- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Smart Insulin Pen Market Size, Share & Forecast | CAGR 18.9%

Global Smart Insulin Pen Market Size, Share, Growth Analysis By Product Type (Reusable Smart Insulin Pens, Disposable Smart Insulin Pens, Smart Pen Caps & Add-On Connectors), By Diabetes Type (Type 1 Diabetes, Type 2 Diabetes), By Connectivity Technology (Bluetooth, NFC, USB), By End-User (Homecare, Hospitals, Retail Pharmacies), Digital Diabetes Management Trends & Forecast 2026-2034

Report Overview

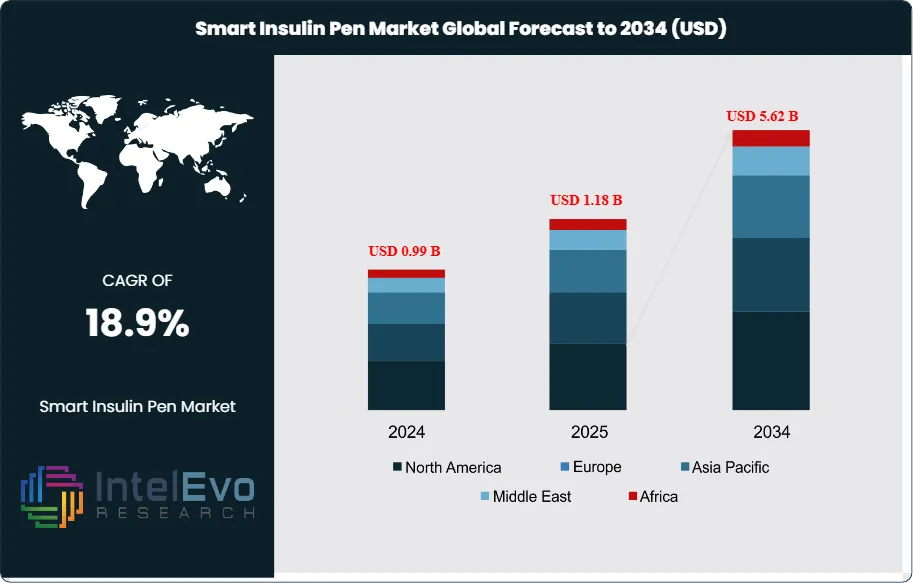

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

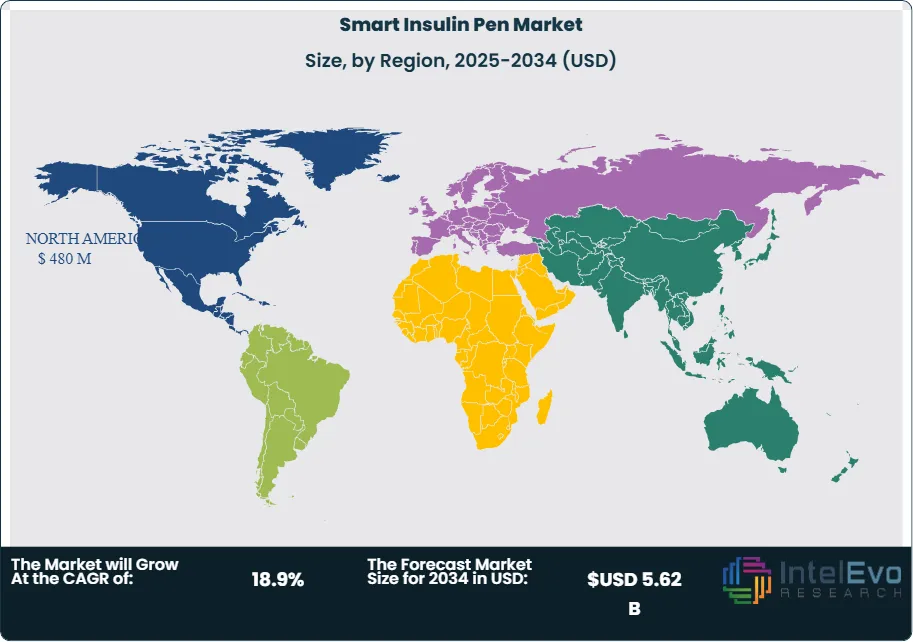

| USD 1.18 Billion | USD 5.62 Billion | 18.9% | North America, 40.7% |

The Smart Insulin Pen Market was valued at approximately USD 0.99 Billion in 2024 and reached USD 1.18 Billion in 2025. The market is projected to grow to USD 5.62 Billion by 2034, expanding at a CAGR of 18.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 4.44 Billion over the analysis period, driven by the convergence of digital health connectivity, insulin delivery precision engineering, and a rapidly expanding global diabetes population that demands smarter self-management tools.

