- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Smart Meter Data Analytics Market Size, Share | CAGR 19.1%

Global Smart Meter Data Analytics Market Size, Share, Growth Analysis By Offering (Software, Managed Services, Hardware-Integrated Analytics), By Application (Revenue Protection, Load Forecasting, Grid Operations Analytics, Demand Response Optimization), By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User (Electric, Water, Gas Utilities), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 6.18 Billion | USD 29.74 Billion | 19.1% | North America, 36.8% |

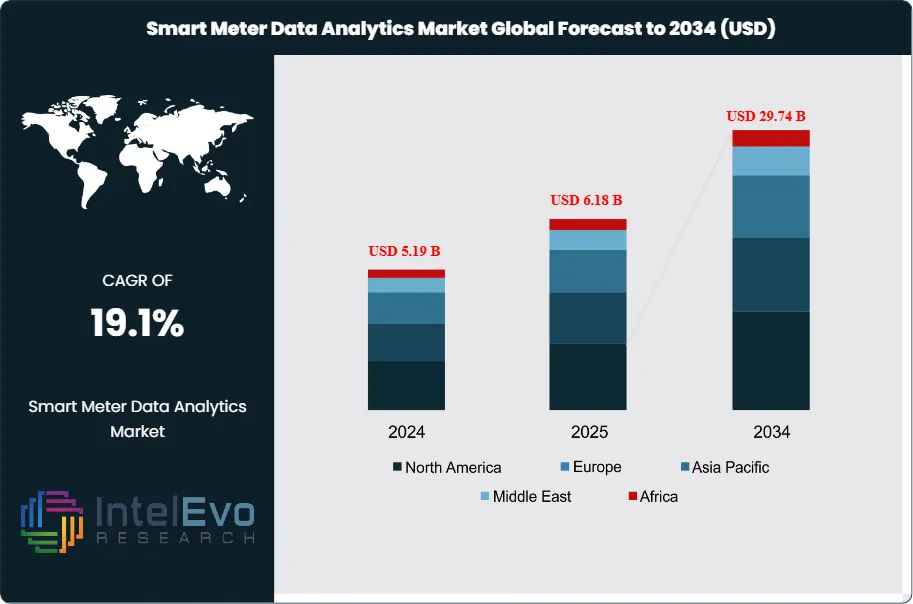

The Smart Meter Data Analytics Market was valued at approximately USD 5.19 Billion in 2024 and reached USD 6.18 Billion in 2025. The market is projected to grow to USD 29.74 Billion by 2034, expanding at a CAGR of 19.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 23.56 Billion over the analysis period, establishing Smart Meter Data Analytics as one of the most strategically important software and services categories within the broader utility technology and energy management sector.

Get More Information about this report -

Request Free Sample ReportSmart Meter Data Analytics encompasses the software platforms, algorithms, machine learning models, and managed services that process, interpret, and derive actionable intelligence from the interval consumption data, power quality signals, outage notifications, and tamper alerts generated by advanced metering infrastructure (AMI) deployments. A single smart meter generates between 3,000 and 35,000 data readings per year depending on interval granularity, and a utility with 5 million deployed meters produces data volumes comparable to a mid-sized social media platform, requiring purpose-built ingestion, storage, and analysis architectures. The analytical outputs of these systems, spanning revenue protection, load forecasting, customer segmentation, grid fault detection, demand response optimization, and non-technical loss identification, generate measurable financial value that utilities are increasingly able to quantify against platform licensing costs.

Three forces are driving structural market expansion through the forecast period. First, the global smart meter installed base is expanding at approximately 8.3% annually, with the IEA estimating 1.1 billion smart meters deployed globally by 2025, each requiring analytics infrastructure to convert raw interval data into utility operational value. Second, the integration of distributed energy resources, including rooftop solar, residential batteries, and electric vehicle chargers, onto distribution networks is generating bidirectional power flow complexity that conventional SCADA and billing systems cannot process, creating acute demand for advanced edge and cloud analytics. Third, utility regulators in the EU, United Kingdom, United States, and Australia are mandating data transparency and consumer access provisions that require utilities to invest in customer-facing analytics portals and data sharing APIs, expanding the analytics technology surface area beyond internal utility operations.

