- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Smart Contract Audit Tools Market Size, Share | CAGR 17.8%

Global Smart Contract Audit Tools Market Size, Share, Growth Analysis By Tool Type (Automated Static Analysis, Dynamic Analysis & Fuzzing, Formal Verification, AI-Powered Audit Platforms), By Blockchain Platform (Ethereum & EVM-Compatible Chains, BNB Smart Chain, Solana, Avalanche, Cosmos), By Deployment (Cloud, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

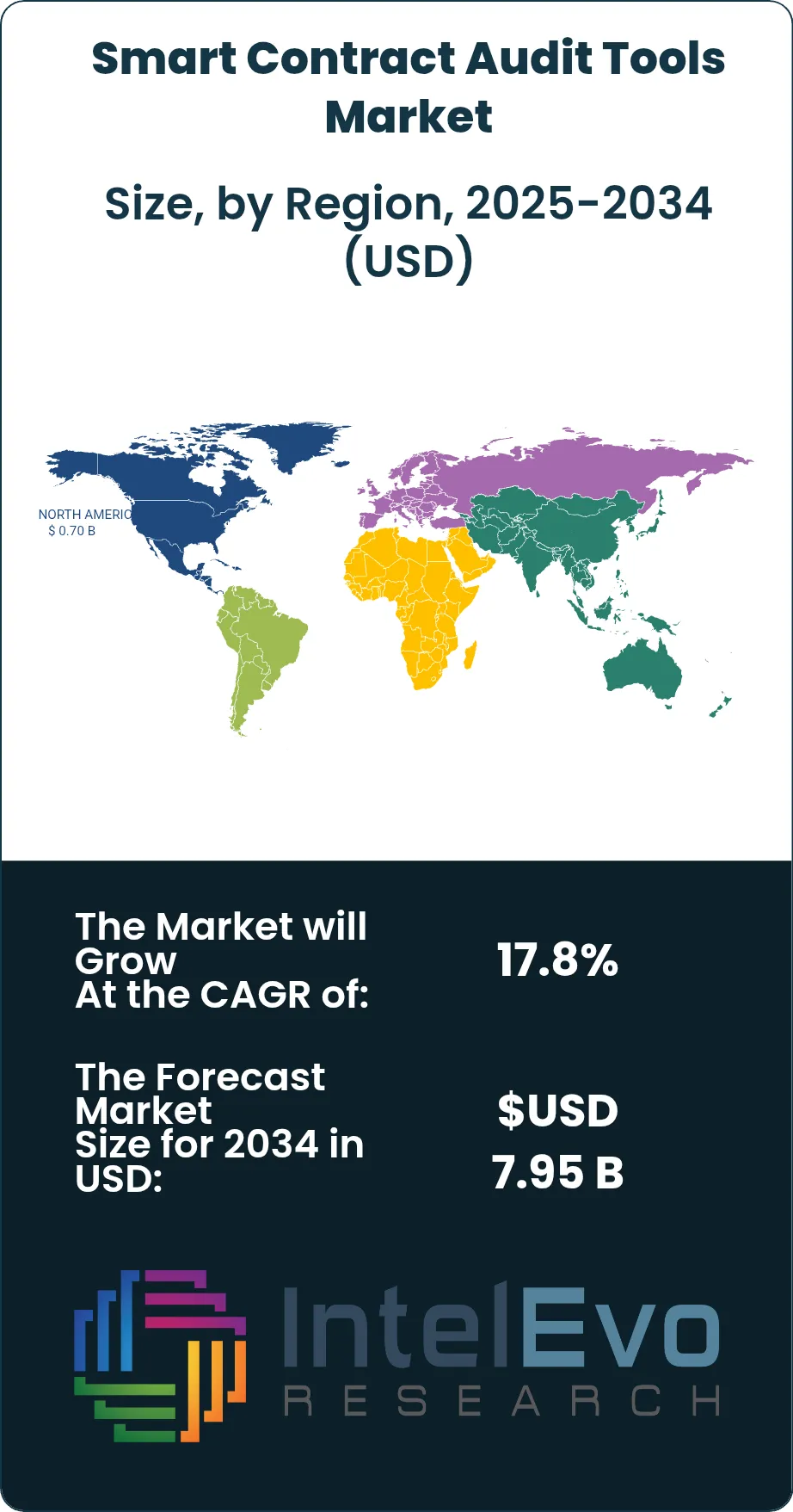

| USD 1.82 Billion | USD 7.95 Billion | 17.8% | North America, 38.4% |

The Smart Contract Audit Tools Market was valued at approximately USD 1.55 Billion in 2024 and reached USD 1.82 Billion in 2025. The market is projected to grow to USD 7.95 Billion by 2034, expanding at a CAGR of 17.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 6.13 Billion over the analysis period — an expansion driven by the collision of three converging forces: the institutionalization of decentralized finance creating quantifiable audit procurement obligations, a mounting blockchain exploit loss record that has made pre-deployment security verification a commercial necessity rather than an optional quality measure, and the emergence of AI-assisted static analysis that is simultaneously reducing audit cycle times and creating new competitive tiers within the vendor landscape.

Get More Information about this report -

Request Free Sample ReportThe first specific causal trigger behind current market momentum is the cumulative financial damage of smart contract exploits, which reached USD 2.4 Billion in total on-chain losses across publicly disclosed incidents in 2024 alone, according to cross-chain security monitoring data. This figure, while representing a decline from the USD 3.7 Billion peak of 2022, remained sufficient to sustain institutional risk aversion and pushed DeFi protocol governance frameworks — particularly those operating treasury assets above USD 50 million — to mandate external audits as preconditions for protocol upgrade votes. The practical result was a 28% increase in audit demand volume between Q2 2024 and Q2 2025, outpacing the capacity expansion of established audit firms and creating a service backlog that has elevated average audit pricing by an estimated 18–23% year-over-year for complex multi-contract protocol engagements.

A second distinct growth trigger operates at the regulatory layer. The European Union's Markets in Crypto-Assets Regulation (MiCA), fully applicable from December 2024, introduced technical documentation and security assessment requirements for crypto-asset issuers operating within EU jurisdictions. While MiCA does not explicitly mandate third-party smart contract audits, the liability exposure for issuers under MiCA's Article 82 investor protection