- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Smart Contact Lens Market Size, Share & Forecast | CAGR 25.2%

Global Smart Contact Lens Market Size, Share, Growth Analysis By Product Type (Diagnostic & Monitoring Smart Lenses, AR & Display Smart Lenses, Drug Delivery Smart Lenses, Vision Correction Smart Lenses), By Application (Healthcare Monitoring, Consumer Electronics & AR, Sports & Defense), By Technology (Sensor-Integrated Lenses, Passive Smart Lenses), By End-User, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

| USD 1.12 Billion | USD 8.47 Billion | 25.2% | North America, 38.4% |

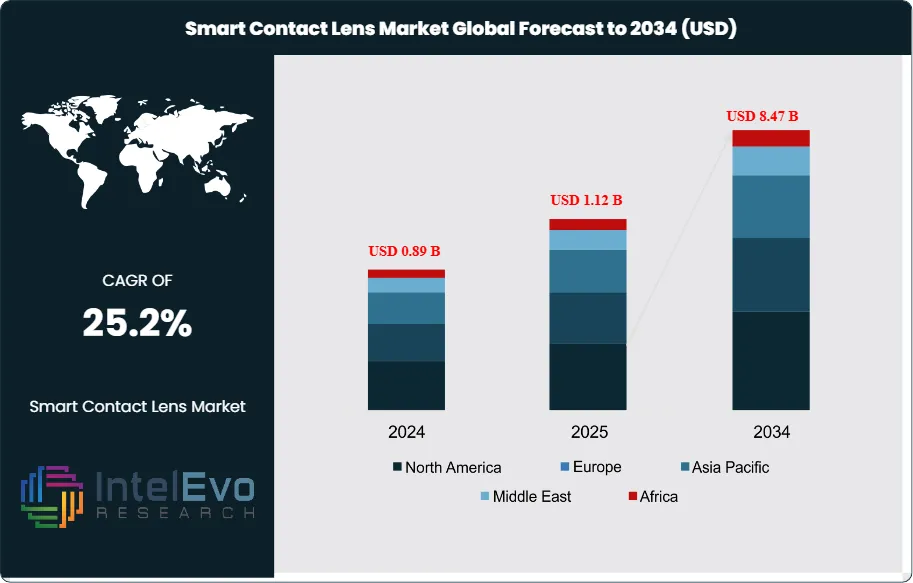

The Smart Contact Lens Market was valued at approximately USD 0.89 Billion in 2024 and reached USD 1.12 Billion in 2025. The market is projected to grow to USD 8.47 Billion by 2034, expanding at a CAGR of 25.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 7.35 Billion over the analysis period, making the smart contact lens market one of the fastest-expanding segments within the broader medical device and wearable technology space.

Get More Information about this report -

Request Free Sample ReportSmart contact lenses integrate miniaturized sensors, wireless communication modules, microprocessors, and power delivery systems into a form factor worn directly on the ocular surface. Current commercial and late-stage development applications span continuous glucose monitoring via tear-fluid analysis, intraocular pressure measurement for glaucoma management, augmented reality display projection, vision correction with electronic focus adjustment, and drug delivery for chronic ophthalmic conditions. The convergence of these capabilities positions smart contact lenses at the intersection of ophthalmology, consumer electronics, and digital health, attracting capital from medical device conglomerates, semiconductor companies, and technology platform operators simultaneously.

Regulatory progress is a defining factor for the smart contact lens market trajectory through 2034. The U.S. Food and Drug Administration classifies smart contact lenses as combination products when they incorporate drug delivery or diagnostic functions alongside their optical properties, requiring coordinated review across the Center for Devices and Radiological Health and the Center for Drug Evaluation and Research. The FDA’s Breakthrough Device Designation has been granted to multiple smart lens programs targeting glucose monitoring and glaucoma management, accelerating development timelines by an estimated 12 to 18 months relative to standard pathways.

Technology convergence is accelerating commercial readiness. Advances in low-power semiconductor fabrication, flexible and stretchable electronics, biocompatible antenna design, and wireless power transfer have reduced the engineering barriers that kept smart contact lenses in research phases throughout the prior decade. The rollout of 5G networks and the expansion of ambient Internet of Things (IoT) infrastructure provide the connectivity backbone for real-time data transmission from ocular-embedded sensors to cloud-based health management platforms.

