- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Smart Garden System Market Size, Share & Forecast | CAGR 6.1%

Global Smart Garden System Market Size, Share, Analysis By Type (Countertop Systems, Floor Gardens, Wall Gardens), By Technology (Self-Watering, Smart Sensing, LED Grow Lights, Nutrient Delivery, Smart Pest Management), By End-Use (Residential Homeowners, Commercial Greenhouses, Indoor Vertical Farming), By Distribution Channel (Online Retail, Specialty Stores) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

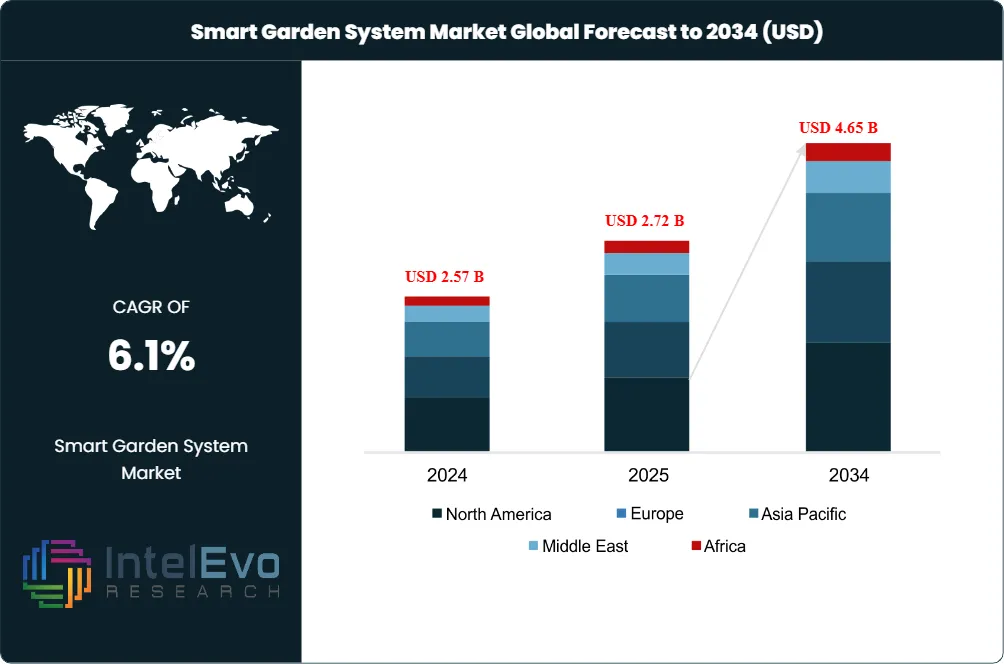

| USD 2.72 Billion | USD 4.65 Billion | 6.1% | North America, 39.5% |

The Smart Garden System Market was valued at USD 2.57 Billion in 2024 and USD 2.72 Billion in 2025. The market is projected to reach USD 4.65 Billion by 2034, expanding at a CAGR of 6.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.93 Billion over the analysis period. The smart garden system market covers connected indoor hydroponic planters, automated irrigation controllers, sensor-linked watering kits, app-based plant-care subscriptions, and robotic garden-maintenance equipment used by residential, education, hospitality, and small commercial buyers.

Get More Information about this report -

Request Free Sample ReportDemand is anchored by two practical problems: urban consumers have less garden space, and outdoor irrigation wastes measurable water. The U.S. Environmental Protection Agency reported in March 2026 that residential outdoor water use in the United States accounts for nearly 8 billion gallons per day, mainly for landscape irrigation, and that inefficient methods can waste up to 50.0% of this water. This creates a clear business case for Rachio, Rain Bird, GARDENA, Orbit B-hyve, and Hunter Hydrawise controllers that adjust schedules using weather data, soil moisture, and plant-zone settings.

