- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Smart Irrigation Controller Market Size & Forecast | CAGR of 12.0%

Global Smart Irrigation Controller Market Size, Share, Growth By Type (Weather-Based, Sensor-Based, Hybrid), By Connectivity (Wi-Fi, Bluetooth, Cellular, LoRaWAN), By Application (Agriculture, Residential & Commercial Landscaping, Golf Courses), By End-User (Farmers, Residential, Municipalities) Region, Key Players – Dynamics, Precision Agriculture IoT & Water Conservation Tech Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

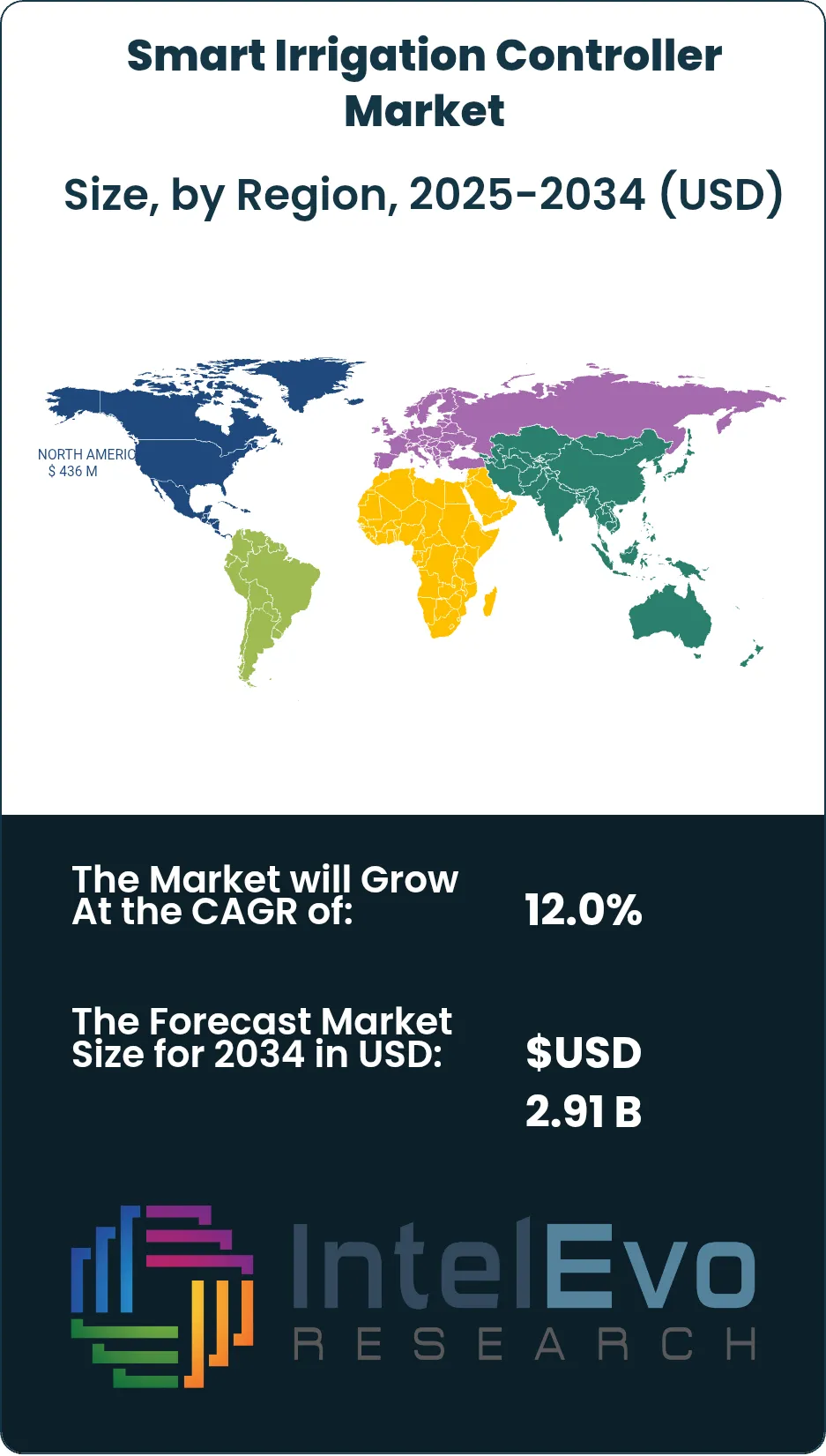

| USD 1.05 Billion | USD 2.91 Billion | 12.0% | North America, 41.5% |

The Smart Irrigation Controller Market was valued at USD 0.94 Billion in 2024 and is estimated to reach USD 1.05 Billion in 2025. The market is projected to reach USD 2.91 Billion by 2034, expanding at a CAGR of 12.0% during the forecast period (2026–2034). This represents an absolute dollar opportunity of USD 1.86 Billion across the analysis window.

Get More Information about this report -

Request Free Sample ReportAdoption is driven by water-scarcity policy, drought response in the U.S. Southwest, and the digital modernization of agricultural and landscape water management. Agriculture accounts for roughly 70% of global freshwater withdrawals, so any gain in scheduling precision translates into meaningful operating savings for farms, municipalities, and commercial property owners. The U.S. Environmental Protection Agency (EPA) WaterSense program continues to anchor U.S. residential and commercial demand, with WaterSense labeled controllers required to deliver a minimum 20% water saving versus standard clock-timer controllers under ANSI/ASABE Standard S627.

The regulatory environment for the smart irrigation controller market gained additional weight in late 2025. Directive (EU) 2025/2360, the EU Soil Monitoring Law, took force on December 16, 2025, requiring Member States to deploy harmonized soil-health monitoring within a three-year transposition window, indirectly accelerating procurement of soil-moisture-based controllers across the bloc. California's Sustainable Groundwater Management Act compliance deadlines, drought-emergency rules under SB 606 and AB 1668, and EQIP cost-share assistance through USDA-NRCS continue to channel installer demand toward WaterSense-certified hardware.

