- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global siRNA Therapeutics Market Forecast 2034 | CAGR 15.8%

Global Small Interfering RNA (siRNA) Therapeutics Market Size, Share, Growth & Industry Analysis By Delivery Technology (GalNAc-Conjugated siRNA, Lipid Nanoparticle (LNP)-Formulated siRNA, Polymer Conjugates, Others), By Therapeutic Area (Rare Genetic Diseases, Cardiovascular & Metabolic Diseases, Infectious Diseases, Oncology, Others), By Route of Administration (Subcutaneous, Intravenous, Intravitreal), By End User (Hospitals, Pharmacies, Clinics, Research Institutes) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 3.8 Billion | USD 14.2 Billion | 15.8% | North America, 46.8% |

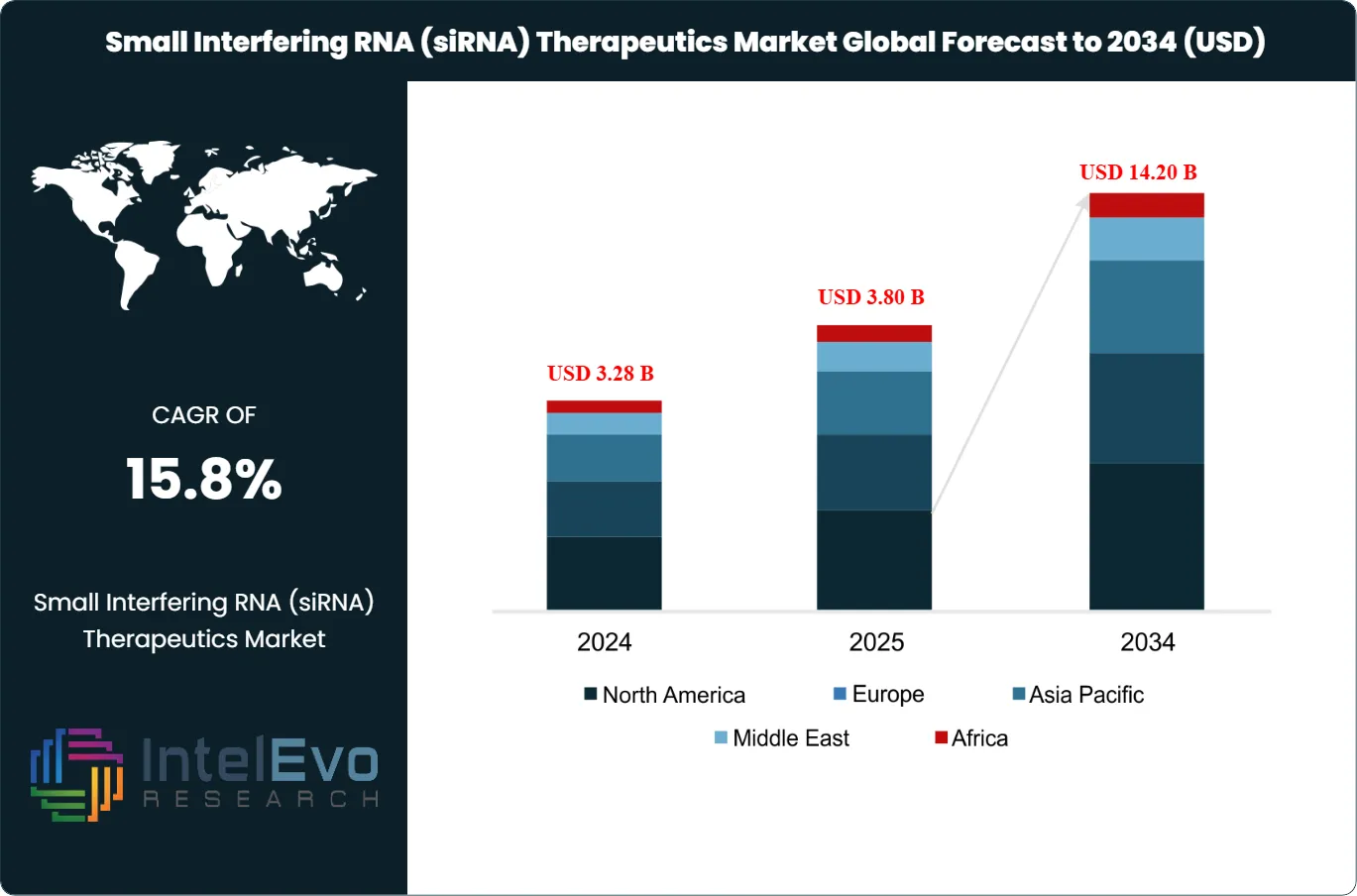

The Small Interfering RNA (siRNA) Therapeutics Market was valued at approximately USD 3.28 Billion in 2024 and reached USD 3.80 Billion in 2025. The market is projected to grow to USD 14.20 Billion by 2034, expanding at a CAGR of 15.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 10.4 Billion over the analysis period. Small interfering RNA (siRNA) therapeutics have emerged as the fastest-growing oligonucleotide modality, leveraging the RNA interference (RNAi) pathway to achieve highly specific and potent gene silencing. These double-stranded RNA molecules, typically 21-23 nucleotides in length, trigger sequence-specific degradation of complementary mRNA through the RISC complex mechanism, enabling precision targeting of disease-causing genes.

Get More Information about this report -

Request Free Sample ReportThe small interfering RNA therapeutics market has achieved rapid commercial validation following FDA approvals of five siRNA products between 2018 and 2025. Alnylam Pharmaceuticals has pioneered this modality with patisiran (Onpattro), givosiran (Givlaari), lumasiran (Oxlumo), inclisiran (Leqvio), and vutrisiran (Amvuttra) addressing hereditary transthyretin amyloidosis, acute hepatic porphyria, primary hyperoxaluria, hypercholesterolemia, and ATTR polyneuropathy respectively. Combined commercial revenue from approved siRNA therapies exceeded USD 2.4 Billion in 2025, representing the majority of current market value. The clinical pipeline contains over 95 siRNA candidates in active development across rare diseases, cardiovascular, metabolic, infectious disease, and oncology therapeutic areas.