Indoor smart garden systems form the most visible consumer segment because Click & Grow, Gardyn, Plantaform, Rise Gardens, Lettuce Grow, iDOO, and Modern Sprout convert gardening into a connected appliance purchase. Gardyn Home 4 supports 30 plants in approximately 2 square feet, while Gardyn Studio 2, introduced in October 2025, targets apartment users with automated lighting, watering, and AI-supported plant guidance. Plantaform entered the U.S. market at CES 2025 with a 15-plant fogponics cabinet, signaling that differentiated root-zone technology is becoming a competitive selling point rather than a laboratory feature.

The smart garden system market also reflects a reset after AeroGarden, formerly owned by Scotts Miracle-Gro, began winding down operations effective January 2025. AeroGarden's exit removed a legacy brand from the indoor hydroponic category, but it redirected demand toward Click & Grow, Gardyn, Plantaform, and open-pod alternatives. For procurement teams, the event increased focus on app longevity, seed-pod interchangeability, warranty terms, and offline operation when evaluating how to choose a smart garden system vendor.

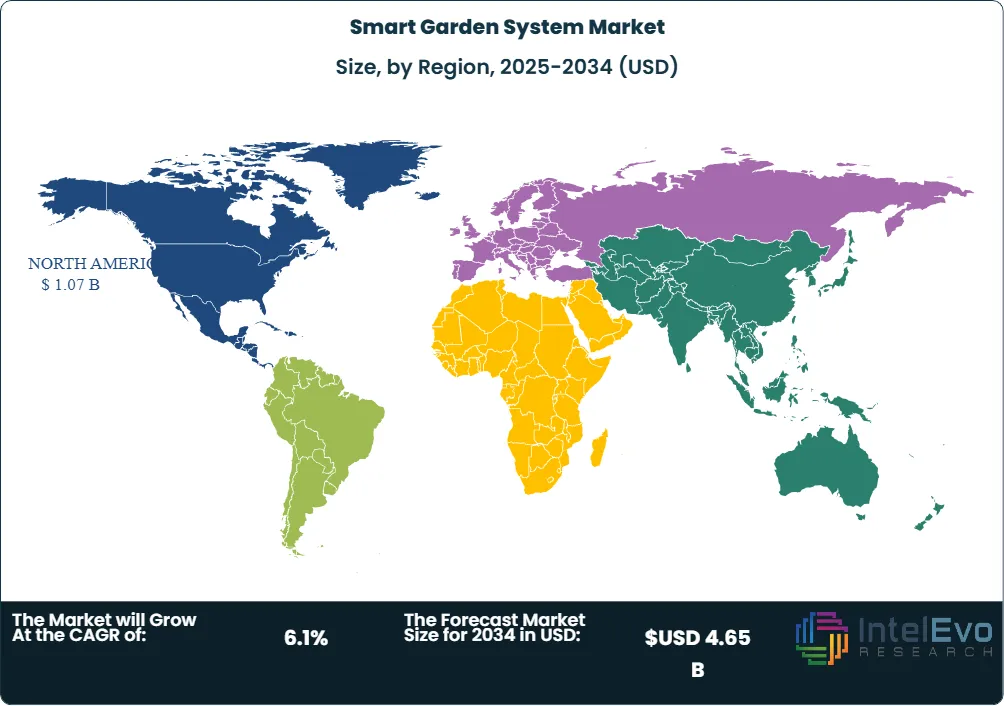

North America held 39.5% of the smart garden system market in 2025, equal to approximately USD 1.07 Billion, supported by high smart-home penetration, drought-sensitive U.S. states, and premium indoor-garden adoption. Europe followed at 27.6%, driven by GARDENA's installed base, EU water efficiency policy, and German, Nordic, Dutch, and U.K. gardening cultures. Asia Pacific is forecast to grow fastest through 2034 as China, Japan, South Korea, Singapore, and India combine compact urban housing with rising interest in hydroponic food production and app-controlled home appliances.