Technology layers are consolidating around weather-based ET controllers, soil-moisture-based controllers, and hybrid systems that combine both inputs. Connectivity has shifted decisively toward Wi-Fi, cellular LTE-M, NB-IoT, and LoRaWAN backhaul, with cloud platforms displacing on-controller scheduling for commercial and large-residential deployments. Modern controllers integrating sensors and IoT connectivity have demonstrated water savings of up to 35% and operational cost reductions of 22% for large-scale farms, according to U.S. industry case-study data.

North America accounted for the largest revenue share at 41.5% in 2025, equivalent to roughly USD 436 Million, supported by a dense WaterSense-certified product portfolio, EQIP cost-sharing, and concentrated residential adoption across California, Texas, Florida, and Arizona. Asia Pacific is positioned as the fastest-growing region through 2034, propelled by India's Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) and its Per Drop More Crop component, which had brought roughly 21.69 lakh hectares under micro-irrigation coverage as of March 31, 2025 with central-government subsidies of 45% to 55% under the program.

The forward outlook through 2034 hinges on three conditions: continued falls in module cost for cellular and LoRaWAN telemetry; broadening compliance demand from California Sustainable Groundwater Management Act enforcement and the EU Soil Monitoring Law transposition cycle; and intensifying consolidation among irrigation OEMs. Rain Bird Corporation, Hunter Industries Inc., The Toro Company, and Netafim Ltd. retain leading positions, and Rain Bird's October 1, 2025 ownership of Rachio Inc. has reset competitive dynamics across both the residential smart-controller and connected-home channels.

