- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Smart Food Packaging Market Size, Share & Forecast | CAGR 6.3%

Global Smart Food Packaging Market Size, Share, Analysis By Technology (Active Packaging, Intelligent Packaging, Modified Atmosphere Packaging (MAP), Edible and Emerging Packaging Formats), By Material (Plastic, Paper & Paperboard, Metal, Glass, Bio-Based & Biodegradable Materials), By Application (Meat, Poultry & Seafood, Dairy, Bakery & Confectionery, Fruits & Vegetables, Beverages), By End-User (Food Manufacturers, Retailers, Cold-Chain Operators, Foodservice & QSR Chains) Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 28.15 Billion | USD 48.85 Billion | 6.3% | North America, 38.5% |

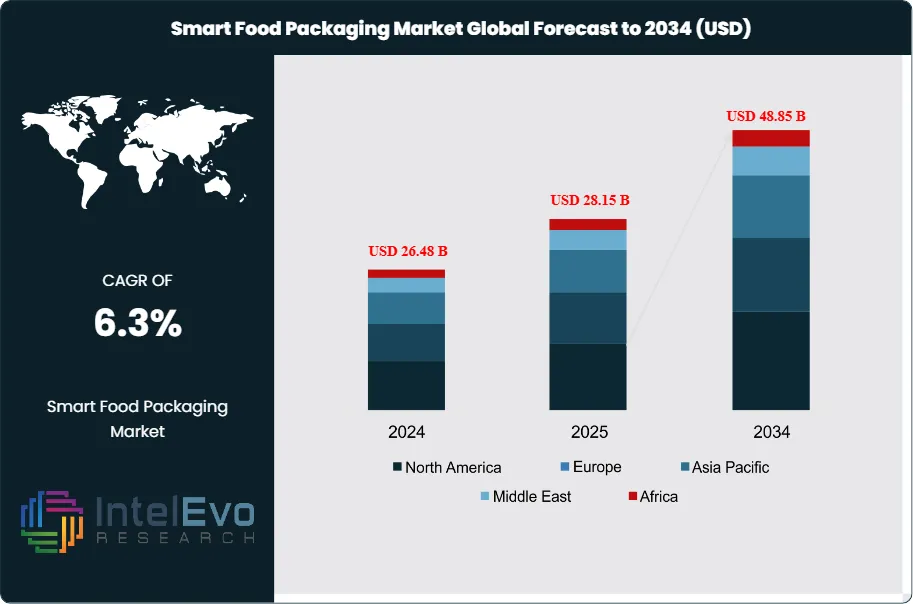

The Smart Food Packaging Market was valued at approximately USD 26.48 Billion in 2024 and reached USD 28.15 Billion in 2025. The market is projected to grow to USD 48.85 Billion by 2034, expanding at a CAGR of 6.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 20.70 Billion over the analysis period. The smart food packaging market is defined as the ecosystem of active, intelligent, and modified-atmosphere packaging technologies that extend shelf life, monitor freshness, improve traceability, and enable consumer engagement for food products through embedded sensors, indicators, scavengers, RFID tags, NFC chips, QR codes, and antimicrobial materials.

Get More Information about this report -

Request Free Sample ReportScope includes active packaging formats such as oxygen scavengers, moisture absorbers, and antimicrobial films; intelligent packaging formats including time-temperature indicators, freshness sensors, RFID, NFC, and blockchain-enabled QR codes; and modified atmosphere packaging (MAP) systems that alter internal gas composition. Conventional non-functional plastic and paper packaging without sensing, indicating, or active chemistry features is excluded. Primary demand is anchored to a USD 427 Billion global food packaging parent market, within which smart packaging represents approximately 5-7% penetration in 2025 and is growing almost twice as fast as the broader category.

Food safety regulation is the decisive catalyst in 2025. The FDA Food Traceability Final Rule under FSMA Section 204(d) mandates 24-hour recordkeeping retrieval across Critical Tracking Events for foods on the Food Traceability List. On March 20, 2025, the FDA announced a 30-month compliance extension, pushing the deadline from January 20, 2026 to approximately July 20, 2028. This extension provides smart packaging adopters additional runway to deploy RFID, GS1 barcodes, and IoT sensors at scale. The EU General Food Law, Regulation (EC) 1935/2004 on food contact materials, and the Packaging and Packaging Waste Regulation (PPWR) 2025/40 adopted in January 2025 further accelerate smart packaging adoption across 27 member states.