Market Definition & Scope

The smart garden system market is defined as the global commercial market for connected hardware, consumables, software, and services that automate plant growth, garden irrigation, plant monitoring, and small-scale residential food production. The market encompasses smart indoor hydroponic gardens, countertop herb gardens, vertical indoor planters, smart sprinkler controllers, hose-end timers, soil and moisture sensors, robotic lawn and garden tools, mobile apps, AI plant-advice engines, and recurring plant-pod or nutrient subscriptions.

This analysis includes residential and light-commercial products sold through direct-to-consumer websites, Amazon, garden centers, hardware retailers, landscaper channels, and smart-home distributors. It excludes conventional pots, non-connected drip irrigation, commercial greenhouse automation, farm-scale controlled-environment agriculture, generic grow lights sold without system integration, and professional irrigation design services without connected controllers. The smart garden system market sits between the smart-home appliance category, the home hydroponics category, and the residential irrigation equipment category, with demand shaped by water savings, food freshness, convenience, and space efficiency.

, By Technology (Self-Watering, Smart Sensing, LED Grow Lights, Nutrient Delivery, Smart Pest Management), By End-Use (Residential Homeowners, Commercial Greenhouses, Indoor Vertical Farming), By Distribution Channel (Online Retail, Specialty Stores) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The smart garden system market increased to USD 2.72 Billion in 2025 and is projected to reach USD 4.65 Billion by 2034 at a 6.1% CAGR, creating USD 1.93 Billion in absolute dollar opportunity.

- Segment Dominance: Indoor smart hydroponic systems led by type with 52.8% share in 2025, equal to USD 1.44 Billion, supported by Click & Grow, Gardyn, Rise Gardens, Lettuce Grow, and Plantaform product lines.

- Segment Dominance: Residential use led by application with 71.5% share in 2025, equal to USD 1.94 Billion, because households purchase smart gardens for herbs, leafy greens, and water-managed outdoor spaces.

- Driver: Water efficiency is the clearest outdoor driver, as EPA WaterSense data shows U.S. residential outdoor water use near 8 billion gallons per day and up to 50.0% waste from inefficient irrigation.

- Restraint: Recurring pod, nutrient, and app costs can add USD 80 to USD 360 per year per household, making total ownership cost a larger hurdle than the initial device price.

- Opportunity: Smart irrigation retrofits represent an addressable 2034 opportunity above USD 1.35 Billion as Rain Bird, Rachio, GARDENA, Orbit, and Hunter convert timer-based watering into weather-aware control.

- Trend: AI-guided plant care moved from premium marketing into product design in 2025, visible in Gardyn Studio 2, GARDENA smart SILENO sense, and app-based plant diagnostics across indoor garden systems.

- Regional: North America led with 39.5% share and USD 1.07 Billion in 2025, while Asia Pacific is expected to record the fastest regional CAGR at approximately 7.2% through 2034.

Key Insights Summary

- The smart garden system market benefits from EPA WaterSense labeling because a standard clock-based irrigation timer replacement can save an average U.S. home nearly 8,800 gallons of water annually when installed and operated correctly.

- Residential outdoor water use in the United States reaches nearly 8 billion gallons per day, and EPA analysis indicates that inefficient irrigation methods can waste up to 50.0% of that volume.

- Gardyn Home 4 is positioned for 30 plants in approximately 2 square feet, creating a density benchmark that helps compare premium vertical hydroponic systems against countertop products with 3 to 9 pods.

- Plantaform's 2025 CES-recognized smart indoor garden supports 15 plants and uses fogponics, adding a differentiated root-zone architecture to the smart garden system market.

- GARDENA's smart system requires a connected smart Gateway for core app-linked functions and integrates robotic mowing, water control, and irrigation scheduling through the GARDENA smart App.

- Rain Bird's October 2025 acquisition of Rachio shifted a cloud-connected controller specialist into an established irrigation manufacturer, tightening competition against Hunter Hydrawise, Orbit B-hyve, and GARDENA.