Get More Information about this report -

Request Free Sample ReportSmart insulin pens represent the next generation of insulin delivery devices, incorporating dose capture technology, Bluetooth connectivity, companion mobile applications, and cloud-based data management to supplement or replace conventional analog insulin pens. Unlike continuous subcutaneous insulin infusion pumps, smart pens retain the simplicity and affordability of injection-based therapy while layering digital intelligence that captures dose timing, volume, insulin type, and residual cartridge volume. This data, transmitted to smartphone applications and integrated with continuous glucose monitors, enables closed-loop advisory systems that significantly reduce hypoglycemic episodes and improve time-in-range metrics for type 1 and type 2 diabetes patients.

Approximately 537 million adults worldwide were living with diabetes as of the latest International Diabetes Federation reporting cycle, a figure projected to rise to 783 million by 2045. Of the insulin-dependent population, an estimated 80% to 85% continue to use conventional injection devices including vials and syringes or standard pen injectors, creating a substantial addressable market for smart pen conversion. The smart insulin pen market benefits from secular tailwinds across all geographies as national diabetes management programs incorporate digital therapeutics, payer networks recognize the cost-saving potential of reduced hypoglycemia-related hospitalizations, and technology integration with CGM systems creates a clinically differentiated product category.

Regulatory activity supports market expansion. The FDA’s Digital Health Center of Excellence has established De Novo and 510(k) pathways for connected insulin delivery accessories, and the European Medical Device Regulation has clarified software-as-a-medical-device classification criteria that enable smart pen companion applications to receive CE marking as standalone regulated software. Reimbursement progress in Germany under the DiGA digital health application framework and in France under the PECAN program demonstrates that payers are moving toward structured coverage models for digital diabetes management tools.

The smart insulin pen market intersects directly with the broader connected diabetes management ecosystem, including CGM, insulin pumps, and digital therapeutics platforms. Strategic partnerships between smart pen device manufacturers and CGM leaders such as Dexcom and Abbott have created interoperable product pairs that deliver integrated dose and glucose data in a single patient-facing application. These partnerships accelerate adoption among type 1 diabetes patients and are creating premium market tiers that command price points 40% to 60% above conventional pen devices. Asia Pacific, particularly China and India, is emerging as the highest-growth regional market through 2034, supported by rising insulin use rates, government-led diabetes prevention programs, and expanding digital health infrastructure.

, By Diabetes Type (Type 1 Diabetes, Type 2 Diabetes), By Connectivity Technology (Bluetooth, NFC, USB), By End-User (Homecare, Hospitals, Retail Pharmacies), Digital Diabetes Management Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global smart insulin pen market was valued at USD 1.18 Billion in 2025 and is projected to reach USD 5.62 Billion by 2034, registering a CAGR of 18.9% during the forecast period 2026–2034.

- Segment Dominance: By product type, reusable smart insulin pens account for the largest share at approximately 58.4% of market revenue in 2025, driven by lower long-term patient cost and higher device intelligence integration compared to disposable formats.

- Segment Dominance: By diabetes type, type 2 diabetes represents the dominant end-use segment at approximately 62.3% of market revenue in 2025, reflecting the significantly larger type 2 patient population among insulin-dependent users globally.

- Driver: The global diabetes burden, with over 537 million adults affected and 80% to 85% of insulin users still on conventional delivery devices, creates a structural conversion opportunity that is the primary commercial growth engine for the smart insulin pen market.

- Restraint: Premium pricing of smart insulin pens, ranging from USD 50 to USD 300 per device compared to USD 10 to USD 30 for conventional pens, combined with absent or limited reimbursement coverage in most emerging markets, constrains adoption in price-sensitive populations that represent the majority of the global diabetes burden.

