shift within the biopharmaceutical manufacturing sector toward disposable, contamination-free production technologies.

Get More Information about this report -

Request Free Sample ReportSingle-use bioprocessing encompasses a broad category of disposable equipment and assemblies used across upstream and downstream biomanufacturing stages, including bioreactors, mixers, filtration systems, storage bags, tubing manifolds, and sensors. The technology eliminates the need for clean-in-place and steam-in-place procedures, which reduces facility capital expenditure, shortens turnaround time between batches, and lowers cross-contamination risk. These attributes make single-use systems particularly attractive for contract development and manufacturing organizations (CDMOs), clinical-stage biotech firms, and vaccine manufacturers operating under time-compressed regulatory timelines.

Demand-side momentum in the single-use bioprocessing market is driven primarily by the rapid expansion of biologic drug pipelines, with FDA data indicating that biologics accounted for over 40% of all novel drug approvals in 2024. The global pipeline of monoclonal antibodies, cell therapies, gene therapies, and mRNA vaccines continues to grow, requiring flexible manufacturing infrastructure that single-use systems are uniquely positioned to provide. Regulatory bodies including the FDA, EMA, and the WHO have increasingly acknowledged the quality and traceability advantages of single-use assemblies, further reducing adoption barriers.

On the supply side, material innovation is producing single-use components with improved extractable and leachable (E&L) profiles, higher operating pressures, and greater biocompatibility. Industry consortia including the Bio-Process Systems Alliance (BPSA) and the BioPhorum Operations Group (BPOG) are advancing standardization of connector fittings, bag film specifications, and integrity testing protocols, which is accelerating supplier qualification timelines across the industry.

North America holds the leading position in the single-use bioprocessing market with a 41.3% share in 2025, anchored by dense concentrations of biopharmaceutical manufacturers, CDMOs, and research institutions in the United States. Asia Pacific is the fastest-growing regional market, driven by biomanufacturing capacity buildout in China, India, and South Korea, each supported by government-backed pharmaceutical self-sufficiency initiatives. Europe, particularly Germany, Switzerland, and Ireland, maintains a strong manufacturing base supported by EMA regulatory frameworks and established biopharma clusters.

Supply chain resilience concerns that emerged post-2020 have spurred efforts to regionalize single-use component manufacturing, with multiple suppliers announcing dedicated production facilities in the United States, Germany, and Singapore between 2023 and 2025. This regionalization trend is expected to reduce lead times, moderate pricing volatility for film-grade polymers, and improve long-term supply security for bioprocessing customers through 2034.

, By Application (mAb Production, Vaccine Manufacturing, Cell & Gene Therapy, Recombinant Proteins, Plasma Products), By End-User (Biopharma, CDMOs, CROs) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global single-use bioprocessing market was valued at USD 8.74 Billion in 2025 and is projected to reach USD 22.10 Billion by 2034, expanding at a CAGR of 10.9% during 2026–2034.

- Segment Dominance: By product type, single-use bioreactors lead with approximately 32.4% of market revenue in 2025, driven by high adoption in clinical and commercial-scale mAb and vaccine manufacturing.

- Segment Dominance: By application, monoclonal antibody (mAb) production accounts for the largest application share at 38.2% in 2025, reflecting the continued expansion of approved biologics and biosimilar pipelines.

- Driver: Rising biologic drug approvals, with FDA approving over 40 novel biologics annually, are the primary force accelerating adoption of single-use bioprocessing systems across CDMOs and integrated biopharma manufacturers.

- Restraint: High per-unit consumable costs and waste disposal challenges associated with single-use plastics are constraining adoption in cost-sensitive emerging markets, limiting addressable market penetration by an estimated 8–12% in these regions.

- Opportunity: The expansion of cell and gene therapy (CGT) manufacturing represents an incremental addressable opportunity exceeding USD 3.8 Billion through 2034, as autologous and allogeneic therapy production requires flexible, batch-dedicated single-use assemblies.

- Trend: Integration of embedded sensors and real-time bioprocess analytics within single-use assemblies is gaining traction, with sensor-integrated products comprising approximately 18.5% of new product launches in 2025, up from 9.2% in 2021.

- Regional Analysis: North America leads the global single-use bioprocessing market with a 41.3% share in 2025, generating approximately USD 3.61 Billion in revenue, underpinned by the United States' dominant biopharmaceutical manufacturing base.