- AeroGarden's January 2025 closure changed buyer risk assessment because connected garden hardware depends on long-term app support, replacement pods, spare parts, and offline control continuity.

Competitive Landscape Overview

The smart garden system market is fragmented across indoor hydroponics, irrigation controls, plant sensors, and robotic garden maintenance. The top four commercial groups, Click & Grow, Gardyn, GARDENA, and Rain Bird/Rachio, accounted for an estimated 34.0% of 2025 revenue because no single vendor dominates both indoor food-growing systems and outdoor irrigation automation. Competition is based on device reliability, seed-pod economics, water-saving proof, app quality, retail reach, and support continuity.

Competitive dynamics changed after AeroGarden left the market in January 2025 and Rain Bird acquired Rachio in October 2025. The first event opened shelf space for Click & Grow, Gardyn, Rise Gardens, Lettuce Grow, iDOO, and Plantaform. The second event moved Rachio from a smart-home specialist into a professional irrigation channel, strengthening contractor access and utility-rebate credibility.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Click & Grow | Estonia / United States | Leader | Smart Garden 3, 9, 25, 27, plant pods | North America, Europe | Expanded post-AeroGarden replacement reach through compact pod-based indoor gardens |

| Gardyn, Inc. | United States | Leader | Gardyn Home 4, Gardyn Studio 2, Kelby app guidance | North America | Introduced Studio 2 in October 2025 for compact apartments |

| GARDENA / Husqvarna Group | Germany / Sweden | Leader | GARDENA smart system, AquaPrecise, smart SILENO | Europe, selected global markets | Highlighted AquaPrecise and AI vision mower technology in 2025 reporting |

| Rain Bird / Rachio | United States | Leader | Rachio smart sprinkler controllers, hose timer, Rain Bird irrigation | North America | Rain Bird acquired Rachio in October 2025 |

| Orbit Irrigation | United States | Challenger | B-hyve smart watering devices | North America | Continued retail expansion of app-linked irrigation controls |

| Hunter Industries | United States | Challenger | Hydrawise smart irrigation controllers | Global professional irrigation | Expanded contractor-led smart irrigation adoption through Hydrawise platform |

| Rise Gardens | United States | Challenger | Personal, Family, and large indoor garden systems | North America | Focused on modular family-scale indoor hydroponic systems |

| Plantaform | Canada | Niche Player | 15-plant fogponics smart indoor garden | North America | Entered U.S. market at CES 2025 |

| iDOO / LetPot | China | Niche Player | Countertop hydroponic grow systems | Global e-commerce | Expanded low-cost connected indoor garden options through online channels |

Segmentation Analysis

The smart garden system market segments by type, component, application, and distribution channel, with economics shaped by hardware margins, consumable refill frequency, app subscriptions, and outdoor water-saving regulations. Indoor systems generate higher device prices, while irrigation controllers provide clearer utility-savings justification and rebate support.

By Type

The smart garden system market by type is led by indoor hydroponic and countertop systems, which held 52.8% share and USD 1.44 Billion in 2025. Click & Grow, Gardyn, Rise Gardens, Lettuce Grow, Plantaform, iDOO, and LetPot compete across three price bands: compact herb units below USD 150, mid-size systems from USD 150 to USD 550, and premium vertical gardens above USD 600. Growth comes from apartment households that want herbs and leafy greens without soil, balcony space, or outdoor sunlight. The segment also benefits from recurring plant-pod, nutrient, and accessory purchases, which create more durable revenue than one-time hardware sales.

Smart irrigation and outdoor watering systems accounted for 32.4% share and USD 0.88 Billion in 2025. Rain Bird/Rachio, Orbit B-hyve, Hunter Hydrawise, GARDENA, Netro, and Eve Aqua address this category through sprinkler controllers, hose timers, smart valves, weather-linked schedules, and soil-sensor integrations. This segment has a stronger cost-saving claim than indoor planters because EPA WaterSense data translates water avoided into household utility savings. Robotic and sensor-enabled garden maintenance represented 14.8% share, led by GARDENA smart SILENO, Husqvarna Automower, and related connected mower systems that increasingly link lawn care with irrigation.