Market Definition & Scope

The global smart irrigation controller market comprises automated devices that schedule and adjust irrigation runtimes using real-time inputs from local weather stations, soil moisture sensors, evapotranspiration models, or some combination of these inputs, in place of fixed clock-based scheduling. The market encompasses weather-based irrigation controllers (WBICs) certified under ANSI/ASABE S627, soil-moisture-based controllers (SMBICs), hybrid weather-plus-sensor controllers, and the cellular, Wi-Fi, NB-IoT, and LoRaWAN modules that connect controllers to cloud scheduling platforms.

Scope inclusions cover controller hardware, embedded telemetry units, the cloud subscription services bundled at point of sale, and the rain, freeze, and flow-detection accessories that earn the WaterSense label when paired with the base controller. Excluded items include standalone clock-based timers without smart logic, manually operated valves, micro-irrigation hardware (drip line, emitters, sprinkler heads) sold separately from the controller, and pump VFD packages used in agricultural booster systems. The parent market is the broader smart irrigation segment, valued at roughly USD 2.0 Billion in 2025; smart irrigation controllers represent approximately 52% of that parent.

, By Connectivity (Wi-Fi, Bluetooth, Cellular, LoRaWAN), By Application (Agriculture, Residential & Commercial Landscaping, Golf Courses), By End-User (Farmers, Residential, Municipalities) Region, Key Players – Dynamics, Precision Agriculture IoT & Water Conservation Tech Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The smart irrigation controller market reached USD 1.05 Billion in 2025 and is projected to climb to USD 2.91 Billion by 2034 at a 12.0% CAGR, an absolute dollar opportunity of USD 1.86 Billion.

- Segment Dominance (Type): Weather-based controllers led with 56.0% revenue share in 2025, equivalent to roughly USD 588 Million.

- Segment Dominance (Application): Agriculture commanded 56.0% share at USD 588 Million in 2025, anchored by row-crop and specialty-horticulture deployments.

- Driver: Drought policy and water-rate inflation are the primary growth drivers, with WaterSense-labeled controllers delivering verified water savings of at least 20% per ANSI/ASABE S627 certification, and field-reported savings of 30% to 50% in California and Arizona households.

- Restraint: Subscription fees of USD 30 to USD 200 per year for cloud-platform features and WiFi connectivity dependence continue to slow adoption among rural smallholders without reliable broadband.

- Opportunity: The trailing nine-year window offers an absolute dollar opportunity of USD 1.86 Billion, concentrated in cellular and NB-IoT controllers (forecast to grow at roughly 16.5% CAGR) and agricultural deployments under EU Soil Monitoring Law transposition.

- Trend: Wi-Fi and cloud-connected controllers captured an estimated 52.0% of unit shipments in 2025, with cellular and NB-IoT variants the fastest-growing connectivity tier.

- Regional: North America held 41.5% revenue share at approximately USD 436 Million in 2025, supported by EPA WaterSense certification, USDA EQIP cost-sharing, and state-level mandates including California SB 606 and AB 1668.

Key Insights Summary

- On October 1, 2025, Rain Bird Corporation closed its acquisition of Rachio, Inc., the cloud-connected smart-controller specialist founded in Denver, Colorado in 2013, integrating Rachio as a wholly owned subsidiary under continued leadership of co-founder Chris Klein.

- On December 16, 2025, Directive (EU) 2025/2360 (Soil Monitoring Law) took force, requiring all 27 EU Member States to deploy harmonized soil-health monitoring within a three-year transposition window, with downstream procurement implications for soil-moisture-based controllers across the bloc.

- Per the EPA WaterSense program, replacing a standard clock-based controller with a labeled weather-based controller can save an average U.S. home up to 15,000 gallons of water annually; if every home with an in-ground sprinkler system installed one, the U.S. would save up to USD 4.5 Billion in water costs and 390 Billion gallons annually.

- Under India's PMKSY Per Drop More Crop component, roughly 21.69 lakh hectares had been brought under micro-irrigation as of March 31, 2025, with the program extended through 2026 at an expanded outlay of approximately ₹93,068 crore including ₹37,454 crore in central assistance.

