Global Smart Pet Care Technology Market Size, Share | CAGR 13.0%

Global Smart Pet Care Technology Market Size, Share, Analysis By Product (Smart Feeders, Trackers, Cameras), By Pet Type (Dogs, Cats, Others), By Technology (Artificial Intelligence - AI, IoT, GPS & RFID), By Application (Health Monitoring, Feeding, Tracking & Safety), By End-User (Pet Owners, Vet Clinics) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Tech Trends & Forecast 2026-2034

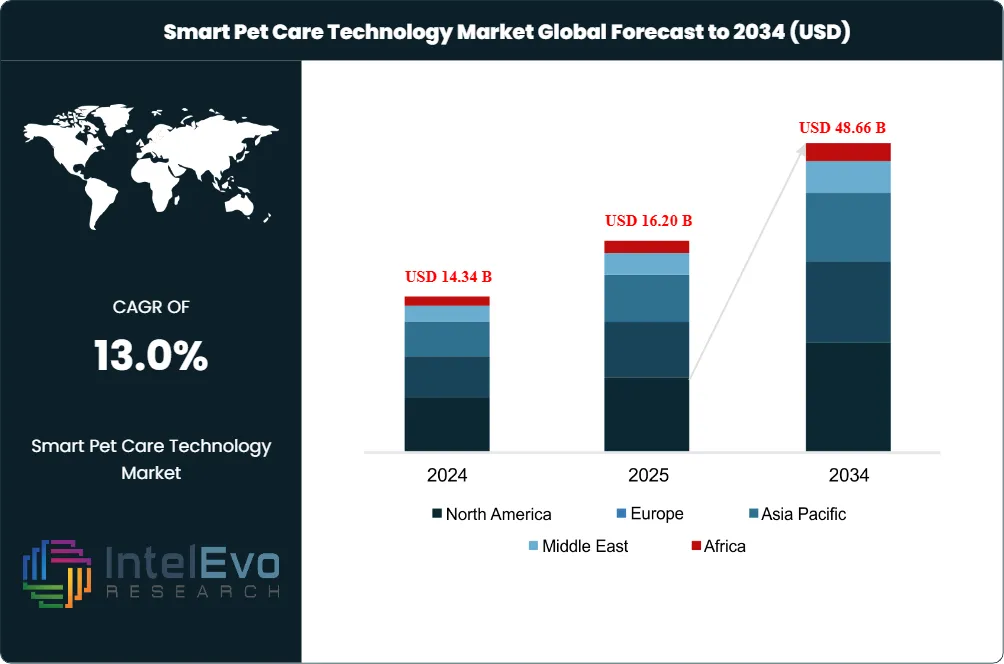

The Smart Pet Care Technology Market was valued at USD 14.34 Billion in 2024 and USD 16.20 Billion in 2025. The market is projected to reach USD 48.66 Billion by 2034, expanding at a CAGR of 13.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 32.46 Billion over the analysis period. Demand is anchored by 94 million U.S. pet-owning households disclosed by the American Pet Products Association in 2025 and by the EU's 127 million cats and 104 million dogs reported by the European Commission ahead of its June 2025 microchipping vote.

Premiumization within smart pet care technology is concentrated in three product clusters: GPS and health-monitoring wearables, AI-enabled cameras and feeders, and microchip-gated access devices. Wearables alone accounted for roughly 38.0% of 2025 revenue, lifted by Tractive's 1.4 million active subscribers and Halo Collar's projected USD 100 Million revenue year. Smart cameras and AI-feeders trail at a combined 25.0% share, while microchip-recognition products gained tailwind from the UK's June 2024 cat microchipping mandate and the European Parliament's June 19, 2025 vote to extend identification rules across all 27 member states.

Regulatory tailwinds are now structural to the smart pet care technology market. The EU's draft framework, building on 24 member states already requiring dog microchipping and 7 requiring cat microchipping, will compel ISO 11784/11785-compliant identification across an estimated 231 million dogs and cats. UK enforcement under DEFRA, with fines of up to GBP 500 for non-compliance, has converted what was a discretionary purchase into a regulated one. Insurance integration is the parallel demand engine, with Uelzener-Tractive subscription reimbursement signaling that European pet insurers now treat connected wellness data as a preventive-care input rather than a consumer accessory.

Asia Pacific is the fastest-growing region within smart pet care technology, projected to expand at a 15.5% regional CAGR through 2034. China's premiumization wave drove PETKIT's three-product CES 2026 launch and the March 27, 2026 debut of Pilo under the Dreame consumer-tech parent. Tariff exposure on China-sourced electronics has nudged manufacturers toward dual-sourcing in Vietnam and Mexico, particularly for feeders and litter robots destined for North American retail. The shift creates a 12-24 month rebalancing window for distributors negotiating private-label terms.