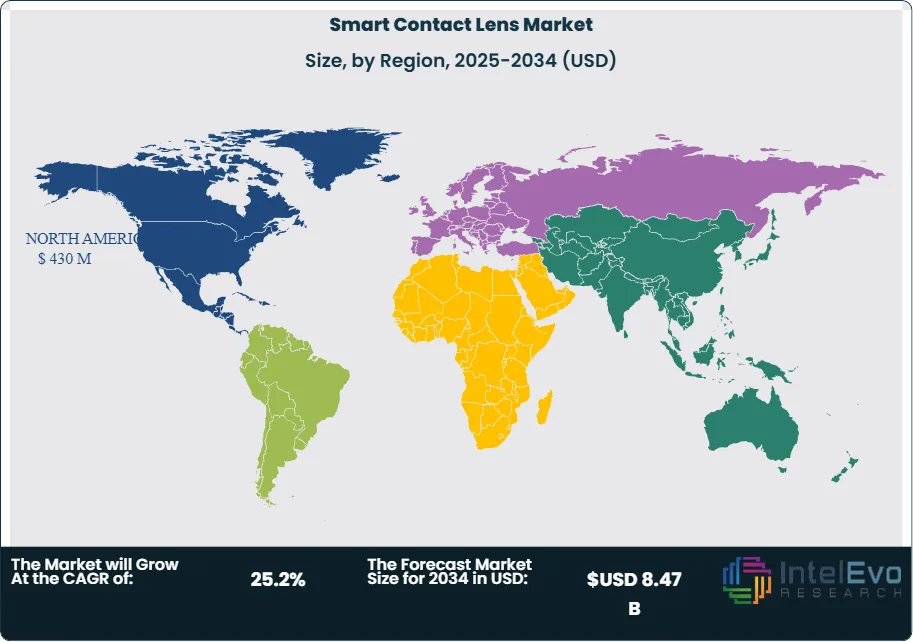

North America leads the smart contact lens market with a 38.4% share in 2025 at USD 430 Million, driven by concentrated R&D investment, robust FDA engagement frameworks, and a large diabetic population requiring continuous metabolic monitoring. Asia Pacific is the fastest-growing region, propelled by South Korea and Japan’s advanced electronics manufacturing ecosystems, China’s escalating myopia epidemic affecting an estimated 600 million individuals, and government-backed digital health infrastructure investment. Europe holds 24.6% of global market share, with Germany, the United Kingdom, and France leading clinical adoption of smart lens diagnostic applications.

, By Application (Healthcare Monitoring, Consumer Electronics & AR, Sports & Defense), By Technology (Sensor-Integrated Lenses, Passive Smart Lenses), By End-User, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global smart contact lens market was valued at USD 1.12 Billion in 2025 and is projected to reach USD 8.47 Billion by 2034, expanding at a CAGR of 25.2% during the 2026–2034 forecast period.

- Segment Dominance: By product type, diagnostic and monitoring smart lenses hold the largest share at 44.8% of the market in 2025, anchored by glucose monitoring and intraocular pressure sensing applications that address large chronic disease populations.

- Segment Dominance: By application, healthcare and medical monitoring represents the dominant application segment at 61.3% in 2025, reflecting the primary clinical-stage deployment of smart contact lens technology in diabetes management and glaucoma care.

- Driver: The global diabetic population exceeded 537 million adults in 2025 per International Diabetes Federation data, creating a substantial addressable market for non-invasive continuous glucose monitoring via tear-fluid-sensing smart lenses, a modality that eliminates the discomfort and infection risk of traditional finger-prick and subcutaneous sensor approaches.

- Restraint: Biocompatibility and ocular safety requirements impose stringent material and design constraints, with clinical trials for smart contact lens programs averaging 4 to 6 years from first-in-human studies to regulatory submission, extending time-to-market and capital requirements significantly.

- Opportunity: The augmented reality smart contact lens segment, currently at early commercial and late development stage, represents an addressable market exceeding USD 2.1 Billion by 2034 as consumer electronics manufacturers pursue ocular display as the successor form factor to headset-based AR devices.