- On December 8, 2025, The Toro Company closed the acquisition of Tornado Infrastructure Equipment Ltd. for USD 279 Million Canadian dollars, broadening its underground-construction portfolio and reinforcing its dual-engine strategy across smart irrigation and infrastructure equipment.

- In Q4 2025, parent company Orbia engaged Evercore to manage a sale process for Israeli irrigation pioneer Netafim Ltd., with prospective valuations of USD 1.3 Billion to USD 1.5 Billion versus the USD 1.8 Billion paid in 2017, reported by Calcalist on October 15, 2025.

Competitive Landscape Overview

The global smart irrigation controller market is moderately consolidated. Rain Bird Corporation, Hunter Industries Inc., The Toro Company, and Netafim Ltd. collectively held an estimated 33% to 38% of revenue in 2025, with HydroPoint Data Systems, Valmont Industries (Valley Irrigation), Lindsay Corporation, Galcon, Weathermatic, and Orbit Irrigation rounding out the top tier. Competition is technology-led at the upper end, where vendors compete on cloud-platform sophistication, ANSI/ASABE S627 conformance, and the breadth of integration with soil moisture sensors, weather stations, and farm management software.

The competitive structure shifted noticeably during 2024 and 2025. Rain Bird closed its purchase of Rachio Inc. on October 1, 2025, layering connected-home capability and direct-to-consumer reach on top of its century-old contractor channel. The Toro Company finalized the USD 279 Million Canadian dollar Tornado Infrastructure acquisition on December 8, 2025 and announced an exclusive partnership with TerraRad for soil-moisture sensing tied to its irrigation control software. Orbia engaged Evercore in Q4 2025 to manage a sale process for Netafim, valuing the Israeli irrigation specialist at USD 1.3 Billion to USD 1.5 Billion. Lindsay Corporation closed its 49.9% minority interest in Pessl Instruments on January 6, 2025, and integrated METOS soil and weather monitoring with its FieldNET platform.

Competitive Landscape Matrix:

| Company | HQ | Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Rain Bird Corporation | United States | Leader | ESP-Me3, ESP-LXIVM, and Rachio 3 controllers | North America, Europe, Australia | Closed Rachio acquisition on October 1, 2025 |

| Hunter Industries Inc. | United States | Leader | Hydrawise, X-Core, and ACC2 controller families | North America, Europe, Asia Pacific | Continued Hydrawise platform expansion through 2025 |

| The Toro Company | United States | Leader | Lynx, Sentinel, and EVOLUTION smart controllers | North America, Australia | Closed Tornado acquisition for USD 279M CAD on December 8, 2025 |

| Netafim Ltd. (Orbia) | Israel | Leader | NetBeat digital irrigation platform | Asia Pacific, Latin America, EMEA | Sale process initiated by parent Orbia in Q4 2025 |

| HydroPoint Data Systems | United States | Challenger | WeatherTRAK ET Pro3 series | North America | Continued enterprise SaaS growth across municipal accounts |

| Valmont Industries (Valley) | United States | Challenger | Valley 365 cloud control platform | North America, Latin America | Maintained pivot-control integration partnerships |

| Lindsay Corporation | United States | Challenger | FieldNET Advisor irrigation control | North America, Europe, Australia | Closed 49.9% stake in Pessl Instruments on January 6, 2025 |

| Galcon | Israel | Niche Player | Galileo Cloud and BT-series controllers | EMEA, Asia Pacific | Broadened greenhouse-fertigation channel partnerships |

| Weathermatic | United States | Niche Player | SmartLine SL series | North America | Sustained commercial-landscape contract base |

| Orbit Irrigation Products | United States | Niche Player | B-hyve Wi-Fi controller series | North America | Maintained retail distribution leadership in residential channel |

Segmentation Analysis

The global smart irrigation controller market segments by type, connectivity, application, and end-user. Each segmentation reveals distinct adoption curves, pricing dynamics, and competitive structure across the 2025-2034 forecast period.