GalNAc conjugation technology has transformed siRNA therapeutic profiles by enabling subcutaneous administration with extended dosing intervals ranging from monthly to every six months. Alnylam's Enhanced Stabilization Chemistry (ESC) combined with GalNAc targeting has improved potency 20-30 fold relative to first-generation lipid nanoparticle formulations. ICH guidelines (S6R1, Q6B) provide standardized regulatory requirements for oligonucleotide quality and safety assessment. FDA Breakthrough Therapy Designations have been granted to over 15 siRNA programs since 2018, accelerating development timelines. North America dominates with 46.8% market share driven by Alnylam's commercial leadership, robust specialty pharmacy infrastructure, and favorable reimbursement pathways for genetic medicines. Asia Pacific represents the fastest-growing region at 18.4% CAGR as regulatory harmonization and manufacturing capacity expansion accelerate market penetration.

Therapeutics Market Size, Share, Growth & Industry Analysis By Delivery Technology (GalNAc-Conjugated siRNA, Lipid Nanoparticle (LNP)-Formulated siRNA, Polymer Conjugates, Others), By Therapeutic Area (Rare Genetic Diseases, Cardiovascular & Metabolic Diseases, Infectious Diseases, Oncology, Others), By Route of Administration (Subcutaneous, Intravenous, Intravitreal), By End User (Hospitals, Pharmacies, Clinics, Research Institutes) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The small interfering RNA therapeutics market grows from USD 3.8 Billion in 2025 to USD 14.2 Billion by 2034, registering a CAGR of 15.8% across the forecast period 2026–2034.

- Segment Dominance: GalNAc-conjugated siRNA leads the market by delivery technology at 72.4% share in 2025, driven by five FDA-approved products and over 60 clinical-stage programs utilizing this platform.

- Segment Dominance: Rare genetic diseases represent the largest therapeutic application at 48.6% market share in 2025, anchored by approved products for hATTR, AHP, and PH1 generating combined revenue exceeding USD 1.6 Billion.

- Driver: Commercial success of approved siRNA products validates the modality with 94% patient adherence rates and 85% reduction in disease biomarkers demonstrated across approved indications.