- Trend: Miniaturized wireless power transfer and energy harvesting technologies are eliminating battery dependency in smart contact lens designs, with at least six development programs in 2025 demonstrating functional prototypes powered exclusively by radiofrequency energy harvesting or photovoltaic ocular illumination.

- Regional Analysis: North America leads the global smart contact lens market with a 38.4% share in 2025, representing USD 430 Million, supported by the highest concentration of clinical-stage smart lens programs and a diabetes prevalence rate exceeding 11% of the adult population.

Competitive Landscape Overview

The smart contact lens market is highly fragmented in 2025, with no single company controlling more than 22% of global market share. The top four players collectively account for approximately 54% of market revenue, reflecting the early-stage commercial environment where multiple technology platforms compete across different application verticals rather than for the same clinical indication. Competition is primarily technology-driven, with differentiation based on sensor accuracy, power management architecture, data transmission reliability, ocular biocompatibility, and regulatory designation status. Strategic partnerships between ophthalmic device companies, semiconductor firms, and digital health platform operators are the primary mode of competitive escalation, supplementing internal R&D with acquired capabilities. Venture capital investment into smart lens startups totaled an estimated USD 680 Million globally between 2023 and 2025, intensifying competitive dynamics at the development-stage tier.

Competitive Landscape Matrix

| Company | HQ | Market Position | Key Product | Geographic Strength | Recent Strategic Move (2024–2026) |

|---|---|---|---|---|---|

| Johnson & Johnson Vision | USA | Leader | ACUVUE Sense smart lens program | North America, Europe | Announced expanded clinical trial partnership with academic medical centers in 2025 for glucose-monitoring smart lens; targeting FDA Breakthrough Device submission by 2026. |

| Mojo Vision | USA | Leader | Mojo Lens AR display lens | North America | Secured USD 205 Million Series C extension in 2024; initiated FDA pre-submission process for AR display smart lens as a non-medical consumer device. |

| Sony (Smart Lens Program) | Japan | Challenger | Sony piezoelectric smart contact lens | Asia Pacific, Europe | Filed additional patents in 2025 for image-capture and storage integrated into contact lens form factor; expanded collaborative R&D with Japanese university optics labs. |

| Samsung Electronics | South Korea | Challenger | Smart lens AR platform | Asia Pacific | Disclosed prototype AR smart lens with embedded display and eye-tracking in a 2025 patent cluster; reported pilot user testing underway in South Korea. |

| Sensimed | Switzerland | Niche Player | Triggerfish IOP monitoring lens | Europe, North America | Received CE Mark renewal and expanded reimbursement coverage in three additional European markets in 2025 for Triggerfish continuous IOP monitoring. |

| Verily (Alphabet) | USA | Niche Player | Smart lens glucose program | North America | Refocused smart lens glucose program toward partnership model in 2024; entered technology licensing discussions with two major ophthalmic device companies. |

| InWith Corporation | USA | Niche Player | Electronic soft contact lens | North America | Demonstrated soft hydrogel electronic contact lens prototype with dynamic focus adjustment at CES 2025; advancing toward FDA pre-submission for corrective lens classification. |

| Innovega | USA | Niche Player | iOptik smart contact lens | North America | Completed Series B funding round of USD 42 Million in 2025; initiated FDA IDE application process for iOptik AR display contact lens system. |

By Product Type

The smart contact lens market by product type is led by diagnostic and monitoring lenses, which captured 44.8% of global market revenue in 2025 at approximately USD 502 Million. This segment encompasses lenses embedded with biosensors capable of detecting glucose concentration in tear fluid, intraocular pressure fluctuations associated with glaucoma progression, and other biomarkers accessible through the ocular microenvironment. Glucose-monitoring smart lenses are the most commercially advanced diagnostic application, benefiting from the enormous global diabetic population and the clinical imperative to reduce the burden of invasive monitoring. Sensimed’s Triggerfish, the only CE-marked smart contact lens in commercial use as of 2025, demonstrates that the regulatory pathway for diagnostic smart lenses is navigable, providing a reference framework that other developers are using to structure their submissions. Augmented reality and display lenses represent the second-largest product type at 28.6% of the market in 2025 at approximately USD 320 Million, primarily reflecting development-stage activity, prototype evaluation contracts, and technology licensing revenues rather than consumer device sales. Drug delivery smart lenses account for 15.3% of the market at USD 171 Million, addressing chronic ophthalmic conditions including dry eye disease, glaucoma, and allergic conjunctivitis by providing sustained therapeutic release calibrated to biological need. Vision correction smart lenses with electronic focus adjustment represent 11.3% of the market at USD 127 Million, an emerging segment addressing presbyopia populations.