Competitive Landscape Overview

The single-use bioprocessing market is moderately consolidated, with the top four players — Sartorius AG, Thermo Fisher Scientific, Danaher Corporation (Cytiva), and Merck KGaA — collectively accounting for approximately 58.4% of global market revenue in 2025. Competition is primarily technology-driven, with suppliers differentiating on proprietary film formulations, connector standardization, and integrated digital bioprocess monitoring. Competitive intensity has increased as mid-tier players pursue acquisitions to broaden their portfolio scope and improve service coverage in high-growth geographies, particularly Asia Pacific and Latin America.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product | Geo Strength | Recent Strategic Move (2024–2026) |

| Sartorius AG | Germany | Leader | Biostat STR Bioreactor | Europe / Global | Jan 2025: Expanded single-use bioreactor manufacturing capacity in Germany by 35%, targeting mAb and CGT clients. |

| Thermo Fisher Scientific | USA | Leader | HyPerforma Single-Use Bioreactor | North America / Global | Mar 2025: Acquired a specialist single-use sensor firm to integrate PAT-ready analytics into its disposable bioreactor line. |

| Danaher (Cytiva) | USA | Leader | WAVE Bioreactor System | North America / Europe | Jun 2025: Launched a new single-use tangential flow filtration platform targeting downstream purification for gene therapy. |

| Merck KGaA | Germany | Leader | Mobius Single-Use Bioreactor | Europe / Asia Pacific | Sep 2025: Entered a strategic supply agreement with a major South Korea-based CDMO for multi-year single-use consumable supply. |

| Entegris | USA | Challenger | FlexForm Single-Use Bags | North America | Apr 2025: Unveiled improved low-extractable film for high-pH bioprocess applications, expanding addressable use cases. |

| Parker Hannifin (Bioscience) | USA | Challenger | Fulflex Single-Use Assemblies | North America / Europe | Feb 2026: Partnered with a European CDMO consortium to qualify its single-use flow path for advanced therapy applications. |

| Saint-Gobain Performance Plastics | France | Challenger | BioFluid Transfer Assemblies | Europe | Nov 2024: Launched a new silicone-free tubing product line addressing leachable reduction demands from CGT manufacturers. |

| Lonza Group | Switzerland | Niche Player | Ibex Single-Use Platform | Europe / Asia Pacific | Jan 2026: Expanded single-use manufacturing capacity at its Singapore facility by 40% to serve Asia Pacific CDMO demand. |

| Getinge AB | Sweden | Niche Player | Single-Use Mixing Systems | Europe | Jul 2025: Introduced a 2,000 L single-use mixing bag system targeting large-scale buffer preparation in commercial biomanufacturing. |

| Repligen Corporation | USA | Niche Player | XCell Single-Use ATF System | North America | May 2025: Secured FDA qualification for its single-use alternating tangential flow filtration system for perfusion bioreactors. |

By Product Type

The single-use bioprocessing market by product type is led by single-use bioreactors, which command approximately 32.4% of total market revenue in 2025, valued at USD 2.83 Billion. These disposable reactor systems — available in rocking-motion, stirred-tank, and wave formats — have replaced stainless steel fermenters for a growing share of clinical and commercial manufacturing runs. Their ability to support perfusion culture, reduce cleaning validation burden, and facilitate rapid changeover between biologic products makes them the preferred choice for multi-product manufacturing facilities. The 10 L to 2,000 L bioreactor segment is the most commercially active, with scale-up beyond 2,000 L gaining traction as polymer film and sensor technologies mature. Single-use bioreactors are growing at an estimated 12.1% CAGR through 2034, outpacing the overall market average, driven by CGT manufacturing and next-generation vaccine platforms.

Filtration and purification products, encompassing single-use tangential flow filtration (TFF) cassettes, depth filtration capsules, and sterile filtration assemblies, represent approximately 24.6% of market revenue in 2025, or USD 2.15 Billion. These components are embedded across downstream bioprocessing workflows for clarification, concentration, and buffer exchange. The replacement of regenerable ceramic or stainless-steel filter housings with disposable capsules eliminates regeneration validation steps and reduces inter-batch contamination risk. Demand from mAb and plasma protein fractionation manufacturers is particularly strong, with TFF cassette adoption growing at 11.3% annually.

Fluid management and storage products, including single-use bags, manifolds, and tubing assemblies, account for 21.8% of revenue in 2025 at USD 1.90 Billion. These foundational components facilitate buffer preparation, media storage, harvest pooling, and fill-finish transfer across all bioprocessing scales. Innovations in multi-layer film formulations, particularly those with reduced ethylene vinyl acetate (EVA) extractable profiles, are extending the applicability of single-use bags to high-pH and high-temperature processes previously dominated by stainless-steel vessels. Sensors and monitoring equipment within single-use formats, though nascent, represent 11.4% of revenue and are growing at the fastest rate — approximately 18.9% CAGR — as embedded optical pH, dissolved oxygen, and turbidity sensors achieve commercial maturity. Mixing systems and other accessories make up the remaining 9.8% of the product mix.