- Restraint: High therapy costs limit market penetration with annual treatment expenses ranging from USD 200,000 to USD 450,000 per patient. Payer prior authorization adds 35 days average delay to treatment initiation.

- Opportunity: Cardiometabolic expansion presents a USD 5.8 Billion opportunity by 2034. Phase III programs targeting Lp(a), ANGPTL3, and APOC3 address patient populations exceeding 100 million globally.

- Trend: Extended dosing intervals have achieved 6-month administration schedules for certain siRNA therapies, with 88% of new clinical programs targeting quarterly or less frequent dosing.

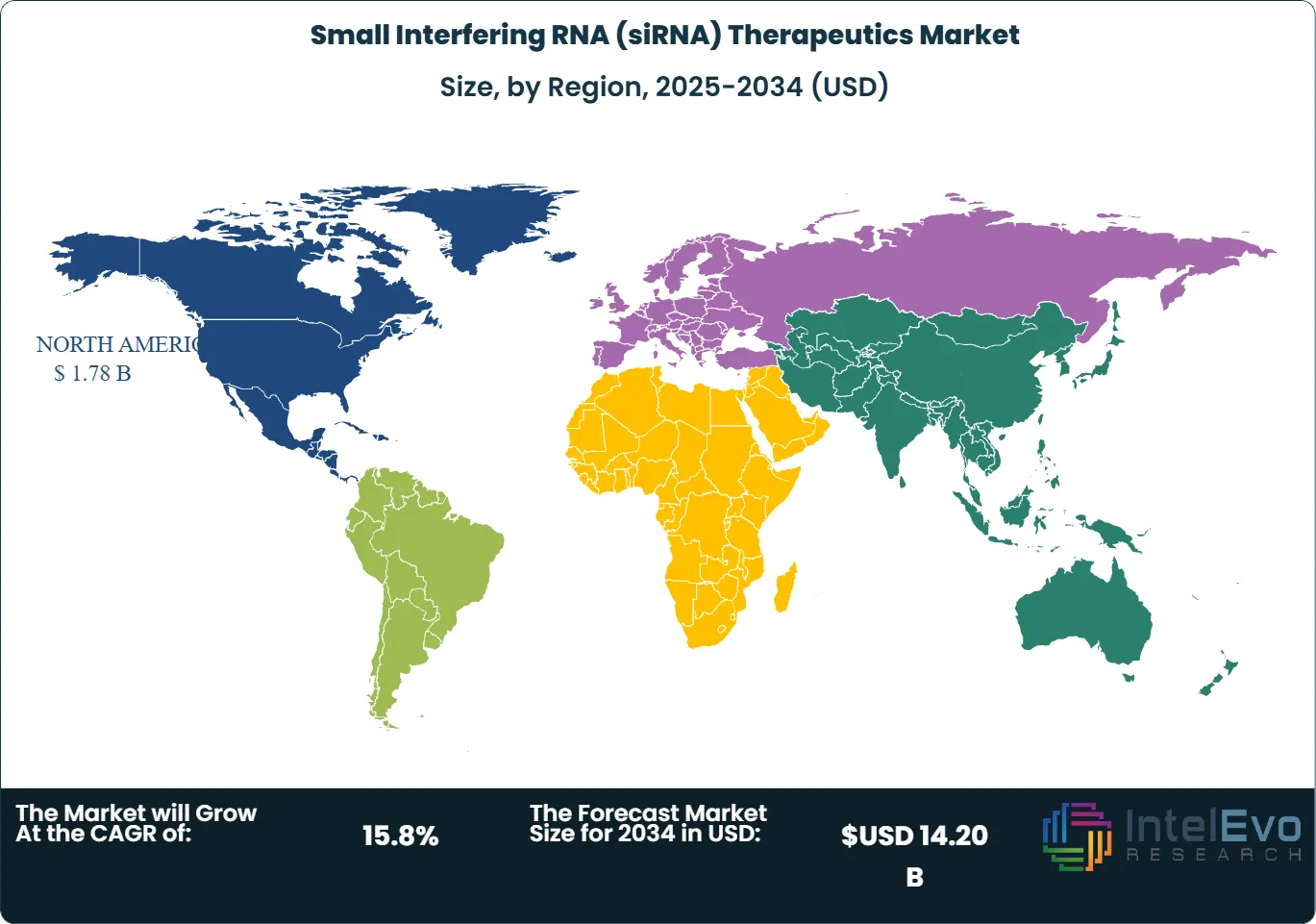

- Regional Analysis: North America commands 46.8% market share valued at USD 1.78 Billion in 2025, driven by Alnylam's commercial portfolio and favorable FDA regulatory pathways for genetic medicines.

