- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Smart Pill Technology Market Size, Share & Forecast | CAGR 13.4%

Global Smart Pill Technology Market Size, Share, Growth Analysis By Product Type (Capsule Endoscopy Systems, Patient Monitoring Smart Pills, Drug Delivery Smart Capsules), By Application (Small Bowel Diagnosis, Colon Cancer Screening, Gastric Disease Evaluation, Drug Delivery, Physiological Monitoring), By Target Area (Small Bowel, Colon, Esophagus, Stomach), By End-User, Industry Trends & Forecast 2026-2034

Report Overview

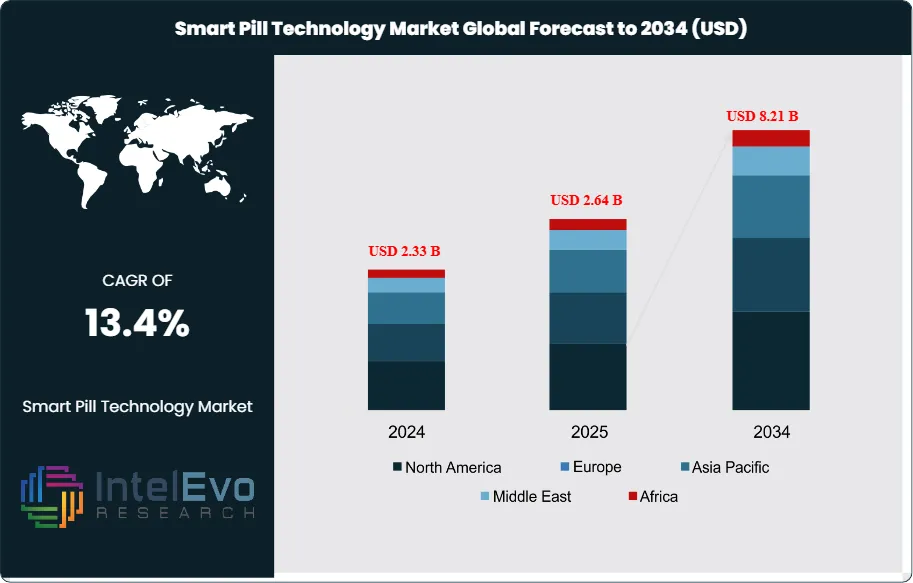

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

| USD 2.64 Billion | USD 8.21 Billion | 13.4% | North America, 41.3% |

The Smart Pill Technology Market was valued at approximately USD 2.33 Billion in 2024 and reached USD 2.64 Billion in 2025. The market is projected to grow to USD 8.21 Billion by 2034, expanding at a CAGR of 13.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 5.57 Billion over the analysis period, reflecting the clinical maturation of ingestible sensor platforms, capsule endoscopy expansion into small bowel and colon applications, and the growing deployment of drug delivery smart capsules in targeted gastrointestinal therapies.

Get More Information about this report -

Request Free Sample ReportThe smart pill technology market encompasses three distinct product categories that share a common ingestible form factor: capsule endoscopy systems for gastrointestinal visualization, patient monitoring smart pills that transmit physiological data from within the digestive tract, and targeted drug delivery capsules that release payloads at specified anatomical locations or in response to biological triggers. Capsule endoscopy remains the commercially dominant category in 2025, with an installed base exceeding 40 million capsules administered cumulatively since the technology's FDA clearance in 2001. Medtronic's PillCam platform, following its acquisition of Given Imaging, retains the leading position by procedure volume, while Olympus, CapsoVision, and IntroMedic compete across regional markets.

Regulatory signals shaping the smart pill technology market have become more favorable through 2025. The FDA has issued targeted guidance on ingestible sensors under the digital health framework, establishing predictable review pathways for new-generation devices that combine sensing, imaging, and wireless transmission within a single capsule. The CMS has maintained stable reimbursement coverage for capsule endoscopy procedures under CPT codes 91110, 91111, and 91113, with the 2025 physician fee schedule preserving approximately USD 1,220 in average per-procedure facility reimbursement for small bowel capsule endoscopy. European MDR compliance has become mandatory for all new smart pill devices marketed in the EU, adding approximately 18 to 24 months to product launch timelines but reinforcing market positions of established vendors with mature regulatory documentation.