Technology maturation is compressing unit economics. Passive RFID tag prices dropped to USD 0.05-0.08 per unit in 2025, down from USD 0.15 in 2020, making item-level serialization economically viable for mainstream fresh produce and dairy categories. Time-temperature indicator (TTI) label costs fell below USD 0.06 per unit for deployments above 10 million tags annually. Near-Field Communication (NFC) chip integration into carton packaging supports authentication, anti-counterfeiting, and consumer engagement through smartphone taps, with adoption scaling across premium spirits, infant nutrition, and traceable coffee.

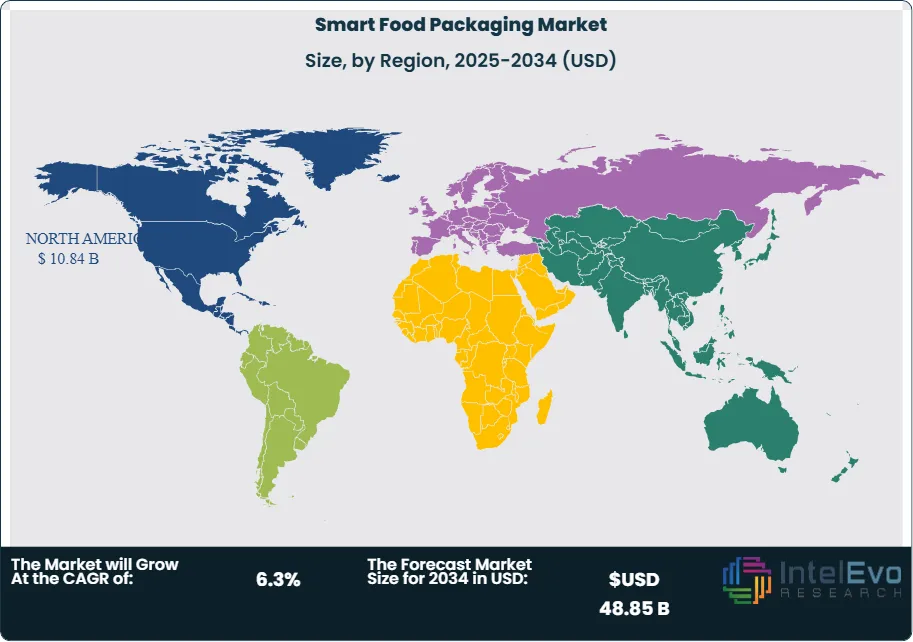

Regional concentration is pronounced. North America held 38.5% of the smart food packaging market in 2025 at approximately USD 10.84 Billion, supported by FSMA traceability mandates and early RFID adoption by Walmart, Kroger, and Albertsons. Asia Pacific accounted for 28.0% share at USD 7.88 Billion, with China projected to reach USD 8.7 Billion by 2034 and India expanding at a country CAGR of 8.9%. Europe held 22.0% share at USD 6.19 Billion, anchored by PPWR compliance and the EU Farm to Fork Strategy targeting digital traceability across the food chain.

Supply-chain dynamics are consolidating around integrated platform providers. Amcor plc completed its USD 8.4 Billion all-stock combination with Berry Global on April 30, 2025, creating one of the largest global packaging companies with 212 sites across 40 countries. Sealed Air, Tetra Pak, 3M, and Mondi compete across active and intelligent formats, while specialists such as Timestrip, Insignia Technologies, and Senoptica Technologies target niche sensor categories. Blockchain traceability partnerships between consumer-goods majors and technology providers are extending beyond pilots into production deployments.

Forward to 2034, three forces will shape smart food packaging market direction. Regulatory expansion of traceability rules to additional food categories in North America, Europe, and Asia Pacific will drive sustained RFID and sensor demand. Sustainability mandates under the EU PPWR and extended producer responsibility schemes will push active packaging toward biodegradable, mono-material, and recyclable formats. Artificial intelligence integration into freshness prediction and supply-chain optimization will convert passive packaging into data-generating endpoints across the cold chain.

, Edible and Emerging Packaging Formats), By Material (Plastic, Paper & Paperboard, Metal, Glass, Bio-Based & Biodegradable Materials), By Application (Meat, Poultry & Seafood, Dairy, Bakery & Confectionery, Fruits & Vegetables, Beverages), By End-User (Food Manufacturers, Retailers, Cold-Chain Operators, Foodservice & QSR Chains) Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global smart food packaging market expanded from USD 28.15 Billion in 2025 and is projected to reach USD 48.85 Billion by 2034, delivering a CAGR of 6.3% across the forecast period.