Forward to 2034, three vectors will define winners in the smart pet care technology market: subscription monetization tied to GPS connectivity, AI-driven preventive health analytics that veterinarians will accept as longitudinal evidence, and embedded-finance partnerships with pet insurers and employee benefit providers. The Wagmo-Fi February 24, 2026 employer-channel deal points to a new acquisition lane that lowers the customer-acquisition cost ceiling currently capping mass-market penetration.

Market Definition & Scope

The smart pet care technology market is defined as connected hardware, embedded software, and cloud-platform services that monitor, track, feed, contain, entertain, or diagnose companion animals through wireless connectivity (GPS, RFID, Bluetooth, Wi-Fi, LTE-M, or NB-IoT). The market encompasses smart collars and harnesses, GPS trackers, health-monitoring wearables, AI cameras, automated feeders and water fountains, microchip-gated doors and feeders, robotic litter systems, smart pet beds, and connected toys with companion mobile applications.

This analysis includes hardware revenue, recurring subscription fees for cellular connectivity and premium analytics, and ancillary cloud-service revenue tied to connected pet devices. Excluded from scope are non-digital pet accessories (traditional collars, leashes, plain feeders), pet food and treats, in-clinic veterinary diagnostic equipment, traditional pet insurance, and standalone training services without an embedded device. The smart pet care technology market sits within the parent global pet care market valued at USD 273.42 Billion in 2025 and represents approximately 5.9% of that parent today.

Key Takeaways

Market Growth: The smart pet care technology market expanded from USD 16.20 Billion in 2025 toward a projected USD 48.66 Billion by 2034, registering a 13.0% CAGR.

Segment Dominance (Product): Pet wearables (smart collars, GPS trackers, harnesses) commanded 38.0% of 2025 smart pet care technology revenue, anchored by GPS connectivity-led growth.

Segment Dominance (Application): Pet safety and tracking captured 40.0% of 2025 application revenue across the smart pet care technology market, ahead of health monitoring at 26.0%.

Driver: Pet humanization expenditure scaled to over 50% of pet owners ranking pet costs above discretionary personal spending in 2025, sustaining premium device adoption.

Restraint: Cost sensitivity affects roughly 46% of consumers who cite USD 100-USD 300 device prices and platform fragmentation as adoption barriers.

Opportunity: Insurance-linked subscription bundles represent a USD 4.5 Billion incremental opportunity through 2034, building on the Tractive-Uelzener March 2026 reimbursement model.

Trend: AI-feature integration appeared in roughly 58% of smart pet care technology product launches during 2025, displacing single-function GPS-only devices.

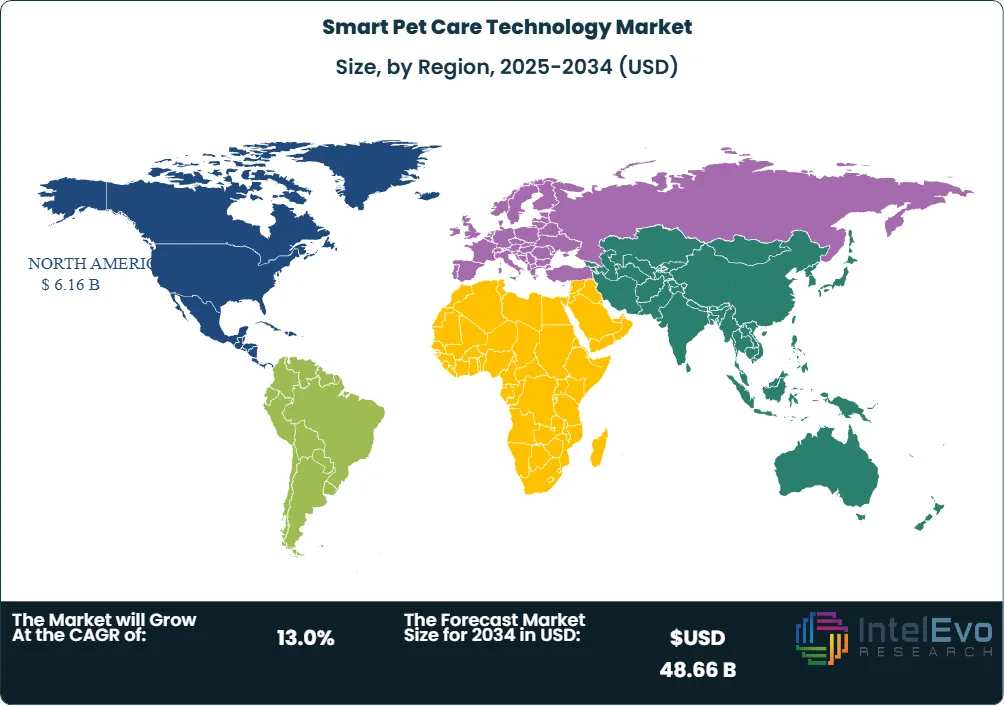

Regional: North America led the smart pet care technology market with 38.0% share and USD 6.16 Billion in 2025 revenue, supported by 70% U.S. household pet ownership.