By Type

Weather-based irrigation controllers (WBICs) led the smart irrigation controller market with 56.0% revenue share in 2025, equivalent to approximately USD 588 Million. WBICs ingest local weather data, evapotranspiration values, and landscape conditions to tailor watering schedules in place of fixed clock schedules, and the dominant designs comply with ANSI/ASABE S627 to qualify for EPA WaterSense certification. Rain Bird's ESP-Me3 and ESP-LXIVM, Hunter Industries' Hydrawise platform, The Toro Company's EVOLUTION series, and HydroPoint's WeatherTRAK ET Pro3 anchor the segment. Compared with sensor-based controllers, WBICs require lower upfront installation effort because they avoid in-ground probe deployment, which has supported their dominance among residential and small-commercial customers.

Soil-moisture-based controllers held 31.5% share at roughly USD 331 Million in 2025 and remain preferred for high-value horticulture, athletic turf, and protected cultivation where root-zone water content drives runtime decisions directly. Hybrid weather-plus-sensor controllers accounted for 12.5% share at USD 131 Million and represent the fastest-growing sub-segment through 2034 at an estimated 14.8% CAGR, with vendors bundling soil moisture inputs from CropX, METER Group, or Sentek probes alongside ET-based scheduling logic. Type sub-segment shares total 100.0%.

By Connectivity

Wi-Fi and cloud-connected controllers captured 52.0% of revenue in the smart irrigation controller market at approximately USD 546 Million in 2025, anchored by residential and small-commercial deployments where home broadband is the default. Cellular LTE-M and NB-IoT controllers accounted for 18.5% at USD 194 Million and represent the fastest-growing connectivity tier through 2034, supported by lower module pricing, broader carrier coverage, and the operational independence that cellular offers in fields without Wi-Fi.

LoRaWAN and mesh-based controllers held 12.0% share at USD 126 Million in 2025, with traction concentrated in larger agricultural deployments and municipal-scale landscape installations, while wired and local-only controllers retained 17.5% share at USD 184 Million. The Reinke-CropX integration disclosed in November 2025, which now bundles a complimentary CropX sensor with every new Reinke pivot, illustrates how cellular-backhauled controllers are increasingly procured as default peripherals on new irrigation infrastructure rather than as aftermarket upgrades. Connectivity sub-segment shares sum to 100.0%.

By Application

Agriculture led the smart irrigation controller market with 56.0% revenue share at USD 588 Million in 2025, encompassing both open-field row crops and protected cultivation across China, the United States, India, Spain, Brazil, and Israel. Center pivot and drip irrigation platforms remain the dominant insertion point for agricultural smart controllers, with Lindsay Corporation's FieldNET, Valmont Industries' Valley 365, and Netafim's NetBeat anchoring the field-scale controller category. Residential lawn and landscaping took 22.0% share at USD 231 Million and continues to expand under EPA WaterSense certification, municipal rebate programs, and state-level mandates such as California SB 606 and AB 1668.

Commercial landscape (golf courses, hotels, parks, and homeowner-association common areas) accounted for 14.5% share at USD 152 Million in 2025, with HydroPoint Data Systems and Weathermatic holding strong positions in enterprise SaaS-based irrigation management. Sports turf and municipal applications captured 7.5% share at USD 79 Million, including stadium and university-campus deployments. Application sub-segment shares total 100.0%.

By End-User

Large commercial farms held 32.0% revenue share at approximately USD 336 Million in the smart irrigation controller market in 2025, propelled by economies of scale across center-pivot and drip-irrigated row-crop operations. Residential homeowners accounted for 28.0% at USD 294 Million, with Rachio Inc. (now under Rain Bird ownership), Orbit Irrigation's B-hyve, and Hunter Industries' Hydrawise dominant in the consumer channel. Commercial property managers took 17.0% at USD 179 Million, municipal and public-sector buyers 13.0% at USD 137 Million, and mid-sized and smallholder farms 10.0% at USD 105 Million.