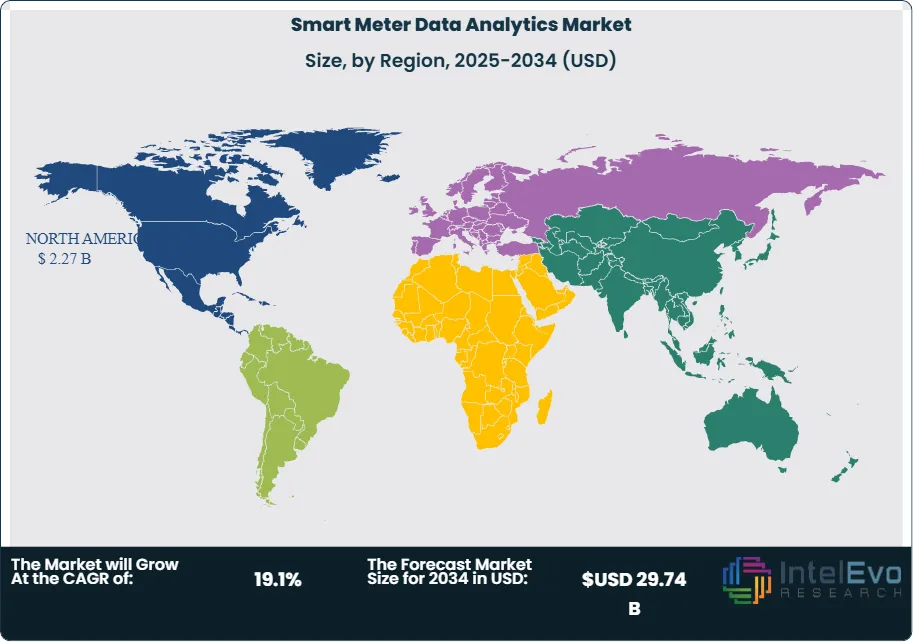

North America leads the global Smart Meter Data Analytics market at a 36.8% share in 2025, equivalent to approximately USD 2.27 Billion, driven by the maturity of U.S. AMI deployments and aggressive state-level utility commission incentive programs for grid modernization. Europe holds a 29.4% share, anchored by the EU's Smart Metering Directive and the United Kingdom's national smart meter rollout covering 30 million premises. Asia Pacific accounted for 24.7% of global Smart Meter Data Analytics revenue in 2025, with China's State Grid Corporation AMI expansion and Japan's post-Fukushima grid modernization program as primary demand sources. The competitive environment is intensifying, with cloud hyperscalers including Microsoft Azure, Amazon Web Services, and Google Cloud entering the utility analytics market through purpose-built energy data platforms, challenging established meter data management system vendors and creating new integration and partnership dynamics across the value chain.

, By Application (Revenue Protection, Load Forecasting, Grid Operations Analytics, Demand Response Optimization), By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User (Electric, Water, Gas Utilities), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global Smart Meter Data Analytics market reached USD 6.18 Billion in 2025 and is forecast to reach USD 29.74 Billion by 2034, expanding at a CAGR of 19.1% over the 2026–2034 forecast period.

- Segment Dominance: By offering, software solutions held the largest share at 58.3% of global Smart Meter Data Analytics revenue in 2025, driven by demand for meter data management systems, analytics platforms, and customer engagement applications that monetize AMI data investments already made by utilities.

- Segment Dominance: By application, revenue protection and non-technical loss detection accounted for the largest application share at 27.4% in 2025, reflecting utilities' priority to recover the estimated USD 96 Billion in annual global electricity losses attributable to theft, meter tampering, and billing errors detectable through interval data analysis.

- Driver: Accelerating AMI deployment globally, with the IEA estimating 1.1 billion smart meters installed by 2025 and 1.8 billion targeted by 2030, is generating exponentially growing data volumes that utilities cannot process with legacy billing and SCADA systems, creating structural demand for purpose-built analytics platforms.