Key Insights Summary

EU lawmakers backed mandatory microchipping for all dogs and cats on June 19, 2025, covering 127 million cats and 104 million dogs across 27 member states with combined annual sales of EUR 1.3 Billion.

On July 28, 2025, Austria-based Tractive closed its purchase of Whistle from Mars Petcare, folding Whistle's customer base into a connected-pet platform now serving 1.4 million active users.

Microchipping for owned cats over 20 weeks of age became enforceable across England under DEFRA Regulations 2023 from June 10, 2024, with non-compliance penalties reaching GBP 500.

Halo Collar booked roughly USD 75 Million in 2024 revenue and projected USD 100 Million for 2025 against a USD 400 Million Series B valuation, with installed base spanning 200,000 dogs across 350 breeds.

PETKIT received the Microsoft AI Innovation Award at CES 2026 in Las Vegas during January 2026, recognizing real-world deployment of Azure-backed pet-care AI inference.

Traini, an OpenAI- and ByteDance-alumnus team, secured USD 7.5 Million on December 29, 2025 to commercialize a cognitive smart collar trained on more than 900 peer-reviewed animal behavior studies and 2 million dog datasets.

Industry analysis indicates online and direct-to-consumer subscription channels are growing at 17.41% CAGR through 2031, against 56.10% offline retail share in the smart pet care technology market in 2025.

Competitive Landscape Overview

The smart pet care technology market is moderately fragmented, with the top four hardware-and-platform providers (Tractive, Radio Systems Corporation, Garmin, PETKIT) collectively holding an estimated 33% of 2025 revenue. Below this tier, the field divides into three lanes: GPS-and-wellness pure-plays (Halo, Fi, FitBark, PetPace), camera-and-feeder specialists (Furbo, Petcube, Petlibro, Litter-Robot), and microchip-access incumbents (Sure Petcare, SureFlap).

Competition is restructuring around platform consolidation rather than hardware differentiation. Tractive's Whistle absorption in July 2025 and the Pilo-Dreame backing announced March 27, 2026 both signal that scale players are buying connected user bases rather than building them. AI-feature parity at the device layer (heart-rate, respiratory-rate, scratching, bark-pattern monitoring) means the durable moat now sits in mobile-app retention, veterinary-data partnerships, and insurance reimbursement deals such as Tractive-Uelzener and Fi-Wagmo.

Competitive Landscape Matrix

Company

HQ

Position

Key Product

Geographic Strength

Recent Strategic Move

Tractive GmbH

Austria

Leader

GPS and health tracker collars (DOG 6, CAT 6 Mini)

Europe, expanding US

Took ownership of Whistle from Mars Petcare in July 2025

Radio Systems Corporation (PetSafe)

United States

Leader

Smart fences, feeders, water fountains, treat dispensers

North America retail dominance

Broadened product range across PetSmart and Petco shelves

Garmin Ltd.

Switzerland

Leader

Astro, Alpha, and Sport DOG GPS handhelds and collars

Capitalized on UK cat microchipping mandate since June 2024

Petlibro

United States / China

Niche Player

Granary feeders, refrigerated wet-food feeders

North America, Europe

Polar refrigerated wet-food feeder shipped through 2025

By Product Type

Smart pet wearables (collars, harnesses, vests, on-collar cameras) commanded 38.0% of 2025 smart pet care technology revenue and are projected to expand at a 13.6% CAGR through 2034. The category is dominated by Tractive (1.4 million active users), Garmin's Astro and Alpha lines, Halo Collar 5 with AlwaysOn GPS released September 2025, and Fi Series 3 and Fi Mini for cats and small dogs. Smart pet feeders and water fountains held 25.0% share, propelled by PETKIT's EVERSWEET ULTRA and YUMSHARE DAILY FEAST CES 2026 lineup, Petlibro's Polar refrigerated wet-food feeder, and Sure Petcare's microchip-gated bowls.

Interactive cameras and treat dispensers contributed 15.0% of 2025 smart pet care technology revenue, with Furbo 360°, Petcube Cam and Bites, and Enabot's EBO Air 2 (released March 2025) as anchors. Robotic litter systems and waste-management hardware reached 10.0%, projected to grow at 16.18% CAGR through 2031 per industry analysis, with Litter-Robot 4 and PETKIT PUROBOT CRYSTAL DUO leading. Microchip-access doors, smart pet beds, and connected toys made up the residual 12.0%, drawing direct benefit from regulatory traceability mandates.

By Pet Type

The dogs segment represented 62.0% of 2025 smart pet care technology revenue, reflecting product-design legacy (GPS collars, geofencing, activity tracking) built around canine outdoor behavior. Garmin's Sport DOG and Astro lines, Halo Collar 5, and Tractive's DOG 6 XL released April 8, 2026 illustrate the dog-first architecture of the category. Retained ownership of GPS-tracking subscriptions averages 18 months for dog products against 9 months for cat products, sustaining the segment's revenue dominance.