Competitive Landscape Overview

The small interfering RNA therapeutics market exhibits high consolidation with the top four companies controlling approximately 82% of global revenue in 2025. Alnylam Pharmaceuticals dominates with over 62% market share through five FDA-approved products and the most extensive siRNA pipeline globally. Competition centers on therapeutic area expansion, delivery platform innovation, and extra-hepatic targeting capabilities. Strategic partnerships between siRNA platform companies and large pharmaceutical partners have defined competitive dynamics, with cumulative deal values exceeding USD 12 Billion since 2020. Novartis commercializes inclisiran (Leqvio) through licensing agreement with Alnylam, while Arrowhead Pharmaceuticals and Silence Therapeutics advance differentiated siRNA platforms toward late-stage development.

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| Alnylam Pharmaceuticals | US | Leader | Onpattro (patisiran) | North America | FDA sNDA filed for vutrisiran ATTR cardiomyopathy (Dec 2024) |

| Arrowhead Pharmaceuticals | US | Challenger | Plozasiran (Phase III) | North America | Completed Phase III SHASTA-2 for hypertriglyceridemia (Mar 2025) |

| Novartis | Switzerland | Leader | Leqvio (inclisiran) | Global | Achieved USD 1B cumulative inclisiran revenue (Sep 2025) |

| Silence Therapeutics | UK | Challenger | Zerlasiran (Lp(a)) | Europe | Initiated Phase III ALLEVIATE-HF cardiovascular trial (Jan 2026) |

| Amgen | US | Challenger | Olpasiran (Lp(a)) | North America | Phase III OCEAN(a)-Outcomes trial enrollment (Jun 2025) |

| Dicerna (Novo Nordisk) | US | Challenger | Nedosiran (PH) | Global | Integrated siRNA platform into Novo Nordisk cardiometabolic R&D (Apr 2025) |

| GSK | UK | Challenger | Bepirovirsen (HBV) | Europe | Phase III HBV functional cure results reported (Feb 2026) |

| Janssen | US | Niche Player | JNJ-3989 (HBV) | North America | Expanded HBV combination therapy trials (Aug 2025) |

| Sirnaomics | China | Niche Player | STP705 (oncology) | Asia Pacific | Initiated Phase IIb for squamous cell carcinoma (May 2025) |

| Arcturus Therapeutics | US | Niche Player | LUNAR-OTC | North America | Advanced mRNA/siRNA platform for liver diseases (Jul 2025) |

By Delivery Technology

GalNAc-conjugated siRNA dominates the market by delivery technology at 72.4% share valued at USD 2.75 Billion in 2025. N-acetylgalactosamine (GalNAc) conjugation enables hepatocyte-specific uptake through asialoglycoprotein receptor (ASGPR) binding, achieving highly efficient liver targeting without lipid nanoparticle formulation. Five FDA-approved siRNA products utilize GalNAc conjugation: givosiran, lumasiran, inclisiran, and vutrisiran from Alnylam's portfolio. The technology enables subcutaneous self-administration with dosing intervals extending from monthly to every six months. Over 60 clinical-stage siRNA programs employ GalNAc delivery, representing 88% of the active siRNA pipeline for hepatic indications. Manufacturing simplicity compared to LNP formulations reduces production costs by approximately 30% and eliminates cold chain requirements for certain products.

Lipid nanoparticle (LNP)-formulated siRNA represents 22.8% market share at USD 0.87 Billion in 2025. Patisiran (Onpattro), the first FDA-approved siRNA therapy (2018), established the LNP delivery platform for hereditary transthyretin amyloidosis. LNP encapsulation protects siRNA from degradation and facilitates endosomal escape for cytoplasmic delivery. The technology enables broader tissue distribution beyond hepatocyte-specific GalNAc targeting. Intravenous administration requires healthcare facility infusion with premedication protocols to manage infusion-related reactions. Development focus has shifted toward GalNAc alternatives for liver indications, though LNP platforms maintain relevance for extra-hepatic targeting in oncology and other therapeutic areas. Other delivery technologies including polymer conjugates and exosome-based systems account for the remaining 4.8% market share.