provisions has prompted legal counsel at major EU-registered exchanges and stablecoin issuers to recommend pre-deployment audits as a standard risk mitigation measure — effectively creating a compliance-adjacent procurement driver. Simultaneously, the U.S. Commodity Futures Trading Commission's 2025 Digital Asset Market Structure Proposal, under Congressional deliberation, includes language requiring registered digital asset intermediaries to attest to smart contract code review processes, injecting a regulatory procurement catalyst into the world's largest capital market.

Technology maturation provides the third growth enabler. Automated static analysis tools based on abstract syntax tree traversal — the foundational technology in tools such as Slither and Aderyn — have reduced the cost of preliminary vulnerability screening by approximately 60% since 2020, enabling smaller protocols with limited security budgets to access at least baseline audit coverage. This cost deflation expands the total addressable market downward into the long tail of sub-USD 10 million TVL protocols that previously could not justify four-to-six-week manual audit timelines at USD 15,000–80,000 price points. A nuanced counterobservation: the proliferation of automated tools has not reduced the premium commanded by senior manual auditors. Industry compensation data from blockchain security recruiting platforms indicates that credentialed smart contract auditors with Ethereum Virtual Machine expertise commanded average total compensation of USD 195,000–340,000 in 2025, up 22% versus 2023 — a talent scarcity premium that constrains capacity scaling for firms reliant on human review and sustains pricing power for automated tool vendors serving the self-service audit segment. This growth trajectory mirrors the application security testing market's evolution between 2014 and 2018, when automated SAST tooling expanded addressable demand by 40% while simultaneously elevating pricing for expert manual penetration testing.

, By Blockchain Platform (Ethereum & EVM-Compatible Chains, BNB Smart Chain, Solana, Avalanche, Cosmos), By Deployment (Cloud, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global smart contract audit tools market reached USD 1.82 Billion in 2025 and is forecast to reach USD 7.95 Billion by 2034, registering a CAGR of 17.8% over the 2026–2034 period, driven by compounding regulatory compliance demand and blockchain exploit-related procurement urgency.

- Segment Dominance (By Tool Type): Automated static analysis tools held 41.2% of tool-type revenue in 2025 because their ability to scan 100,000+ lines of Solidity code in under four minutes — at near-zero marginal cost per additional scan — provides audit firms with a scalable pre-screening layer that manual review alone cannot match economically.