The cats segment reached 30.0% share in 2025 and is the fastest-growing pet type at 14.5% CAGR through 2034, propelled by Tractive's CAT 6 Mini debut in April 2026, the UK cat microchipping mandate effective June 10, 2024, and PETKIT's open-top PUROBOT CRYSTAL DUO cat litter robot. Fi Mini, weighing 18 grams, opened the under-25-pound category to cats and small dogs starting August 2025. Birds, fish, and small mammals together accounted for 8.0%, dominated by automated feeders and environmental sensors.

By Technology

GPS held 35.0% of smart pet care technology revenue in 2025, supported by LTE-M and NB-IoT integration that extended battery life past 30 days for low-frequency tracking. RFID and NFC accounted for 25.0%, anchored by ISO 11784/11785-compliant microchipping infrastructure that the EU framework will scale to 231 million pets. Bluetooth and Wi-Fi short-range systems represented 20.0%, deployed across in-home cameras and feeders, while AI/ML analytics layers sat at 12.0%, projected to expand at 14.92% CAGR through 2031 per industry analysis. Cellular and LPWAN connectivity made up the residual 8.0%.

By Application

Pet safety and tracking captured 40.0% of 2025 smart pet care technology application revenue, drawing on the American Humane Association estimate of 10 million U.S. pets going missing each year. Health and wellness monitoring sat at 26.0%, accelerating at 16.74% CAGR through 2031 per industry analysis, with vet-grade collars from PetPace 2.0 and Tractive's resting heart-rate monitoring driving share gains. Owner convenience (automated feeding, water dispensing, microchip-access doors) accounted for 20.0%, while entertainment and interactive engagement contributed 14.0%, anchored by Furbo and Petcube cameras.

By End-User

Households dominated the smart pet care technology market with 78.0% of 2025 revenue, reflecting tight integration into home Wi-Fi and smart-home platforms (Alexa, Google Home, Apple HomeKit). The commercial segment, comprising veterinary clinics, boarding facilities, daycare operators, and animal shelters, held 22.0% share. Veterinary-clinic adoption advanced through the Whistle Health+ platform launched October 2024, integrating wellness data into clinical workflows. Boarding facilities and pet daycares are projected to be the fastest-growing commercial sub-segment through 2034 as insurance-backed wellness monitoring extends to short-stay care.

Regional Analysis

North America led the global smart pet care technology market in 2025 with 38.0% share and USD 6.16 Billion in revenue, supported by 70% U.S. household pet ownership disclosed by the American Pet Products Association. The United States anchors the region with USD 4.47 Billion, propelled by 41% of dog owners deploying GPS-enabled trackers. Canada contributed approximately USD 0.81 Billion under a 12.7% projected CAGR through 2033 per aggregated industry estimates. Mexico added USD 0.88 Billion, with cross-border e-commerce flows from Petlibro and Furbo as primary distribution. Tariff exposure on China-sourced electronics has begun shifting feeder and litter-robot assembly to Vietnam and Mexico for the North American distribution lane.

Asia Pacific accounted for 26.0% of the smart pet care technology market in 2025, generating USD 4.21 Billion in revenue under the highest regional CAGR at 15.5% through 2034. China commanded USD 1.85 Billion, propelled by PETKIT's CES 2026 product lineup, the March 27, 2026 Pilo launch under Dreame's consumer-tech parent, and roughly 124 million urban pets per the China Pet Industry Association. Japan delivered USD 0.84 Billion, supported by aging demographics that favor automated feeding and indoor-camera monitoring. South Korea contributed USD 0.55 Billion, while India and Southeast Asia added USD 0.97 Billion combined, with India projected at a 28.0% national CAGR through 2034 per industry estimates.

Europe represented 21.0% of the smart pet care technology market in 2025 with USD 3.40 Billion in revenue. Germany led the region with USD 0.92 Billion, anchored by Tractive's headquarters in neighboring Austria and high consumer adoption of GPS trackers. The United Kingdom contributed USD 0.78 Billion, accelerated by the cat microchipping mandate enforceable since June 10, 2024 and DEFRA fines reaching GBP 500. France added USD 0.49 Billion, Italy USD 0.36 Billion, and the Netherlands USD 0.21 Billion, with the European Parliament's June 19, 2025 mandatory microchipping vote setting up bloc-wide harmonization across 27 member states.

Latin America held 8.0% of the smart pet care technology market in 2025, with USD 1.30 Billion in revenue. Brazil represented USD 0.66 Billion, the largest national market in the region, supported by half a billion dogs and cats across the U.S., Brazil, Europe, and China per the Global Pet Parent Study 2024. Mexico added USD 0.32 Billion, while Argentina, Chile, and Colombia together contributed USD 0.32 Billion. E-commerce penetration through Mercado Libre is the dominant distribution lane in the region.