By Therapeutic Area

Rare genetic diseases lead therapeutic applications for the small interfering RNA therapeutics market at 48.6% share valued at USD 1.85 Billion in 2025. Hereditary transthyretin amyloidosis (hATTR) treatment with patisiran and vutrisiran generates combined annual revenue exceeding USD 1.1 Billion. Acute hepatic porphyria treatment with givosiran and primary hyperoxaluria type 1 treatment with lumasiran address additional rare disease populations. Orphan Drug Act incentives including seven-year market exclusivity and FDA fee waivers have accelerated rare disease siRNA development. The pipeline contains over 35 siRNA candidates targeting rare metabolic, hematologic, and hepatic conditions. Patient identification through expanded genetic testing has increased diagnosed populations by 180% since 2018 for hATTR alone.

Cardiovascular and metabolic diseases account for 32.4% market share at USD 1.23 Billion in 2025. Inclisiran (Leqvio) targeting PCSK9 for hypercholesterolemia generates annual revenue exceeding USD 620 million globally, demonstrating siRNA viability for common chronic diseases. Twice-yearly dosing administered by healthcare providers offers differentiated convenience versus daily oral statins or biweekly injectable PCSK9 antibodies. Phase III programs targeting lipoprotein(a), ANGPTL3, and APOC3 address dyslipidemia patient populations exceeding 100 million globally. Cardiovascular expansion positions siRNA technology for significantly larger markets than traditional rare disease applications. The segment grows at 22.4% CAGR through 2034, faster than the overall market.

Infectious diseases represent 10.8% market share at USD 0.41 Billion in 2025. Hepatitis B virus (HBV) functional cure programs represent the largest infectious disease opportunity, with over 290 million people living with chronic HBV globally. siRNA candidates targeting HBsAg, HBV polymerase, and viral cccDNA have advanced to Phase II and Phase III development. Arrowhead Pharmaceuticals, Janssen, and GSK maintain active HBV siRNA programs. Combination approaches with other antiviral modalities aim for functional cure defined as sustained HBsAg loss without ongoing treatment. Oncology represents 5.4% share at USD 0.21 Billion, with siRNA approaches targeting KRAS, MYC, and other validated cancer genes. Delivery to solid tumors remains challenging, driving development of antibody-siRNA conjugates and tumor-targeted nanoparticles. Other therapeutic areas account for the remaining 2.8% share.

By Route of Administration

Subcutaneous injection leads the small interfering RNA therapeutics market by administration route at 68.4% share valued at USD 2.60 Billion in 2025. GalNAc conjugation technology has enabled subcutaneous delivery for all liver-targeted siRNA therapies approved since 2019. Self-administration at home or clinic-based dosing provides significant convenience advantages over intravenous alternatives requiring healthcare facility visits. Dosing intervals range from monthly (givosiran, lumasiran) to every six months (vutrisiran), with quarterly dosing (inclisiran) representing the most common regimen. Patient preference studies demonstrate 92% satisfaction rates with subcutaneous siRNA administration. The route dominates cardiovascular, metabolic, and hepatic siRNA programs where liver-expressed targets drive disease pathology.

Intravenous infusion accounts for 28.2% market share at USD 1.07 Billion in 2025. Patisiran (Onpattro) remains the primary IV-administered siRNA therapy, requiring infusion every three weeks in healthcare settings. LNP-formulated siRNA products necessitate premedication with corticosteroids, antihistamines, and acetaminophen to manage infusion-related reactions occurring in approximately 20% of patients. The route enables broader tissue distribution for indications requiring systemic exposure beyond hepatocytes. Development focus has shifted toward subcutaneous alternatives, though IV delivery persists for oncology applications and certain rare disease programs. Vutrisiran (Amvuttra), a subcutaneous GalNAc-conjugated alternative to patisiran for hATTR, has captured significant market share since approval in 2022. Other routes including intravitreal for ophthalmology applications represent the remaining 3.4% share.