- Restraint: Data privacy regulations including GDPR in Europe, CCPA in California, and utility-specific consumer data protection rules impose compliance overhead on Smart Meter Data Analytics platforms, requiring privacy-by-design architecture investments that increase development costs by an estimated 15–25% and create market access barriers for smaller analytics vendors.

- Opportunity: AI-driven predictive grid analytics, combining smart meter interval data with weather feeds, satellite imagery, and IoT sensor streams for distribution transformer load forecasting and fault prediction, represents an addressable platform upgrade opportunity estimated at USD 7.8 Billion by 2034 as utilities accelerate grid hardening investment in response to climate-driven outage frequency increases.

- Trend: Cloud-native, multi-utility data platform models are replacing on-premise meter data management system deployments as the dominant architecture in 2025, with SaaS-based analytics delivered as managed services achieving 34% annual subscription growth, reducing utility capital expenditure requirements while enabling continuous AI model updates without costly on-site software release cycles.

- Regional Analysis: North America leads the global Smart Meter Data Analytics market with a 36.8% share in 2025, representing approximately USD 2.27 Billion, supported by FERC Order 2222's distributed resource integration requirements and state utility commission mandates for AMI data utilization reporting.

Competitive Landscape Overview

The global Smart Meter Data Analytics market is moderately fragmented, with the top four vendors, Itron, Oracle Utilities, Landis+Gyr, and Honeywell (Forge Energy), collectively holding approximately 33.6% of global platform revenue in 2025. Competition operates across three distinct tiers: integrated AMI and analytics vendors that supply both hardware and software, pure-play analytics and meter data management system providers, and cloud hyperscaler platforms offering energy-sector data services. Competitive differentiation centers on data ingestion scalability, pre-built utility use case libraries, regulatory compliance automation, and the depth of AI model libraries for non-technical loss detection and demand forecasting. M&A activity accelerated in 2023–2025, with cloud platforms acquiring utility analytics specialists and meter hardware OEMs purchasing software firms to extend from device to data value. New entrants from the enterprise software sector, including Palantir Technologies and C3.ai, have entered utility analytics under energy transition positioning, intensifying competition for large utility enterprise contracts.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Platform | Geographic Strength | Recent Strategic Move (2024–2026) |

| Itron | USA | Leader | Itron Riva Intelligence Platform | North America / Europe | Launched Riva AI Forecasting module with 15-minute interval demand prediction; signed 8-year AMI analytics contract with Pacific Gas & Electric (Jan 2025). |

| Oracle Utilities | USA | Leader | Oracle Utilities Analytics Cloud | North America / Asia Pacific | Released Oracle Energy and Water Analytics 24.1 with generative AI demand-response optimization; expanded to 14 new utility clients in APAC (Mar 2025). |

| Landis+Gyr | Switzerland | Leader | Gridstream Analytics Suite | Europe / North America | Acquired Enbala Power Networks' demand flexibility analytics assets; integrated into Gridstream cloud platform for VPP dispatch (Dec 2024). |

| Honeywell (Forge Energy) | USA | Leader | Honeywell Forge Energy Optimization | North America / MEA | Deployed Forge Energy at 3 GCC utility clients covering 4.2M meters; launched Arabic-language customer engagement module (Sep 2025). |

| Aclara (Hubbell) | USA | Challenger | Aclara STAR Network Analytics | North America | Extended STAR Analytics platform with AI-driven non-technical loss detection across 6 new U.S. investor-owned utility clients (Jun 2025). |

| Siemens (EnergyIP) | Germany | Challenger | Siemens EnergyIP MDMS | Europe / Asia Pacific | Upgraded EnergyIP with Azure OpenAI integration for automated meter event classification; expanded to Indian utility clients (Apr 2025). |

| Bidgee (formerly Bidgely) | USA | Challenger | UtilityAI Platform | North America / Europe | Signed partnership with E.ON UK for AI-driven EV load disaggregation across 3.8M smart meters; expanded UtilityAI to Australia (Oct 2025). |

| Enercomp / AutoGrid | USA | Niche Player | AutoGrid Flex Platform | North America | AutoGrid Flex VPP analytics deployed by 4 U.S. co-ops for demand response aggregation covering 280,000 enrolled endpoints (Jan 2026). |

| Powerley | USA | Niche Player | Powerley Energy Management Platform | North America | Partnered with DTE Energy to deploy AI home energy advisor to 900,000 residential smart meter customers (Feb 2026). |