Technology convergence is reshaping the smart pill technology market through the integration of AI-powered image analysis, miniaturized wireless transmission, and biodegradable electronics. AI-based reading of capsule endoscopy video, with FDA-cleared platforms from Medtronic, Olympus, and AI Medical Service reducing radiologist review time from 40 to 60 minutes per study to under 15 minutes, is a key productivity enabler for procedure volume expansion. The approval of colon capsule endoscopy as an alternative to optical colonoscopy for selected patient populations across the EU and within specific US pilots expands the addressable procedure volume materially. Drug delivery capsules from Progenity, Celero Systems, and Rani Therapeutics are advancing through clinical development, targeting orally administered biologics and location-specific GI drug release with regulatory submissions anticipated between 2026 and 2029.

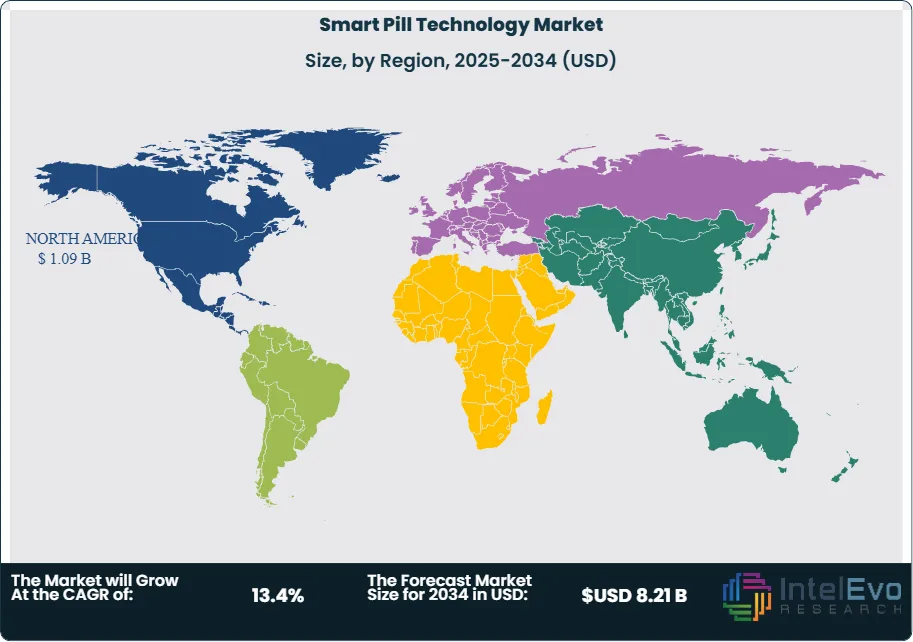

North America leads the smart pill technology market at 41.3% share in 2025, supported by established gastroenterology practice patterns, CMS reimbursement depth, and domestic clinical AI adoption. Europe retains a strong secondary position at 28.7% with Germany and the UK anchoring regional demand. Asia Pacific, particularly Japan and China, is the fastest-growing region due to high gastric cancer screening prevalence and expanding capsule endoscopy coverage within national insurance frameworks. The smart pill technology market trajectory through 2034 will be shaped by the commercialization of oral biologics delivery capsules, the expansion of colon capsule endoscopy into asymptomatic screening populations, and the integration of AI-powered diagnostic workflows that materially improve gastroenterologist productivity.

, By Application (Small Bowel Diagnosis, Colon Cancer Screening, Gastric Disease Evaluation, Drug Delivery, Physiological Monitoring), By Target Area (Small Bowel, Colon, Esophagus, Stomach), By End-User, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global smart pill technology market was valued at USD 2.64 Billion in 2025 and is projected to reach USD 8.21 Billion by 2034, expanding at a CAGR of 13.4% during the 2025–2034 forecast period.