Middle East and Africa captured 7.0% of the smart pet care technology market in 2025 with USD 1.13 Billion in revenue. The United Arab Emirates and Saudi Arabia together delivered USD 0.41 Billion, propelled by Vision 2030 pet-friendly urban planning. South Africa added USD 0.18 Billion. The remaining USD 0.54 Billion was distributed across Israel, Turkey, Egypt, and Sub-Saharan Africa, with adoption clustered in expat communities and high-net-worth households. Cross-border e-commerce from European brands dominates supply.

Country Analysis

The United States smart pet care technology market reached USD 4.47 Billion in 2025 with a 12.5% projected CAGR through 2034. Demand is anchored by 94 million pet-owning households per APPA's 2025 figures and by 41% of U.S. dog owners deploying GPS-enabled tracking devices. Federal microchipping is encouraged but not mandated, leaving identification adoption a state-by-state and shelter-driven function. The American Veterinary Medical Association's 2024 telehealth guidelines opened reimbursement pathways for connected-device data. Halo Collar's projected USD 100 Million 2025 revenue and Fi's February 24, 2026 Wagmo employer-benefits deal illustrate two distinct US-centric distribution channels: direct-to-consumer subscription and employer-funded pet benefits.

China's smart pet care technology market reached USD 1.85 Billion in 2025 with a 16.4% projected CAGR through 2034. The country's urban pet population, estimated at 124 million dogs and cats by the China Pet Industry Association, is concentrated in Tier 1 and Tier 2 cities where smart feeder and litter-robot adoption is highest. PETKIT's January 2026 CES launch and the March 27, 2026 Pilo emergence under Dreame's parent demonstrate that Chinese consumer-tech conglomerates now treat pet care as a smart-home extension. WeChat-integrated subscription models and JD.com same-day fulfillment have compressed the device-purchase-to-app-activation cycle to under 48 hours in major metros.

Germany's smart pet care technology market generated USD 0.92 Billion in 2025 with an 11.8% projected CAGR through 2034. Domestic distribution leans on tech-forward consumers willing to pay premium for GDPR-compliant data storage and EU-domiciled cloud infrastructure. Tractive, headquartered in Pasching, Austria, captures disproportionate German share due to language localization and Eurozone payment integration. Pet insurer Uelzener's March 17, 2026 partnership with Tractive, providing Tractive subscription reimbursement for eligible policyholders, opened a regulated reimbursement channel with no clear US analog. The German Federal Association of Pet Owners records pet ownership at 47% of households.

The United Kingdom smart pet care technology market reached USD 0.78 Billion in 2025 with a 12.6% projected CAGR through 2034. UK enforcement of the Microchipping of Cats and Dogs (England) Regulations 2023 since June 10, 2024 produced a 22% year-on-year jump in microchipping device shipments through DEFRA-approved databases. Sure Petcare, headquartered in Cambridge, dominates UK microchip-recognition feeders and cat flaps. The UK's stronger pet insurance penetration (over 30% of households per industry analysis) supports wearables that integrate with claims systems. Battersea Dogs Home reported 94% reunification rates for accurately microchipped dogs in 2021, a benchmark sustained through 2025.

By Product Type, (Smart Pet Feeders, Smart Pet Trackers, Smart Pet Cameras, Others), By Pet Type, (Dogs, Cats, Other Pets, Others), By Technology, (Artificial Intelligence (AI), Internet of Things (IoT), GPS & RFID, Others), By Application, (Health Monitoring, Feeding & Nutrition, Tracking & Safety, Others), By End-User, (Pet Owners, Veterinary Clinics, Pet Care Centers, Others),

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 176 SMART PET CARE TECHNOLOGY MARKET CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Player Analysis

Tractive GmbH holds the leadership position in the global smart pet care technology market by active subscriber base, with 1.4 million paying users worldwide as disclosed at the time of the Whistle deal. Founded in Pasching, Austria in 2012, the company anchors its revenue model on a hardware-plus-monthly-subscription bundle for GPS and health tracking, supported by LTE-M cellular partnerships across 175+ countries. The product line spans the DOG 6 XL and CAT 6 Mini introduced April 8, 2026, with collar-mounted resting heart-rate and respiratory-rate sensors that no other GPS-tracker has commercialized at consumer price points.

Tractive's strategic profile in 2025 was reshaped by closing the Whistle purchase from Mars Petcare on July 28, 2025, which converted a parallel-running US competitor into an integrated customer-migration channel. Whistle's connected wearable customer base transitioned to Tractive's platform with the legacy Whistle service shutting down August 31, 2025. The March 17, 2026 Uelzener insurance reimbursement deal in Germany and the April 2026 product refresh together signal a shift from hardware-only revenue to insurance-funded subscription, the highest-margin lane in the smart pet care technology market.