By End User

Specialty pharmacies dominate the small interfering RNA therapeutics market by end user at 52.6% share valued at USD 2.00 Billion in 2025. Limited distribution networks restrict siRNA access to designated specialty pharmacy partners ensuring proper handling, patient education, and adherence monitoring. Hub service models coordinate among prescribers, payers, and pharmacies to facilitate prior authorization, benefits investigation, and treatment initiation. Cold chain management for LNP-formulated products and proper storage for GalNAc-conjugated therapies require specialized distribution capabilities. Patient support programs operated through specialty pharmacies have achieved 94% treatment persistence at 12 months for chronic siRNA therapies. Alnylam's Alnylam Assist and Novartis's Leqvio patient support programs provide comprehensive access services.

Hospitals represent 34.8% market share at USD 1.32 Billion in 2025. Academic medical centers and specialty hospitals provide infrastructure for intravenous siRNA infusion, rare disease diagnosis, and complex patient monitoring. Cardiology and hepatology departments have concentrated expertise in inclisiran and hATTR treatment respectively. Hospital pharmacy formulary decisions drive institutional access, with value-based contracts linking reimbursement to clinical outcomes. Integrated delivery networks negotiate pricing with manufacturers. Clinics and physician offices account for 9.4% market share at USD 0.36 Billion, growing fastest as subcutaneous siRNA therapies with infrequent dosing expand into primary care and cardiology office settings. Research institutions represent the remaining 3.2% share.

Regional Analysis

North America Small Interfering RNA Therapeutics Market

North America commands 46.8% of the global small interfering RNA therapeutics market, valued at USD 1.78 Billion in 2025. The United States represents 93% of regional revenue at USD 1.66 Billion, establishing clear dominance through Alnylam Pharmaceuticals' commercial leadership and favorable FDA regulatory pathways. Alnylam (Cambridge, Massachusetts) has built the only approved siRNA portfolio globally with five FDA-approved products generating combined revenue exceeding USD 2.1 Billion in 2025. Arrowhead Pharmaceuticals (Pasadena, California) and Dicerna Pharmaceuticals (now part of Novo Nordisk) contribute additional siRNA pipeline assets advancing toward commercialization.

FDA regulatory frameworks provide multiple expedited pathways accelerating siRNA development. Breakthrough Therapy Designation has been granted to over 15 siRNA programs, enabling intensive FDA guidance and rolling review. Accelerated Approval based on biomarker endpoints facilitated early market access for rare disease siRNA therapies. The Inflation Reduction Act's orphan drug exemption from Medicare price negotiation preserves economic incentives for rare disease development through 2028. Specialty pharmacy infrastructure supporting high-cost therapies and established patient access programs facilitate commercial uptake. Alnylam's manufacturing facility in Norton, Massachusetts provides dedicated siRNA production capacity. Canada contributes USD 120 million in 2025 market value with regulatory alignment through Health Canada's Notice of Compliance process.

Europe Small Interfering RNA Therapeutics Market

Europe accounts for 30.2% market share valued at USD 1.15 Billion in 2025 for small interfering RNA therapeutics. Germany leads regional adoption at USD 310 million (27.0% of Europe), driven by strong specialty pharmacy infrastructure and SHI coverage decisions for genetic medicines. Novartis commercializes inclisiran (Leqvio) aggressively in European markets through its cardiovascular commercial organization. The UK market at USD 245 million benefits from NHS England's managed access agreements providing early patient access while generating real-world evidence. France at USD 195 million maintains centralized HTA evaluation through Haute Autorite de Sante determining pricing and reimbursement.

European Medicines Agency (EMA) centralized marketing authorization provides single approval across 27 EU member states plus EEA countries. Conditional Marketing Authorization has enabled earlier access for siRNA therapies addressing unmet medical needs. The EMA has developed assessment expertise for RNA therapeutics through multiple approval procedures since 2018. Italy and Spain collectively represent USD 265 million in 2025 market value with national pricing negotiations following EMA approval. Silence Therapeutics (London, UK) contributes European siRNA innovation with its mRNAi GOLD platform advancing cardiovascular programs to late-stage development. Contract manufacturing capacity in Ireland and Switzerland supports global siRNA supply chains.