- Segment Dominance (Technology): Active Packaging led with 53.0% share in 2025, approximately USD 14.92 Billion, driven by oxygen scavengers, moisture absorbers, and antimicrobial films for meat, dairy, and bakery categories.

- Segment Dominance (Material): Plastic materials including PET, PE, and PP captured 44.0% share in 2025, equal to USD 12.39 Billion, supported by barrier performance and compatibility with embedded sensors.

- Driver: The FDA FSMA Section 204 Food Traceability Final Rule and the EU Packaging and Packaging Waste Regulation adopted in January 2025 compelled food processors to adopt item-level RFID, GS1 barcodes, and IoT temperature tracking across Critical Tracking Events.

- Restraint: High implementation cost of intelligent sensors averaging USD 0.10-0.25 per SKU in small deployments, combined with fragmented cross-border standards, constrains adoption among mid-sized food processors and private-label brands.

- Opportunity: Blockchain-enabled traceability for fresh produce and meat covering an addressable USD 5.2 Billion sub-segment by 2034, driven by consumer demand for farm-to-fork authentication and FSMA 204 compliance.

- Trend: Mono-material recyclable barrier films embedded with printed sensors grew from under 2% of smart-packaging shipments in 2022 to an estimated 8% in 2025, targeting EU PPWR recyclability thresholds.

- Regional Analysis: North America dominated with 38.5% share, generating USD 10.84 Billion in 2025, anchored by FSMA 204 compliance preparation and Walmart, Kroger, and Albertsons RFID mandates.

Key Insights Summary

- The FDA announced on March 20, 2025 a 30-month extension of the FSMA Section 204 Food Traceability Rule compliance deadline, moving enforcement from January 20, 2026 to approximately July 20, 2028 for foods on the Food Traceability List.

- Amcor plc completed its USD 8.4 Billion all-stock combination with Berry Global on April 30, 2025, creating a combined entity with 212 manufacturing sites across 40 countries and consolidated revenue exceeding USD 24 Billion.

- Active packaging holds the largest technology share at 53% of the smart food packaging market in 2025, with oxygen scavengers and antimicrobial films dominating meat, poultry, dairy, and bakery applications.

- Passive RFID tag prices declined to USD 0.05-0.08 per unit in 2025 compared with USD 0.15 in 2020, enabling item-level serialization across fresh produce and protein categories under Walmart and Kroger traceability mandates.

- The EU Packaging and Packaging Waste Regulation (PPWR) 2025/40 was adopted on January 22, 2025 and sets recyclability thresholds of 35% recycled content for contact-sensitive plastic food packaging by 2030, directly driving mono-material smart packaging design.

- Tetra Pak introduced carton packages for India's food and beverages industry containing 5% certified recycled polymer in February 2025, expanding the addressable smart carton market under India's sustainable packaging initiative.

- According to USDA data from October 2024, Brazil is expected to lead global chicken meat exports in 2025 at 11.8 Million tons, creating sustained demand for smart packaging with time-temperature indicators across protein export corridors.

Competitive Landscape Overview

The smart food packaging market is moderately consolidated, with the top four players accounting for approximately 45-52% of combined global revenue in 2025. Competition is technology-based, centered on proprietary active chemistry, sensor accuracy, barrier performance, and sustainability credentials rather than price. Amcor plc, Sealed Air Corporation, Tetra Pak, and 3M Company compete across integrated portfolios spanning active, intelligent, and MAP solutions. Competitive evolution accelerated in 2025 with Amcor's USD 8.4 Billion acquisition of Berry Global completed April 30, Sealed Air's January 2025 appointment of a new Chief Technology Officer to accelerate smart packaging strategy, and Nestlé's Q1 2025 blockchain-enabled dairy pilot in France. Specialist innovators including Timestrip UK, Insignia Technologies, and Mitsubishi Gas Chemical are capturing targeted niches in time-temperature indicators, color-change freshness labels, and oxygen-scavenging resins.