By Offering:

The software segment dominates the global Smart Meter Data Analytics market with a 58.3% share in 2025, approximately USD 3.60 Billion, reflecting the ongoing shift from raw meter data collection toward value-added analytics platforms that convert interval data into operational intelligence. Within the software segment, meter data management systems (MDMS) form the foundational data processing layer, validating, estimating, and editing interval data before routing it to downstream applications. Purpose-built MDMS platforms from vendors including Itron, Oracle Utilities, and Siemens EnergyIP typically process 15-minute interval reads from millions of endpoints, applying data quality rules and gap-filling algorithms before exposing clean datasets to analytics applications via APIs. Advanced analytics and artificial intelligence applications built on MDMS foundations represent the fastest-growing software sub-category, with AI-driven platforms for non-technical loss detection, load disaggregation, demand response optimization, and predictive maintenance achieving an estimated 28% compound growth within the software segment in 2024–2025. Customer engagement and energy advisory applications, including web and mobile portals that present household-level consumption insights to residential customers, accounted for approximately 22% of software segment revenue in 2025 and are increasingly required by utility regulators as a condition of AMI deployment approval.

The services segment held a 31.4% share of the global Smart Meter Data Analytics market in 2025, approximately USD 1.94 Billion, encompassing managed analytics services, system integration, data engineering, and consulting engagements. Managed services, where the vendor operates the analytics platform on behalf of the utility and delivers processed outputs through dashboards and APIs, are the fastest-growing services sub-category, growing at approximately 24% annually as smaller and mid-sized utilities without large IT organizations seek to access analytics capabilities without building internal data science teams. Hardware-integrated analytics, where analytics processing occurs at the edge within the meter or communication gateway device itself, accounted for the remaining 10.3% of market revenue in 2025. Edge analytics is growing in importance as utilities seek to reduce cloud data transmission costs and achieve sub-second response times for grid fault detection applications.

By Application:

Revenue protection and non-technical loss detection represent the highest-priority and most immediately monetizable application of Smart Meter Data Analytics platforms, accounting for 27.4% of global application revenue in 2025, approximately USD 1.69 Billion. Non-technical losses attributable to electricity theft, meter tampering, billing errors, and metering fraud are estimated at 8–12% of total electricity distributed in developing markets and 1–3% in mature markets, representing a global annual financial loss of approximately USD 96 Billion. Smart meter interval data enables detection of tamper events through voltage sag signatures, unusual consumption patterns, and communication anomalies that legacy monthly-read meters cannot identify. Utilities deploying AI-driven NTL detection platforms report recovery rates of USD 2–USD 8 per meter per year in lost revenue, providing clear and measurable return on analytics platform investment that accelerates procurement decisions.

Load forecasting applications accounted for 22.1% of market revenue in 2025, valued at approximately USD 1.37 Billion, with machine learning models trained on smart meter interval data achieving demand forecast accuracy improvements of 15–30% over traditional econometric models at the distribution circuit and substation level. Grid operations analytics, encompassing outage detection, power quality monitoring, and distribution transformer load management, held an 18.6% share in 2025 and is growing rapidly as utilities face increasing grid stress from EV charging loads and rooftop solar intermittency. Customer engagement applications accounted for 16.8% of revenue, while demand response optimization platforms represented 15.1%, covering virtual power plant dispatch, time-of-use tariff optimization, and demand flexibility program management.