- Segment Dominance (By Blockchain Platform): Ethereum and EVM-compatible chains commanded 52.4% of platform-segmented revenue in 2025, reflecting the concentration of DeFi total value locked — approximately 62% of global on-chain TVL — on Ethereum Mainnet and its Layer 2 ecosystem, which directly determines audit procurement volume.

- Driver: USD 2.4 Billion in on-chain exploit losses in 2024, combined with DeFi governance frameworks mandating pre-upgrade audits for protocols above USD 50 million TVL, produced a 28% year-over-year increase in audit service demand between Q2 2024 and Q2 2025, creating service backlogs that elevated average audit pricing by 18–23%.

- Restraint: A structural shortage of credentialed smart contract auditors — with Ethereum Virtual Machine experts commanding USD 195,000–340,000 total compensation in 2025 — limits human-review capacity and prevents established firms from scaling audit throughput proportionally with demand growth, particularly constraining complex cross-chain bridge and zero-knowledge circuit audit engagements.

- Opportunity: Fewer than 9% of active smart contracts on non-EVM chains — Solana, Cosmos, and StarkNet combined — underwent third-party security review as of 2025, representing an addressable market expansion of USD 820 million–1.4 Billion by 2029 if audit tooling coverage matures across alternative virtual machine architectures.

- Trend: AI-integrated audit platforms reached 34% workflow adoption among North American audit firms in 2025 versus 11% in Asia Pacific, with LLM-assisted vulnerability classification reducing per-engagement analyst hours by an estimated 22%, creating a productivity arbitrage that is accelerating consolidation around tool vendors with proprietary training datasets.

- Regional Analysis: North America held 38.4% of global smart contract audit tools revenue at USD 0.70 Billion in 2025, anchored by Silicon Valley-based DeFi protocol concentration, USD 4.8 Billion in venture capital deployed into US blockchain companies in 2024, and CFTC digital asset market structure proposals creating compliance-adjacent audit procurement.

Competitive Landscape Overview

The smart contract audit tools market is moderately fragmented, with the top four vendors — CertiK, Trail of Bits, OpenZeppelin, and Hacken — collectively accounting for an estimated 48.7% of total market revenue in 2025. Competition operates on three distinct axes: methodology credibility (formal verification depth, false-positive rates, vulnerability taxonomy comprehensiveness), chain coverage breadth (number of supported virtual machine architectures and protocol standards), and turnaround speed (increasingly driven by automated tooling and AI-assisted review). The competitive environment bifurcates sharply between full-service audit firms that combine manual expert review with proprietary automated scanning (CertiK, Trail of Bits, Hacken) and pure-play tool vendors providing self-service or API-access scanning platforms (Slither, Aderyn, MythX). In 2025, two Chinese-affiliated security firms — PeckShield and SlowMist — accelerated geographic expansion into Southeast Asia and the Middle East with pricing 20–35% below Western incumbents for equivalent automated scan coverage, triggering CertiK's launch of a tiered community audit tier at reduced price points and prompting Trail of Bits to open-source Slither to defend its ecosystem positioning against price-based competitive displacement.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move (2024–2026) |

| CertiK | USA | Leader | CertiK Skynet Continuous Security Platform | North America / Asia Pacific | Launched CertiK Shield insurance product in Feb 2025, offering on-chain compensation up to USD 5 million per protocol for exploits on audited contracts, attracting 200+ DeFi protocols within six months. |

| Trail of Bits | USA | Leader | Slither Static Analyzer & Echidna Fuzzer | North America / Europe | Released Slither v0.11 with AI-assisted vulnerability classification in Apr 2025, reducing false-positive rates by 38% for Solidity and Vyper codebases; adopted by 65+ enterprise blockchain teams. |

| OpenZeppelin | USA | Leader | Defender 2.0 Smart Contract Security Suite | North America / Europe | Integrated AI-driven upgrade safety checks into Defender 2.0 in Jan 2026, covering 14 EVM-compatible chains and enabling automated pre-deployment regression testing for proxy contract patterns. |

| Hacken | Ukraine / UAE | Leader | HackenAI Smart Contract Audit Platform | Europe / Middle East | Expanded audit coverage to Solana Virtual Machine and Cosmos SDK protocols in Q3 2025; onboarded 140 new protocol clients, growing annual audit revenue by an estimated 44% year-over-year. |