- Segment Dominance: By product type, capsule endoscopy leads with approximately 68.4% market share in 2025, equivalent to USD 1.81 Billion, driven by established reimbursement coverage and expanding colon capsule endoscopy indications.

- Segment Dominance: By application, small bowel disease diagnosis represents the largest application segment with 42.7% market share in 2025, supported by capsule endoscopy's role as the gold standard for obscure gastrointestinal bleeding and Crohn's disease assessment.

- Driver: Global colorectal cancer incidence reaching 1.93 million new cases in 2025 and the shift toward non-invasive screening modalities is driving capsule endoscopy adoption, with colon capsule procedure volumes growing at 17.2% annually.

- Restraint: High per-procedure capsule cost of USD 500 to USD 800 plus facility fees restricts patient access in emerging markets and creates reimbursement tension in universal healthcare systems facing budget constraints.

- Opportunity: Oral biologics delivery capsules present an addressable opportunity of USD 2.4 Billion within the smart pill technology market by 2034, as the RaniPill, SOMA, and LUMI platforms progress through pivotal clinical trials targeting GLP-1, insulin, and monoclonal antibody oral delivery.

- Trend: AI-powered automated reading of capsule endoscopy video has reached 54% adoption among US gastroenterology practices performing capsule endoscopy in 2025, reducing review time by over 70% and transforming procedure throughput economics.

- Regional Analysis: North America leads the smart pill technology market with 41.3% share in 2025, equivalent to USD 1.09 Billion in annual revenue, driven by CMS reimbursement, gastroenterology practice density, and AI reading platform adoption.

Competitive Landscape Overview

The smart pill technology market is moderately consolidated, with the top four providers, Medtronic, Olympus, CapsoVision, and Check-Cap, collectively holding approximately 71% combined market share in 2025. Competition is primarily clinical-evidence-driven and reimbursement-gated, with FDA clearance depth, peer-reviewed sensitivity and specificity data, and CMS coding coverage serving as primary procurement criteria. Medtronic's PillCam platform retains clear procedure volume leadership, while emerging drug delivery and ingestible sensor specialists including Rani Therapeutics, Celero Systems, and Novartis-backed Lyndra Therapeutics are building platform positions ahead of anticipated commercial launches. M&A activity has remained moderate, with strategic investment flows from pharmaceutical companies into oral biologics delivery platforms representing the most consequential recent capital deployment.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Medtronic plc | Ireland/USA | Leader | PillCam SB 3 / Colon 2 | North America, Europe | FDA clearance for PillCam Genius AI reading platform, Mar 2025 |

| Olympus Corporation | Japan | Leader | EndoCapsule 10 System | Asia Pacific, Europe | Launched Endo-AID Capsule AI reading module in EU, Jun 2025 |

| CapsoVision, Inc. | USA | Leader | CapsoCam Plus (360°) | North America | Received expanded FDA indication for pediatric use, Feb 2025 |

| Check-Cap Ltd. | Israel | Challenger | C-Scan Prep-less Colon | Global (dev stage) | Restructured operations with renewed focus on C-Scan 3, Apr 2025 |

| Rani Therapeutics | USA | Challenger | RaniPill HC / RT-111 | North America, Asia Pacific | Completed Phase 1 RT-111 (IL-23 oral) in psoriasis, Q3 2025 |

| IntroMedic Co., Ltd. | South Korea | Niche Player | MiroCam MC2000 | Asia Pacific | Launched MiroCam Colon with extended battery, Aug 2025 |

| Celero Systems | USA | Niche Player | CoreMedic Vital Sensor | North America | Published JAMA study on opioid overdose detection, May 2025 |

| Proteus Digital Health (OTSUKA) | USA/Japan | Niche Player | Ingestible Event Marker | North America, Japan | Relaunched digital ingestion platform under Otsuka, Jan 2025 |