The municipal and public-sector sub-segment is set to gain share through 2034 as California Sustainable Groundwater Management Act enforcement and EU Soil Monitoring Law transposition pull water-monitoring procurement into city, county, and Member-State agency budgets. Smallholder demand in India and Sub-Saharan Africa is rising on the back of PMKSY subsidies of 45% to 55% under Per Drop More Crop and donor-funded micro-irrigation pilots. End-user sub-segment shares sum to 100.0%.

Regional Analysis

The global smart irrigation controller market spans North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, with regional shares summing to 100.0%.

North America

North America led the smart irrigation controller market with 41.5% revenue share in 2025, equivalent to USD 436 Million. The United States accounted for the bulk of regional demand, with Canada and Mexico contributing supporting volumes. EPA WaterSense certification, ANSI/ASABE S627 conformance for weather-based controllers, USDA-NRCS Environmental Quality Incentives Program (EQIP) cost-sharing for irrigation upgrades, and California-specific mandates under SB 606 and AB 1668 anchored procurement through 2025. Drought conditions across the Colorado River Basin, Central Valley, and Texas Panhandle continued to push contractors toward WaterSense-certified hardware. State-level rebate programs offered by water utilities (typically USD 75 to USD 200 per controller) further supported residential conversion.

Europe

Europe held 23.0% revenue share at USD 242 Million in the smart irrigation controller market in 2025. Spain, Italy, France, Germany, and the Netherlands anchor regional demand, with deployments concentrated in citrus, olive, viticulture, and protected horticulture. Directive (EU) 2025/2360 took force on December 16, 2025, with a three-year Member-State transposition window that requires harmonized soil-health monitoring at five-year minimum intervals. Common Agricultural Policy support payments and Horizon Europe's Mission Soil program (including AI4SoilHealth and TRAILS4SOIL projects) have channeled grant funding into reference sites that specify WaterSense-equivalent or sensor-coupled controllers. Spain alone accounts for an outsized share of European demand owing to its drip-irrigated horticulture exports.

Asia Pacific

Asia Pacific captured 22.5% revenue share at USD 236 Million in 2025 and is the fastest-growing regional market through 2034. India leads regional growth on the back of PMKSY Per Drop More Crop subsidies of 45% to 55%, the Micro Irrigation Fund (MIF) managed by NABARD with an initial corpus of ₹5,000 crore (with ₹4,719 crore sanctioned and ₹3,751 crore released to states as of May 2025), and the National Mission on Micro Irrigation. China contributes through state-supported smart agriculture projects across Heilongjiang, Shandong, and Sichuan. Japan's November 17, 2025 collaboration between Internet Initiative Japan and Sony Semiconductor Solutions Corporation extends satellite-connected soil moisture sensing into smart-farm pilot zones. Australia rounds out the region through specialty-crop and turf-management deployments.

Latin America

Latin America accounted for 7.0% revenue share at USD 73 Million in the smart irrigation controller market in 2025. Brazil dominates regional volumes through soybean, sugarcane, and citrus operations, while Mexico, Chile, and Peru contribute via greenhouse exports, wine-grape production, and avocado plantings respectively. Adoption stays concentrated among large estates because capital cost and connectivity gaps slow smallholder penetration. Brazilian agribusinesses have begun deploying CropX-integrated platforms across Mato Grosso and Goiás soybean operations, while Chilean exporters use Valmont and Lindsay center-pivot controllers in conjunction with Sentek probes for vineyard moisture management.