By Application

The smart contact lens market by application is dominated by healthcare and medical monitoring, which represents 61.3% of global revenue in 2025 at USD 687 Million. Within this application cluster, ophthalmic disease management, specifically glaucoma and dry eye, and systemic disease monitoring, primarily diabetes, account for the bulk of clinical deployment and development investment. The case for smart lenses in glaucoma management is compelling because intraocular pressure fluctuates throughout the day and night, and single-point tonometry measurements at clinic visits miss the nocturnal pressure peaks that cause progressive optic nerve damage. Continuous IOP monitoring via a wearable ocular sensor addresses this clinical gap directly, and health economic models support the cost-effectiveness of early glaucoma progression detection relative to the cost of advanced vision loss treatment. The consumer electronics and augmented reality application segment accounts for 24.4% of the smart contact lens market in 2025 at USD 273 Million, driven by technology companies’ strategic positioning in anticipation of the AR display transition from headsets to contact lens form factors. Sports performance and defense applications represent the remaining 14.3% of the market at USD 160 Million, with military agencies and professional sports organizations funding smart lens programs for real-time biometric monitoring and field-of-view enhancement.

By Technology

The smart contact lens market by technology is bifurcated between electronic and sensor-integrated lenses, which account for 67.4% of market share in 2025 at USD 755 Million, and passive smart lenses incorporating microfluidic or colorimetric detection without active electronics, which represent 32.6% at USD 365 Million. Electronic smart lenses embed miniaturized application-specific integrated circuits (ASICs), flexible antenna coils, and electrochemical or photonic sensors within biocompatible polymer substrates. Their performance capabilities substantially exceed passive alternatives, but their engineering complexity, power requirements, and manufacturing costs are correspondingly higher. Passive smart lenses leverage tear-fluid-driven colorimetric reactions or molecularly imprinted polymers to detect analyte concentrations without power requirements. While their accuracy and data transmission capabilities are limited, passive lenses can be manufactured at costs approaching conventional soft contact lenses, making them commercially viable for large-scale screening or lower-acuity monitoring applications. Within electronic smart lenses, wireless power harvesting designs are overtaking battery-integrated architectures, with an estimated 68% of active development programs in 2025 pursuing batteryless power delivery.

By End-User

The smart contact lens market by end-user is primarily served by hospitals and ophthalmic specialty clinics, which account for 52.7% of market revenue in 2025 at USD 590 Million, reflecting the clinical-stage nature of most deployed smart lens applications. Ophthalmologists, endocrinologists, and optometrists at specialized centers are the primary prescribers and adopters of diagnostic smart lens systems, given the monitoring protocols, patient education requirements, and data interpretation infrastructure these technologies require. Direct-to-consumer channels represent 21.8% of the market at USD 244 Million, predominantly through early commercial AR and vision correction smart lens offerings marketed to technology-forward consumers. Research institutions and universities account for 15.6% of the market at USD 175 Million, reflecting extensive government-funded smart lens research programs at institutions in the United States, United Kingdom, South Korea, and China. Defense and government agencies represent the remaining 9.9% at USD 111 Million, funding specialized smart lens programs for soldier performance monitoring and night-vision or AR display integration.

Regional Analysis

North America

North America accounts for 38.4% of the global smart contact lens market in 2025, representing USD 430 Million, and is the world’s leading region by both R&D investment and clinical development activity. The United States hosts the majority of advanced smart lens development programs, with companies including Mojo Vision, Johnson & Johnson Vision, Verily, InWith, and Innovega operating clinical and pre-commercial programs from Silicon Valley, Boston, and New Jersey innovation hubs. The National Institutes of Health funded over USD 85 Million in smart lens and ocular sensor research grants between 2022 and 2025, sustaining early-stage technology development that feeds into commercial pipeline. The Centers for Medicare and Medicaid Services are actively evaluating reimbursement frameworks for diagnostic smart contact lenses, and a positive coverage determination for continuous IOP monitoring devices would materially accelerate clinical adoption. Canada contributes approximately 9% of the regional market, with University of Toronto and University of Waterloo maintaining internationally recognized programs in flexible electronics and biocompatible sensor development. The FDA’s Breakthrough Device pathway has been granted to at least three smart contact lens programs as of 2025, reducing regulatory timeline uncertainty for the leading clinical candidates.