By Deployment Mode:

Cloud deployment has become the dominant mode for new Smart Meter Data Analytics platform implementations, holding a 52.4% share of new contract revenue in 2025, valued at approximately USD 3.24 Billion. Cloud-native analytics platforms offer utilities the ability to scale data ingestion capacity elastically as AMI deployments expand without capital expenditure on server infrastructure, and to receive continuous AI model updates without on-site software release cycles. Microsoft Azure, Amazon Web Services, and Google Cloud have each established utility-specific cloud environments with pre-configured AMI data ingestion connectors, regulatory compliance frameworks including SOC 2 Type II and ISO 27001, and integration with their respective AI and machine learning services. On-premise deployment retained a 29.8% share in 2025, concentrated among large utilities with established data center infrastructure, data sovereignty requirements, or regulatory restrictions on cloud data transfer. Hybrid architectures, where edge and on-premise analytics handle real-time grid operations while cloud platforms process historical analytics and customer applications, accounted for the remaining 17.8% of market revenue and represent the fastest-growing deployment model at approximately 27% annual growth.

By End-User:

Electric utilities represent the dominant end-user category for Smart Meter Data Analytics solutions, accounting for 74.6% of global market revenue in 2025, approximately USD 4.61 Billion. Electric AMI deployments are the most analytically complex and data-rich, generating interval reads, power quality signals, voltage measurements, and grid event notifications that support a broad range of analytics applications from billing accuracy to grid fault detection. Water utilities held a 14.8% share in 2025, valued at approximately USD 914 Million, with smart water meter analytics focused on leak detection, consumption anomaly identification, and demand forecasting for reservoir and treatment plant capacity management. Gas utilities accounted for the remaining 10.6%, with analytics applications centered on consumption pattern analysis for safety monitoring, theft detection, and supply network pressure optimization.

Regional Analysis

North America

North America leads the global Smart Meter Data Analytics market with a 36.8% share in 2025, representing approximately USD 2.27 Billion in revenue, reflecting the region's mature AMI infrastructure base and aggressive utility investment in data analytics capabilities. The United States accounts for approximately 87% of North American market revenue, supported by an installed base of approximately 115 million smart electric meters, representing 75% of all U.S. electric meters, following two decades of AMI deployment investment by investor-owned utilities, electric cooperatives, and municipal utilities. The Edison Electric Institute estimates U.S. utilities invested USD 85 Billion in grid modernization from 2015 to 2024, of which AMI and associated analytics infrastructure represented approximately USD 22 Billion. FERC Order 2222's mandate for distributed energy resource aggregation in wholesale markets requires utilities to develop metering and analytics capabilities that can identify and dispatch enrolled flexible loads, creating a regulatory demand signal for advanced analytics investment beyond traditional utility operations. State utility commission incentive programs for AMI data utilization are an important driver: California's Public Utilities Commission, New York's Public Service Commission, and Illinois' Future Energy Jobs Act each include provisions rewarding utilities for demonstrable analytics-driven operational improvements. Canada's Clean Electricity Regulation and provincial smart grid investment programs in Ontario, British Columbia, and Alberta contribute secondary market demand, with Ontario alone targeting full AMI coverage of its 5 million electricity customers by 2027.

Europe

Europe held a 29.4% share of the global Smart Meter Data Analytics market in 2025, approximately USD 1.82 Billion, driven by the EU's Smart Metering Directive mandating cost-effective smart meter rollout across member states and the UK's national smart meter program targeting 30 million premises. The EU's Electricity Market Directive requires member states to deploy smart meters to at least 80% of consumers where cost-benefit analyses demonstrate positive returns, a threshold already met in most Western European markets, creating a growing installed base requiring analytics investment. The United Kingdom is Europe's most advanced Smart Meter Data Analytics market, with a dedicated Data Communications Company (DCC) operating the national smart metering data infrastructure and enabling third-party access to anonymized meter data for analytics and energy services. The DCC's central data platform, connecting 30 million smart meters across Great Britain, has spawned an ecosystem of analytics vendors including Hildebrand, Kaluza, and Green Running that develop consumer-facing and grid-facing applications on the DCC's open data architecture. Germany's AMI rollout, mandated under the Messstellenbetriebsgesetz (MsbG) for metered points above 6,000 kWh annually and all new installations from 2025, is driving MDMS and analytics platform investment among German distribution system operators. Scandinavian markets, with near-complete smart meter penetration in Sweden, Norway, and Finland, are advanced markets for second-generation analytics applications including flexibility market participation and EV integration management.