Radio Systems Corporation, marketed under the PetSafe brand and headquartered in Knoxville, Tennessee, holds a leading position based on installed base across North American retail. The portfolio spans wireless and in-ground containment fences, smart feeders, water fountains, treat-dispensing devices, and ScoopFree litter products. Radio Systems Corporation does not publicly disclose smart-device segment revenue, but the company holds a leading position based on installed base across PetSmart, Petco, and mass-merchant shelves where its product breadth exceeds direct-to-consumer specialists.

PetSafe's strategic differentiation in 2025 was the depth of its physical-retail moat. Where Tractive and Halo lean direct-to-consumer, PetSafe's omnichannel footprint allows it to bundle hardware with installer networks and big-box rebate programs that pure-play DTC brands cannot economically replicate. The ScoopFree Smart Spin Cat LitterBox, refreshed for the 2025 holiday cycle, illustrates the company's late-mover-but-mass-distribution playbook against Litter-Robot 4.

Garmin Ltd. (NYSE: GRMN), headquartered in Schaffhausen, Switzerland with operating headquarters in Olathe, Kansas, holds a leading position in the rugged GPS-tracking sub-segment of the smart pet care technology market through its Astro, Alpha, and Sport DOG product families. The Outdoor segment, which encompasses the pet GPS line, posted 29% revenue growth in Q4 2024 with USD 629.4 Million in quarterly revenue per the company's earnings release dated February 19, 2025. Garmin's outdoor segment generated USD 366.2 Million in Q1 2024 net sales per its 10-Q SEC filing.

Garmin's strategic position in 2025 drew on the Astro 900, Alpha 200i, and TT 25 collar architecture for hunting and field-trial use cases that consumer-electronics brands cannot match on durability, satellite connectivity, or multi-collar simultaneous tracking. Garmin does not publicly disaggregate pet GPS revenue, but the company holds a leading position based on installed base in the field-sport and working-dog category. Pricing premiums of USD 700-USD 1,200 for handheld-and-collar bundles sustain the highest gross margins in the smart pet care technology market.

PETKIT, headquartered in Shanghai with a global product office in Wuxi, holds the leadership position in Asia Pacific smart pet care technology and is the most product-broad consumer-tech entrant from China. The 2026 lineup spans EVERSWEET ULTRA automatic water fountains, YUMSHARE DAILY FEAST robotic wet-food feeders, and PUROBOT CRYSTAL DUO open-top automatic litter boxes. The company's CES 2026 booth at the Venetian Expo Halls A-D January 6-9, 2026 generated direct pre-orders on the show floor and earned the Microsoft AI Innovation Award for applied Azure-backed pet-care AI.

PETKIT's competitive moat is system-level integration: cross-device data flows between water fountain hydration logs, feeder portion records, and litter-box behavior signals create a single longitudinal pet-health record that single-product competitors cannot match. The YUMSHARE DAILY FEAST was named CNET Best of CES 2026 finalist in the Pet Tech category and won the Future Innovation Awards. PETKIT does not publicly disclose annual revenue, but the company holds a leading position based on installed base across mainland China and is positioned for accelerated expansion into the US, Japan, and EU through 2026.

Market Key Players:

TRACTIVE GMBH

RADIO SYSTEMS CORPORATION (PETSAFE)

GARMIN LTD.

PETKIT

HALO COLLAR

FURBO (TOMOFUN)

PETCUBE INC.

FI SMART COLLAR

SURE PETCARE (ANTELLIQ, MERCK ANIMAL HEALTH)

PETLIBRO

FITBARK INC.

PETPACE

WHISKER (LITTER-ROBOT)

ENABOT

DOGNESS

WAGZ

MARS, INCORPORATED (FORMER WHISTLE)

GOPRO INC.

MOTOROLA SOLUTIONS

TRAINI

ELECOM CO., LTD.

Others

Drivers

Rising Pet Ownership and Humanization of Pets

The increasing global pet population and the growing trend of treating pets as family members are significantly driving demand for smart pet care technologies. Pet owners are increasingly investing in intelligent devices such as smart feeders, GPS trackers, health monitoring wearables, interactive cameras, and connected pet care systems to improve animal health, safety, and overall well-being.

Higher disposable incomes, growing expenditure on premium pet care products, and rising awareness regarding preventive pet healthcare are further supporting the widespread adoption of smart pet technologies across residential households.

Growing Adoption of Connected and Digital Pet Care Solutions

Consumers are increasingly embracing connected devices that enable remote pet monitoring, automated feeding, activity tracking, and real-time health insights through smartphone applications. Smart pet care technologies offer convenience while helping owners maintain continuous interaction with their pets even when away from home.

Advancements in Internet of Things (IoT), artificial intelligence, cloud computing, wearable sensors, and mobile connectivity are enhancing the functionality, accuracy, and reliability of next-generation pet care devices.