| Quantstamp | USA | Challenger | Quantstamp Ethereum Audit Suite | North America / Europe | Signed multi-year audit framework agreement with a G10 central bank digital currency (CBDC) pilot program in Nov 2025, marking first sovereign-grade smart contract audit mandate for the firm. |

| PeckShield | China | Challenger | PeckShield Smart Contract Scanner | Asia Pacific / Global | Deployed real-time on-chain threat monitoring for 800+ DeFi protocols across BNB Smart Chain and Ethereum, detecting and publicly disclosing 23 critical vulnerabilities in Q1 2026 before exploitation. |

| ConsenSys Diligence | USA | Challenger | MythX Automated Security Analysis | North America / Europe | Released DASP++ vulnerability taxonomy update in Sep 2025, extending classification coverage to ERC-4337 account abstraction patterns and cross-chain bridge contract risks. |

| Cyfrin | USA | Niche Player | Aderyn Rust-Based Static Analyzer | North America | Open-sourced Aderyn v1.0 in Oct 2025 with 60+ built-in Solidity detectors; garnered 4,200 GitHub stars within 90 days, establishing developer community traction against established commercial tools. |

| SlowMist | China | Niche Player | SlowMist MistTrack & Audit Suite | Asia Pacific | Partnered with Binance's SAFU emergency fund in Dec 2024 to provide real-time exploit forensics and fund-tracing for BNB Smart Chain incidents, covering a combined USD 1.2 billion in protected assets. |

| Veridise | USA | Niche Player | Picus Formal Verification Engine | North America / Europe | Secured USD 18 million Series A in Aug 2025 to expand formal verification coverage to zero-knowledge proof circuits and Layer 2 rollup contracts, a segment competitors have not yet productized. |

By Tool Type

Automated static analysis tools captured 41.2% of smart contract audit tools market revenue at USD 0.75 Billion in 2025, a dominance explained by an economic argument that is specific to the blockchain security context rather than generic to software testing. Smart contract code, once deployed to a public blockchain, is immutable — a vulnerability discovered post-deployment cannot be patched through a server-side hotfix but requires an entirely new contract deployment with associated migration risks and costs. This immutability premium means that pre-deployment scanning tools command sustained willingness-to-pay from protocol teams who recognize that a single post-deployment exploit can erase protocol TVL, trigger governance crises, and generate personal liability for founding team members in jurisdictions with nascent crypto asset liability frameworks. Trail of Bits' Slither, the most widely deployed open-source static analyzer, underwent 4.1 million unique downloads in 2024, demonstrating market penetration that no commercial tool has matched; however, the commercial opportunity lies in enterprise-grade wrappers that add CI/CD pipeline integration, audit trail documentation, and vulnerability management dashboards atop the open-source core — a layer that Trail of Bits monetizes through its enterprise subscription product.

Dynamic analysis and fuzzing tools held 22.8% of tool-type revenue at USD 0.415 Billion in 2025, growing at the highest rate within the segment at an estimated 24.1% annually. Fuzzing tools — most prominently Echidna (Trail of Bits) and Medusa (Crytic) — generate pseudo-random transaction sequences to identify logic-layer vulnerabilities that static analyzers cannot detect from code structure alone. The fastest-growing application for dynamic analysis is cross-chain bridge testing, where the interaction between two or more independently deployed contract systems creates state dependency vulnerabilities that only executable transaction simulation can reliably expose. Bridge exploits accounted for 41% of total 2024 on-chain losses by value, a concentration that has elevated bridge-specific fuzzing from a specialty capability into a procurement prerequisite for any cross-chain infrastructure seeking institutional backing. Formal verification tools at 18.6% and AI-powered audit platforms at 17.4% complete the type segmentation, with formal verification commanding the highest per-engagement pricing due to mathematically exhaustive correctness proofs required for critical financial infrastructure.

By Blockchain Platform

Ethereum and EVM-compatible chains generated 52.4% of platform-segmented smart contract audit tools revenue at USD 0.953 Billion in 2025 — a share anchored by the concentration of deployable financial value within the Ethereum ecosystem. Approximately 62% of global on-chain DeFi TVL resided on Ethereum Mainnet and its Layer 2 networks (Arbitrum, Optimism, Base, zkSync) as of mid-2025, creating a direct proportionality between TVL concentration and audit procurement demand. The EVM's dominance as the reference execution environment also means that the global developer population writing auditable smart contract code skews overwhelmingly toward Solidity and Vyper, languages for which static analysis tooling is most mature. OpenZeppelin's Contracts library — providing audited reusable components used in an estimated 75% of EVM protocol deployments — represents an upstream quality gate that paradoxically both reduces audit burden (audited components require less re-verification) and increases it (novel compositions of audited components create new attack surfaces requiring compositional security review).