Europe

Europe represents 24.6% of the global smart contact lens market in 2025 at USD 276 Million, anchored by Sensimed’s Triggerfish as the only regulatory-cleared commercial smart contact lens product in global use. Switzerland’s regulatory relationship with the European Medicines Agency under post-Brexit arrangements allowed Sensimed to maintain CE Mark status, and the Triggerfish system has achieved reimbursement in Germany, France, the Netherlands, and several Nordic markets for continuous glaucoma monitoring. Germany is the largest European market, supported by its ophthalmology specialist density and the statutory health insurance system’s willingness to reimburse novel monitoring devices with demonstrated clinical utility. The United Kingdom’s National Institute for Health and Care Research has funded smart contact lens clinical studies through its Efficacy and Mechanism Evaluation program. France’s CEA research organization and the Netherlands’ IMEC microelectronics institute are contributing foundational flexible electronics research applicable to smart lens platforms. The EU Medical Device Regulation’s enhanced post-market clinical follow-up requirements add compliance burden for smart lens manufacturers but provide a clear, credible quality framework that builds hospital purchasing confidence.

Asia Pacific

Asia Pacific accounts for 23.8% of the global smart contact lens market in 2025 at USD 267 Million and is the fastest-growing regional market, projected to expand at a CAGR exceeding 30% through 2034. South Korea and Japan lead the region in technology development, with Samsung, Sony, and LG Electronics each maintaining smart contact lens programs that leverage domestic semiconductor and display manufacturing expertise. China represents the largest addressable market by patient population, with an estimated 600 million myopia sufferers and a diabetes prevalence approaching 12.8% of the adult population as of 2025. The National Medical Products Administration has introduced expedited review tracks for digital health devices under China’s 14th Five-Year Plan healthcare modernization targets, reducing approval timelines for smart medical devices. India’s market is at an earlier development stage but growing rapidly as domestic ophthalmic care infrastructure expands and international smart lens companies establish partnership relationships with Indian hospital groups. Australia’s Vision CRC research consortium maintains collaborative programs with global smart lens developers, contributing to clinical evidence generation for regulatory submissions across the Asia Pacific region.

Latin America

Latin America represents 7.6% of the global smart contact lens market in 2025 at USD 85 Million, a share that reflects the region’s constrained medical device technology budget relative to clinical need. Brazil is the dominant market, with its large diabetic population, concentrated private hospital network, and technology-forward consumer base creating demand for both diagnostic and AR smart lens applications. The Brazilian health technology assessment body CONITEC is beginning to evaluate smart diagnostic medical devices, though formal reimbursement determination for smart contact lenses remains at least two to three years away. Mexico and Argentina represent secondary markets with growing private ophthalmology practice networks adopting advanced diagnostic tools. Currency instability across major Latin American economies creates import cost volatility for U.S. dollar-denominated medical devices, which is a structural constraint on technology adoption speed. Regional distribution partnerships between global smart lens companies and established Latin American ophthalmic device distributors are the primary market entry strategy, reducing the commercial infrastructure investment required for initial market penetration.

Middle East & Africa

Middle East & Africa accounts for 5.6% of the global smart contact lens market in 2025 at USD 63 Million. The United Arab Emirates is the regional leader, with Dubai and Abu Dhabi’s advanced healthcare ecosystems, high-income patient populations, and government investment in smart health technology creating favorable conditions for smart lens adoption. Saudi Arabia’s Vision 2030 program has prioritized digital health technology adoption, and the Saudi Food and Drug Authority has established regulatory frameworks for novel medical devices that align with FDA and CE Mark standards, simplifying multi-market approval strategies. South Africa represents the most established sub-Saharan market, centered on Johannesburg and Cape Town private hospital networks with specialist ophthalmology practices. The region’s diabetes epidemic, with Gulf Cooperation Council countries among the world’s highest prevalence populations, creates a clinically compelling market for glucose-monitoring smart contact lenses once these products achieve commercial regulatory clearance.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Diagnostic and Monitoring Smart Lenses