- Opportunity: Integration of smart insulin pen dose data with CGM systems and AI-driven dose advisory algorithms addresses a USD 1.2 Billion incremental software and connectivity opportunity by 2034, as closed-loop advisory features drive premium software subscription revenues above device hardware margins.

- Trend: Interoperability between smart pens and continuous glucose monitors accelerated in 2025, with over 65% of new smart pen product launches featuring native CGM data integration, compared to approximately 28% in 2022, reshaping competitive positioning toward connected ecosystem leadership.

- Regional Analysis: North America leads with a 40.7% regional share, equivalent to approximately USD 480 Million in 2025, supported by FDA regulatory clarity, commercial insurance coverage in major plans, and strong adoption among type 1 diabetes patients at endocrinology practices.

Competitive Landscape Overview

The global smart insulin pen market is moderately consolidated, with the top four companies holding a combined revenue share of approximately 64% in 2025. Competition is technology and ecosystem-driven, centered on CGM interoperability, companion app functionality, dose advisory accuracy, and payer reimbursement positioning. The market has seen significant partnership activity between device manufacturers and diabetes technology platforms rather than traditional price-based competition. New entrants from digital health and medical device sectors are challenging incumbents primarily through software-defined differentiation and broader connected device ecosystem integration.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| Novo Nordisk | Denmark | Leader | NovoPen 6 / Echo Plus | Global | Expanded NovoPen 6 connectivity with Dexcom G7 native integration; launched smart pen reimbursement program in Germany and France (2025) |

| Eli Lilly | USA | Leader | Tempo Smart Button | North America / Europe | Extended Tempo pen cap compatibility to Humalog and Basaglar cartridges; partnered with Dario Health for data platform integration (2025) |

| Sanofi | France | Leader | SoloStar Smart Pen Cap | Europe / Global | Launched connected pen cap solution for Toujeo and Lantus across 12 European markets; initiated CMS coverage discussions in the US (Jan 2025) |

| Bigfoot Biomedical | USA | Challenger | Bigfoot Unity Smart Pen System | North America | Received expanded FDA clearance for Bigfoot Unity dose advisory integration with Abbott LibreLink; secured Blue Cross Blue Shield network coverage (2025) |

| Insulet Corporation | USA | Challenger | Omnipod Smart Pen Companion | North America / Europe | Announced smart pen accessory roadmap to complement Omnipod 5 closed-loop system for MDI patients transitioning to hybrid closed-loop (2025) |

| Emperra | Germany | Niche Player | ESYSTA Smart Pen | Europe | Integrated ESYSTA platform with German DiGA reimbursement framework; expanded to Austrian and Swiss markets (Q2 2025) |

| Pendiq | Germany | Niche Player | Pendiq 2.0 Smart Insulin Pen | Europe | Completed CE MDR recertification for Pendiq 2.0; launched dose reminder and logbook app update (Mar 2025) |

| Companion Medical (Medtronic) | USA | Niche Player | InPen Smart Insulin Pen | North America | Medtronic completed InPen integration with Guardian 4 CGM for unified diabetes management dashboard (Jan 2026) |

By Product Type

The smart insulin pen market by product type is segmented into reusable smart insulin pens, disposable smart insulin pens, and smart pen caps or add-on connectors. Reusable smart insulin pens held the largest share at approximately 58.4% of market revenue in 2025, valued at approximately USD 689 Million. These devices feature integrated Bluetooth transmitters, dose capture sensors, and memory storage within the pen body itself, and are designed for use with replaceable insulin cartridges. The reusable format commands premium pricing that is partially offset by lower lifetime cost of ownership compared to disposable alternatives, making it the preferred choice for type 1 diabetes patients and motivated type 2 users who require multiple daily injections. Leading products in this category, including the Novo Nordisk NovoPen 6 and the Medtronic InPen, have established clinical evidence bases with published studies demonstrating statistically significant improvements in glycated hemoglobin and time-in-range when used with integrated CGM data.

Disposable smart insulin pens account for approximately 24.8% of market revenue in 2025 at USD 293 Million. These devices combine the convenience of prefilled, single-use pens with embedded connectivity features. While per-device margins are lower than reusable formats, disposable smart pens are commercially attractive in markets where insulin is dispensed in prefilled pen format, including several European and Asia Pacific health systems. The category is growing as large pharmaceutical manufacturers embed smart technology directly into prefilled disposable pen devices to differentiate their insulin products from biosimilar competition.