Asia Pacific Small Interfering RNA Therapeutics Market

Asia Pacific represents 16.4% market share valued at USD 0.62 Billion in 2025, positioned as the fastest-growing region at 18.4% CAGR through 2034 for the small interfering RNA therapeutics market. Japan contributes USD 265 million (42.7% of regional revenue) with advanced regulatory frameworks and high willingness-to-pay for genetic medicines. PMDA has approved multiple siRNA therapies and developed assessment pathways aligning with ICH guidelines. Japanese pharmaceutical companies including Takeda have established siRNA development capabilities through licensing agreements with Alnylam and other platform companies.

China's siRNA market reaches USD 185 million in 2025 with 22.6% growth projected annually through 2034. NMPA regulatory reforms have accelerated approval timelines with conditional approval pathways available for therapies addressing unmet needs. Domestic companies including Sirnaomics and RiboBio are advancing proprietary siRNA pipelines targeting Chinese patient populations. Contract manufacturing capacity expansion in Suzhou and Shanghai positions China as an emerging siRNA synthesis hub. South Korea contributes USD 92 million with Samsung Biologics investing in nucleic acid manufacturing capabilities alongside domestic biotech innovation. India at USD 48 million serves primarily as a CDMO destination. Australia rounds out regional activity with USD 32 million in market value.

Latin America Small Interfering RNA Therapeutics Market

Latin America holds 3.8% market share valued at USD 0.14 Billion in 2025 for small interfering RNA therapeutics. Brazil dominates regional activity at USD 78 million (55.7% of Latin America), serving as the primary market entry point for specialty pharmaceutical products. ANVISA regulatory pathways incorporate expedited review for rare disease therapies, with patisiran and inclisiran approved following reference to FDA and EMA procedures. The Brazilian Unified Health System (SUS) evaluates siRNA therapies through CONITEC technology assessment.

Mexico contributes USD 38 million with proximity to US pharmaceutical supply chains facilitating product access. COFEPRIS regulatory alignment with FDA procedures enables technology transfer. Argentina at USD 16 million maintains limited siRNA access concentrated in Buenos Aires metropolitan specialty centers. Colombia and Chile collectively represent the remainder of regional activity with emerging specialty care capabilities. Regional growth at 14.2% CAGR through 2034 remains constrained by limited specialty pharmacy infrastructure and reimbursement frameworks for high-cost genetic medicines. Novartis cardiovascular commercial presence supports inclisiran market development across the region.

Middle East & Africa Small Interfering RNA Therapeutics Market

Middle East & Africa accounts for 2.8% market share valued at USD 0.11 Billion in 2025 for the small interfering RNA therapeutics market. The United Arab Emirates leads regional adoption at USD 35 million, driven by Dubai Healthcare City and Abu Dhabi's advanced healthcare infrastructure. UAE genetic medicine access programs have facilitated siRNA therapy availability for Emirati citizens. Saudi Arabia contributes USD 32 million with Vision 2030 healthcare investments prioritizing specialty center development.

Israel at USD 24 million benefits from advanced biotechnology capabilities and regulatory alignment with European systems. South Africa represents the primary sub-Saharan market at USD 12 million, with specialty pharmaceutical distribution limited to major metropolitan centers. High therapy costs relative to regional healthcare budgets constrain broader market penetration. Regional growth at 15.2% CAGR through 2034 reflects healthcare modernization investments in Gulf Cooperation Council countries, though access disparities persist across the broader MEA region. Inclisiran cardiovascular launch represents the primary commercial opportunity for market expansion.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Delivery Technology