BNB Smart Chain held 17.3% of platform revenue at USD 0.315 Billion in 2025, sustained by high transaction volume in gaming, NFT, and retail DeFi applications that generate recurring audit demand for protocol upgrades and feature additions. Solana captured 14.6% at USD 0.266 Billion, growing at an estimated 29.4% annually — the fastest rate among major platform segments — driven by Solana's resurgence in developer activity following network stability improvements and the migration of several high-value perpetual trading protocols from Ethereum. Critically, Solana's Rust-based programming model and Sealevel parallel execution environment require entirely distinct audit tooling from EVM chains, creating a platform-specific expertise barrier that limits auditor supply and sustains premium pricing for Solana-credentialed review teams. Other chains including Avalanche, Polkadot, and Cosmos contributed a combined 15.7% share, with Cosmos SDK's modular architecture requiring bespoke audit coverage for each custom chain module — a complexity that is attracting specialized boutique audit practices.

By Deployment

Cloud and SaaS deployment accounted for 61.3% of the smart contract audit tools market at USD 1.116 Billion in 2025, reflecting the developer-centric purchasing culture of the blockchain industry, where self-service API access to scanning tools is the default expectation rather than the exception. SaaS audit platforms enable protocol teams to run automated scans continuously throughout development cycles rather than as discrete pre-launch events — a shift from episodic to continuous security posture that increases platform revenue per client by 2.8–4.2x versus one-time scan pricing models. On-premise deployment retained 23.8% share at USD 0.433 Billion, sustained by sovereign CBDC programs, central bank digital infrastructure projects, and enterprise blockchain deployments at financial institutions with code confidentiality requirements that prohibit uploading proprietary contract source code to third-party cloud scanning infrastructure. Hybrid deployment at 14.9% is growing fastest as enterprise clients adopt architectures that perform initial static scanning locally while uploading sanitized intermediate representations to cloud-based AI analysis layers.

By End-User

DeFi protocols and decentralized applications represented 38.7% of end-user demand at USD 0.704 Billion in 2025. This segment's dominant position derives from a governance-mechanism procurement driver that is structurally unique to decentralized finance: major DeFi protocols including Aave, Compound, and Uniswap operate DAO-governed upgrade processes that require community audit approval before any parameter change or contract upgrade reaches on-chain vote. This governance gate effectively mandates continuous audit engagement rather than one-time pre-launch review, generating annualized recurring revenue per protocol that established audit firms estimate at USD 80,000–600,000 depending on protocol complexity and upgrade frequency. Enterprise blockchain at 22.1% is the fastest-growing end-user segment at an estimated 26.3% annually, as Fortune 500 financial institutions deploying tokenized asset settlement and cross-border payment infrastructure on permissioned blockchain networks introduce procurement budgets and compliance requirements that dwarf those of native crypto-native protocol teams. NFT and gaming platforms at 19.4%, government and public sector at 9.8%, and other industries at 10.0% complete the end-user distribution.

Regional Analysis

North America

Backed by USD 4.8 Billion in venture capital deployed into U.S.-headquartered blockchain companies in 2024 — the largest annual figure since the 2021 peak — and the regulatory pressure created by the CFTC's 2025 Digital Asset Market Structure Proposal requiring smart contract code review attestations from registered digital asset intermediaries, North America's smart contract audit tools market captured 38.4% of global revenue at USD 0.70 Billion in 2025. The United States accounts for approximately 86% of regional revenue, concentrated in San Francisco Bay Area-domiciled DeFi protocol teams, New York-headquartered institutional blockchain infrastructure firms, and Austin-based crypto-native companies that relocated from high-tax coastal markets. New York's Department of Financial Services BitLicense framework, which the NYDFS extended in 2025 to cover DeFi protocol operators with New York-resident users above a defined threshold, created a compliance-driven audit procurement event affecting an estimated 340 protocols in Q2–Q3 2025. Canada contributed the regional remainder, with Toronto-based Ethereum and Polkadot development communities generating audit procurement concentrated in the cross-chain bridge and Layer 2 infrastructure segments.