- Augmented Reality and Display Smart Lenses

- Drug Delivery Smart Lenses

- Vision Correction Smart Lenses

By Application

- Healthcare and Medical Monitoring

- Consumer Electronics and Augmented Reality

- Sports Performance and Defense

By Technology

- Electronic and Sensor-Integrated Lenses

- Passive Smart Lenses (Microfluidic / Colorimetric)

By End-User

- Hospitals and Ophthalmic Specialty Clinics

- Direct-to-Consumer

- Research Institutions and Universities

- Defense and Government Agencies

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.12 B |

| Forecast Revenue (2034) | USD 8.47 B |

| CAGR (2025-2034) | 25.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Diagnostic and Monitoring Smart Lenses, Augmented Reality and Display Smart Lenses, Drug Delivery Smart Lenses, Vision Correction Smart Lenses), By Application, (Healthcare and Medical Monitoring, Consumer Electronics and Augmented Reality, Sports Performance and Defense), By Technology, (Electronic and Sensor-Integrated Lenses, Passive Smart Lenses (Microfluidic / Colorimetric)), By End-User, (Hospitals and Ophthalmic Specialty Clinics, Direct-to-Consumer, Research Institutions and Universities, Defense and Government Agencies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | JOHNSON & JOHNSON VISION, MOJO VISION, SENSIMED, SONY CORPORATION, SAMSUNG ELECTRONICS, VERILY LIFE SCIENCES (ALPHABET), INWITH CORPORATION, INNOVEGA, ALCON, COOPERVISION, BAUSCH + LOMB, OPTERNATIVE, SIGHT DIAGNOSTICS, IOPTIC MEDICAL, LG ELECTRONICS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Healthcare Monitoring, Consumer Electronics & AR, Sports & Defense), By Technology (Sensor-Integrated Lenses, Passive Smart Lenses), By End-User, Industry Trends & Forecast 2026-2034")

, By Application (Healthcare Monitoring, Consumer Electronics & AR, Sports & Defense), By Technology (Sensor-Integrated Lenses, Passive Smart Lenses), By End-User, Industry Trends & Forecast 2026-2034")

, By Application (Healthcare Monitoring, Consumer Electronics & AR, Sports & Defense), By Technology (Sensor-Integrated Lenses, Passive Smart Lenses), By End-User, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Smart Contact Lens Market?

The Global Smart Contact Lens Market was valued at USD 0.89 Billion in 2024 and is projected to reach USD 8.47 Billion by 2034, growing at a CAGR of 25.2% from 2026 to 2034, driven by rising adoption of wearable healthcare technologies, increasing demand for continuous glucose monitoring and vision enhancement solutions, advancements in biosensors and augmented reality technologies, and expanding applications across healthcare, consumer electronics, and defense sectors worldwide.

Who are the major players in the Smart Contact Lens Market?

JOHNSON & JOHNSON VISION, MOJO VISION, SENSIMED, SONY CORPORATION, SAMSUNG ELECTRONICS, VERILY LIFE SCIENCES (ALPHABET), INWITH CORPORATION, INNOVEGA, ALCON, COOPERVISION, BAUSCH + LOMB, OPTERNATIVE, SIGHT DIAGNOSTICS, IOPTIC MEDICAL, LG ELECTRONICS, Others

Which segments covered the Smart Contact Lens Market?

By Product Type, (Diagnostic and Monitoring Smart Lenses, Augmented Reality and Display Smart Lenses, Drug Delivery Smart Lenses, Vision Correction Smart Lenses), By Application, (Healthcare and Medical Monitoring, Consumer Electronics and Augmented Reality, Sports Performance and Defense), By Technology, (Electronic and Sensor-Integrated Lenses, Passive Smart Lenses (Microfluidic / Colorimetric)), By End-User, (Hospitals and Ophthalmic Specialty Clinics, Direct-to-Consumer, Research Institutions and Universities, Defense and Government Agencies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date