Smart pen caps and add-on connectors represent approximately 16.8% of market revenue in 2025 at USD 198 Million. These accessories retrofit existing conventional insulin pens with Bluetooth connectivity, dose tracking, and time-stamp capture capabilities without replacing the underlying pen device. Products such as the Eli Lilly Tempo Smart Button and the Sanofi smart pen cap allow pharmaceutical companies to extend connectivity features to their existing pen injector installed base without requiring patients to replace functional devices. The add-on segment is growing at a rate above the overall market as it provides the lowest-cost entry point into connected insulin delivery for health systems and payers exploring coverage models.

By Diabetes Type

Type 2 diabetes dominates the smart insulin pen market by indication, accounting for approximately 62.3% of market revenue in 2025 at USD 735 Million. The type 2 population represents the numerically dominant segment of insulin-dependent patients globally, with insulin initiation rates rising as disease duration extends and oral antidiabetic agents become insufficient for glycemic control. Smart pen adoption in type 2 diabetes is driven primarily by adherence improvement and dose titration support features, as this population frequently struggles with medication compliance, self-monitoring, and basal insulin dose optimization. Dose advisory algorithms calibrated for basal insulin titration protocols have demonstrated 0.4% to 0.7% HbA1c reductions in real-world evidence studies conducted in Germany and the United Kingdom, providing outcome data that supports payer coverage discussions.

Type 1 diabetes accounts for approximately 37.7% of market revenue in 2025 at USD 445 Million. Despite the smaller absolute patient population, type 1 diabetes users generate disproportionately high device value per patient due to multiple daily injection requirements, higher device replacement frequency, and stronger adoption of premium connectivity features including CGM integration and closed-loop advisory functions. Type 1 patients also drive the highest average software subscription attachment rates, as this population is more intensively engaged with digital diabetes management tools and more likely to use connected platforms that generate recurring software revenue above device hardware margins.

By End-User

Homecare and self-administration represents the dominant end-user segment at approximately 71.4% of market revenue in 2025, valued at USD 843 Million. Smart insulin pens are fundamentally patient-facing technologies designed for self-managed outpatient insulin therapy, and the home setting is the primary deployment environment across all geographies. Patient-facing companion applications that support dose tracking, reminders, and logbook management are central to the product value proposition in this segment. Adoption is strongly correlated with digital health literacy, smartphone penetration, and the availability of remote endocrinology consultation services that can act on the dose data captured by smart pens.

Hospital and clinic settings account for approximately 17.6% of market revenue in 2025 at USD 208 Million. Inpatient use of smart insulin pens is concentrated in endocrinology departments, diabetes education centers, and clinical research sites where structured dose capture data is required for patient monitoring or clinical trial protocols. Outpatient diabetes clinics are increasingly specifying smart pen use as part of structured diabetes management programs where the captured data supplements routine HbA1c testing. The remaining approximately 11.0% of market revenue in 2025, valued at USD 130 Million, comes from pharmacy and diabetes specialty retail channels where device trial programs and educational promotions drive initial smart pen adoption.

By Connectivity Technology

Bluetooth Low Energy connectivity is the dominant technology standard, present in approximately 78.3% of smart insulin pen products on the market in 2025 and accounting for a proportional share of revenue at USD 924 Million. BLE’s combination of low power consumption, standardized mobile device compatibility, and sufficient data transmission bandwidth for dose logging makes it the industry default for smart pen connectivity. Near-field communication technology is used in approximately 14.2% of products, primarily in specific European and Japanese market devices where NFC-based data transfer to reader devices aligns with pharmacy dispensing workflows. USB and proprietary wired data transfer solutions represent approximately 7.5% of market revenue, found primarily in legacy connected pen systems and clinical trial data capture platforms where wireless connectivity is restricted.