By Component

Hardware dominated the smart garden system market with 64.2% share and USD 1.75 Billion in 2025. Hardware includes grow bases, LED arrays, water reservoirs, pumps, sensors, controllers, gateways, valves, and robotic mower components. Gardyn Home 4, Click & Grow Smart Garden 9, Rachio 3, GARDENA smart Gateway, and Hunter Hydrawise controllers illustrate the breadth of this category. Hardware revenue is front-loaded, so vendors use plant pods, nutrients, and app subscriptions to defend customer lifetime value after the initial device purchase.

Consumables represented 24.5% share and USD 0.67 Billion in 2025, while apps, analytics, and services held 11.3% share and USD 0.31 Billion. Click & Grow plant capsules, Gardyn yCubes, nutrient kits, replacement pumps, LED accessories, and specialty seeds create a recurring margin pool for indoor systems. Services are smaller today but faster-growing because AI plant monitoring, pest alerts, vacation watering, and cloud schedule optimization provide reasons to keep customers inside proprietary apps. Buyers comparing smart garden system pricing benchmarks should model three-year spending, not just the device shelf price.

By Application

Residential users led the smart garden system market with 71.5% share and USD 1.94 Billion in 2025. Households use indoor gardens for herbs, lettuces, microgreens, tomatoes, flowers, and educational growing, while outdoor controllers reduce wasted watering for lawns, shrubs, and vegetable beds. The residential smart garden system procurement checklist now includes replacement-pod availability, noise, pump reliability, LED power consumption, app privacy, spare parts, and whether the device keeps working if cloud services change. AeroGarden's exit made these durability questions more visible.

Commercial, education, hospitality, and assisted-living applications together captured 28.5% share and USD 0.78 Billion in 2025. Schools use compact hydroponic gardens to teach plant science, nutrition, and sustainability; restaurants and hotels use vertical systems for herbs and guest-facing freshness; assisted-living operators use gardening as a wellness activity with lower physical effort. Outdoor smart irrigation is also used by small offices, campuses, hotels, and property managers. This segment grows more slowly than residential hardware but delivers larger average order values and more structured after-sales service opportunities.

By Distribution Channel

Online direct-to-consumer and marketplace sales led the smart garden system market with 46.0% share in 2025. Amazon, brand websites, Walmart.com, and specialty e-commerce stores are critical because buyers compare device capacity, plant counts, pod costs, warranty terms, and app reviews before purchase. Retail garden centers and home-improvement stores held 34.0% share, led by Home Depot, Lowe's, garden-center chains, and European DIY retailers. Contractor and professional irrigation channels represented 20.0% share and are especially relevant for Rain Bird, Hunter, Orbit, and GARDENA outdoor systems.

Regional Analysis

The smart garden system market is geographically led by North America, which held 39.5% share and USD 1.07 Billion in 2025. The United States accounts for most regional revenue because EPA WaterSense, drought management in California and Arizona, Amazon distribution, and smart-home adoption support controllers from Rachio, Rain Bird, Orbit, and Hunter. Indoor demand comes from Gardyn, Rise Gardens, Lettuce Grow, Click & Grow, and legacy AeroGarden replacement demand. Canada adds compact urban apartment demand, while Mexico remains earlier-stage but benefits from garden-center expansion in large cities.

Europe represented 27.6% of the smart garden system market in 2025, equal to USD 0.75 Billion. Germany, the United Kingdom, France, the Netherlands, and the Nordics anchor demand through GARDENA, Bosch smart-home compatibility, urban gardening culture, and water-conscious landscaping. EU Regulation 2020/741 on water reuse applies to agricultural irrigation, but its risk-management logic strengthens broader policy attention toward irrigation efficiency. Europe has lower indoor hydroponic device penetration than North America, but its robotic mower and smart watering adoption is deeper because GARDENA and Husqvarna have long-standing retail channels.