Middle East & Africa

Middle East and Africa held 6.0% revenue share at USD 63 Million in 2025. Israel, the United Arab Emirates, Saudi Arabia, South Africa, and Kenya lead regional deployments. Israeli vendor Netafim Ltd., headquartered in Tel Aviv, plays both domestic and export roles, and Galcon serves the regional small-controller and greenhouse segments. Gulf states have channeled sovereign-wealth funding into controlled-environment agriculture and saline-soil mitigation programs, where soil-moisture-based controllers measuring electrical conductivity carry premium relevance. Sub-Saharan deployments stay donor-driven, with World Bank and African Development Bank programs financing pilot smart-irrigation networks across Kenya, Ethiopia, Senegal, and Morocco.

Country Analysis

The global smart irrigation controller market concentrates around four national markets that together accounted for approximately 56% of 2025 revenue: the United States, India, China, and Spain.

United States

The United States smart irrigation controller market was valued at USD 365 Million in 2025 with a country-specific CAGR of 11.4% projected through 2034. EPA WaterSense certification under ANSI/ASABE S627 acts as the de-facto procurement gate for residential and commercial landscapes, with more than 28 Million U.S. homes operating in-ground sprinkler systems that remain candidates for retrofit. USDA-NRCS EQIP cost-sharing, California Sustainable Groundwater Management Act enforcement, California Senate Bill 606 and Assembly Bill 1668, and state-level rebate programs in Colorado, Nevada, Texas, and Florida sustain procurement. Rain Bird's October 1, 2025 acquisition of Rachio reinforces the U.S. as the dominant innovation cluster for the residential smart-controller category.

India

The Indian smart irrigation controller market reached USD 88 Million in 2025 with a country-specific CAGR of 15.2% through 2034, the fastest among the major national markets. PMKSY Per Drop More Crop subsidies cover 45% to 55% of indicative micro-irrigation system cost (with 65% available to SC/ST farmers under select state variants), and the program had brought 21.69 lakh hectares under micro-irrigation as of March 31, 2025. The Micro Irrigation Fund administered by NABARD targets approximately 22.22 lakh hectares with ₹4,719 crore sanctioned and ₹3,751 crore released to state governments by May 2025. Telangana's Indira Solar Giri Jal Vikasam scheme provides a 100% subsidy on solar-powered irrigation pumps with drip irrigation support, layering renewable-power demand on top of controller adoption.

China

The Chinese smart irrigation controller market was valued at USD 105 Million in 2025 with a country-specific CAGR of 13.8% through 2034. State-supported smart agriculture projects, soil-pollution remediation programs, and Ministry of Agriculture and Rural Affairs precision-farming subsidies anchor demand. Domestic OEMs in Shenzhen and Hangzhou have driven aggressive pricing on Wi-Fi controllers retailing under USD 100, while imported high-end controllers from Hunter Industries, Rain Bird, and Netafim hold preferred positioning in research stations and export-oriented horticulture. China's Smart Agriculture Projects continue funding controller-network buildouts across Heilongjiang, Shandong, and Sichuan grain-producing zones, supported by provincial-level cost-sharing programs.

Spain

The Spanish smart irrigation controller market reached USD 38 Million in 2025 with a country-specific CAGR of 12.6% through 2034. Demand stems from drip-irrigated citrus, olive, almond, and table-grape operations across Andalusia, Murcia, Valencia, and Castile-La Mancha, where summer-drought pressure has driven sustained procurement. Following the December 16, 2025 entry into force of Directive (EU) 2025/2360, Spain's central and autonomous-community governments are tasked with transposing the directive within three years, pulling forward sensor-coupled controller procurement. Spain's domestic vendor base remains modest, with imported controllers from Netafim, Rain Bird, Hunter Industries, and Galcon capturing the majority of installed base, supplemented by specialist greenhouse vendors.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Type