Asia Pacific

Asia Pacific accounted for 24.7% of the global Smart Meter Data Analytics market in 2025, approximately USD 1.53 Billion, with China and Japan as the two primary national markets and significant growth vectors in India, Australia, and South Korea. China's State Grid Corporation and China Southern Power Grid are operating the world's largest single-utility AMI deployments, with an estimated 550 million smart meters installed across China's national grid by 2025. China's State Grid has established dedicated big data analytics centers processing smart meter data for revenue protection, transformer load management, and demand forecasting at provincial and national levels, representing a substantial internal technology development investment that also creates commercial opportunities for analytics software vendors providing specialized AI modules. Japan's AMI rollout, accelerated by the Fukushima nuclear accident-driven energy efficiency mandate, covers approximately 90% of Japan's 77 million electricity metering points, and Japan's liberalized retail electricity market since 2016 has created commercial demand for customer analytics platforms among new market entrant retailers. Australia's National Electricity Market regulatory framework, including the Australian Energy Regulator's consumer data right provisions, mandates utility data sharing with consumers and authorized third parties, driving analytics platform investment in Victoria, New South Wales, and Queensland. India's RDSS (Revamped Distribution Sector Scheme) program, backed by INR 3 Trillion in central government support, targets 250 million smart prepaid meter installations by 2026, creating one of the world's largest near-term AMI analytics market opportunities.

Latin America

Latin America held a 4.9% share of the global Smart Meter Data Analytics market in 2025, approximately USD 303 Million, with Brazil representing the dominant regional market. Brazil's National Electric Energy Agency (ANEEL) has mandated smart meter installation for all consumers above 30 kWh monthly by 2024 and full coverage by 2031, creating a multi-year AMI rollout that generates growing analytics demand. Enel Brasil and Energisa are the largest AMI deployers in Brazil and have invested in analytics platforms focused on non-technical loss reduction, where Brazilian utilities report losses of 12–18% of distributed energy annually in urban areas. Chile's electricity regulator CNE has integrated smart meter data reporting requirements into distribution company regulatory frameworks, with analytics applications for outage management and demand-side management gaining adoption among Chilean distribution utilities. Mexico's CFE (Comision Federal de Electricidad) operates a national smart meter rollout program targeting 20 million installations by 2028, with analytics investment concentrated on revenue protection given Mexico's historically high non-technical loss rates of 10–14%.

Middle East & Africa

The Middle East and Africa region accounted for 4.2% of the global Smart Meter Data Analytics market in 2025, approximately USD 260 Million, with the Gulf Cooperation Council states and South Africa as the primary markets. Saudi Arabia's SEC (Saudi Electricity Company) has deployed approximately 10 million smart meters as part of the Vision 2030 energy sector modernization program and is investing in analytics platforms for demand forecasting, customer segmentation, and grid operations optimization. The UAE's distribution utilities, including DEWA and Abu Dhabi Distribution Company, operate advanced AMI deployments integrated with smart city data platforms, and DEWA's analytics capabilities include real-time consumption monitoring, predictive meter failure detection, and customer-facing energy efficiency advisory services delivered through the DEWA app. South Africa's Eskom and municipal distributors face severe non-technical loss challenges, with electricity theft estimated at approximately 12–15% of distributed energy, creating urgent demand for AI-driven revenue protection analytics. The African Development Bank's energy access programs and smart grid investment initiatives in Kenya, Ghana, and Nigeria are creating early-stage AMI and analytics market opportunities in sub-Saharan Africa, though deployment timelines remain constrained by grid infrastructure investment needs.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software (Meter Data Management Systems, Advanced Analytics and AI Platforms, Customer Engagement Applications)

- Services (Managed Analytics Services, System Integration, Data Engineering and Consulting)

- Hardware-Integrated Analytics (Edge Analytics, Gateway Processing)

By Application

- Revenue Protection and Non-Technical Loss Detection

- Load Forecasting and Demand Planning

- Grid Operations Analytics (Outage Detection, Power Quality, Transformer Management)