Europe

Regulatory requirements under MiCA, fully applicable since December 2024 across all 27 EU member states, reshaped procurement dynamics across the European smart contract audit tools market, which held 24.7% share worth USD 0.449 Billion in 2025. Germany represented the largest European sub-market through its concentration of regulated crypto custodians — 40 BaFin-licensed crypto custody providers as of mid-2025 — and enterprise blockchain initiatives within Munich's automotive and Frankfurt's financial services clusters. Switzerland's Crypto Valley in Zug contributed disproportionate demand from the estimated 1,100+ blockchain-native companies registered in the canton, including several DeFi protocol foundations that restructured as Swiss associations to access MiCA's EU passporting provisions. The United Kingdom's Financial Conduct Authority, operating its own post-Brexit crypto regulatory framework, published technical audit guidance for UK-registered cryptoasset businesses in March 2025, creating a parallel procurement trigger to MiCA that affected approximately 290 FCA-registered entities. The Netherlands, home to multiple stablecoin issuers seeking MiCA Article 16 authorization, represents the fourth-highest European demand concentration, with Amsterdam-based issuers driving demand for reserve attestation and smart contract audit combinations.

Asia Pacific

Sustained developer activity across blockchain accelerator programs in Singapore's one-north technology district and South Korea's Pangyo Techno Valley, combined with Hong Kong's Virtual Asset Service Provider licensing framework requiring security assessment documentation for licensed VASP smart contract deployments, propelled Asia Pacific's smart contract audit tools market to 22.8% global share at USD 0.415 Billion in 2025. Singapore accounted for the largest APAC sub-market share, anchored by MAS-regulated digital asset firms and the concentration of Southeast Asian DeFi protocol foundations in the Monetary Authority of Singapore's sandbox program. South Korea's Financial Services Commission digital asset framework, updated in Q1 2025 to require technical security disclosures for Korean won-denominated stablecoin issuers, generated a defined procurement wave among Kakao-affiliated Klaytn ecosystem projects and Hashed portfolio companies. India's web3 developer population — estimated at 12% of the global total by the World Economic Forum's 2025 Digital Economy Report — represents a latent demand corridor as Indian regulatory clarity progresses, with several Hyderabad and Bengaluru-based blockchain development studios already generating inbound audit revenue for established Western and regional vendors. Japan's FSA-registered crypto exchanges, totaling 32 licensed entities as of 2025, collectively generated audit procurement primarily for yen-denominated tokenized securities settlement contracts.

Latin America

Currency depreciation risk across Argentina and Venezuela paradoxically accelerated smart contract adoption for dollar-denominated stablecoin protocols, yet constrained Latin America's smart contract audit tools market to USD 0.153 Billion (8.4% global share) in 2025 as enterprise procurement budgets remained USD-denominated while operating revenues in local currency eroded purchasing power. Brazil dominated regional demand, where the Banco Central do Brasil's Drex CBDC pilot — a tokenized digital real project incorporating smart contracts for programmable finance — generated specialized audit procurement for the eight financial institutions selected as primary participants. São Paulo-based fintech ecosystem companies building on Ethereum and Polygon for cross-border remittance and trade finance applications constituted the secondary demand source, with Itaú Unibanco's digital asset division completing smart contract security reviews for its tokenized fund infrastructure in Q2 2025. Mexico's Comisión Nacional Bancaria y de Valores published blockchain technology guidance for regulated entities in late 2024, creating nascent but directionally positive regulatory tailwinds that audit tool vendors are beginning to address through regional partnership arrangements with Mexico City-based security consulting firms.

Middle East & Africa

Abu Dhabi Global Market's Financial Services Regulatory Authority finalized smart contract governance standards for ADGM-registered digital asset businesses in Q2 2025 — requiring documented pre-deployment security reviews for any smart contract managing client assets above USD 500,000 — creating a regulatory purchase mandate that directly expanded addressable demand across the MEA smart contract audit tools market to USD 0.104 Billion (5.7% share) in 2025. The UAE leads regional demand by a substantial margin, with Dubai International Financial Centre-regulated entities accounting for approximately 61% of MEA regional audit revenue, concentrated in tokenized real estate, sukuk digitization, and cross-border trade finance contract deployments. Saudi Arabia's Project Neom digital infrastructure initiative and the Saudi Central Bank's Aber cross-border payment program — a distributed ledger project with Saudi Aramco supply chain smart contract integrations — represent the two highest-value single-procurement opportunities in the MEA region, with combined security assessment budgets estimated at USD 14 million through 2026. South Africa's Financial Sector Conduct Authority, monitoring blockchain activity among the 11 licensed crypto asset service providers registered as of 2025, represents the MEA's third-largest demand concentration point, though provincial infrastructure constraints limit cloud SaaS deployment penetration relative to UAE and Saudi markets.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Tool Type