By Application

By application, monoclonal antibody production dominates the single-use bioprocessing market with a 38.2% revenue share in 2025, amounting to USD 3.34 Billion. The global mAb market has expanded substantially over the past decade, with over 160 approved mAb therapeutics commercially available and more than 600 in active clinical development as of 2025. Single-use systems are the default technology for clinical-stage mAb manufacturing and are increasingly adopted at commercial scale, as manufacturers value the reduced capital expenditure and lower contamination risk relative to traditional stainless-steel infrastructure. The mAb segment is expected to grow at a 10.4% CAGR through 2034, largely in step with the overall market.

Vaccine manufacturing accounts for 22.7% of single-use bioprocessing market revenue in 2025, representing USD 1.98 Billion. The COVID-19 pandemic permanently shifted vaccine manufacturing strategy toward single-use platforms, particularly for mRNA, viral vector, and recombinant subunit vaccine production. WHO and GAVI-supported capacity expansion programs in Africa and Southeast Asia are prioritizing single-use infrastructure to reduce facility construction costs and accelerate time-to-production. This segment is forecast to grow at 11.8% CAGR through 2034.

Cell and gene therapy manufacturing represents 16.4% of market revenue in 2025 at USD 1.43 Billion and is the fastest-growing application segment with a projected CAGR of 15.2% through 2034. CAR-T cell production, lentiviral and adeno-associated virus (AAV) vector manufacturing, and iPSC expansion workflows are heavily reliant on single-use assemblies due to their batch-dedicated nature. Each patient batch in autologous therapy production requires a new, sterile flow path, making single-use not merely preferred but functionally required. Recombinant proteins, plasma-derived products, and other biologics account for the remaining 22.7% of the application mix, with shares across these sub-segments approximately 14.1%, 5.9%, and 2.7% respectively.

By End-User

By end-user, biopharmaceutical manufacturers represent the largest purchaser segment within the single-use bioprocessing market, generating 48.6% of total revenue in 2025 at USD 4.25 Billion. Large integrated biopharmaceutical companies have adopted single-use across clinical supply and, increasingly, at commercial scale for early-launched biologics where dedicated manufacturing suites have not yet been constructed. CDMOs comprise the second-largest end-user segment at 31.4% of revenue or USD 2.74 Billion, reflecting the structural shift toward outsourced biomanufacturing. CDMOs operate multi-product facilities serving diverse client pipelines, making the flexibility of single-use systems operationally critical. Academic research institutes and contract research organizations (CROs) collectively account for approximately 14.8% of demand, while government and public health organizations make up the remaining 5.2%, largely through pandemic preparedness and vaccine manufacturing contracts.