Restraints

High Product Costs and Limited Consumer Awareness

Smart pet care devices equipped with advanced sensors, artificial intelligence capabilities, cloud connectivity, and integrated software often carry premium pricing compared to traditional pet accessories. Cost-sensitive consumers may hesitate to adopt connected pet technologies despite their long-term benefits.

Limited awareness regarding the capabilities of intelligent pet monitoring solutions in developing regions also restricts broader market penetration.

Data Privacy and Device Reliability Concerns

Connected pet care systems continuously collect location, behavioral, and health-related information, raising concerns regarding cybersecurity, cloud data protection, and user privacy. Manufacturers must ensure secure communication and data management to build consumer confidence.

Battery life, wireless connectivity, device durability, waterproofing, and sensor accuracy remain important technical challenges for wearable pet devices used in diverse environments.

Trends

Integration of Artificial Intelligence and Predictive Pet Healthcare

Artificial intelligence is increasingly transforming pet care by enabling predictive health monitoring, behavioral analysis, nutrition recommendations, activity optimization, and early disease detection. AI-powered algorithms continuously analyze biometric and behavioral data to provide personalized pet wellness insights.

Veterinary professionals and pet owners are increasingly utilizing intelligent monitoring platforms to improve preventive care and support long-term animal health management.

Expansion of Connected Pet Ecosystems

Smart pet devices are becoming integrated with mobile applications, cloud-based veterinary platforms, wearable ecosystems, smart homes, and digital healthcare services. These connected ecosystems enable seamless monitoring of feeding schedules, physical activity, medication reminders, and location tracking.

Advancements in Internet of Things (IoT), GPS technology, cloud analytics, Bluetooth connectivity, and digital pet healthcare platforms are enhancing user experience while strengthening pet safety and wellness management.

Opportunities

Increasing Demand for Remote Pet Monitoring Solutions

Growing urbanization, busy lifestyles, and increasing numbers of working pet owners are creating significant opportunities for remote pet monitoring technologies. Consumers are seeking intelligent solutions that enable continuous interaction, automated feeding, real-time alerts, and health monitoring while pets remain unattended at home.

The expansion of tele-veterinary services, digital pet insurance, and preventive veterinary care is expected to further accelerate adoption of connected pet technologies.

Innovation in Next-Generation Smart Pet Technologies

Rapid advancements in artificial intelligence, wearable biosensors, cloud computing, computer vision, smart collars, GPS tracking, biometric monitoring, and IoT connectivity are creating opportunities for next-generation pet care platforms capable of delivering comprehensive health management and intelligent behavioral analysis.

Increasing collaboration among pet technology companies, veterinary healthcare providers, consumer electronics manufacturers, software developers, artificial intelligence firms, wearable technology companies, and smart home solution providers is accelerating innovation across the connected pet care ecosystem. Continued advancements in AI-powered health analytics, intelligent feeding systems, GPS-enabled safety monitoring, cloud-based veterinary platforms, IoT-enabled pet wearables, digital wellness applications, and predictive animal healthcare technologies are expected to position smart pet care technology as a key component of future companion animal healthcare and connected lifestyle ecosystems worldwide.

Investment & M&A Activity

The smart pet care technology market recorded approximately USD 0.62 Billion in disclosed M&A and funding activity over the trailing 12 months ending April 2026, reflecting consolidation among GPS-and-wellness providers and venture-backed expansion in AI-driven behavioral analytics. Capital concentration remains in the Series B-and-later wearables tier, while seed and Series A activity is migrating toward AI behavior models and insurance-distribution platforms.

On July 28, 2025, Pasching-based Tractive closed its purchase of Whistle from Mars Petcare, taking ownership of the connected-pet wearable brand and migrating Whistle subscribers onto its platform with the legacy Whistle service ending August 31, 2025. The financial terms were not publicly disclosed, but Mars had originally bought Whistle in April 2016 for approximately USD 117 Million per industry coverage. The transaction reinforces Tractive's US footprint and brings resting heart-rate and respiratory-rate monitoring into the merged subscriber base.

In late December 2025, Palo Alto-based Traini secured USD 7.5 Million in strategic funding to commercialize its Cognitive Smart Collar, a generative-AI device built on the company's Valence-Arousal model and trained against more than 900 peer-reviewed animal-behavior studies and 2 million dog datasets. The round was disclosed on December 29, 2025. Halo Collar, with revenue progression from USD 75 Million in 2024 toward a projected USD 100 Million in 2025 and a USD 400 Million Series B valuation, signals that GPS-fence pure-plays continue to attract growth-stage capital. Petwealth emerged from stealth with USD 1.7 Million in seed funding through 2026, focused on functional pet-health platforms.

Recent Developments

April 2026 | Tractive GmbH

On April 8, 2026, Tractive introduced the DOG 6 XL collar tracker for larger breeds and the CAT 6 Mini, the first collar-integrated GPS and health tracker engineered for cats. The April refresh layered AI-generated weekly wellness digests, scratch-pattern detection, and feline-tuned cardiac and breathing-rate analytics across the company's 175-country footprint.