Asia Pacific accounted for 24.2% of the smart garden system market in 2025, equal to USD 0.66 Billion, and is forecast to post the fastest CAGR through 2034. China, Japan, South Korea, Singapore, and Australia drive growth because compact housing, dense cities, and food-safety concerns support countertop and vertical hydroponic systems. Xiaomi ecosystem sellers, iDOO, LetPot, and other China-based manufacturers compete aggressively on price, while Japan emphasizes design, quiet operation, and small-apartment fit. India remains earlier-stage, but rising apartment ownership in Bengaluru, Pune, Mumbai, Hyderabad, and Delhi supports smart herb-garden adoption.

Latin America held 5.2% of the smart garden system market in 2025, equal to USD 0.14 Billion. Brazil and Mexico lead regional demand, supported by garden-center retail and climate-sensitive irrigation needs in water-stressed urban regions. Adoption remains concentrated among premium households because imported smart controllers and indoor hydroponic kits face higher landed costs. Local distributors that bundle warranty, spare parts, and Spanish or Portuguese app support will outperform cross-border sellers that only compete on device price.

Middle East and Africa accounted for 3.5% of the smart garden system market in 2025, equal to USD 0.10 Billion. The United Arab Emirates, Saudi Arabia, Israel, and South Africa are the most relevant country markets. Water scarcity gives smart irrigation a clearer value proposition than decorative indoor gardening, particularly for villas, hotels, compounds, and municipal landscaping. Indoor hydroponic systems sell into high-income urban households and hospitality venues, while wider adoption is constrained by product price, replacement-pod logistics, and after-sales service coverage.

Country Analysis

The United States smart garden system market reached USD 0.95 Billion in 2025 and is projected to grow at a country CAGR of 5.8% through 2034. EPA WaterSense labeling creates a measurable case for replacing clock timers with weather-aware controllers, while drought-prone states such as California, Arizona, Nevada, Colorado, and Texas provide the strongest outdoor retrofit demand. Rain Bird's October 2025 acquisition of Rachio strengthened the professional channel for smart irrigation. Indoor demand is shaped by Gardyn, Rise Gardens, Lettuce Grow, Click & Grow, iDOO, and consumers replacing or maintaining AeroGarden units after the brand's 2025 exit.

Germany's smart garden system market reached approximately USD 0.20 Billion in 2025, with a forecast CAGR of 5.4% through 2034. GARDENA's German retail strength, Husqvarna Group's product portfolio, and high gardening participation support adoption of smart watering, robotic mowing, and connected garden accessories. GARDENA AquaPrecise and smart SILENO sense show how German and European buyers are moving toward integrated mowing and irrigation systems rather than isolated controllers. Premium indoor hydroponic systems remain smaller than outdoor automation but benefit from urban apartments in Berlin, Munich, Hamburg, and Frankfurt.

China's smart garden system market reached approximately USD 0.28 Billion in 2025 and is forecast to grow at a 7.9% CAGR through 2034. China-based sellers compete strongly in countertop hydroponic gardens, LED grow-light systems, water sensors, and app-controlled planters sold through domestic e-commerce and export channels. Xiaomi-compatible smart-home ecosystems, compact apartments, and younger consumers interested in herbs and microgreens support growth. Price competition is intense, so brands that combine low device cost with reliable pumps, LEDs, and local-language plant guidance are better positioned than premium imported systems.