Competitive Landscape Matrix

| Company | HQ | Position | Key Offering | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Amcor plc | Switzerland | Leader | AmFiber paper, AmPrima mono-PE, IMPRESSIONS QR closures | Global, 40 countries | USD 8.4B Berry Global merger completed April 2025 |

| Sealed Air Corporation | USA | Leader | CRYOVAC active films, compostable overwrap trays, LIQUIBOX | Americas, EMEA, APAC | New CTO appointed Q1 2025 for smart packaging acceleration |

| Tetra Pak (Tetra Laval Group) | Sweden/Switzerland | Leader | Connected Package platform, aseptic cartons, QR engagement | Europe, Asia Pacific | 5% recycled polymer cartons launched in India, Feb 2025 |

| 3M Company | USA | Leader | TTI labels, RFID, antimicrobial layers, oxygen scavengers | North America, Europe | Advanced TTI and sensor partnerships across food OEMs, 2025 |

| Mondi plc | UK/Austria | Challenger | Paper-based smart pouches, barrier films, FunctionalBarrier Paper | Europe, emerging markets | Expanded paper-based barrier portfolio for EU PPWR, 2025 |

| Huhtamäki Oyj | Finland | Challenger | Recyclable fiber packaging, foodservice smart solutions | Europe, North America, Asia | Circular fiber-based smart solutions ramp, 2025 |

| Crown Holdings, Inc. | USA | Challenger | Metal cans with smart labels, specialty beverage packaging | Global | Smart label rollouts for beverage OEMs, 2025 |

| Avery Dennison Corporation | USA | Challenger | RFID inlays, connected labels, atma.io platform | Global | atma.io connected products platform scaling food trials, 2025 |

| Mitsubishi Gas Chemical | Japan | Niche Player | MXD6 barrier resin, AGELESS oxygen scavengers | Asia Pacific, global | Berry Global MXD6 recyclable barrier partnership, March 2024 |

| Timestrip UK Ltd. | UK | Niche Player | Time-temperature indicators and smart cold-chain labels | Europe, global | Expanded cold-chain TTI portfolio for perishables, 2025 |

By Technology

Active Packaging dominated the smart food packaging market with 53.0% share in 2025, equal to USD 14.92 Billion. The technology integrates oxygen scavengers, moisture absorbers, ethylene absorbers, carbon-dioxide emitters, and antimicrobial layers directly into the packaging material to regulate internal conditions and extend shelf life. Active packaging is widely deployed across meat, poultry, seafood, dairy, and bakery categories, where spoilage prevention and microbial control deliver measurable savings against shrinkage. Key active packaging innovations in 2025 included Mitsubishi Gas Chemical's AGELESS oxygen scavengers and Amcor's AmPrima mono-PE recyclable barrier for shredded cheese, which replaced multilayer non-recyclable films.

Intelligent Packaging held 29.0% share at USD 8.16 Billion in 2025 and is the fastest-growing segment through 2034. Core technologies include time-temperature indicators (TTIs), freshness sensors, RFID inlays, NFC chips, QR codes, and blockchain-enabled authentication tags. Intelligent packaging adoption accelerated sharply in 2025 under FSMA Section 204 preparation and EU PPWR traceability rules. Avery Dennison's atma.io connected-products platform, Senoptica Technologies' printed oxygen sensors, and 3M's TTI labels lead commercial deployments. Modified Atmosphere Packaging (MAP) accounted for 15.0% share at USD 4.22 Billion, dominant in fresh produce and ready-meals where altered oxygen, nitrogen, and carbon dioxide ratios slow microbial and enzymatic spoilage. Edible coatings and other emerging formats contributed 3.0% share, spanning chitosan antimicrobial films and edible alginate barrier layers.

By Material

Plastic materials including PET, PE, and PP held 44.0% share at USD 12.39 Billion in 2025. Plastic remains the dominant material because of barrier performance, transparency, and compatibility with embedded sensor chemistry. Polyethylene terephthalate (PET) leads rigid food containers, while polyethylene (PE) and polypropylene (PP) dominate flexible smart pouches and MAP films. Mono-material plastic structures such as Amcor's AmPrima PE and Berry Global's MXD6-compatible PE are gaining share because they meet EU PPWR recyclability thresholds while maintaining oxygen barrier performance. Paper and paperboard captured 28.0% share at USD 7.88 Billion, driven by the shift to paper-based aseptic cartons by Tetra Pak and Mondi's FunctionalBarrier Paper for snack and confectionery segments.