- GalNAc-Conjugated siRNA

- Lipid Nanoparticle (LNP)-Formulated siRNA

- Polymer Conjugates

- Others

By Therapeutic Area

- Rare Genetic Diseases

- Cardiovascular and Metabolic Diseases

- Infectious Diseases

- Oncology

- Others

By Route of Administration

- Subcutaneous Injection

- Intravenous Infusion

- Intravitreal Injection

- Others

By End User

- Specialty Pharmacies

- Hospitals

- Clinics and Physician Offices

- Research Institutions

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.80 B |

| Forecast Revenue (2034) | USD 14.20 B |

| CAGR (2025-2034) | 15.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Delivery Technology, (GalNAc-Conjugated siRNA, Lipid Nanoparticle (LNP)-Formulated siRNA, Polymer Conjugates, Others), By Therapeutic Area, (Rare Genetic Diseases, Cardiovascular and Metabolic Diseases, Infectious Diseases, Oncology, Others), By Route of Administration, (Subcutaneous Injection, Intravenous Infusion, Intravitreal Injection, Others), By End User, (Specialty Pharmacies, Hospitals, Clinics and Physician Offices, Research Institutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ALNYLAM PHARMACEUTICALS, ARROWHEAD PHARMACEUTICALS, NOVARTIS, SILENCE THERAPEUTICS, DICERNA PHARMACEUTICALS (NOVO NORDISK), SIRNAOMICS, ARCTURUS THERAPEUTICS, GSK, JANSSEN (JOHNSON & JOHNSON), AMGEN, ASTRAZENECA, REGENERON PHARMACEUTICALS, TAKEDA, ROCHE, OLX PHARMACEUTICALS, RIBOCURE PHARMACEUTICALS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Therapeutics Market Size, Share, Growth & Industry Analysis By Delivery Technology (GalNAc-Conjugated siRNA, Lipid Nanoparticle (LNP)-Formulated siRNA, Polymer Conjugates, Others), By Therapeutic Area (Rare Genetic Diseases, Cardiovascular & Metabolic Diseases, Infectious Diseases, Oncology, Others), By Route of Administration (Subcutaneous, Intravenous, Intravitreal), By End User (Hospitals, Pharmacies, Clinics, Research Institutes) Industry Trends & Forecast 2026–2034")

Therapeutics Market Size, Share, Growth & Industry Analysis By Delivery Technology (GalNAc-Conjugated siRNA, Lipid Nanoparticle (LNP)-Formulated siRNA, Polymer Conjugates, Others), By Therapeutic Area (Rare Genetic Diseases, Cardiovascular & Metabolic Diseases, Infectious Diseases, Oncology, Others), By Route of Administration (Subcutaneous, Intravenous, Intravitreal), By End User (Hospitals, Pharmacies, Clinics, Research Institutes) Industry Trends & Forecast 2026–2034")

Therapeutics Market Size, Share, Growth & Industry Analysis By Delivery Technology (GalNAc-Conjugated siRNA, Lipid Nanoparticle (LNP)-Formulated siRNA, Polymer Conjugates, Others), By Therapeutic Area (Rare Genetic Diseases, Cardiovascular & Metabolic Diseases, Infectious Diseases, Oncology, Others), By Route of Administration (Subcutaneous, Intravenous, Intravitreal), By End User (Hospitals, Pharmacies, Clinics, Research Institutes) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Small Interfering RNA (siRNA) Therapeutics Market?

Global siRNA therapeutics market valued at USD 3.28B in 2024, reaching USD 14.2B by 2034, growing at a CAGR of 15.8% from 2026–2034.

Who are the major players in the Small Interfering RNA (siRNA) Therapeutics Market?

ALNYLAM PHARMACEUTICALS, ARROWHEAD PHARMACEUTICALS, NOVARTIS, SILENCE THERAPEUTICS, DICERNA PHARMACEUTICALS (NOVO NORDISK), SIRNAOMICS, ARCTURUS THERAPEUTICS, GSK, JANSSEN (JOHNSON & JOHNSON), AMGEN, ASTRAZENECA, REGENERON PHARMACEUTICALS, TAKEDA, ROCHE, OLX PHARMACEUTICALS, RIBOCURE PHARMACEUTICALS, Others

Which segments covered the Small Interfering RNA (siRNA) Therapeutics Market?

By Delivery Technology, (GalNAc-Conjugated siRNA, Lipid Nanoparticle (LNP)-Formulated siRNA, Polymer Conjugates, Others), By Therapeutic Area, (Rare Genetic Diseases, Cardiovascular and Metabolic Diseases, Infectious Diseases, Oncology, Others), By Route of Administration, (Subcutaneous Injection, Intravenous Infusion, Intravitreal Injection, Others), By End User, (Specialty Pharmacies, Hospitals, Clinics and Physician Offices, Research Institutions)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Small Interfering RNA (siRNA) Therapeutics Market

Published Date : 10 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date