- Customer Engagement and Energy Advisory

- Demand Response and Flexibility Optimization

By Deployment Mode

- Cloud

- On-Premise

- Hybrid

By End-User

- Electric Utilities

- Water Utilities

- Gas Utilities

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.18 B |

| Forecast Revenue (2034) | USD 29.74 B |

| CAGR (2025-2034) | 19.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Software (Meter Data Management Systems, Advanced Analytics and AI Platforms, Customer Engagement Applications), Services (Managed Analytics Services, System Integration, Data Engineering and Consulting), Hardware-Integrated Analytics (Edge Analytics, Gateway Processing)), By Application, (Revenue Protection and Non-Technical Loss Detection, Load Forecasting and Demand Planning, Grid Operations Analytics (Outage Detection, Power Quality, Transformer Management), Customer Engagement and Energy Advisory, Demand Response and Flexibility Optimization), By Deployment Mode, (Cloud, On-Premise, Hybrid), By End-User, (Electric Utilities, Water Utilities, Gas Utilities) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ITRON, ORACLE UTILITIES, LANDIS+GYR, HONEYWELL (FORGE ENERGY), ACLARA (HUBBELL), SIEMENS (ENERGYIP), BIDGELY, AUTOGRID (SCHNEIDER ELECTRIC), POWERLEY, EATON (BRIGHTLAYER UTILITIES), ELSTER (HONEYWELL SMART ENERGY), SENSUS (XYLEM), TRILLIANT NETWORKS, INCLINA (FORMERLY GRID4C), UPLIGHT, ARCADIA POWER, SILVER SPRING NETWORKS (S&T), C3.AI (ENERGY SUITE), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Revenue Protection, Load Forecasting, Grid Operations Analytics, Demand Response Optimization), By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User (Electric, Water, Gas Utilities), Industry Trends & Forecast 2026-2034")

, By Application (Revenue Protection, Load Forecasting, Grid Operations Analytics, Demand Response Optimization), By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User (Electric, Water, Gas Utilities), Industry Trends & Forecast 2026-2034")

, By Application (Revenue Protection, Load Forecasting, Grid Operations Analytics, Demand Response Optimization), By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User (Electric, Water, Gas Utilities), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Smart Meter Data Analytics Market?

The Global Smart Meter Data Analytics Market was valued at USD 5.19 Billion in 2024 and is projected to reach USD 29.74 Billion by 2034, growing at a CAGR of 19.1% from 2026 to 2034, driven by increasing smart grid deployments, rising adoption of advanced metering infrastructure, growing demand for real-time energy analytics, and advancements in AI-powered utility management and IoT-enabled smart meter technologies worldwide.

Who are the major players in the Smart Meter Data Analytics Market?

ITRON, ORACLE UTILITIES, LANDIS+GYR, HONEYWELL (FORGE ENERGY), ACLARA (HUBBELL), SIEMENS (ENERGYIP), BIDGELY, AUTOGRID (SCHNEIDER ELECTRIC), POWERLEY, EATON (BRIGHTLAYER UTILITIES), ELSTER (HONEYWELL SMART ENERGY), SENSUS (XYLEM), TRILLIANT NETWORKS, INCLINA (FORMERLY GRID4C), UPLIGHT, ARCADIA POWER, SILVER SPRING NETWORKS (S&T), C3.AI (ENERGY SUITE), Others

Which segments covered the Smart Meter Data Analytics Market?

By Offering, (Software (Meter Data Management Systems, Advanced Analytics and AI Platforms, Customer Engagement Applications), Services (Managed Analytics Services, System Integration, Data Engineering and Consulting), Hardware-Integrated Analytics (Edge Analytics, Gateway Processing)), By Application, (Revenue Protection and Non-Technical Loss Detection, Load Forecasting and Demand Planning, Grid Operations Analytics (Outage Detection, Power Quality, Transformer Management), Customer Engagement and Energy Advisory, Demand Response and Flexibility Optimization), By Deployment Mode, (Cloud, On-Premise, Hybrid), By End-User, (Electric Utilities, Water Utilities, Gas Utilities)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Smart Meter Data Analytics Market

Published Date : 23 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date