Metal materials held 15.0% share at USD 4.22 Billion in 2025, concentrated in aluminum cans for carbonated beverages, ready-meals, and preserved foods where Crown Holdings and Ball Corporation integrate NFC-enabled smart labels. Glass accounted for 9.0% share at USD 2.53 Billion, used primarily in premium dairy, infant nutrition, and beverages where NFC and QR-enabled labels support premium product authentication. Bio-based and biodegradable materials including PLA, cellulose nanocrystals, and chitosan contributed approximately 4.0% share at USD 1.13 Billion. Bio-based materials are the fastest-growing material segment at a CAGR above 10% through 2034, supported by EU PPWR rules mandating recyclable or compostable contact-sensitive packaging by 2030.

By Application

Meat, poultry, and seafood applications led with 32.0% share in 2025, equal to USD 9.01 Billion. The category requires active and intelligent packaging because of high contamination and spoilage risk. Typical solutions include CRYOVAC shrink bags with oxygen scavengers, MAP trays with raised carbon dioxide, and time-temperature indicators for cold-chain integrity. Dairy products held 22.0% share at USD 6.19 Billion, driven by aseptic carton adoption for milk and yogurt. Bakery and confectionery captured 16.0% at USD 4.50 Billion, supported by moisture-absorbing sachets and oxygen-scavenging films that extend shelf life of crusty breads and chocolate. Fruits and vegetables accounted for 13.0% at USD 3.66 Billion, beverages for 11.0% at USD 3.10 Billion, and other categories including pet food and frozen meals for 6.0% at USD 1.69 Billion.

By End-User

Food manufacturers held the largest end-user share at 52.0% in 2025 (USD 14.64 Billion), deploying smart packaging at the point of production to meet FSMA 204 Traceability Lot Code mandates and EU food contact material rules under Regulation (EC) 1935/2004. Retailers including Walmart, Kroger, Tesco, and Carrefour accounted for 24.0% share (USD 6.76 Billion), driven by RFID mandates for case-level and item-level traceability across fresh produce, meat, and dairy. Logistics and cold-chain operators held 15.0% share (USD 4.22 Billion), using temperature-tracking RFID tags and GPS-enabled sensors to document transit conditions. Foodservice and QSR chains held 9.0% share (USD 2.53 Billion), deploying smart packaging in meal-kit, takeaway, and delivery formats where tamper-evidence and freshness verification support consumer trust.

Regional Analysis

North America

North America held the largest share of the smart food packaging market at 38.5% in 2025, generating USD 10.84 Billion. The United States anchored regional leadership through FSMA Section 204 Food Traceability Rule compliance preparation, with an extended deadline of July 20, 2028 following the March 20, 2025 FDA announcement. Walmart, Kroger, Albertsons, and Target expanded item-level RFID mandates across fresh produce, meat, and dairy categories in 2025. Canada contributed through the Safe Food for Canadians Regulations requiring traceability for fresh produce and seafood. Mexico gained investment as a near-shoring hub for smart label manufacturing serving US retailers. Amcor's April 30, 2025 completion of the USD 8.4 Billion Berry Global acquisition further concentrated US smart packaging capacity.

Asia Pacific

Asia Pacific accounted for 28.0% of global revenue in 2025 at approximately USD 7.88 Billion. China leads regional demand and is projected to reach USD 8.7 Billion by 2034 on the back of tightened food safety enforcement under the State Administration for Market Regulation (SAMR) and GB standards for food contact materials. Japan operates a mature TTI and MAP market anchored by Toyo Seikan Group and Mitsubishi Gas Chemical. India is expanding at a country CAGR of 8.9% through 2034, supported by Tetra Pak's February 2025 launch of carton packages with 5% certified recycled polymer for Indian food and beverage brands. South Korea, Australia, and Singapore added traceability pilots through Singapore Food Agency and the Singapore-MIT Alliance for Research and Technology (SMART) nanosensor research program.

Europe

Europe held 22.0% share in 2025, equal to USD 6.19 Billion. The EU Packaging and Packaging Waste Regulation (PPWR) 2025/40 was adopted on January 22, 2025 and directly drives smart packaging redesign across 27 member states. Mandatory recyclability thresholds for contact-sensitive plastic food packaging set at 35% recycled content by 2030 accelerated mono-material PE and paper-based barrier development. Germany led regional demand through BASF SE and multilayer film specialists, while France advanced through Nestlé's Q1 2025 blockchain-enabled smart packaging pilot for dairy. The United Kingdom supported innovation through Timestrip UK and Insignia Technologies. Italy and Spain expanded smart packaging for PDO-protected foods requiring anti-counterfeiting NFC authentication.