By Product Type

The smart pill technology market by product type divides into capsule endoscopy systems, patient monitoring smart pills, and drug delivery smart capsules. Capsule endoscopy leads with 68.4% share in 2025, generating USD 1.81 Billion in annual revenue, anchored by established procedural workflows in gastroenterology, comprehensive CMS reimbursement coverage under stable CPT codes, and a global installed capsule base exceeding 40 million cumulative procedures. Within capsule endoscopy, small bowel capsules account for the largest sub-category, while colon capsules represent the fastest-growing configuration as alternative-to-colonoscopy indications expand. Patient monitoring smart pills account for 18.2% share at USD 0.48 Billion, encompassing ingestible sensors that measure core body temperature, gastrointestinal pH, pressure, and transit time. Applications include athletic physiology monitoring, inflammatory bowel disease management, and emerging overdose detection research pioneered by Celero Systems. Drug delivery smart capsules represent 13.4% share at USD 0.35 Billion in 2025, with the majority of current revenue attributed to research use and early commercial programs. The drug delivery sub-segment carries the highest long-term growth potential, with oral biologics delivery representing a transformative market expansion opportunity as RaniPill, SOMA, and LUMI platforms progress toward pivotal trials and regulatory submissions over 2026–2029. Commercial maturation of oral biologics delivery could increase the drug delivery sub-segment share to 28% or higher by 2034.

By Application

The smart pill technology market by application spans small bowel disease diagnosis, colon cancer screening, esophageal disease assessment, gastric disease evaluation, drug delivery, and patient physiological monitoring. Small bowel disease diagnosis leads with 42.7% share in 2025 at USD 1.13 Billion, encompassing obscure gastrointestinal bleeding, Crohn's disease assessment, small bowel tumor detection, and celiac disease monitoring. Capsule endoscopy remains the clinical gold standard for small bowel visualization given the anatomical limitations of flexible endoscopy in this region. Colon cancer screening accounts for 22.8% share at USD 0.60 Billion and is the fastest-growing application at 17.2% CAGR, driven by colon capsule endoscopy's role as an alternative for patients unable or unwilling to undergo optical colonoscopy. Esophageal disease assessment represents 11.3% share at USD 0.30 Billion, primarily in Barrett's esophagus surveillance. Gastric disease evaluation accounts for 8.9% share at USD 0.23 Billion. Drug delivery applications hold 9.4% share at USD 0.25 Billion, while patient physiological monitoring accounts for 4.9% share at USD 0.13 Billion.

By Target Area

The smart pill technology market by target area divides by anatomical location of primary use: small bowel, colon, esophagus, stomach, and systemic applications. Small bowel applications dominate at 47.6% share in 2025 at USD 1.26 Billion, reflecting the clinical primacy of capsule endoscopy for small bowel indications where traditional endoscopy cannot reach effectively. Colon applications account for 26.2% share at USD 0.69 Billion and are growing most rapidly due to colon capsule endoscopy expansion. Esophageal applications represent 12.4% share at USD 0.33 Billion, with PillCam ESO 3 and competitor systems targeting Barrett's esophagus screening in high-volume primary care settings where referral to traditional endoscopy creates friction. Gastric applications hold 8.5% share at USD 0.22 Billion. Systemic applications, where ingested smart pills transmit data or deliver drugs that affect systemic physiology rather than targeting specific GI anatomical segments, account for 5.3% share at USD 0.14 Billion. The systemic applications category is expected to grow fastest among target areas through 2034 as oral biologics delivery capsules reach commercial launch.

By End-User

The smart pill technology market by end-user spans hospitals and health systems, ambulatory surgery centers and gastroenterology clinics, research institutions, and home-use settings. Hospitals and health systems lead with 51.3% share in 2025 at USD 1.35 Billion, reflecting the procedural infrastructure required for capsule preparation, data retrieval, and physician interpretation. Ambulatory surgery centers and dedicated gastroenterology clinics account for 34.7% share at USD 0.92 Billion, with US gastroenterology practice consolidation into large multi-site groups such as GI Alliance and United Digestive driving enterprise-scale capsule endoscopy procurement. Research institutions hold 8.6% share at USD 0.23 Billion, supporting clinical development of drug delivery platforms and investigational sensing applications. Home-use and decentralized settings represent 5.4% share at USD 0.14 Billion, an emerging category enabled by direct-to-consumer capsule ingestion workflows paired with remote monitoring services, particularly relevant for patient-administered colon capsule screening programs.