Strategic Impact: The cat-specific hardware closes a gap that GPS-and-health competitors have left underserved and validates the post-Whistle product-roadmap acceleration.

March 2026 | Pilo (Dreame Technology)

During March 27, 2026, Pilo officially debuted under Dreame's wider smart-home parent, building smart feeding, health monitoring, hardware, software, services, and a unified pet-care platform. The launch positions a major consumer-tech conglomerate against PETKIT in the Asia Pacific smart pet care technology market.

Strategic Impact: Capital-rich consumer-electronics entrants raise competitive pressure on smaller startups and validate pet care as a serious smart-home extension category.

January 2026 | PETKIT

During CES 2026 in Las Vegas from January 6-9, 2026, PETKIT introduced its three-product AI lineup for everyday pet care at booth #56342, comprising EVERSWEET ULTRA water fountain, YUMSHARE DAILY FEAST robotic wet-food feeder, and PUROBOT CRYSTAL DUO open-top automatic cat litter box. PETKIT earned the Microsoft AI Innovation Award and was named CNET Best of CES 2026 finalist in the Pet Tech category.

Strategic Impact: System-level integration across feeders, fountains, and litter robots establishes a pet-health-data flywheel that single-product competitors cannot match.

October 2025 | DEFRA (UK Regulator)

From October 1, 2025, the United Kingdom intensified enforcement of the Microchipping of Cats and Dogs (England) Regulations 2023 across England, Wales, Scotland, and Northern Ireland. Penalties for unmicrochipped dogs and cats reached GBP 500, supported by random checks at dog parks, events, and pet-related incident sites.

Strategic Impact: Regulator enforcement converted microchip-gated feeders, doors, and identification readers from optional purchases into compliance-driven hardware demand.

September 2025 | Halo Collar

During September 2025, Halo unveiled Halo Collar 5 with AlwaysOn GPS location tracking, 20 GPS updates per second, on-board AI signal processing, dual-chip Wi-Fi-Bluetooth design, and battery life extending to 48 hours per charge. The Halo Health module delivered daily activity insights through a refreshed Halo app.

Strategic Impact: Halo's transition from a pure containment product into combined containment-plus-health monitoring narrows the feature gap with Tractive and Fi at retail price points.

July 2025 | Tractive (Whistle Acquisition)

On July 28, 2025, Tractive closed its purchase of Whistle from Mars Petcare in Pasching, Austria and Seattle, taking ownership of the connected pet wearable brand. Whistle subscribers were offered transition to the Tractive platform; the legacy Whistle service ended August 31, 2025.

Strategic Impact: Consolidation among the two original pet-tracker pioneers reinforces Tractive's US footprint and establishes the highest combined-active-user count in the smart pet care technology market.

Frequently Asked Questions

How big is the Smart Pet Care Technology Market?

The Global Smart Pet Care Technology Market was valued at USD 14.34 Billion in 2024 and USD 16.20 Billion in 2025, and is projected to reach USD 48.66 Billion by 2034, growing at a CAGR of 13.0% from 2026 to 2034. Market growth is driven by AI-powered pet care solutions, IoT-enabled devices, and connected pet health technologies.

Who are the major players in the Smart Pet Care Technology Market?

Which segments covered the Smart Pet Care Technology Market?

By Product Type, (Smart Pet Feeders, Smart Pet Trackers, Smart Pet Cameras, Others), By Pet Type, (Dogs, Cats, Other Pets, Others), By Technology, (Artificial Intelligence (AI), Internet of Things (IoT), GPS & RFID, Others), By Application, (Health Monitoring, Feeding & Nutrition, Tracking & Safety, Others), By End-User, (Pet Owners, Veterinary Clinics, Pet Care Centers, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, By Pet Type (Dogs, Cats, Others), By Technology (Artificial Intelligence - AI, IoT, GPS & RFID), By Application (Health Monitoring, Feeding, Tracking & Safety), By End-User (Pet Owners, Vet Clinics) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Tech Trends & Forecast 2026-2034")

, By Pet Type (Dogs, Cats, Others), By Technology (Artificial Intelligence - AI, IoT, GPS & RFID), By Application (Health Monitoring, Feeding, Tracking & Safety), By End-User (Pet Owners, Vet Clinics) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Tech Trends & Forecast 2026-2034")

, By Pet Type (Dogs, Cats, Others), By Technology (Artificial Intelligence - AI, IoT, GPS & RFID), By Application (Health Monitoring, Feeding, Tracking & Safety), By End-User (Pet Owners, Vet Clinics) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Tech Trends & Forecast 2026-2034")

, By Pet Type (Dogs, Cats, Others), By Technology (Artificial Intelligence - AI, IoT, GPS & RFID), By Application (Health Monitoring, Feeding, Tracking & Safety), By End-User (Pet Owners, Vet Clinics) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Tech Trends & Forecast 2026-2034")