- Weather-Based Controllers

- Sensor-Based Controllers

- Hybrid Controllers

By Connectivity

- Wi-Fi

- Bluetooth

- Cellular

- LoRaWAN & LPWAN

- Others

By Application

- Agriculture

- Residential Landscaping

- Commercial Landscaping

- Golf Courses

- Sports Grounds

- Others

By End-User

- Farmers

- Residential Users

- Commercial Facilities

- Municipalities

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.05 B |

| Forecast Revenue (2034) | USD 2.91 B |

| CAGR (2025-2034) | 12.0% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type, (Weather-Based Controllers, Sensor-Based Controllers, Hybrid Controllers), By Connectivity, (Wi-Fi, Bluetooth, Cellular, LoRaWAN & LPWAN, Others), By Application, (Agriculture, Residential Landscaping, Commercial Landscaping, Golf Courses, Sports Grounds, Others), By End-User, (Farmers, Residential Users, Commercial Facilities, Municipalities, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | RAIN BIRD CORPORATION, HUNTER INDUSTRIES INC., THE TORO COMPANY, NETAFIM LTD., HYDROPOINT DATA SYSTEMS, INC., VALMONT INDUSTRIES, INC., LINDSAY CORPORATION, GALCON, WEATHERMATIC, ORBIT IRRIGATION PRODUCTS, LLC, RACHIO, INC., RIVULIS IRRIGATION LTD., BANYAN WATER, INC., JAIN IRRIGATION SYSTEMS LTD., CALSENSE, ET WATER SYSTEMS, INC., STORM IRRIGATION, INC., DELTA-T DEVICES LTD., BLOSSOM, NELSON IRRIGATION CORPORATION, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Connectivity (Wi-Fi, Bluetooth, Cellular, LoRaWAN), By Application (Agriculture, Residential & Commercial Landscaping, Golf Courses), By End-User (Farmers, Residential, Municipalities) Region, Key Players – Dynamics, Precision Agriculture IoT & Water Conservation Tech Trends & Forecast 2026-2034")

, By Connectivity (Wi-Fi, Bluetooth, Cellular, LoRaWAN), By Application (Agriculture, Residential & Commercial Landscaping, Golf Courses), By End-User (Farmers, Residential, Municipalities) Region, Key Players – Dynamics, Precision Agriculture IoT & Water Conservation Tech Trends & Forecast 2026-2034")

, By Connectivity (Wi-Fi, Bluetooth, Cellular, LoRaWAN), By Application (Agriculture, Residential & Commercial Landscaping, Golf Courses), By End-User (Farmers, Residential, Municipalities) Region, Key Players – Dynamics, Precision Agriculture IoT & Water Conservation Tech Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Smart Irrigation Controller Market?

Global Smart Irrigation Controller Market was valued at USD 0.94 billion in 2024 and is projected to reach USD 2.91 billion by 2034, at a CAGR of 12.0% (2026–2034).

Who are the major players in the Smart Irrigation Controller Market?

RAIN BIRD CORPORATION, HUNTER INDUSTRIES INC., THE TORO COMPANY, NETAFIM LTD., HYDROPOINT DATA SYSTEMS, INC., VALMONT INDUSTRIES, INC., LINDSAY CORPORATION, GALCON, WEATHERMATIC, ORBIT IRRIGATION PRODUCTS, LLC, RACHIO, INC., RIVULIS IRRIGATION LTD., BANYAN WATER, INC., JAIN IRRIGATION SYSTEMS LTD., CALSENSE, ET WATER SYSTEMS, INC., STORM IRRIGATION, INC., DELTA-T DEVICES LTD., BLOSSOM, NELSON IRRIGATION CORPORATION, Others

Which segments covered the Smart Irrigation Controller Market?

By Type, (Weather-Based Controllers, Sensor-Based Controllers, Hybrid Controllers), By Connectivity, (Wi-Fi, Bluetooth, Cellular, LoRaWAN & LPWAN, Others), By Application, (Agriculture, Residential Landscaping, Commercial Landscaping, Golf Courses, Sports Grounds, Others), By End-User, (Farmers, Residential Users, Commercial Facilities, Municipalities, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Smart Irrigation Controller Market

Published Date : 16 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date