Latin America

Latin America represented 6.5% of the global smart food packaging market at USD 1.83 Billion in 2025. Brazil led the region, reinforced by projected leadership in global chicken meat exports at 11.8 Million tons in 2025 per USDA October 2024 data, which drives time-temperature indicator demand across protein export corridors. Mexico expanded through near-shoring investments serving US retailers, while Argentina, Chile, and Colombia added smart packaging capacity for fresh produce exports. Middle East & Africa accounted for 5.0% share at USD 1.41 Billion, with the UAE Food Safety Control Department and Saudi SFDA driving traceability compliance for imports. South Africa contributed through Nampak and local smart packaging converters, while Egypt and Nigeria advanced formal-sector packaging modernization.

Country Analysis

United States:

The US smart food packaging market reached USD 8.65 Billion in 2025 and is projected to grow at a CAGR of 6.5%, reaching approximately USD 15.25 Billion by 2034. Market depth is anchored by the FDA FSMA Section 204 Food Traceability Final Rule and its 30-month compliance extension announced March 20, 2025. Walmart's store-level RFID mandate, first applied to apparel and expanded to fresh produce in 2024-2025, drives downstream traceability investment. USDA Food Safety Inspection Service rules for meat and poultry further support RFID and MAP adoption. Key US activity in 2025 included Amcor's April 30 completion of the USD 8.4 Billion Berry Global merger, Sealed Air's January 2025 CTO appointment, and Amcor's September 2025 partnership with Burts for packaging with 55% post-consumer recycled content.

China:

China's smart food packaging market reached USD 3.25 Billion in 2025 and is projected to grow at a CAGR of 8.2% to approximately USD 6.60 Billion by 2034. Market expansion is anchored by the State Administration for Market Regulation enforcement of GB standards for food contact materials and the Food Safety Law amendments expanding cold-chain and traceability requirements. China hosts the world's largest ready-meal production base, generating strong demand for MAP trays and QR-enabled consumer engagement. Domestic packaging leaders include Zijiang Enterprise and Greatview Aseptic, while Tetra Pak operates multiple aseptic carton plants across the Yangtze River Delta. Government support under the 14th Five-Year Plan for Food Industry Modernization accelerated smart packaging capacity additions through 2025.

Germany:

Germany's smart food packaging market reached USD 1.75 Billion in 2025 and is projected to grow at a CAGR of 5.8% to approximately USD 2.90 Billion by 2034. Growth is propelled by the EU PPWR 2025/40, the German Packaging Act (VerpackG) requiring registration with Zentrale Stelle Verpackungsregister, and strict BfR food contact material guidelines. BASF SE leads material innovation with antimicrobial polymers and bio-based barriers. Major food processors including Dr. Oetker, Rügenwalder Mühle, and Meica integrate MAP and TTI solutions. Germany is also the European hub for recyclable barrier film development supporting the 35% PPWR recycled-content threshold by 2030.

India:

India's smart food packaging market reached USD 0.82 Billion in 2025 and is projected to grow at a CAGR of 8.9% to approximately USD 1.78 Billion by 2034, the fastest growth among major national markets. The Food Safety and Standards Authority of India (FSSAI) tightened packaging rules under the Food Safety and Standards (Packaging) Regulations 2018 and subsequent amendments extending traceability requirements to dairy, edible oils, and ready-to-eat categories. The Invest India food processing sector projection of USD 535 Billion in 2025 at 15.2% CAGR underpins packaging demand. Tetra Pak's February 2025 launch of carton packages with 5% certified recycled polymer established a template for sustainable smart packaging, while domestic converters including UFlex and Huhtamaki PPL expanded intelligent label capacity.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Technology

- Active Packaging

- Intelligent Packaging

- Modified Atmosphere Packaging (MAP)

- Edible and Other Emerging Formats

By Material

- Plastic (PET, PE, PP)