Regional Analysis

North America Single-Use Bioprocessing Market

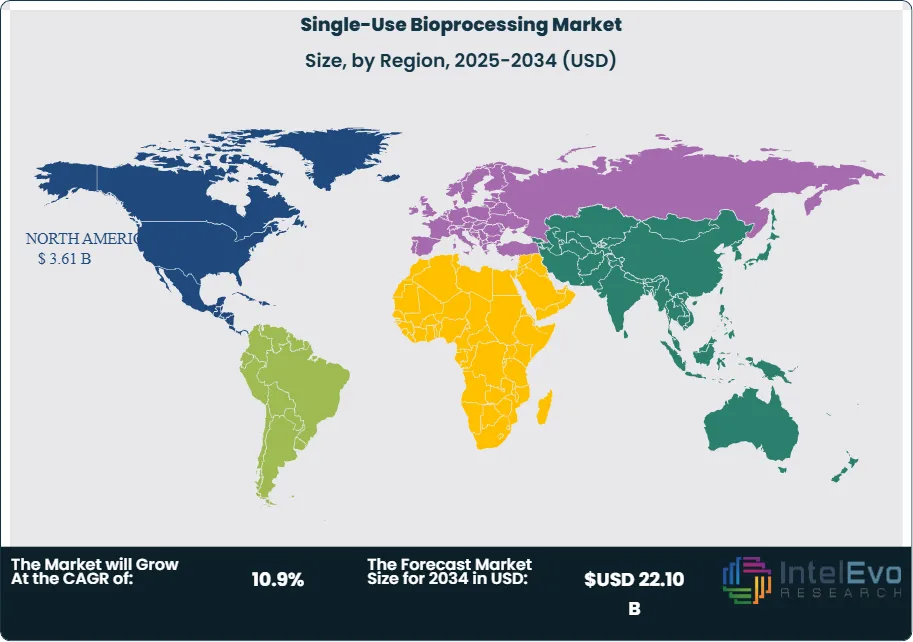

North America holds a dominant 41.3% share of the global single-use bioprocessing market in 2025, generating approximately USD 3.61 Billion in revenue. The United States is the primary driver, hosting the largest concentration of FDA-regulated biopharmaceutical manufacturers, CDMOs, and CGT developers globally. The Inflation Reduction Act's provisions affecting biologic drug pricing have prompted some manufacturers to defer commercial-scale stainless-steel facility investments, channeling capital toward more flexible single-use production models. Major CDMO campuses across New Jersey, Massachusetts, North Carolina, and California are investing heavily in multi-suite single-use facilities to meet outsourced biologics demand. Canada contributes meaningfully through its national biomanufacturing strategy, which has allocated significant public funding to build domestic single-use bioreactor capacity. The single-use bioprocessing market in North America is projected to grow at a 10.2% CAGR through 2034, reaching approximately USD 8.94 Billion.

Europe Single-Use Bioprocessing Market

Europe accounts for 28.6% of the single-use bioprocessing market in 2025, equivalent to USD 2.50 Billion in revenue. Germany, Switzerland, and Ireland are the anchor markets, collectively hosting several of the world's largest biopharmaceutical production sites and CDMO campuses. The EMA's progressive stance on continuous manufacturing and flexible production technologies has reinforced European manufacturers' appetite for single-use adoption. The United Kingdom, post-Brexit, has maintained its status as a gene therapy manufacturing hub, with several academic-commercial partnerships driving single-use CGT infrastructure investments. French biopharma groups and Nordic life sciences firms are also increasing single-use procurement. Environmental regulations in the EU targeting plastic waste are prompting suppliers to develop recyclable and bio-based single-use film alternatives, which is expected to become a competitive differentiator for European procurement teams by 2027. Europe's single-use bioprocessing market is expected to grow at a 10.5% CAGR through 2034.

Asia Pacific Single-Use Bioprocessing Market

Asia Pacific represents 20.8% of the global single-use bioprocessing market in 2025 at USD 1.82 Billion and is the fastest-growing region with a projected CAGR of 13.4% through 2034. China's biopharmaceutical sector has undergone structural transformation following NMPA regulatory reforms aligning approval pathways with ICH guidelines, significantly increasing domestic biologics output and the supporting demand for single-use manufacturing equipment. South Korea has emerged as a major CDMO powerhouse, with Samsung Biologics and Celltrion operating some of the largest biologics manufacturing facilities globally — facilities that increasingly incorporate single-use components in clinical and early commercial production. India's CDMO sector, supported by the Production Linked Incentive (PLI) scheme for pharmaceuticals, is building single-use bioprocessing capacity to capture CDMO contracts from global biopharma firms seeking geographic diversification. Japan's well-established biopharmaceutical sector contributes to regional demand, particularly through cell therapy manufacturing investments.

Latin America Single-Use Bioprocessing Market

Latin America holds a 5.8% share of the single-use bioprocessing market in 2025, valued at approximately USD 0.51 Billion. Brazil is the largest market in the region, supported by ANVISA-regulated biopharmaceutical production and government efforts to localize biosimilar and vaccine manufacturing. Fiocruz, Brazil's leading public health biotech institution, has committed to single-use bioprocessing infrastructure as part of its expanded vaccine production mandate. Mexico benefits from proximity to the United States pharmaceutical supply chain and hosts a growing number of CDMO facilities supplying North American clients. Argentina's biopharmaceutical sector, though smaller, has seen targeted investment from domestic biologics developers. The region faces structural constraints including import duties on single-use components and limited local supplier presence, but these are partially offset by multilateral health institution investments supporting biomanufacturing capacity. Latin America's market is projected to grow at a 9.8% CAGR through 2034.