- Automated Static Analysis Tools

- Dynamic Analysis & Fuzzing Tools

- Formal Verification Tools

- AI-Powered Audit Platforms

By Blockchain Platform

- Ethereum & EVM-Compatible Chains

- BNB Smart Chain

- Solana

- Other Chains (Avalanche, Polkadot, Cosmos, etc.)

By Deployment

- Cloud / SaaS

- On-Premise

- Hybrid

By End-User

- DeFi Protocols & Decentralized Applications

- NFT & Blockchain Gaming Platforms

- Enterprise Blockchain

- Government & Public Sector

- Other Industries

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.82 B |

| Forecast Revenue (2034) | USD 7.95 B |

| CAGR (2025-2034) | 17.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Tool Type, (Automated Static Analysis Tools, Dynamic Analysis & Fuzzing Tools, Formal Verification Tools, AI-Powered Audit Platforms), By Blockchain Platform,(Ethereum & EVM-Compatible Chains, BNB Smart Chain, Solana, Other Chains (Avalanche, Polkadot, Cosmos, etc.)), By Deployment, (Cloud / SaaS, On-Premise, Hybrid), By End-User, (DeFi Protocols & Decentralized Applications, NFT & Blockchain Gaming Platforms, Enterprise Blockchain, Government & Public Sector, Other Industries) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CERTIK, TRAIL OF BITS, OPENZEPPELIN, HACKEN, QUANTSTAMP, PECKSHIELD, CONSENSYS DILIGENCE, CYFRIN, SLOWMIST, VERIDISE, HALBORN SECURITY, SPEARBIT, CODE4RENA, SHERLOCK (DECENTRALIZED AUDIT), MIXBYTES, NETHERMIND SECURITY, IMMUNEFI, ZELLIC, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Blockchain Platform (Ethereum & EVM-Compatible Chains, BNB Smart Chain, Solana, Avalanche, Cosmos), By Deployment (Cloud, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

, By Blockchain Platform (Ethereum & EVM-Compatible Chains, BNB Smart Chain, Solana, Avalanche, Cosmos), By Deployment (Cloud, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

, By Blockchain Platform (Ethereum & EVM-Compatible Chains, BNB Smart Chain, Solana, Avalanche, Cosmos), By Deployment (Cloud, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Smart Contract Audit Tools Market?

The Global Smart Contract Audit Tools Market was valued at USD 1.55 Billion in 2024 and is projected to reach USD 7.95 Billion by 2034, growing at a CAGR of 17.8% from 2026 to 2034, driven by rising adoption of blockchain and DeFi platforms, increasing smart contract security vulnerabilities, growing demand for AI-powered code auditing solutions, formal verification technologies, and expanding deployment of automated blockchain security tools across Web3 ecosystems worldwide.

Who are the major players in the Smart Contract Audit Tools Market?

CERTIK, TRAIL OF BITS, OPENZEPPELIN, HACKEN, QUANTSTAMP, PECKSHIELD, CONSENSYS DILIGENCE, CYFRIN, SLOWMIST, VERIDISE, HALBORN SECURITY, SPEARBIT, CODE4RENA, SHERLOCK (DECENTRALIZED AUDIT), MIXBYTES, NETHERMIND SECURITY, IMMUNEFI, ZELLIC, Others

Which segments covered the Smart Contract Audit Tools Market?

By Tool Type, (Automated Static Analysis Tools, Dynamic Analysis & Fuzzing Tools, Formal Verification Tools, AI-Powered Audit Platforms), By Blockchain Platform,(Ethereum & EVM-Compatible Chains, BNB Smart Chain, Solana, Other Chains (Avalanche, Polkadot, Cosmos, etc.)), By Deployment, (Cloud / SaaS, On-Premise, Hybrid), By End-User, (DeFi Protocols & Decentralized Applications, NFT & Blockchain Gaming Platforms, Enterprise Blockchain, Government & Public Sector, Other Industries)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Smart Contract Audit Tools Market

Published Date : 27 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date