Regional Analysis

North America

North America holds the largest share of the global smart insulin pen market at approximately 40.7%, equivalent to USD 480 Million in 2025. The United States dominates regional revenue, supported by the FDA’s established 510(k) clearance pathway for smart pen connected accessories and companion software applications, commercial insurance coverage of smart insulin pen systems by major payers including UnitedHealth, Aetna, and Blue Cross Blue Shield networks, and a large type 1 diabetes patient population with high digital health engagement. The American Diabetes Association’s 2024 Standards of Medical Care in Diabetes explicitly referenced connected insulin delivery technology as a component of best-practice multiple daily injection management, creating clinical guideline support that facilitates prescriber adoption. Canada contributes to regional growth through provincial health technology assessment programs evaluating smart pen coverage under public formularies, with British Columbia and Ontario leading provincial pilot programs. The United States CGM adoption rate exceeding 35% among type 1 insulin users creates a favorable interoperability demand environment for smart pen systems with native CGM integration.

Europe

Europe accounts for approximately 27.4% of global market revenue at USD 323 Million in 2025. Germany leads European adoption through the Federal Joint Committee’s DiGA digital health application framework, which has approved several smart insulin pen companion applications as reimbursable digital therapeutics, creating a structured payer coverage model that reduces out-of-pocket barriers. France has advanced coverage discussions through its PECAN program for connected medical devices, while the United Kingdom’s NICE has issued guidance supporting CGM-integrated insulin delivery tools for type 1 diabetes management that encompasses smart pen connectivity. The European Medical Device Regulation transition has required software-as-a-medical-device re-certification for smart pen companion applications, creating a short-term compliance cost burden but establishing stronger regulatory credibility that supports payer coverage arguments. The Nordic countries demonstrate the highest smart pen penetration rates in Europe, driven by universal healthcare systems with established diabetes management protocols and high digital health infrastructure quality. Pan-European biosimilar insulin adoption is paradoxically supporting smart pen sales as manufacturers embed connectivity in premium pen formats to differentiate branded insulin from lower-cost biosimilar competitors.

Asia Pacific

Asia Pacific represents approximately 22.8% of global market revenue at USD 269 Million in 2025 and is the fastest-growing region, with demand driven by a diabetes patient population that represents over 60% of the global total. China holds the largest Asia Pacific market share, supported by the National Medical Products Administration’s progressive approach to connected device approvals and the government’s Healthy China 2030 initiative that targets diabetes management improvement as a public health priority. China’s expanding domestic medical device manufacturing base has produced competitively priced smart pen products aimed at the national health insurance formulary, reducing the premium pricing barrier that constrains adoption in many markets. Japan’s Pharmaceuticals and Medical Devices Agency has approved multiple smart pen systems, and Japan’s strong culture of precision medical device use supports adoption among the country’s aging insulin-dependent population. India represents a high-growth opportunity with an estimated 101 million diabetes patients as of 2023 per IDF data, though smart pen penetration remains below 2% due to affordability constraints, creating a substantial conversion opportunity as price points decline through increased domestic competition. South Korea’s advanced digital health infrastructure and national diabetes screening programs are accelerating adoption among newly diagnosed insulin users.

Latin America

Latin America represents approximately 5.8% of global market revenue at USD 68 Million in 2025. Brazil leads regional adoption through its SUS public health system’s diabetes management programs and a growing private health insurance sector that covers connected diabetes devices for commercially insured populations. The Brazilian Health Regulatory Agency has established a digital health device pathway that has cleared several smart insulin pen systems for commercial distribution. Argentina and Colombia represent secondary markets with active private sector adoption in urban diabetes specialty practices. The region’s growth is constrained by foreign exchange volatility that inflates device costs relative to local purchasing power, public health system budget limitations, and a fragmented diabetes care infrastructure that reduces the prescriber network for smart pen recommendations. However, rising smartphone penetration across the region, reaching approximately 72% of the adult population in 2025, ensures the necessary infrastructure for connected pen companion application functionality in growing urban populations.

Middle East & Africa

The Middle East and Africa region accounts for approximately 3.3% of global market revenue at USD 39 Million in 2025. The Gulf Cooperation Council countries, led by the UAE and Saudi Arabia, represent the majority of regional revenue, driven by some of the world’s highest diabetes prevalence rates and well-funded healthcare systems capable of covering premium connected device costs. The UAE’s Dubai Health Authority has incorporated connected diabetes management tools into its chronic disease management framework, and Saudi Arabia’s Vision 2030 health transformation agenda has allocated investment toward diabetes prevention and digital health infrastructure. South Africa leads Sub-Saharan adoption through private hospital networks and academic diabetes centers. The wider African continent faces significant infrastructure and affordability barriers, though mobile health initiatives and device-leasing models being piloted by global NGOs and health ministries represent early-stage conversion pathways for smart pen technology in higher-burden settings.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Reusable Smart Insulin Pens