Middle East & Africa Single-Use Bioprocessing Market

The Middle East and Africa (MEA) region accounts for 3.5% of global single-use bioprocessing market revenue in 2025 at USD 0.31 Billion. The UAE and Saudi Arabia are the primary markets, where Vision 2030 and national health strategies are channeling investment into domestic biopharmaceutical manufacturing and local vaccine production capabilities. The Serum Institute of Africa and similar public-private manufacturing initiatives across sub-Saharan Africa are prioritizing single-use infrastructure for vaccine production, supported by funding from GAVI and the African Vaccine Manufacturing Accelerator (AVMA). South Africa's established pharmaceutical sector and clinical trial infrastructure provide a foundation for single-use adoption in research and commercial settings. MEA's single-use bioprocessing market is forecast to grow at a 11.2% CAGR through 2034, the second-fastest regional growth rate, as healthcare investment and domestic biomanufacturing ambitions intensify across the Gulf Cooperation Council (GCC) and key African economies.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Single-Use Bioreactors

- Filtration & Purification Products

- Fluid Management & Storage (Bags, Manifolds, Tubing)

- Sensors & Monitoring Equipment

- Mixing Systems & Other Accessories

By Application

- Monoclonal Antibody (mAb) Production

- Vaccine Manufacturing

- Cell & Gene Therapy Manufacturing

- Recombinant Protein Production

- Plasma-Derived Products & Other Biologics

By End-User

- Biopharmaceutical Manufacturers

- Contract Development & Manufacturing Organizations (CDMOs)

- Academic Research Institutes & CROs

- Government & Public Health Organizations

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.74 B |

| Forecast Revenue (2034) | USD 22.10 B |

| CAGR (2025-2034) | 10.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Single-Use Bioreactors, Filtration & Purification Products, Fluid Management & Storage (Bags, Manifolds, Tubing), Sensors & Monitoring Equipment, Mixing Systems & Other Accessories), By Application, (Monoclonal Antibody (mAb) Production, Vaccine Manufacturing, Cell & Gene Therapy Manufacturing, Recombinant Protein Production, Plasma-Derived Products & Other Biologics), By End-User, (Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Academic Research Institutes & CROs, Government & Public Health Organizations) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SARTORIUS AG, THERMO FISHER SCIENTIFIC, DANAHER CORPORATION (CYTIVA), MERCK KGAA (LIFE SCIENCE / MILLIPORESIGMA), ENTEGRIS, PARKER HANNIFIN (BIOSCIENCE DIVISION), SAINT-GOBAIN PERFORMANCE PLASTICS, LONZA GROUP, GETINGE AB, REPLIGEN CORPORATION, PALL CORPORATION (DANAHER), 3M COMPANY (SEPARATION & PURIFICATION SCIENCES), COBETTER FILTRATION, MEISSNER FILTRATION PRODUCTS, GORE (W.L. GORE & ASSOCIATES), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (mAb Production, Vaccine Manufacturing, Cell & Gene Therapy, Recombinant Proteins, Plasma Products), By End-User (Biopharma, CDMOs, CROs) Industry Trends & Forecast 2026–2034")

, By Application (mAb Production, Vaccine Manufacturing, Cell & Gene Therapy, Recombinant Proteins, Plasma Products), By End-User (Biopharma, CDMOs, CROs) Industry Trends & Forecast 2026–2034")

, By Application (mAb Production, Vaccine Manufacturing, Cell & Gene Therapy, Recombinant Proteins, Plasma Products), By End-User (Biopharma, CDMOs, CROs) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Single-Use Bioprocessing Market?

Global Single-use bioprocessing market valued at USD 7.88B in 2024, reaching USD 22.10B by 2034, growing at a CAGR of 10.9% from 2026–2034.

Who are the major players in the Single-Use Bioprocessing Market?

SARTORIUS AG, THERMO FISHER SCIENTIFIC, DANAHER CORPORATION (CYTIVA), MERCK KGAA (LIFE SCIENCE / MILLIPORESIGMA), ENTEGRIS, PARKER HANNIFIN (BIOSCIENCE DIVISION), SAINT-GOBAIN PERFORMANCE PLASTICS, LONZA GROUP, GETINGE AB, REPLIGEN CORPORATION, PALL CORPORATION (DANAHER), 3M COMPANY (SEPARATION & PURIFICATION SCIENCES), COBETTER FILTRATION, MEISSNER FILTRATION PRODUCTS, GORE (W.L. GORE & ASSOCIATES), Others

Which segments covered the Single-Use Bioprocessing Market?

By Product Type, (Single-Use Bioreactors, Filtration & Purification Products, Fluid Management & Storage (Bags, Manifolds, Tubing), Sensors & Monitoring Equipment, Mixing Systems & Other Accessories), By Application, (Monoclonal Antibody (mAb) Production, Vaccine Manufacturing, Cell & Gene Therapy Manufacturing, Recombinant Protein Production, Plasma-Derived Products & Other Biologics), By End-User, (Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Academic Research Institutes & CROs, Government & Public Health Organizations)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Single-Use Bioprocessing Market

Published Date : 30 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date