- Paper and Paperboard

- Metal

- Glass

- Bio-based and Biodegradable

By Application

- Meat, Poultry, and Seafood

- Dairy Products

- Bakery and Confectionery

- Fruits and Vegetables

- Beverages

- Others

By End-User

- Food Manufacturers

- Retailers

- Logistics and Cold-Chain Operators

- Foodservice and QSR Chains

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 28.15 B |

| Forecast Revenue (2034) | USD 48.85 B |

| CAGR (2025-2034) | 6.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Active Packaging, Intelligent Packaging, Modified Atmosphere Packaging (MAP), Edible and Other Emerging Formats), By Material, (Plastic (PET, PE, PP), Paper and Paperboard, Metal, Glass, Bio-based and Biodegradable), By Application, (Meat, Poultry, and Seafood, Dairy Products, Bakery and Confectionery, Fruits and Vegetables, Beverages, Others), By End-User, (Food Manufacturers, Retailers, Logistics and Cold-Chain Operators, Foodservice and QSR Chains) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | AMCOR PLC, SEALED AIR CORPORATION, TETRA PAK (TETRA LAVAL GROUP), 3M COMPANY, MONDI PLC, HUHTAMÄKI OYJ, CROWN HOLDINGS, INC., AVERY DENNISON CORPORATION, BERRY GLOBAL GROUP, INC., MITSUBISHI GAS CHEMICAL COMPANY, INC., TOYO SEIKAN GROUP HOLDINGS, LTD., TIMESTRIP UK LTD., STORA ENSO OYJ, SMURFIT KAPPA GROUP, SONOCO PRODUCTS COMPANY, DS SMITH PLC, BALL CORPORATION, BASF SE, SIG GROUP AG, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Edible and Emerging Packaging Formats), By Material (Plastic, Paper & Paperboard, Metal, Glass, Bio-Based & Biodegradable Materials), By Application (Meat, Poultry & Seafood, Dairy, Bakery & Confectionery, Fruits & Vegetables, Beverages), By End-User (Food Manufacturers, Retailers, Cold-Chain Operators, Foodservice & QSR Chains) Industry Trends & Forecast 2026-2034")

, Edible and Emerging Packaging Formats), By Material (Plastic, Paper & Paperboard, Metal, Glass, Bio-Based & Biodegradable Materials), By Application (Meat, Poultry & Seafood, Dairy, Bakery & Confectionery, Fruits & Vegetables, Beverages), By End-User (Food Manufacturers, Retailers, Cold-Chain Operators, Foodservice & QSR Chains) Industry Trends & Forecast 2026-2034")

, Edible and Emerging Packaging Formats), By Material (Plastic, Paper & Paperboard, Metal, Glass, Bio-Based & Biodegradable Materials), By Application (Meat, Poultry & Seafood, Dairy, Bakery & Confectionery, Fruits & Vegetables, Beverages), By End-User (Food Manufacturers, Retailers, Cold-Chain Operators, Foodservice & QSR Chains) Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Smart Food Packaging Market?

The Global Smart Food Packaging Market was valued at USD 26.48 Billion in 2024 and is projected to reach USD 48.85 Billion by 2034, growing at a CAGR of 6.3% from 2026 to 2034. Growth is driven by increasing demand for food safety, shelf-life extension, active and intelligent packaging solutions, RFID tracking, freshness indicators, IoT-enabled packaging technologies, supply chain transparency, and sustainable food packaging innovations across the global food and beverage industry.

Who are the major players in the Smart Food Packaging Market?

AMCOR PLC, SEALED AIR CORPORATION, TETRA PAK (TETRA LAVAL GROUP), 3M COMPANY, MONDI PLC, HUHTAMÄKI OYJ, CROWN HOLDINGS, INC., AVERY DENNISON CORPORATION, BERRY GLOBAL GROUP, INC., MITSUBISHI GAS CHEMICAL COMPANY, INC., TOYO SEIKAN GROUP HOLDINGS, LTD., TIMESTRIP UK LTD., STORA ENSO OYJ, SMURFIT KAPPA GROUP, SONOCO PRODUCTS COMPANY, DS SMITH PLC, BALL CORPORATION, BASF SE, SIG GROUP AG, Others

Which segments covered the Smart Food Packaging Market?

By Technology, (Active Packaging, Intelligent Packaging, Modified Atmosphere Packaging (MAP), Edible and Other Emerging Formats), By Material, (Plastic (PET, PE, PP), Paper and Paperboard, Metal, Glass, Bio-based and Biodegradable), By Application, (Meat, Poultry, and Seafood, Dairy Products, Bakery and Confectionery, Fruits and Vegetables, Beverages, Others), By End-User, (Food Manufacturers, Retailers, Logistics and Cold-Chain Operators, Foodservice and QSR Chains)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date