Regional Analysis

North America

North America dominates the smart pill technology market with 41.3% share in 2025, equivalent to USD 1.09 Billion in annual revenue. The United States accounts for approximately 93% of the regional total at USD 1.02 Billion, underpinned by CMS reimbursement under CPT codes 91110, 91111, and 91113, gastroenterology practice density exceeding 15,000 practicing physicians, and the consolidation of gastroenterology practices under national groups that standardize capsule endoscopy procurement. The FDA Digital Health Center of Excellence has established clear regulatory pathways for ingestible sensors, with 2025 clearance activity reflecting expanded approvals for AI-reading platforms and pediatric indications. Domestic innovation concentration is notable: Medtronic, CapsoVision, Rani Therapeutics, Celero Systems, and Proteus Digital Health (now under Otsuka) all operate primary R&D operations in North America. Canada contributes approximately USD 0.06 Billion, with adoption concentrated in university teaching hospitals and growing coverage under provincial health authorities such as Ontario Health. Mexico represents a smaller USD 0.02 Billion market, with private gastroenterology practices in Mexico City, Monterrey, and Guadalajara leading adoption. Clinical AI integration is accelerating materially, with 54% of US capsule endoscopy procedures in 2025 utilizing AI-assisted reading platforms, reducing physician interpretation time from 40-60 minutes to under 15 minutes per study and fundamentally improving the procedural economics that had previously constrained throughput.

Europe

Europe accounts for 28.7% of the global smart pill technology market in 2025, generating USD 0.76 Billion in annual revenue. Germany leads the European market at an estimated USD 0.21 Billion, driven by comprehensive statutory health insurance coverage under G-BA assessment, a dense gastroenterology practice network, and strong clinical research output from academic centers including the University Hospital Erlangen. The United Kingdom follows at USD 0.17 Billion, where NHS England's introduction of colon capsule endoscopy as an alternative to optical colonoscopy during and after the COVID-19 backlog recovery materially expanded procedure volumes, with over 240,000 colon capsule procedures performed cumulatively through 2025. France contributes approximately USD 0.12 Billion, supported by Sécurité Sociale coverage and Groupement Hospitalier de Territoire procurement at scale. Italy accounts for approximately USD 0.09 Billion with strong gastroenterology research positioning. EU Medical Device Regulation (MDR) compliance is now mandatory across the region, which has added approximately 18 to 24 months to product registration timelines but reinforced the market positions of established vendors with documented clinical evidence. The European Society of Gastrointestinal Endoscopy has issued updated guidelines in 2024 expanding the recommended indications for capsule endoscopy, contributing to procedure volume growth. The region is projected to grow at 12.1% CAGR through 2034.

Asia Pacific

Asia Pacific represents 22.6% of the smart pill technology market in 2025 at USD 0.60 Billion and is projected at a CAGR of 15.8% through 2034, among the highest across all regions. Japan is the largest country market in the region at an estimated USD 0.22 Billion, supported by the world's highest per-capita gastric cancer screening volume, broad PMDA clearance of both domestic (Olympus EndoCapsule) and imported capsule endoscopy systems, and national health insurance coverage that establishes predictable procedure reimbursement. Japan's aging demographics and strong cultural acceptance of preventive screening sustain structural demand growth. China contributes approximately USD 0.18 Billion, with the National Medical Products Administration having approved multiple domestic capsule endoscopy manufacturers including JinShan Science & Technology and Ankon Technologies, whose magnetically controlled capsule gastroscopy systems have found strong adoption in gastric cancer screening programs. India is the third-largest country market at approximately USD 0.09 Billion, growing at an estimated 18.3% CAGR as private hospital chains including Apollo Hospitals, Fortis, and Max Healthcare expand capsule endoscopy programs. South Korea at approximately USD 0.07 Billion is home to IntroMedic, whose MiroCam platform competes in domestic and export markets. Australia and Southeast Asian markets are expanding with growing coverage from private insurance schemes and public health system integration in Singapore and Thailand.