- Disposable Smart Insulin Pens

- Smart Pen Caps / Add-On Connectors

By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

By End-User

- Homecare / Self-Administration

- Hospitals and Clinics

- Pharmacy and Diabetes Specialty Retail

By Connectivity Technology

- Bluetooth Low Energy (BLE)

- Near-Field Communication (NFC)

- USB / Proprietary Wired Transfer

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.18 B |

| Forecast Revenue (2034) | USD 5.62 B |

| CAGR (2025-2034) | 18.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Reusable Smart Insulin Pens, Disposable Smart Insulin Pens, Smart Pen Caps / Add-On Connectors), By Diabetes Type, (Type 1 Diabetes, Type 2 Diabetes), By End-User, (Homecare / Self-Administration, Hospitals and Clinics, Pharmacy and Diabetes Specialty Retail), By Connectivity Technology, (Bluetooth Low Energy (BLE), Near-Field Communication (NFC), USB / Proprietary Wired Transfer) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NOVO NORDISK, ELI LILLY, COMPANION MEDICAL (MEDTRONIC), BIGFOOT BIOMEDICAL, SANOFI, INSULET CORPORATION, EMPERRA GMBH E-HEALTH TECHNOLOGIES, PENDIQ GMBH, ROCHE DIABETES CARE, OWEN MUMFORD, YPSOMED, BAYER AG (DIABETES CARE), DEXCOM (CONNECTED PEN PARTNERSHIPS), ABBOTT DIABETES CARE (CONNECTED PEN PARTNERSHIPS), JIANGSU DELFU MEDICAL DEVICE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Diabetes Type (Type 1 Diabetes, Type 2 Diabetes), By Connectivity Technology (Bluetooth, NFC, USB), By End-User (Homecare, Hospitals, Retail Pharmacies), Digital Diabetes Management Trends & Forecast 2026-2034")

, By Diabetes Type (Type 1 Diabetes, Type 2 Diabetes), By Connectivity Technology (Bluetooth, NFC, USB), By End-User (Homecare, Hospitals, Retail Pharmacies), Digital Diabetes Management Trends & Forecast 2026-2034")

, By Diabetes Type (Type 1 Diabetes, Type 2 Diabetes), By Connectivity Technology (Bluetooth, NFC, USB), By End-User (Homecare, Hospitals, Retail Pharmacies), Digital Diabetes Management Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Smart Insulin Pen Market?

The Global Smart Insulin Pen Market was valued at USD 0.99 Billion in 2024 and is projected to reach USD 5.62 Billion by 2034, growing at a CAGR of 18.9% from 2026 to 2034, driven by rising diabetes prevalence, increasing adoption of connected diabetes management devices, advancements in digital health technologies, and growing demand for accurate insulin dosing, remote monitoring, and personalized patient care solutions.

Who are the major players in the Smart Insulin Pen Market?

NOVO NORDISK, ELI LILLY, COMPANION MEDICAL (MEDTRONIC), BIGFOOT BIOMEDICAL, SANOFI, INSULET CORPORATION, EMPERRA GMBH E-HEALTH TECHNOLOGIES, PENDIQ GMBH, ROCHE DIABETES CARE, OWEN MUMFORD, YPSOMED, BAYER AG (DIABETES CARE), DEXCOM (CONNECTED PEN PARTNERSHIPS), ABBOTT DIABETES CARE (CONNECTED PEN PARTNERSHIPS), JIANGSU DELFU MEDICAL DEVICE, Others

Which segments covered the Smart Insulin Pen Market?

By Product Type, (Reusable Smart Insulin Pens, Disposable Smart Insulin Pens, Smart Pen Caps / Add-On Connectors), By Diabetes Type, (Type 1 Diabetes, Type 2 Diabetes), By End-User, (Homecare / Self-Administration, Hospitals and Clinics, Pharmacy and Diabetes Specialty Retail), By Connectivity Technology, (Bluetooth Low Energy (BLE), Near-Field Communication (NFC), USB / Proprietary Wired Transfer)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date