Japan's smart garden system market reached approximately USD 0.14 Billion in 2025 and is projected to grow at a 5.9% CAGR through 2034. Demand centers on compact apartments, kitchen-counter herb systems, elderly-friendly gardening aids, and premium design-led devices. Panasonic-adjacent home appliance channels, local electronics retailers, and Japanese hydroponic research culture support buyer familiarity with controlled plant growth. Outdoor irrigation automation is smaller than in the United States or Germany because garden sizes are more limited, but balcony, indoor, and small-space solutions provide a durable growth base.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Type

- Indoor Smart Garden Systems

- Outdoor Smart Garden Systems

- Hydroponic Smart Garden Systems

- Others

By Component

- Smart Sensors

- Controllers

- Irrigation Systems

- Software & Mobile Applications

- Others

By Application

- Residential

- Commercial

- Institutional

- Others

By Distribution Channel

- Online Retail

- Specialty Stores

- Home Improvement Stores

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.72 B |

| Forecast Revenue (2034) | USD 4.65 B |

| CAGR (2025-2034) | 6.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type, (Indoor Smart Garden Systems, Outdoor Smart Garden Systems, Hydroponic Smart Garden Systems, Others), By Component, (Smart Sensors, Controllers, Irrigation Systems, Software & Mobile Applications, Others), By Application, (Residential, Commercial, Institutional, Others), By Distribution Channel, (Online Retail, Specialty Stores, Home Improvement Stores, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CLICK & GROW, GARDYN, INC., GARDENA / HUSQVARNA GROUP, RAIN BIRD / RACHIO, ORBIT IRRIGATION PRODUCTS, LLC, HUNTER INDUSTRIES, RISE GARDENS, LETTUCE GROW, PLANTAFORM, IDOO, LETPOT, MODERN SPROUT, XIAOMI ECOSYSTEM SELLERS, BOSCH SMART HOME, SCOTTS MIRACLE-GRO / AEROGARDEN LEGACY, EDYN, PLANTUI, VERITABLE, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Self-Watering, Smart Sensing, LED Grow Lights, Nutrient Delivery, Smart Pest Management), By End-Use (Residential Homeowners, Commercial Greenhouses, Indoor Vertical Farming), By Distribution Channel (Online Retail, Specialty Stores) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Technology (Self-Watering, Smart Sensing, LED Grow Lights, Nutrient Delivery, Smart Pest Management), By End-Use (Residential Homeowners, Commercial Greenhouses, Indoor Vertical Farming), By Distribution Channel (Online Retail, Specialty Stores) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Technology (Self-Watering, Smart Sensing, LED Grow Lights, Nutrient Delivery, Smart Pest Management), By End-Use (Residential Homeowners, Commercial Greenhouses, Indoor Vertical Farming), By Distribution Channel (Online Retail, Specialty Stores) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Smart Garden System Market?

The Global Smart Garden System Market was valued at USD 2.57 Billion in 2024 and USD 2.72 Billion in 2025, and is projected to reach USD 4.65 Billion by 2034, growing at a CAGR of 6.1% from 2026 to 2034. Market growth is driven by smart irrigation, IoT-enabled gardening solutions, and AI-powered garden automation.

Who are the major players in the Smart Garden System Market?

CLICK & GROW, GARDYN, INC., GARDENA / HUSQVARNA GROUP, RAIN BIRD / RACHIO, ORBIT IRRIGATION PRODUCTS, LLC, HUNTER INDUSTRIES, RISE GARDENS, LETTUCE GROW, PLANTAFORM, IDOO, LETPOT, MODERN SPROUT, XIAOMI ECOSYSTEM SELLERS, BOSCH SMART HOME, SCOTTS MIRACLE-GRO / AEROGARDEN LEGACY, EDYN, PLANTUI, VERITABLE, OTHERS

Which segments covered the Smart Garden System Market?

By Type, (Indoor Smart Garden Systems, Outdoor Smart Garden Systems, Hydroponic Smart Garden Systems, Others), By Component, (Smart Sensors, Controllers, Irrigation Systems, Software & Mobile Applications, Others), By Application, (Residential, Commercial, Institutional, Others), By Distribution Channel, (Online Retail, Specialty Stores, Home Improvement Stores, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date