Latin America

Latin America accounts for 4.6% of the global smart pill technology market in 2025 at USD 0.12 Billion, representing a nascent but accelerating adoption environment. Brazil leads the region at an estimated USD 0.06 Billion, with Hospital Israelita Albert Einstein, Hospital Sírio-Libanês, and Rede D'Or São Luiz operating as flagship capsule endoscopy centers. ANVISA regulatory pathways for capsule endoscopy have matured, supporting broader vendor access across the Brazilian market. The Brazilian Federation of Gastroenterology has issued updated clinical guidelines referencing capsule endoscopy for specific indications, stabilizing clinical practice uptake. Mexico contributes approximately USD 0.03 Billion, with private hospital groups Grupo Angeles and ABC Medical Center driving adoption. Argentina accounts for approximately USD 0.02 Billion, supported by private healthcare coverage through companies such as OSDE and Swiss Medical. Coverage limitations under public health systems, currency volatility affecting imported device pricing, and capsule device costs of USD 500 to USD 800 per procedure constrain broad population access, maintaining the region at the smaller end of global market share. The region is projected to grow at a CAGR of 14.1% through 2034 as private healthcare penetration deepens and domestic regulatory pathways continue to streamline.

Middle East and Africa

The Middle East and Africa region represents 2.8% of the smart pill technology market in 2025, generating USD 0.07 Billion in annual revenue. The UAE is the dominant market at approximately USD 0.03 Billion, anchored by Cleveland Clinic Abu Dhabi, Sheikh Khalifa Medical City, and American Hospital Dubai operating advanced gastroenterology programs with full capsule endoscopy capability. The UAE Ministry of Health has integrated capsule endoscopy coverage within public sector health insurance for Emirati nationals and broad private sector coverage for expatriate populations. Saudi Arabia follows at approximately USD 0.02 Billion, with King Faisal Specialist Hospital and Johns Hopkins Aramco Healthcare operating high-volume gastroenterology services. Vision 2030 health sector transformation has driven expanded procurement of advanced diagnostic technologies including capsule endoscopy through the National Unified Procurement Company. South Africa accounts for approximately USD 0.01 Billion, serving as the primary Sub-Saharan deployment hub with Netcare and Mediclinic private hospital groups leading adoption. Israel, which is the home country of Given Imaging (acquired by Medtronic) and several emerging ingestible sensor companies, maintains notable clinical adoption and research concentration. The MEA region is projected to grow at a CAGR of 14.6% through 2034, supported by sovereign wealth fund investment in healthcare infrastructure and continued referral pattern maturation in gastroenterology practice.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Capsule Endoscopy Systems

- Patient Monitoring Smart Pills

- Drug Delivery Smart Capsules

By Application

- Small Bowel Disease Diagnosis

- Colon Cancer Screening

- Esophageal Disease Assessment

- Gastric Disease Evaluation

- Drug Delivery Applications

- Patient Physiological Monitoring

By Target Area

- Small Bowel

- Colon

- Esophagus

- Stomach

- Systemic Applications

By End-User

- Hospitals and Health Systems

- Ambulatory Surgery Centers and Gastroenterology Clinics

- Research Institutions

- Home-Use / Decentralized Settings

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.64 B |

| Forecast Revenue (2034) | USD 8.21 B |

| CAGR (2025-2034) | 13.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Capsule Endoscopy Systems, Patient Monitoring Smart Pills, Drug Delivery Smart Capsules), By Application, (Small Bowel Disease Diagnosis, Colon Cancer Screening, Esophageal Disease Assessment, Gastric Disease Evaluation, Drug Delivery Applications, Patient Physiological Monitoring), By Target (Area, Small Bowel, Colon, Esophagus, Stomach, Systemic Applications), By End-User, (Hospitals and Health Systems, Ambulatory Surgery Centers and Gastroenterology Clinics, Research Institutions, Home-Use / Decentralized Settings) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MEDTRONIC PLC, OLYMPUS CORPORATION, CAPSOVISION, INC., CHECK-CAP LTD., RANI THERAPEUTICS HOLDINGS, INC., INTROMEDIC CO., LTD., CELERO SYSTEMS, INC., OTSUKA PHARMACEUTICAL (PROTEUS DIGITAL HEALTH), LYNDRA THERAPEUTICS, INC., JINSHAN SCIENCE & TECHNOLOGY CO., LTD., ANKON TECHNOLOGIES CO., LTD., BDD LIMITED, MEDIMETRICS PERSONALIZED DRUG DELIVERY, ETECTRX, INC., HQ MEDICAL KOREA LTD., AI MEDICAL SERVICE, INC., CELPATH INTERNATIONAL GMBH, COVIDIEN (MEDTRONIC), ENDIATX, INC., NOVAGATE SURGICAL, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Small Bowel Diagnosis, Colon Cancer Screening, Gastric Disease Evaluation, Drug Delivery, Physiological Monitoring), By Target Area (Small Bowel, Colon, Esophagus, Stomach), By End-User, Industry Trends & Forecast 2026-2034")

, By Application (Small Bowel Diagnosis, Colon Cancer Screening, Gastric Disease Evaluation, Drug Delivery, Physiological Monitoring), By Target Area (Small Bowel, Colon, Esophagus, Stomach), By End-User, Industry Trends & Forecast 2026-2034")

, By Application (Small Bowel Diagnosis, Colon Cancer Screening, Gastric Disease Evaluation, Drug Delivery, Physiological Monitoring), By Target Area (Small Bowel, Colon, Esophagus, Stomach), By End-User, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Smart Pill Technology Market?

The Global Smart Pill Technology Market was valued at USD 2.33 Billion in 2024 and is projected to reach USD 8.21 Billion by 2034, growing at a CAGR of 13.4% from 2026 to 2034, driven by rising demand for minimally invasive diagnostics, increasing adoption of capsule endoscopy, advancements in digital health technologies, and growing focus on remote patient monitoring and precision medicine.

Who are the major players in the Smart Pill Technology Market?

MEDTRONIC PLC, OLYMPUS CORPORATION, CAPSOVISION, INC., CHECK-CAP LTD., RANI THERAPEUTICS HOLDINGS, INC., INTROMEDIC CO., LTD., CELERO SYSTEMS, INC., OTSUKA PHARMACEUTICAL (PROTEUS DIGITAL HEALTH), LYNDRA THERAPEUTICS, INC., JINSHAN SCIENCE & TECHNOLOGY CO., LTD., ANKON TECHNOLOGIES CO., LTD., BDD LIMITED, MEDIMETRICS PERSONALIZED DRUG DELIVERY, ETECTRX, INC., HQ MEDICAL KOREA LTD., AI MEDICAL SERVICE, INC., CELPATH INTERNATIONAL GMBH, COVIDIEN (MEDTRONIC), ENDIATX, INC., NOVAGATE SURGICAL, Others

Which segments covered the Smart Pill Technology Market?

By Product Type, (Capsule Endoscopy Systems, Patient Monitoring Smart Pills, Drug Delivery Smart Capsules), By Application, (Small Bowel Disease Diagnosis, Colon Cancer Screening, Esophageal Disease Assessment, Gastric Disease Evaluation, Drug Delivery Applications, Patient Physiological Monitoring), By Target (Area, Small Bowel, Colon, Esophagus, Stomach, Systemic Applications), By End-User, (Hospitals and Health Systems, Ambulatory Surgery Centers and Gastroenterology Clinics, Research Institutions, Home-Use / Decentralized Settings)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Smart Pill Technology Market

Published Date : 18 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date